Download as docx, pdf, or txt

You might also like

- Government Accounting SyllabusDocument12 pagesGovernment Accounting SyllabusJean Diane JoveloNo ratings yet

- Chapter 12Document11 pagesChapter 12Kim Patrice NavarraNo ratings yet

- Interview NotesDocument134 pagesInterview NotesJerrico GomezNo ratings yet

- Introduction To Industry 4.0 and Industrial IoT Week 2 Quiz SolutionsDocument5 pagesIntroduction To Industry 4.0 and Industrial IoT Week 2 Quiz Solutionssathya100% (1)

- Lesson 3 - Fundamentals of Income Taxation PDFDocument9 pagesLesson 3 - Fundamentals of Income Taxation PDFErika ApitaNo ratings yet

- Chapter 10Document5 pagesChapter 10여자라라No ratings yet

- Chapter 8 Regular Income Tax - Exclusion From Gross IncomeDocument2 pagesChapter 8 Regular Income Tax - Exclusion From Gross IncomeJason MablesNo ratings yet

- Capital Gains TaxationDocument44 pagesCapital Gains TaxationPrince Anton DomondonNo ratings yet

- Chapter 10 Compensation IncomeDocument4 pagesChapter 10 Compensation IncomeJason MablesNo ratings yet

- Intax Test BankDocument2 pagesIntax Test BankMitchie FaustinoNo ratings yet

- Chap. 6 8Document44 pagesChap. 6 82vpsrsmg7jNo ratings yet

- Chapter 7 - Intro To Regular Income Taxation (RIT)Document5 pagesChapter 7 - Intro To Regular Income Taxation (RIT)claritaquijano526No ratings yet

- Chapter 4 v4Document18 pagesChapter 4 v4Sheilamae Sernadilla GregorioNo ratings yet

- Chapter 1 5 Income Tax MCDocument14 pagesChapter 1 5 Income Tax MCNoella Marie BaronNo ratings yet

- Lesson 2: Income Tax Schemes, Accounting Periods, Methods and ReportingDocument28 pagesLesson 2: Income Tax Schemes, Accounting Periods, Methods and ReportingCJ GranadaNo ratings yet

- Title Viii Corporate Books and Records: I. LimitationsDocument12 pagesTitle Viii Corporate Books and Records: I. LimitationsRengeline LucasNo ratings yet

- CPA Review School of The Philippines Manila First Pre-Board Solutions TaxationDocument8 pagesCPA Review School of The Philippines Manila First Pre-Board Solutions TaxationLive LoveNo ratings yet

- Income Tax Computation For Corporate TaxpayersDocument79 pagesIncome Tax Computation For Corporate TaxpayersPATATASNo ratings yet

- Mansci - Chapter 3Document2 pagesMansci - Chapter 3Rae WorksNo ratings yet

- PFRS of SME and SE - Concept MapDocument1 pagePFRS of SME and SE - Concept MapRey OñateNo ratings yet

- Tax Chapter 10, 11, 12Document13 pagesTax Chapter 10, 11, 12Sheraldine MendozaNo ratings yet

- CHAPTER 6 Final Income Taxation (Module)Document14 pagesCHAPTER 6 Final Income Taxation (Module)Shane Mark CabiasaNo ratings yet

- Chapter 5 Final Income TaxationDocument26 pagesChapter 5 Final Income TaxationJason MablesNo ratings yet

- 93-09 - Capital AssetsDocument8 pages93-09 - Capital AssetsJuan Miguel UngsodNo ratings yet

- Definition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeDocument13 pagesDefinition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeSKEETER BRITNEY COSTANo ratings yet

- Accounting For Income Tax: Technical KnowledgeDocument42 pagesAccounting For Income Tax: Technical KnowledgeAngela Miles DizonNo ratings yet

- Finals Government Accounting: Petty Cash FundDocument4 pagesFinals Government Accounting: Petty Cash FundRafael Capunpon VallejosNo ratings yet

- Chapter 3 Corporate Liquidation and Reorganization-PROFE01Document3 pagesChapter 3 Corporate Liquidation and Reorganization-PROFE01Steffany RoqueNo ratings yet

- Taxation Sia/Tabag TAX.2812-Accounting Methods MAY 2020: Lecture NotesDocument2 pagesTaxation Sia/Tabag TAX.2812-Accounting Methods MAY 2020: Lecture NotesMay Grethel Joy PeranteNo ratings yet

- Intermediate Accounting 3 - January 24, 2023, F2F DiscussionDocument8 pagesIntermediate Accounting 3 - January 24, 2023, F2F DiscussionZhaira Kim CantosNo ratings yet

- Ia1 5a Investments 15 FVDocument55 pagesIa1 5a Investments 15 FVJm SevallaNo ratings yet

- PFRS 12 Disclosures of Interest in Other EntitiesDocument32 pagesPFRS 12 Disclosures of Interest in Other EntitiesRenge TañaNo ratings yet

- Break-Even Analysis: Cost-Volume-Profit AnalysisDocument64 pagesBreak-Even Analysis: Cost-Volume-Profit AnalysisKelvin LeongNo ratings yet

- Pas 12Document2 pagesPas 12JennicaBailonNo ratings yet

- 93-04 - Partnership TaxDocument8 pages93-04 - Partnership TaxJuan Miguel UngsodNo ratings yet

- MULTIPLE CHOICE: Choose The Best AnswerDocument3 pagesMULTIPLE CHOICE: Choose The Best AnswerEppie SeverinoNo ratings yet

- True or FalseDocument76 pagesTrue or FalsepangytpangytNo ratings yet

- Exclusions and Inclusions - MANTUANODocument8 pagesExclusions and Inclusions - MANTUANODonita MantuanoNo ratings yet

- IT Audit WorkbookDocument52 pagesIT Audit Workbookgeraldjohn.mondejarNo ratings yet

- CPA Dreams Test BankDocument6 pagesCPA Dreams Test BankMayla MasxcxlNo ratings yet

- Local Taxation and Real Property Taxation-SummaryDocument1 pageLocal Taxation and Real Property Taxation-SummaryErika Mae Legaspi100% (1)

- Cost Accounting Reviewer Chapter 1-4Document10 pagesCost Accounting Reviewer Chapter 1-4hanaNo ratings yet

- INTGR TAX 005 Compensation IncomeDocument5 pagesINTGR TAX 005 Compensation IncomeZatsumono YamamotoNo ratings yet

- Income Taxation: Prelims-ReviewerDocument3 pagesIncome Taxation: Prelims-ReviewerFely Maata100% (1)

- Gratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: AnDocument5 pagesGratuitous Define As Given or Done With Free Charge. Inofficious Contrary To Moral Obligation, As The Disinheritance of A Child by His Parents: Ankristine torresNo ratings yet

- Group 2 Exclusion From Gross IncomeDocument32 pagesGroup 2 Exclusion From Gross IncomeMaryrose MalaluanNo ratings yet

- Government Accounting Defined (Section 109 of PD 1445)Document7 pagesGovernment Accounting Defined (Section 109 of PD 1445)Harley GumaponNo ratings yet

- Introduction To Audit Services and Financial Statements AuditDocument35 pagesIntroduction To Audit Services and Financial Statements AuditBryzan Dela CruzNo ratings yet

- Statement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTDocument21 pagesStatement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTRuaya AilynNo ratings yet

- Lesson 5 Income Tax On CorporationDocument20 pagesLesson 5 Income Tax On CorporationReino CabitacNo ratings yet

- Chapter 6 To Chapter 8Document4 pagesChapter 6 To Chapter 8Jarren BasilanNo ratings yet

- Chapter 3 Introduction To Income TaxationDocument38 pagesChapter 3 Introduction To Income TaxationPearlyn Villarin100% (1)

- Afar 1 - TheoriesDocument1 pageAfar 1 - TheoriesAngela Miles DizonNo ratings yet

- Intermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesDocument7 pagesIntermediate Accounting 2 Week 1 Lecture AY 2020-2021 Chapter 1: Current LiabilitiesdeeznutsNo ratings yet

- Introduction To Financial Statement AuditDocument28 pagesIntroduction To Financial Statement AuditJnn CycNo ratings yet

- Chap 10-14: Compensation IncomeDocument44 pagesChap 10-14: Compensation IncomeArna Kaira Kjell DiestraNo ratings yet

- Chapter 5 Final Income TaxationDocument2 pagesChapter 5 Final Income TaxationBisag AsaNo ratings yet

- Taxation CH 5Document6 pagesTaxation CH 5Kristel Nuyda LobasNo ratings yet

- Chapter 9 Other Percentage TaxesDocument56 pagesChapter 9 Other Percentage TaxesKarylle BartolayNo ratings yet

- Quiz in Intacc 1 & 2 (Finals)Document1 pageQuiz in Intacc 1 & 2 (Finals)Sandra100% (1)

- Part IV 2 Exclusion and Inclusion Regular Income TaxationDocument11 pagesPart IV 2 Exclusion and Inclusion Regular Income Taxationmary jhoyNo ratings yet

- OCT. 3 Long QuizDocument4 pagesOCT. 3 Long QuizAudrianna EliseNo ratings yet

- Regular Income Tax: Inclusions in Gross IncomeDocument10 pagesRegular Income Tax: Inclusions in Gross IncomeAngelica PagaduanNo ratings yet

- Measuring Success of Accounting Informat PDFDocument10 pagesMeasuring Success of Accounting Informat PDFJean Diane JoveloNo ratings yet

- Literacy On The Fundamental Information PDFDocument14 pagesLiteracy On The Fundamental Information PDFJean Diane JoveloNo ratings yet

- The Impact of Cost of Capital On Financi PDFDocument238 pagesThe Impact of Cost of Capital On Financi PDFJean Diane JoveloNo ratings yet

- Knowledge Impact On Information Quality PDFDocument12 pagesKnowledge Impact On Information Quality PDFJean Diane JoveloNo ratings yet

- The 3rd AAGBS International Conference oDocument46 pagesThe 3rd AAGBS International Conference oJean Diane JoveloNo ratings yet

- Habit and Hedonic Motivation Are The STRDocument18 pagesHabit and Hedonic Motivation Are The STRJean Diane JoveloNo ratings yet

- Incorporating Multidimensional Images in PDFDocument18 pagesIncorporating Multidimensional Images in PDFJean Diane JoveloNo ratings yet

- Introducing The Approach To Unwell Child PDFDocument128 pagesIntroducing The Approach To Unwell Child PDFJean Diane JoveloNo ratings yet

- The Role of Accounting Information SysteDocument17 pagesThe Role of Accounting Information SysteJean Diane JoveloNo ratings yet

- The Effect of Social Media On Hotel InduDocument141 pagesThe Effect of Social Media On Hotel InduJean Diane JoveloNo ratings yet

- The Effectiveness of Learning Design ModDocument172 pagesThe Effectiveness of Learning Design ModJean Diane JoveloNo ratings yet

- Government BenefitsDocument2 pagesGovernment BenefitsJean Diane JoveloNo ratings yet

- Agency Action Plan-SECDocument4 pagesAgency Action Plan-SECJean Diane JoveloNo ratings yet

- European Journal of Human Resource ManagDocument27 pagesEuropean Journal of Human Resource ManagJean Diane JoveloNo ratings yet

- In Partial Fulfillment of The Requirements in Marketing ManagementDocument26 pagesIn Partial Fulfillment of The Requirements in Marketing ManagementJean Diane JoveloNo ratings yet

- 3rd Pharmacoeconomics and Outcomes ReseaDocument54 pages3rd Pharmacoeconomics and Outcomes ReseaJean Diane JoveloNo ratings yet

- GR12 Business Finance Module 9-10Document7 pagesGR12 Business Finance Module 9-10Jean Diane JoveloNo ratings yet

- GR12 Business Finance Module 7-8Document10 pagesGR12 Business Finance Module 7-8Jean Diane JoveloNo ratings yet

- GR12 Business Finance Module 1-2Document7 pagesGR12 Business Finance Module 1-2Jean Diane JoveloNo ratings yet

- GR12 Business Finance Module 3-4Document8 pagesGR12 Business Finance Module 3-4Jean Diane JoveloNo ratings yet

- GR12 Business Finance Module 5-6Document10 pagesGR12 Business Finance Module 5-6Jean Diane JoveloNo ratings yet

- Streat VibesDocument78 pagesStreat VibesJean Diane JoveloNo ratings yet

- THE HOUSE OF NUTS FEASIB Revision Part 1Document49 pagesTHE HOUSE OF NUTS FEASIB Revision Part 1Jean Diane JoveloNo ratings yet

- Chapter1 201212072034Document10 pagesChapter1 201212072034Jean Diane JoveloNo ratings yet

- Summary of Comments of Sir EdDocument4 pagesSummary of Comments of Sir EdJean Diane JoveloNo ratings yet

- THE HOUSE OF NUTS FEASIB Revision Part 1finalDocument51 pagesTHE HOUSE OF NUTS FEASIB Revision Part 1finalJean Diane JoveloNo ratings yet

- Sponsorship Letter For 1st Webinar 26 Nov 2020Document1 pageSponsorship Letter For 1st Webinar 26 Nov 2020Jean Diane JoveloNo ratings yet

- Business Plan 12 HarveyDocument11 pagesBusiness Plan 12 HarveyKhrystelle BarrionNo ratings yet

- Indent Form For Purchase of Stores: From To Managing Director Hartron ChandigarhDocument4 pagesIndent Form For Purchase of Stores: From To Managing Director Hartron ChandigarhMonzieAirNo ratings yet

- 200+ Public VC FirmsDocument43 pages200+ Public VC FirmsrowieNo ratings yet

- Application Letter Sample For Fresh Graduate AccountingDocument8 pagesApplication Letter Sample For Fresh Graduate AccountinghlizshggfNo ratings yet

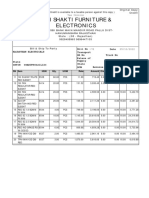

- Shri Shakti Furniture & Electronics: Credit OrginalDocument1 pageShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNo ratings yet

- Cloze TestDocument2 pagesCloze TestDuje GlavinaNo ratings yet

- Nuqui - Quiz On Special JournalsDocument25 pagesNuqui - Quiz On Special JournalsJesther NuquiNo ratings yet

- Castrol Oil - Consumer Behavior of in Pune CityDocument47 pagesCastrol Oil - Consumer Behavior of in Pune CitySohel Bangi100% (1)

- Outline ReportDocument11 pagesOutline ReportYt HuongNo ratings yet

- Mphasis Campus Hiring 2022: 3 MessagesDocument2 pagesMphasis Campus Hiring 2022: 3 MessagesNaveenNo ratings yet

- Agni Iconic 2078-79Document11 pagesAgni Iconic 2078-79sital chandNo ratings yet

- 04 Accounting For Service BusinessDocument37 pages04 Accounting For Service Businesscarlo bundalian100% (1)

- Applications of It in Business: Final ReportDocument13 pagesApplications of It in Business: Final ReportWarda TariqNo ratings yet

- L6M2 External Report Jan 21Document1 pageL6M2 External Report Jan 21KEVIN OKINDANo ratings yet

- Long Thanh CorporationDocument14 pagesLong Thanh Corporation70 CentilitersNo ratings yet

- Plastic Waste ManagementDocument9 pagesPlastic Waste ManagementlaurenjiaNo ratings yet

- NH73034207108458 Finance InvoiceDocument1 pageNH73034207108458 Finance InvoiceNaresh kumarNo ratings yet

- Clearing House Regulations October 2022 - ENDocument36 pagesClearing House Regulations October 2022 - ENnaufan fadhilaNo ratings yet

- PLO 1a: Our Graduates Will Be Able To Identify The Business Problem in A Given SituationDocument4 pagesPLO 1a: Our Graduates Will Be Able To Identify The Business Problem in A Given SituationMEENA J RCBSNo ratings yet

- Problem Set 2: FIN 401: Financial Management Syed Waqar AhmedDocument3 pagesProblem Set 2: FIN 401: Financial Management Syed Waqar AhmedJiteshNo ratings yet

- Ott V Theatre: Anticipating Trends Post PandemicDocument10 pagesOtt V Theatre: Anticipating Trends Post PandemicNitish unniNo ratings yet

- PRI of OdishaDocument52 pagesPRI of OdishaSnehashree SahooNo ratings yet

- Meyer Sound Acheron Designer QuoteDocument2 pagesMeyer Sound Acheron Designer QuoteJasmine WilsonNo ratings yet

- Journal of The Asia Pacific Economy: Psychographic Segmentation of Indian Urban ConsumersDocument24 pagesJournal of The Asia Pacific Economy: Psychographic Segmentation of Indian Urban ConsumersNhi Nguyễn Lê ĐôngNo ratings yet

- End Term - Corporate FinanceDocument3 pagesEnd Term - Corporate FinanceDEBAPRIYA SARKARNo ratings yet

- Co-Branding:: Bayerische Motoren Werke AG BMWDocument3 pagesCo-Branding:: Bayerische Motoren Werke AG BMWdaniyalNo ratings yet

- Manifestación de 15 Minutos ReviewDocument4 pagesManifestación de 15 Minutos ReviewCarlos AlmeidaNo ratings yet

- Lista Fontes e Cabos Reparos 10.2023Document4 pagesLista Fontes e Cabos Reparos 10.2023amsacessorios00No ratings yet