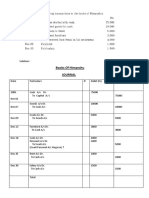

Journal Entries: Date Particular Debit Credit

Journal Entries: Date Particular Debit Credit

You might also like

- Instant Download Ebook PDF Ethics in Marketing International Cases and Perspectives 2nd Edition PDF ScribdDocument29 pagesInstant Download Ebook PDF Ethics in Marketing International Cases and Perspectives 2nd Edition PDF Scribdchester.whelan111100% (52)

- Watson Answering ServiceDocument3 pagesWatson Answering Servicemohitgaba1967% (6)

- 2811501Document12 pages2811501mohitgaba19100% (1)

- Tugas SessionDocument4 pagesTugas SessionJoko Budiman100% (1)

- No. Debits NoDocument11 pagesNo. Debits Nomohitgaba19100% (1)

- Jennys FroyoDocument16 pagesJennys FroyoKailash Kumar100% (2)

- Oracle Project AccountingDocument13 pagesOracle Project Accountingmohanivar77100% (2)

- Lean Six Sigma Black Belt Body of Knowledge PDFDocument11 pagesLean Six Sigma Black Belt Body of Knowledge PDFblack betty0% (1)

- ACCT 6010 Assignment #1Document15 pagesACCT 6010 Assignment #1patel avaniNo ratings yet

- FINANCE AssignmentDocument8 pagesFINANCE AssignmentpranaviNo ratings yet

- Unadjusted Trial BalanceDocument10 pagesUnadjusted Trial BalanceMingxNo ratings yet

- 22i 2763Document3 pages22i 2763i222763 Asma JavaidNo ratings yet

- UntitledDocument3 pagesUntitledi222763 Asma JavaidNo ratings yet

- Accounts Case Study 78Document4 pagesAccounts Case Study 78Vraj AdrojaNo ratings yet

- FA Book ProblemDocument8 pagesFA Book ProblemPhuntru PhiNo ratings yet

- 10 Full Questions Till Closing Account BSSE (2A)Document33 pages10 Full Questions Till Closing Account BSSE (2A)Should Should100% (2)

- EEA UNIT 4 - AccountingDocument57 pagesEEA UNIT 4 - AccountingJayanth GudimellaNo ratings yet

- Journal Problems For AssignmentDocument2 pagesJournal Problems For AssignmentMD. Arif HossainNo ratings yet

- Sports HavenDocument3 pagesSports HavenKailash Kumar100% (1)

- Cash A/C Amount ($) Amount ($)Document12 pagesCash A/C Amount ($) Amount ($)Bhagath VarenyaNo ratings yet

- Week-116 Apr SolutionsDocument2 pagesWeek-116 Apr SolutionsHaya DanishNo ratings yet

- Jawaban Latihan SoalDocument31 pagesJawaban Latihan SoalRizalMawardiNo ratings yet

- Determining Difference in Net Profit Under Cash BasisDocument5 pagesDetermining Difference in Net Profit Under Cash Basisagrawalrohit_228384No ratings yet

- Financial & Managerial Accounting - JunXianDocument5 pagesFinancial & Managerial Accounting - JunXianhashtagjxNo ratings yet

- KP ProblemDocument14 pagesKP ProblemTanveer Ali ShahNo ratings yet

- Practical 1Document31 pagesPractical 1Rohit ReddyNo ratings yet

- Name: Nguyen Thi Tien Tien: InstructionsDocument20 pagesName: Nguyen Thi Tien Tien: InstructionsChery Tiên TiênNo ratings yet

- Question A: Adjusting Entries in The Books of G Inc. Adjusting Journal Entries Sr. No. Particulars/Accounts Title Debit $ Credit $Document7 pagesQuestion A: Adjusting Entries in The Books of G Inc. Adjusting Journal Entries Sr. No. Particulars/Accounts Title Debit $ Credit $Talha Iftekhar KhanNo ratings yet

- Service Business Accounting CycleDocument6 pagesService Business Accounting CycleMarie Kairish Damag Vivar100% (1)

- Dey's Solution Book Accountancy XII Part-A 2021-22 EditionDocument56 pagesDey's Solution Book Accountancy XII Part-A 2021-22 Editionmanoj jainNo ratings yet

- Books of Himanshu JournalDocument4 pagesBooks of Himanshu Journalrakesh19865No ratings yet

- CH1 AssignmentDocument11 pagesCH1 AssignmentDhence BasigaNo ratings yet

- Maria Case - 19 AugDocument12 pagesMaria Case - 19 AugKartikey BharadwajNo ratings yet

- Principles of Accounting: Name: Muhammad Hasnain Shakir Enrolment No: 01-111192-145 Section: BBA4 - 2ADocument3 pagesPrinciples of Accounting: Name: Muhammad Hasnain Shakir Enrolment No: 01-111192-145 Section: BBA4 - 2AOsman Bin SaifNo ratings yet

- Shelsy - 2142003 Tugas Pe 2-7a - PR 3-5BDocument5 pagesShelsy - 2142003 Tugas Pe 2-7a - PR 3-5BShelsy syNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- PcdepotDocument21 pagesPcdepotWidi HartonoNo ratings yet

- Unit 2 Tutorial Worksheet AnswersDocument15 pagesUnit 2 Tutorial Worksheet AnswersHhvvgg BbbbNo ratings yet

- Accounts Case Study 3-3Document10 pagesAccounts Case Study 3-3monudinuNo ratings yet

- Salma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Document6 pagesSalma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Salma BarkahNo ratings yet

- Accounting ProjectDocument36 pagesAccounting ProjectNin QetelauriNo ratings yet

- Abdulla YounisDocument4 pagesAbdulla Younisashwani singhaniaNo ratings yet

- PA-HW Chap3 + 4Document8 pagesPA-HW Chap3 + 4Hà Anh ĐỗNo ratings yet

- 02 - GROUP Soì Ì 1 - TEST GROUP NO.1Document15 pages02 - GROUP Soì Ì 1 - TEST GROUP NO.1My NguyenNo ratings yet

- Practice - Journalizing and Posting-1Document24 pagesPractice - Journalizing and Posting-1Ahmed P. FatehNo ratings yet

- Acc. - Assignment - 2Document15 pagesAcc. - Assignment - 2Tanvir RohanNo ratings yet

- Accounting Question-With AnswerDocument5 pagesAccounting Question-With AnswerApanar OoNo ratings yet

- Journal Entries in The Books of MNM Co. Date Particulars Debit Rs. Credit RsDocument3 pagesJournal Entries in The Books of MNM Co. Date Particulars Debit Rs. Credit RsMitesh GalaNo ratings yet

- Journal Entry Answers 30 Aug 22Document2 pagesJournal Entry Answers 30 Aug 22WarrioropNo ratings yet

- P 4 4 A Vang Management ServicesDocument1 pageP 4 4 A Vang Management ServicesJanice KusnandarNo ratings yet

- 6 DesemberDocument8 pages6 DesemberKezia N. ApriliaNo ratings yet

- Journal Entries Groupings AccountingDocument3 pagesJournal Entries Groupings AccountingGerlyn Mae Delantar100% (1)

- Excercises Chapter 4Document5 pagesExcercises Chapter 4Mar ChahinNo ratings yet

- Pai 2Document20 pagesPai 2ARCNo ratings yet

- Accounting AssignmentDocument10 pagesAccounting AssignmentKotha SarkerNo ratings yet

- Chapter 5Document13 pagesChapter 5Derrick de los ReyesNo ratings yet

- Accounting Cycle Excel Template 2Document11 pagesAccounting Cycle Excel Template 2Islam SamirNo ratings yet

- 3 - Trial Balance To PL Account - ExamplesDocument49 pages3 - Trial Balance To PL Account - ExamplesDivyansh Pandey100% (2)

- Assignment-4 and 8Document15 pagesAssignment-4 and 8Carla Sader0% (1)

- HW 4Document4 pagesHW 4Mishalm96No ratings yet

- ET - Yes Bank-DHFL Scam Accused To Be Tried by PMLA Court, Says Bombay HCDocument11 pagesET - Yes Bank-DHFL Scam Accused To Be Tried by PMLA Court, Says Bombay HCHarshit SinglaNo ratings yet

- ET - BFSI YES Bank-DHFL Case Timeline When and How It HappenedDocument12 pagesET - BFSI YES Bank-DHFL Case Timeline When and How It HappenedHarshit SinglaNo ratings yet

- HT - CBI Moves SC To Quiz Ex-Police Commissioner Rajeev KumarDocument13 pagesHT - CBI Moves SC To Quiz Ex-Police Commissioner Rajeev KumarHarshit SinglaNo ratings yet

- HT - Rana Kapoor Used YES Bank For Illegal Activities, Says EDDocument14 pagesHT - Rana Kapoor Used YES Bank For Illegal Activities, Says EDHarshit SinglaNo ratings yet

- BS - Mallya Bought Properties in England, France While Airline in CrisisDocument4 pagesBS - Mallya Bought Properties in England, France While Airline in CrisisHarshit SinglaNo ratings yet

- ET - Vijay Mallya Asks Govt To Accept Loan Repayment Offer, Close Case Against HimDocument8 pagesET - Vijay Mallya Asks Govt To Accept Loan Repayment Offer, Close Case Against HimHarshit SinglaNo ratings yet

- HT - Vijay Mallya Requests Banks With Folded Hands' To Take 100 Per Cent of Principal Money BackDocument11 pagesHT - Vijay Mallya Requests Banks With Folded Hands' To Take 100 Per Cent of Principal Money BackHarshit SinglaNo ratings yet

- National Colloqium - Pre Budget Session 2023Document2 pagesNational Colloqium - Pre Budget Session 2023Harshit SinglaNo ratings yet

- Wipro TechnologiesDocument5 pagesWipro TechnologiesHarshit SinglaNo ratings yet

- National Colloquium Pre-Budget Expectation 2023 (10 Jan)Document2 pagesNational Colloquium Pre-Budget Expectation 2023 (10 Jan)Harshit SinglaNo ratings yet

- Creative EnergyDocument28 pagesCreative EnergyHarshit SinglaNo ratings yet

- MGT 212 AssignmentDocument5 pagesMGT 212 AssignmentTamzid Islam SanvyNo ratings yet

- Chapter 6 Ethiopian Financial MarketDocument30 pagesChapter 6 Ethiopian Financial Marketyebegashet87% (31)

- NCCB Securities and Financial Services LTD.: Portfolio StatementDocument1 pageNCCB Securities and Financial Services LTD.: Portfolio StatementAfsana TasnimNo ratings yet

- Chapter 1 Solution of RoboticsDocument4 pagesChapter 1 Solution of RoboticsEngr ShabirNo ratings yet

- Elegent Resume Design in Ms Word 2019Document3 pagesElegent Resume Design in Ms Word 2019Zubair khanNo ratings yet

- Journal EntriesDocument12 pagesJournal Entriesg81596262No ratings yet

- When Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityDocument4 pagesWhen Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityJonabelle BiliganNo ratings yet

- L1628-Precision Cut BrochureDocument2 pagesL1628-Precision Cut BrochureAndrade RodrigoNo ratings yet

- Rigid PVC Trouble-Shooting Guide For Twin Screw ExtrusionDocument3 pagesRigid PVC Trouble-Shooting Guide For Twin Screw Extrusionmacnoms50% (2)

- Lavish LawsuitDocument9 pagesLavish LawsuitLauren YoungNo ratings yet

- Chapter 2 Managerial Accounting PowerPointDocument42 pagesChapter 2 Managerial Accounting PowerPointOmar Bani-KhalafNo ratings yet

- 12th All Komatsu Indonesia Technical Olympic 2022 Official ResultDocument2 pages12th All Komatsu Indonesia Technical Olympic 2022 Official ResultMarchal KawengianNo ratings yet

- SITW School Bus UseDocument7 pagesSITW School Bus UseWTKR News 3No ratings yet

- Facebook Comment Volume PredictionDocument12 pagesFacebook Comment Volume PredictionVaraNo ratings yet

- Employment Income TaxDocument10 pagesEmployment Income TaxHarsh Nahar100% (1)

- Case Analysis - Natureview FarmDocument11 pagesCase Analysis - Natureview Farmayush singla100% (1)

- Milkiy FF 2011Document263 pagesMilkiy FF 2011Asfawosen Dingama100% (1)

- Blue ch04Document32 pagesBlue ch04Lokesh ShahareNo ratings yet

- Cattle Fattening Business PlanDocument5 pagesCattle Fattening Business PlanYossantos Solo100% (1)

- AFA Animal Production 9 Quarter 4 Module 7Document16 pagesAFA Animal Production 9 Quarter 4 Module 7Claes TrinioNo ratings yet

- HBO Syllabus 1Document9 pagesHBO Syllabus 1Json FranciscoNo ratings yet

- Comparative Financial Analysis Between Bangladesh and USADocument9 pagesComparative Financial Analysis Between Bangladesh and USAZiad Bin HashemNo ratings yet

- Reg 165-2014 Relevant For TACHOnetDocument3 pagesReg 165-2014 Relevant For TACHOnetperaNo ratings yet

- Mitsubishi Electric Low-Voltage Products PLM (Product Lifecycle Management)Document8 pagesMitsubishi Electric Low-Voltage Products PLM (Product Lifecycle Management)LUATNo ratings yet

- Human Resources: A Case Study of Must-Have HR Policies, Hypothetical Cases, Employment Legal Cases and Their Worst-Case AnalysisDocument10 pagesHuman Resources: A Case Study of Must-Have HR Policies, Hypothetical Cases, Employment Legal Cases and Their Worst-Case AnalysisArjun DNo ratings yet

- Business Plan For Poultry FarmingDocument7 pagesBusiness Plan For Poultry FarmingAbbas Samaila100% (1)

- Contract of Sale of GoodsDocument2 pagesContract of Sale of GoodsUmair Ali100% (1)

Download as docx, pdf, or txt

You might also like

- Instant Download Ebook PDF Ethics in Marketing International Cases and Perspectives 2nd Edition PDF ScribdDocument29 pagesInstant Download Ebook PDF Ethics in Marketing International Cases and Perspectives 2nd Edition PDF Scribdchester.whelan111100% (52)

- Watson Answering ServiceDocument3 pagesWatson Answering Servicemohitgaba1967% (6)

- 2811501Document12 pages2811501mohitgaba19100% (1)

- Tugas SessionDocument4 pagesTugas SessionJoko Budiman100% (1)

- No. Debits NoDocument11 pagesNo. Debits Nomohitgaba19100% (1)

- Jennys FroyoDocument16 pagesJennys FroyoKailash Kumar100% (2)

- Oracle Project AccountingDocument13 pagesOracle Project Accountingmohanivar77100% (2)

- Lean Six Sigma Black Belt Body of Knowledge PDFDocument11 pagesLean Six Sigma Black Belt Body of Knowledge PDFblack betty0% (1)

- ACCT 6010 Assignment #1Document15 pagesACCT 6010 Assignment #1patel avaniNo ratings yet

- FINANCE AssignmentDocument8 pagesFINANCE AssignmentpranaviNo ratings yet

- Unadjusted Trial BalanceDocument10 pagesUnadjusted Trial BalanceMingxNo ratings yet

- 22i 2763Document3 pages22i 2763i222763 Asma JavaidNo ratings yet

- UntitledDocument3 pagesUntitledi222763 Asma JavaidNo ratings yet

- Accounts Case Study 78Document4 pagesAccounts Case Study 78Vraj AdrojaNo ratings yet

- FA Book ProblemDocument8 pagesFA Book ProblemPhuntru PhiNo ratings yet

- 10 Full Questions Till Closing Account BSSE (2A)Document33 pages10 Full Questions Till Closing Account BSSE (2A)Should Should100% (2)

- EEA UNIT 4 - AccountingDocument57 pagesEEA UNIT 4 - AccountingJayanth GudimellaNo ratings yet

- Journal Problems For AssignmentDocument2 pagesJournal Problems For AssignmentMD. Arif HossainNo ratings yet

- Sports HavenDocument3 pagesSports HavenKailash Kumar100% (1)

- Cash A/C Amount ($) Amount ($)Document12 pagesCash A/C Amount ($) Amount ($)Bhagath VarenyaNo ratings yet

- Week-116 Apr SolutionsDocument2 pagesWeek-116 Apr SolutionsHaya DanishNo ratings yet

- Jawaban Latihan SoalDocument31 pagesJawaban Latihan SoalRizalMawardiNo ratings yet

- Determining Difference in Net Profit Under Cash BasisDocument5 pagesDetermining Difference in Net Profit Under Cash Basisagrawalrohit_228384No ratings yet

- Financial & Managerial Accounting - JunXianDocument5 pagesFinancial & Managerial Accounting - JunXianhashtagjxNo ratings yet

- KP ProblemDocument14 pagesKP ProblemTanveer Ali ShahNo ratings yet

- Practical 1Document31 pagesPractical 1Rohit ReddyNo ratings yet

- Name: Nguyen Thi Tien Tien: InstructionsDocument20 pagesName: Nguyen Thi Tien Tien: InstructionsChery Tiên TiênNo ratings yet

- Question A: Adjusting Entries in The Books of G Inc. Adjusting Journal Entries Sr. No. Particulars/Accounts Title Debit $ Credit $Document7 pagesQuestion A: Adjusting Entries in The Books of G Inc. Adjusting Journal Entries Sr. No. Particulars/Accounts Title Debit $ Credit $Talha Iftekhar KhanNo ratings yet

- Service Business Accounting CycleDocument6 pagesService Business Accounting CycleMarie Kairish Damag Vivar100% (1)

- Dey's Solution Book Accountancy XII Part-A 2021-22 EditionDocument56 pagesDey's Solution Book Accountancy XII Part-A 2021-22 Editionmanoj jainNo ratings yet

- Books of Himanshu JournalDocument4 pagesBooks of Himanshu Journalrakesh19865No ratings yet

- CH1 AssignmentDocument11 pagesCH1 AssignmentDhence BasigaNo ratings yet

- Maria Case - 19 AugDocument12 pagesMaria Case - 19 AugKartikey BharadwajNo ratings yet

- Principles of Accounting: Name: Muhammad Hasnain Shakir Enrolment No: 01-111192-145 Section: BBA4 - 2ADocument3 pagesPrinciples of Accounting: Name: Muhammad Hasnain Shakir Enrolment No: 01-111192-145 Section: BBA4 - 2AOsman Bin SaifNo ratings yet

- Shelsy - 2142003 Tugas Pe 2-7a - PR 3-5BDocument5 pagesShelsy - 2142003 Tugas Pe 2-7a - PR 3-5BShelsy syNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- PcdepotDocument21 pagesPcdepotWidi HartonoNo ratings yet

- Unit 2 Tutorial Worksheet AnswersDocument15 pagesUnit 2 Tutorial Worksheet AnswersHhvvgg BbbbNo ratings yet

- Accounts Case Study 3-3Document10 pagesAccounts Case Study 3-3monudinuNo ratings yet

- Salma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Document6 pagesSalma Barkah - Dasar Akuntansi - Latihan E2-9 & E2-10Salma BarkahNo ratings yet

- Accounting ProjectDocument36 pagesAccounting ProjectNin QetelauriNo ratings yet

- Abdulla YounisDocument4 pagesAbdulla Younisashwani singhaniaNo ratings yet

- PA-HW Chap3 + 4Document8 pagesPA-HW Chap3 + 4Hà Anh ĐỗNo ratings yet

- 02 - GROUP Soì Ì 1 - TEST GROUP NO.1Document15 pages02 - GROUP Soì Ì 1 - TEST GROUP NO.1My NguyenNo ratings yet

- Practice - Journalizing and Posting-1Document24 pagesPractice - Journalizing and Posting-1Ahmed P. FatehNo ratings yet

- Acc. - Assignment - 2Document15 pagesAcc. - Assignment - 2Tanvir RohanNo ratings yet

- Accounting Question-With AnswerDocument5 pagesAccounting Question-With AnswerApanar OoNo ratings yet

- Journal Entries in The Books of MNM Co. Date Particulars Debit Rs. Credit RsDocument3 pagesJournal Entries in The Books of MNM Co. Date Particulars Debit Rs. Credit RsMitesh GalaNo ratings yet

- Journal Entry Answers 30 Aug 22Document2 pagesJournal Entry Answers 30 Aug 22WarrioropNo ratings yet

- P 4 4 A Vang Management ServicesDocument1 pageP 4 4 A Vang Management ServicesJanice KusnandarNo ratings yet

- 6 DesemberDocument8 pages6 DesemberKezia N. ApriliaNo ratings yet

- Journal Entries Groupings AccountingDocument3 pagesJournal Entries Groupings AccountingGerlyn Mae Delantar100% (1)

- Excercises Chapter 4Document5 pagesExcercises Chapter 4Mar ChahinNo ratings yet

- Pai 2Document20 pagesPai 2ARCNo ratings yet

- Accounting AssignmentDocument10 pagesAccounting AssignmentKotha SarkerNo ratings yet

- Chapter 5Document13 pagesChapter 5Derrick de los ReyesNo ratings yet

- Accounting Cycle Excel Template 2Document11 pagesAccounting Cycle Excel Template 2Islam SamirNo ratings yet

- 3 - Trial Balance To PL Account - ExamplesDocument49 pages3 - Trial Balance To PL Account - ExamplesDivyansh Pandey100% (2)

- Assignment-4 and 8Document15 pagesAssignment-4 and 8Carla Sader0% (1)

- HW 4Document4 pagesHW 4Mishalm96No ratings yet

- ET - Yes Bank-DHFL Scam Accused To Be Tried by PMLA Court, Says Bombay HCDocument11 pagesET - Yes Bank-DHFL Scam Accused To Be Tried by PMLA Court, Says Bombay HCHarshit SinglaNo ratings yet

- ET - BFSI YES Bank-DHFL Case Timeline When and How It HappenedDocument12 pagesET - BFSI YES Bank-DHFL Case Timeline When and How It HappenedHarshit SinglaNo ratings yet

- HT - CBI Moves SC To Quiz Ex-Police Commissioner Rajeev KumarDocument13 pagesHT - CBI Moves SC To Quiz Ex-Police Commissioner Rajeev KumarHarshit SinglaNo ratings yet

- HT - Rana Kapoor Used YES Bank For Illegal Activities, Says EDDocument14 pagesHT - Rana Kapoor Used YES Bank For Illegal Activities, Says EDHarshit SinglaNo ratings yet

- BS - Mallya Bought Properties in England, France While Airline in CrisisDocument4 pagesBS - Mallya Bought Properties in England, France While Airline in CrisisHarshit SinglaNo ratings yet

- ET - Vijay Mallya Asks Govt To Accept Loan Repayment Offer, Close Case Against HimDocument8 pagesET - Vijay Mallya Asks Govt To Accept Loan Repayment Offer, Close Case Against HimHarshit SinglaNo ratings yet

- HT - Vijay Mallya Requests Banks With Folded Hands' To Take 100 Per Cent of Principal Money BackDocument11 pagesHT - Vijay Mallya Requests Banks With Folded Hands' To Take 100 Per Cent of Principal Money BackHarshit SinglaNo ratings yet

- National Colloqium - Pre Budget Session 2023Document2 pagesNational Colloqium - Pre Budget Session 2023Harshit SinglaNo ratings yet

- Wipro TechnologiesDocument5 pagesWipro TechnologiesHarshit SinglaNo ratings yet

- National Colloquium Pre-Budget Expectation 2023 (10 Jan)Document2 pagesNational Colloquium Pre-Budget Expectation 2023 (10 Jan)Harshit SinglaNo ratings yet

- Creative EnergyDocument28 pagesCreative EnergyHarshit SinglaNo ratings yet

- MGT 212 AssignmentDocument5 pagesMGT 212 AssignmentTamzid Islam SanvyNo ratings yet

- Chapter 6 Ethiopian Financial MarketDocument30 pagesChapter 6 Ethiopian Financial Marketyebegashet87% (31)

- NCCB Securities and Financial Services LTD.: Portfolio StatementDocument1 pageNCCB Securities and Financial Services LTD.: Portfolio StatementAfsana TasnimNo ratings yet

- Chapter 1 Solution of RoboticsDocument4 pagesChapter 1 Solution of RoboticsEngr ShabirNo ratings yet

- Elegent Resume Design in Ms Word 2019Document3 pagesElegent Resume Design in Ms Word 2019Zubair khanNo ratings yet

- Journal EntriesDocument12 pagesJournal Entriesg81596262No ratings yet

- When Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityDocument4 pagesWhen Is A Notice of Donation Needed?: NEDA - National Economic Development AuthorityJonabelle BiliganNo ratings yet

- L1628-Precision Cut BrochureDocument2 pagesL1628-Precision Cut BrochureAndrade RodrigoNo ratings yet

- Rigid PVC Trouble-Shooting Guide For Twin Screw ExtrusionDocument3 pagesRigid PVC Trouble-Shooting Guide For Twin Screw Extrusionmacnoms50% (2)

- Lavish LawsuitDocument9 pagesLavish LawsuitLauren YoungNo ratings yet

- Chapter 2 Managerial Accounting PowerPointDocument42 pagesChapter 2 Managerial Accounting PowerPointOmar Bani-KhalafNo ratings yet

- 12th All Komatsu Indonesia Technical Olympic 2022 Official ResultDocument2 pages12th All Komatsu Indonesia Technical Olympic 2022 Official ResultMarchal KawengianNo ratings yet

- SITW School Bus UseDocument7 pagesSITW School Bus UseWTKR News 3No ratings yet

- Facebook Comment Volume PredictionDocument12 pagesFacebook Comment Volume PredictionVaraNo ratings yet

- Employment Income TaxDocument10 pagesEmployment Income TaxHarsh Nahar100% (1)

- Case Analysis - Natureview FarmDocument11 pagesCase Analysis - Natureview Farmayush singla100% (1)

- Milkiy FF 2011Document263 pagesMilkiy FF 2011Asfawosen Dingama100% (1)

- Blue ch04Document32 pagesBlue ch04Lokesh ShahareNo ratings yet

- Cattle Fattening Business PlanDocument5 pagesCattle Fattening Business PlanYossantos Solo100% (1)

- AFA Animal Production 9 Quarter 4 Module 7Document16 pagesAFA Animal Production 9 Quarter 4 Module 7Claes TrinioNo ratings yet

- HBO Syllabus 1Document9 pagesHBO Syllabus 1Json FranciscoNo ratings yet

- Comparative Financial Analysis Between Bangladesh and USADocument9 pagesComparative Financial Analysis Between Bangladesh and USAZiad Bin HashemNo ratings yet

- Reg 165-2014 Relevant For TACHOnetDocument3 pagesReg 165-2014 Relevant For TACHOnetperaNo ratings yet

- Mitsubishi Electric Low-Voltage Products PLM (Product Lifecycle Management)Document8 pagesMitsubishi Electric Low-Voltage Products PLM (Product Lifecycle Management)LUATNo ratings yet

- Human Resources: A Case Study of Must-Have HR Policies, Hypothetical Cases, Employment Legal Cases and Their Worst-Case AnalysisDocument10 pagesHuman Resources: A Case Study of Must-Have HR Policies, Hypothetical Cases, Employment Legal Cases and Their Worst-Case AnalysisArjun DNo ratings yet

- Business Plan For Poultry FarmingDocument7 pagesBusiness Plan For Poultry FarmingAbbas Samaila100% (1)

- Contract of Sale of GoodsDocument2 pagesContract of Sale of GoodsUmair Ali100% (1)