Download as docx, pdf, or txt

You might also like

- Target Market Project: Itsbobatime Sharetea Simplici-TeaDocument55 pagesTarget Market Project: Itsbobatime Sharetea Simplici-TeaKristia AnagapNo ratings yet

- Lecture Notes Corporate Income TaxDocument25 pagesLecture Notes Corporate Income TaxAU SLNo ratings yet

- Multiple Choice INTXDocument1 pageMultiple Choice INTXSophia KeratinNo ratings yet

- Business Cup Level 1 Quiz BeeDocument28 pagesBusiness Cup Level 1 Quiz BeeRowellPaneloSalapareNo ratings yet

- How To Choose An Exit StrategyDocument5 pagesHow To Choose An Exit StrategySayaga GlobalindoNo ratings yet

- Prob 2Document1 pageProb 2Mitch Tokong MinglanaNo ratings yet

- Accounting For Special TransactionsDocument1 pageAccounting For Special TransactionsKc SevillaNo ratings yet

- Partnership DissolutionDocument3 pagesPartnership DissolutionRoselyn Balik100% (1)

- Partnership DissolutionDocument7 pagesPartnership DissolutionAngel Frolen B. RacinezNo ratings yet

- Illustrative Examples - Accounting For Income TaxDocument3 pagesIllustrative Examples - Accounting For Income Taxr3rvpaudit.nfjpia2324supaccNo ratings yet

- Solution: Merlin, Capital Withdrawal 2,600,000 Property 500,000 900,000 1,200,000Document19 pagesSolution: Merlin, Capital Withdrawal 2,600,000 Property 500,000 900,000 1,200,000MJ NuarinNo ratings yet

- 03 - Partnership DissolutionDocument38 pages03 - Partnership DissolutionDonise Ronadel SantosNo ratings yet

- Liabilities: B-ACTG214 SY2019-2020 de La Salle University - DasmariñasDocument158 pagesLiabilities: B-ACTG214 SY2019-2020 de La Salle University - DasmariñasErika Mae LegaspiNo ratings yet

- 1st Year ExamDocument9 pages1st Year ExamMark Domingo MendozaNo ratings yet

- Activity 1.1 PDFDocument2 pagesActivity 1.1 PDFDe Nev OelNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasAdrian RoxasNo ratings yet

- 7105 - Inventory Cost Flow and LCNRVDocument2 pages7105 - Inventory Cost Flow and LCNRVGerardo YadawonNo ratings yet

- Cash and Cash Equivalents 1Document15 pagesCash and Cash Equivalents 1Micko LagundinoNo ratings yet

- Module 3 - Partnership DissolutionDocument54 pagesModule 3 - Partnership DissolutionMaluDyNo ratings yet

- Distribution of Profits or Losses Based On Partner'sDocument20 pagesDistribution of Profits or Losses Based On Partner'sJOANNA ROSE MANALONo ratings yet

- Chapter 1 None CompressDocument9 pagesChapter 1 None CompressiadcNo ratings yet

- Maria Jasmine, Park PlaceDocument1 pageMaria Jasmine, Park PlaceRolyn EstevesNo ratings yet

- Acctg7-MIDTERM REVIERDocument9 pagesAcctg7-MIDTERM REVIERDave Manalo100% (1)

- ABM003 N5 CaneteDocument17 pagesABM003 N5 CaneteCriscel EstrellaNo ratings yet

- Partnership 2021 - Long ProblemsDocument5 pagesPartnership 2021 - Long ProblemsMichael MagdaogNo ratings yet

- CFAS.100 - Diagnostic Test Part 1Document4 pagesCFAS.100 - Diagnostic Test Part 1Mika MolinaNo ratings yet

- Midterm Exam Parcor 2020Document1 pageMidterm Exam Parcor 2020John Alfred CastinoNo ratings yet

- Pakam, Khiezna E. Bsac-1b Assignment 3-FarDocument5 pagesPakam, Khiezna E. Bsac-1b Assignment 3-FarKhiezna PakamNo ratings yet

- SOLMAN Chapter 7Document21 pagesSOLMAN Chapter 7Na JaeminNo ratings yet

- Parcor TrainingDocument12 pagesParcor TrainingKarl ExacNo ratings yet

- Chapter 18 TestbankDocument8 pagesChapter 18 TestbankBea GarciaNo ratings yet

- St. Vincent College of Cabuyao: Brgy. Mamatid, City of Cabuyao, Laguna Advance Financial Accounting and ReportingDocument3 pagesSt. Vincent College of Cabuyao: Brgy. Mamatid, City of Cabuyao, Laguna Advance Financial Accounting and ReportingGennelyn Grace Peñaredondo100% (1)

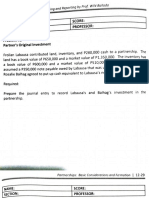

- Name:: Score: ProfessorDocument6 pagesName:: Score: ProfessorkakaoNo ratings yet

- Prefinal Review AcfarDocument8 pagesPrefinal Review AcfarBugoy CabasanNo ratings yet

- Partnership FormationDocument3 pagesPartnership Formationmiss independent100% (1)

- Chapter 5 - Corporation - Share TransactionsDocument14 pagesChapter 5 - Corporation - Share Transactionslou-924No ratings yet

- Retained EarningsDocument3 pagesRetained EarningsChristian Marvin VillanuevaNo ratings yet

- ACCTG 124 Chapter 7Document5 pagesACCTG 124 Chapter 7John Vincent A DioNo ratings yet

- Afar 2901 Diy PDFDocument1 pageAfar 2901 Diy PDFkngnhngNo ratings yet

- Sec Code of Corporate Governance AnswerDocument3 pagesSec Code of Corporate Governance AnswerHechel DatinguinooNo ratings yet

- This Study Resource Was: Problem IDocument8 pagesThis Study Resource Was: Problem IMs VampireNo ratings yet

- Comlaw Prequalifying SolManDocument10 pagesComlaw Prequalifying SolManAnj SueloNo ratings yet

- Re BVPS EpsDocument4 pagesRe BVPS EpsVeron BrionesNo ratings yet

- Key Quiz 2 2022 2023Document4 pagesKey Quiz 2 2022 2023Leslie Mae Vargas ZafeNo ratings yet

- PARCOR Quiz Chapter 6Document2 pagesPARCOR Quiz Chapter 6Angelica ShaneNo ratings yet

- Adjusting Entry - PrepaymentsDocument19 pagesAdjusting Entry - PrepaymentsShayne Aldrae CacaldaNo ratings yet

- Ppe Post TestDocument31 pagesPpe Post TestMarie MagallanesNo ratings yet

- AFAR-01 (Partnership Formation & Operations)Document6 pagesAFAR-01 (Partnership Formation & Operations)Nathalie Shien DagaragaNo ratings yet

- Identify The Choice That Best Completes The Statement or Answers The QuestionDocument6 pagesIdentify The Choice That Best Completes The Statement or Answers The QuestionAIENNA GABRIELLE FABRO100% (1)

- Pre Final JPIA Manual Membership Registration SystemDocument50 pagesPre Final JPIA Manual Membership Registration SystemEdita Lamp DizonNo ratings yet

- University of Mindanao Panabo CollegeDocument2 pagesUniversity of Mindanao Panabo CollegeJessa Beloy100% (1)

- Admission and Retirement of PartnersDocument3 pagesAdmission and Retirement of PartnersJohn Eric MacallaNo ratings yet

- MCQDocument3 pagesMCQPeng GuinNo ratings yet

- Cash Flow AssignmentDocument39 pagesCash Flow AssignmentMUHAMMAD HASSANNo ratings yet

- Chapter 4 - Partnership LiquidationDocument4 pagesChapter 4 - Partnership LiquidationMikaella BengcoNo ratings yet

- Comprehensive Problem Excel SpreadsheetDocument23 pagesComprehensive Problem Excel Spreadsheetapi-237864722100% (3)

- FAR2 Classwork PDFDocument7 pagesFAR2 Classwork PDFBarley ManilaNo ratings yet

- MC Partnership Answer KeyDocument23 pagesMC Partnership Answer KeyHNo ratings yet

- Chapter 7: Receivables: Principles of AccountingDocument50 pagesChapter 7: Receivables: Principles of AccountingRohail Javed100% (1)

- PrelimsDocument24 pagesPrelimsRhea BadanaNo ratings yet

- Ast PPT 1Document16 pagesAst PPT 1Thayen ZyrhieneNo ratings yet

- Accounting For Partnerships: Basic Considerations and FormationDocument22 pagesAccounting For Partnerships: Basic Considerations and FormationAj CapungganNo ratings yet

- Accounting For Partnerships: Basic Considerations and FormationDocument38 pagesAccounting For Partnerships: Basic Considerations and FormationRaihanah008100% (2)

- Notes Receivable DiscountingDocument33 pagesNotes Receivable DiscountingKristia AnagapNo ratings yet

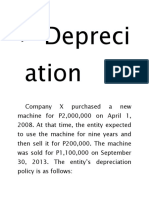

- Depreciation' NatureDocument21 pagesDepreciation' NatureKristia AnagapNo ratings yet

- Merchandising and InventoryDocument12 pagesMerchandising and InventoryKristia AnagapNo ratings yet

- Shareholders' EquityDocument18 pagesShareholders' EquityKristia AnagapNo ratings yet

- 1.0 The Rhetorical Situation: 1.1 ExigenceDocument6 pages1.0 The Rhetorical Situation: 1.1 ExigenceKristia AnagapNo ratings yet

- Liquidation by InstallmentDocument6 pagesLiquidation by InstallmentKristia AnagapNo ratings yet

- Bank ReconciliationDocument11 pagesBank ReconciliationKristia AnagapNo ratings yet

- IPCC (Intergovernmental Panel On Climate Change) : SpeechDocument2 pagesIPCC (Intergovernmental Panel On Climate Change) : SpeechKristia AnagapNo ratings yet

- Inventory Estimation: GP Method: 2 ProceduresDocument4 pagesInventory Estimation: GP Method: 2 ProceduresKristia AnagapNo ratings yet

- Accounting Is The - Of: - , - and - EconomicDocument48 pagesAccounting Is The - Of: - , - and - EconomicKristia AnagapNo ratings yet

- Depreciation 1Document17 pagesDepreciation 1Kristia AnagapNo ratings yet

- What Is Leadership?: Two Related But Distinct IdeasDocument13 pagesWhat Is Leadership?: Two Related But Distinct IdeasKristia AnagapNo ratings yet

- "First Purchased, First Sold ": Note Well That Under FIFO-periodic and FIFO Perpetual, The Inventory Costs Are The SameDocument4 pages"First Purchased, First Sold ": Note Well That Under FIFO-periodic and FIFO Perpetual, The Inventory Costs Are The SameKristia AnagapNo ratings yet

- BONUSDocument16 pagesBONUSKristia AnagapNo ratings yet

- Mgtnotes Week 8-9Document21 pagesMgtnotes Week 8-9Kristia AnagapNo ratings yet

- Common Frameworks For Evaluating The Business EnvironmentDocument10 pagesCommon Frameworks For Evaluating The Business EnvironmentKristia AnagapNo ratings yet

- Mgtnotes Week 6-7Document17 pagesMgtnotes Week 6-7Kristia AnagapNo ratings yet

- Officiating Basketball and Referee Signals: There Are "Fouls" and There Are "Violations"Document8 pagesOfficiating Basketball and Referee Signals: There Are "Fouls" and There Are "Violations"Kristia Anagap100% (1)

- Mgtnotes Week 2-3Document13 pagesMgtnotes Week 2-3Kristia AnagapNo ratings yet

- AConceptual Frameworkfor Environmental Analysisof Social Issuesand Evaluationof Business ResponDocument14 pagesAConceptual Frameworkfor Environmental Analysisof Social Issuesand Evaluationof Business ResponKristia AnagapNo ratings yet

- A Business Plan of Teahouse in Helsinki, Finland: Xu ZeluDocument49 pagesA Business Plan of Teahouse in Helsinki, Finland: Xu ZeluKristia AnagapNo ratings yet

- PersonsDocument99 pagesPersons1222No ratings yet

- 1st Yr Review Questions Parcor 1Document6 pages1st Yr Review Questions Parcor 1Rogen Dane GeneblazaNo ratings yet

- BS Unit 3Document4 pagesBS Unit 3Enea NastriNo ratings yet

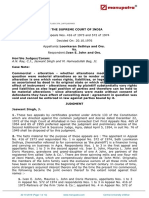

- Loonkaran Sethiya and Ors Vs Ivan E John and OrsDocument13 pagesLoonkaran Sethiya and Ors Vs Ivan E John and OrsAnonymous USJooflFNo ratings yet

- BLR 2022 Prelim Exam Questions For ReproductionDocument12 pagesBLR 2022 Prelim Exam Questions For ReproductionRence MarcoNo ratings yet

- Rush Neess SsDocument51 pagesRush Neess Sssqcanlas.studentNo ratings yet

- Rojas Vs MaglanaDocument2 pagesRojas Vs MaglanaNap GonzalesNo ratings yet

- Business Law Midterms MlquDocument6 pagesBusiness Law Midterms MlquJDR JDRNo ratings yet

- Liton Vs HillDocument4 pagesLiton Vs HillXing Keet LuNo ratings yet

- Ugrd-Ite6301 Technopreneurship Midterm ExamDocument28 pagesUgrd-Ite6301 Technopreneurship Midterm Exampatricia geminaNo ratings yet

- Reviewer 1, Fundamentals of Accounting 2Document13 pagesReviewer 1, Fundamentals of Accounting 2Hunson Abadeer76% (17)

- Entrepre DevelopmentDocument112 pagesEntrepre Developmentsanthanam102No ratings yet

- MRL2601 Assignment 2023Document3 pagesMRL2601 Assignment 2023Gideon MatthewsNo ratings yet

- Tender 64991Document112 pagesTender 64991Nandlal KumavatNo ratings yet

- Feasib Articles of PartnershipDocument3 pagesFeasib Articles of PartnershipSañon TravelsNo ratings yet

- Philex Mining Vs CIRDocument6 pagesPhilex Mining Vs CIRArjay PuyotNo ratings yet

- Concepts of Company LawDocument15 pagesConcepts of Company Lawkuashask2No ratings yet

- Corporate Finance 1Document340 pagesCorporate Finance 1tieuma712No ratings yet

- Group 7 - Organization and Management of Insurance CompanyDocument108 pagesGroup 7 - Organization and Management of Insurance CompanyAnn Tierra100% (1)

- 20-4-2024 DnitDocument51 pages20-4-2024 Dnittejasvi kumawatNo ratings yet

- GCC OF Indian Railways PDFDocument67 pagesGCC OF Indian Railways PDFSarada Dalai100% (1)

- Basic Concept of Income TaxDocument4 pagesBasic Concept of Income TaxNaurah Atika DinaNo ratings yet

- Ona V CIR - TaxDocument2 pagesOna V CIR - TaxKayee KatNo ratings yet

- PartnershipDocument10 pagesPartnershipCaroline ClavioNo ratings yet

- 1 PartnershipDocument54 pages1 PartnershipShajidur RashidNo ratings yet

- Dissolution of Partnership Additional Questions 50 To 53Document6 pagesDissolution of Partnership Additional Questions 50 To 53Ayan NaikNo ratings yet

- JOSE P. OBILLOS, JR., SARAH P. OBILLOS, ROMEO P. OBILLOS and REMEDIOS P. OBILLOS, Brothers and Sisters v. COMMISSIONER OF INTERNAL REVENUE and COURT OF TAX APPEALS - G.R. No. L - 68118Document5 pagesJOSE P. OBILLOS, JR., SARAH P. OBILLOS, ROMEO P. OBILLOS and REMEDIOS P. OBILLOS, Brothers and Sisters v. COMMISSIONER OF INTERNAL REVENUE and COURT OF TAX APPEALS - G.R. No. L - 68118Jo BatsNo ratings yet

- Chapter05 - Business Ownership PDFDocument29 pagesChapter05 - Business Ownership PDFAbdullahNo ratings yet