Download as doc, pdf, or txt

You might also like

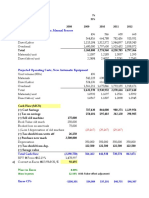

- Projected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Document4 pagesProjected Operating Costs, Manual Process: Inflatio Mexico 7% Tax Rate 35%Cesar CameyNo ratings yet

- Sunshine Stationery Shop Foundation ProjectDocument25 pagesSunshine Stationery Shop Foundation ProjectKripa Raj Devkishin60% (10)

- SDG 4 Quality Education Countries With The Best Education System 1. JapanDocument21 pagesSDG 4 Quality Education Countries With The Best Education System 1. JapanJB LabraNo ratings yet

- B207A - FTHE - Questions - 2020-2021-FirstDocument3 pagesB207A - FTHE - Questions - 2020-2021-FirstRama Naveed100% (1)

- B207A - FTHE - Answer BookletDocument6 pagesB207A - FTHE - Answer BookletRama NaveedNo ratings yet

- PPT: - Budgeting & Cost ControlDocument17 pagesPPT: - Budgeting & Cost Controlaimri_cochin100% (19)

- Bac DCFDocument7 pagesBac DCFVivek GuptaNo ratings yet

- American Cheminal Corp SpreadsheetDocument16 pagesAmerican Cheminal Corp SpreadsheetRahul PandeyNo ratings yet

- BolsaDocument4 pagesBolsaHugo Romo DiazNo ratings yet

- Question 1: Profit MaximazationDocument2 pagesQuestion 1: Profit MaximazationYirgalem AmanuelNo ratings yet

- Netflix Financial StatementsDocument2 pagesNetflix Financial StatementsGoutham RaoNo ratings yet

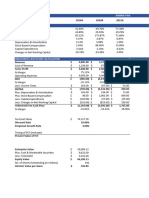

- Historical ProjectionsDocument2 pagesHistorical ProjectionshekmatNo ratings yet

- Cost Per Minute 2013Document76 pagesCost Per Minute 2013dpnairNo ratings yet

- Cost Per Minute Till May 2014Document86 pagesCost Per Minute Till May 2014dpnairNo ratings yet

- Compagnie Du Froid PDFDocument18 pagesCompagnie Du Froid PDFGunjanNo ratings yet

- Nalli Case - SolutionDocument3 pagesNalli Case - SolutionABHIJEET BEURANo ratings yet

- Solucion Caso Lady MDocument13 pagesSolucion Caso Lady Mjohana irma ore pizarroNo ratings yet

- GERENCIAMENTODocument15 pagesGERENCIAMENTOsued monteiroNo ratings yet

- Exercise 16 Looking Up Information: Spell Checking A WorksheetDocument6 pagesExercise 16 Looking Up Information: Spell Checking A WorksheetjoanmubzNo ratings yet

- DOW 30 Companies' Ratio Analysis Excel EdittedDocument23 pagesDOW 30 Companies' Ratio Analysis Excel EdittedLucy GichuNo ratings yet

- MES Saldo Deuda Interes IVA Pago Adelanto Saldo FinalDocument11 pagesMES Saldo Deuda Interes IVA Pago Adelanto Saldo FinalDaniel RamírezNo ratings yet

- Planilha de Gerenciamento Agressivo (10 - Ao Dia) God TraderDocument2 pagesPlanilha de Gerenciamento Agressivo (10 - Ao Dia) God TraderTrader RonaldoNo ratings yet

- Gerenciamento de Risco 2-3Document16 pagesGerenciamento de Risco 2-3JOHN WALKERNo ratings yet

- Genzyme DCF PDFDocument5 pagesGenzyme DCF PDFAbinashNo ratings yet

- Gerenciamento Juros CompostosDocument17 pagesGerenciamento Juros Compostoslostatus1No ratings yet

- ABNB ValuationDocument4 pagesABNB ValuationKasturi MazumdarNo ratings yet

- Meta Luis Com ImpostosDocument12 pagesMeta Luis Com ImpostosLuis BruchNo ratings yet

- Applications 2Document7 pagesApplications 2jaNo ratings yet

- Marketing ExcelDocument4 pagesMarketing ExcelMaria Camila Sierra RamosNo ratings yet

- NetflixDocument13 pagesNetflixRamesh SinghNo ratings yet

- amortizacionPDF PDFDocument2 pagesamortizacionPDF PDFErick NeoNo ratings yet

- Time To FI (RE) SpreadsheetDocument8 pagesTime To FI (RE) SpreadsheetdigiowlmedialabNo ratings yet

- Quarterly Sales Report: Item Code Item Price Quantity Sales CommissionDocument2 pagesQuarterly Sales Report: Item Code Item Price Quantity Sales CommissionManuel ArciniegasNo ratings yet

- Gerenciamento Com 60Document9 pagesGerenciamento Com 60VENHAN PARA O MUNDO PES.No ratings yet

- Gerenciamento Com 60Document9 pagesGerenciamento Com 60VENHAN PARA O MUNDO PES.No ratings yet

- Iqoption PLANILHA 3%Document8 pagesIqoption PLANILHA 3%Rafael Cabral RochaNo ratings yet

- CF ExcelDocument2 pagesCF ExcelAnam AbrarNo ratings yet

- Erika Ximena SueldosDocument4 pagesErika Ximena SueldosXimeeri VFNo ratings yet

- 320 Units - Oakleaf, FL - 4-Story - Conceptual Estimate - 2022.11.30Document10 pages320 Units - Oakleaf, FL - 4-Story - Conceptual Estimate - 2022.11.30Nancie BrennanNo ratings yet

- Gerenciamento de Juros CompostoDocument8 pagesGerenciamento de Juros Compostoernandyoriel54321No ratings yet

- Gerenciamento TraderDocument11 pagesGerenciamento TraderLUMA OLIVEIRANo ratings yet

- Q4 23 Website FinancialsDocument4 pagesQ4 23 Website FinancialsIrina SvyshchukNo ratings yet

- Reporte de Ventas Ok Market Noviembre 2022Document9 pagesReporte de Ventas Ok Market Noviembre 2022XxKevin 1519No ratings yet

- Gerenciamento Do BraboDocument8 pagesGerenciamento Do Brabocareca baixada santistaNo ratings yet

- Beron - FinancialForecastingDocument25 pagesBeron - FinancialForecastingKat BeronNo ratings yet

- Department Name Department Code Average of Salary Department NameDocument8 pagesDepartment Name Department Code Average of Salary Department NameDefi Rizki MaulianiNo ratings yet

- Lady M Exercises-3Document6 pagesLady M Exercises-3MOHIT MARHATTANo ratings yet

- VlookupnestorascencioDocument7 pagesVlookupnestorascencioapi-385842294No ratings yet

- Tco 3Document7 pagesTco 3brianNo ratings yet

- Tasa Premiun ISSSTE e IMSS 90%Document6 pagesTasa Premiun ISSSTE e IMSS 90%MARIA LUZ MARTINEZ CRUZNo ratings yet

- My Pro Forma Indv. AssignmentDocument36 pagesMy Pro Forma Indv. AssignmentGhieAliciaNo ratings yet

- ანრი მაჭავარიანი ფინალურიDocument40 pagesანრი მაჭავარიანი ფინალურიAnri MachavarianiNo ratings yet

- Gerenciamento Juros CompostoDocument8 pagesGerenciamento Juros CompostobrancopelisonkNo ratings yet

- Planilha-Bruninho - 2Document6 pagesPlanilha-Bruninho - 2palmeiras199920202021mdmNo ratings yet

- Leo Projeto CompletoDocument30 pagesLeo Projeto CompletoJadson FernandoNo ratings yet

- Copycooperative Financial Ratio Calculator 2011Document10 pagesCopycooperative Financial Ratio Calculator 2011pradhan13No ratings yet

- CF ExcelDocument4 pagesCF ExcelAnam AbrarNo ratings yet

- MONEY ManagementDocument9 pagesMONEY ManagementRavi KumarNo ratings yet

- Planilha Gerenciamento AtualDocument12 pagesPlanilha Gerenciamento AtualLaísa SantosNo ratings yet

- Gere Nci Amen ToDocument15 pagesGere Nci Amen ToDroop ShopNo ratings yet

- Castillo Antonio Act1Document7 pagesCastillo Antonio Act1Antonio Castillo MiguelNo ratings yet

- Case Study Cashflow Financials (4 Months)Document5 pagesCase Study Cashflow Financials (4 Months)Jeremy smithNo ratings yet

- GrowthDocument7 pagesGrowthFarooq HaiderNo ratings yet

- Profitability of simple fixed strategies in sport betting: Soccer, Italy Serie A League, 2009-2019From EverandProfitability of simple fixed strategies in sport betting: Soccer, Italy Serie A League, 2009-2019No ratings yet

- Modified MBA712 ProjectDocument10 pagesModified MBA712 ProjectRama NaveedNo ratings yet

- VWangenheim-Bayón2007 Article TheChainFromCustomerSatisfactiDocument17 pagesVWangenheim-Bayón2007 Article TheChainFromCustomerSatisfactiRama NaveedNo ratings yet

- CH-06-Web, Nonstore-Based, and Other Firms of Nontraditional RetailingDocument39 pagesCH-06-Web, Nonstore-Based, and Other Firms of Nontraditional RetailingRama NaveedNo ratings yet

- CH-06-Web, Nonstore-Based, and Other Firms of Nontraditional RetailingDocument39 pagesCH-06-Web, Nonstore-Based, and Other Firms of Nontraditional RetailingRama NaveedNo ratings yet

- CH-05-Retail Institutions by Store-Based Strategy MixDocument64 pagesCH-05-Retail Institutions by Store-Based Strategy MixRama NaveedNo ratings yet

- General Purpose Cost StatementDocument36 pagesGeneral Purpose Cost StatementShatrughna SamalNo ratings yet

- Nicholson, The Effects of Machinery On WagesDocument76 pagesNicholson, The Effects of Machinery On Wagesquintus14No ratings yet

- 12 Economics Material PV 2023Document87 pages12 Economics Material PV 2023johnsonNo ratings yet

- Fair Trade: What Does It Mean and Why Does It Matter?Document24 pagesFair Trade: What Does It Mean and Why Does It Matter?ben zilethNo ratings yet

- Disini Labor NotesDocument199 pagesDisini Labor NotesDennise Talan100% (1)

- DLSU AKI - Local Cooperation and Upgrading in Response To GlobalizationDocument51 pagesDLSU AKI - Local Cooperation and Upgrading in Response To GlobalizationBenedict RazonNo ratings yet

- Applied Economics Reviewer 2nd QuarterDocument13 pagesApplied Economics Reviewer 2nd QuarterZack Fair83% (6)

- An Insight Into The Drag Effect of Water Land and EnergyDocument15 pagesAn Insight Into The Drag Effect of Water Land and Energymeshael FahadNo ratings yet

- Ch09 - Standard Costing A Managerial Control ToolDocument46 pagesCh09 - Standard Costing A Managerial Control Toolachmad rezaNo ratings yet

- Farm Size Factor Productivity and Returns To ScaleDocument8 pagesFarm Size Factor Productivity and Returns To ScaleAkshay YadavNo ratings yet

- Micro Final DraftDocument5 pagesMicro Final DraftJigeesha BankaNo ratings yet

- Managerial Accounting by James Jiambalvo: Standard Costs and Variance AnalysisDocument31 pagesManagerial Accounting by James Jiambalvo: Standard Costs and Variance AnalysisRatnesh SinghNo ratings yet

- Executive Shirt Company: Case Study Analysis by Lg-4Document9 pagesExecutive Shirt Company: Case Study Analysis by Lg-4AD RNo ratings yet

- Policies For Reducing UnemploymentDocument14 pagesPolicies For Reducing UnemploymentAnushkaa DattaNo ratings yet

- (Williams) Youth and Minority UnemploymentDocument58 pages(Williams) Youth and Minority Unemploymentdragos_ungureanu_6No ratings yet

- Causes and Effects of Employee Downsizing A ReviewDocument70 pagesCauses and Effects of Employee Downsizing A ReviewIntan SalwaniNo ratings yet

- Procurement (Kat) 2. Inbound Logistics. This Includes Del Monte's Operation of Storing Their Acquired RawDocument5 pagesProcurement (Kat) 2. Inbound Logistics. This Includes Del Monte's Operation of Storing Their Acquired RawEunice MiloNo ratings yet

- David RicardoDocument25 pagesDavid RicardoSuhani RathiNo ratings yet

- Sigdel and Silwal PDFDocument8 pagesSigdel and Silwal PDFuditprakash sigdelNo ratings yet

- The Lewis Model of Economic DevelopmentDocument17 pagesThe Lewis Model of Economic Developmentgazi faisalNo ratings yet

- Economics Paper 3Document10 pagesEconomics Paper 3Hamiz AizuddinNo ratings yet

- Employment Relations in Outsourced Public Services Working Between Market and State 1St Ed 2020 Edition Anna Mori Full ChapterDocument68 pagesEmployment Relations in Outsourced Public Services Working Between Market and State 1St Ed 2020 Edition Anna Mori Full Chapterrichard.williams179100% (7)

- Bslea Ge Elec 1 Living in The It Era Module 5 NaDocument9 pagesBslea Ge Elec 1 Living in The It Era Module 5 NaSiao SabatinNo ratings yet

- Labour Welfare - Paternalistic, Industrial Efficiency and Social ApproachDocument7 pagesLabour Welfare - Paternalistic, Industrial Efficiency and Social ApproachAzra MuftiNo ratings yet

- CHAPTER TWO FinalDocument89 pagesCHAPTER TWO Finalyiberta69No ratings yet

- Higher Diploma in Human Resource Management: Employee RelationsDocument119 pagesHigher Diploma in Human Resource Management: Employee RelationsDaisy JepkosgeiNo ratings yet

- Hrp-Human Resource Planning: Pps - Personal PoliciesDocument7 pagesHrp-Human Resource Planning: Pps - Personal PoliciesMd. Muhinur Islam AdnanNo ratings yet