Download as docx, pdf, or txt

You might also like

- Wildcat Capital Case M&A Invesment Real EstateDocument7 pagesWildcat Capital Case M&A Invesment Real EstatePaco Colín8% (12)

- Engineering Economics Reviewer Part 2 PDFDocument99 pagesEngineering Economics Reviewer Part 2 PDFagricultural and biosystems engineeringNo ratings yet

- Capter 2Document5 pagesCapter 2DiwakarNo ratings yet

- Ifoa ExamDocument12 pagesIfoa ExamLUKENo ratings yet

- Tax On Individuals Quiz - ProblemsDocument3 pagesTax On Individuals Quiz - ProblemsJP Mirafuentes100% (1)

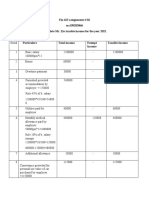

- Information On Salaries 2023Document6 pagesInformation On Salaries 2023JuNo ratings yet

- Bottom of Your Answer DocumentDocument6 pagesBottom of Your Answer Documentlim qsNo ratings yet

- Economics ReviewerDocument117 pagesEconomics Reviewerzane truesdale0% (1)

- Practice Problems, CH 9 10 (MCQ)Document5 pagesPractice Problems, CH 9 10 (MCQ)scridNo ratings yet

- Service Rules FR SubDocument2 pagesService Rules FR SubMuhammad MustafaNo ratings yet

- NBC 568-Second TrancheDocument30 pagesNBC 568-Second TrancheRaymund P. CruzNo ratings yet

- APGLIDocument7 pagesAPGLIskssahul59No ratings yet

- Griya Step Up RegulerDocument1 pageGriya Step Up ReguleranjabkelompokduaNo ratings yet

- Mutahir ProjectDocument46 pagesMutahir Projectprince khanNo ratings yet

- Personal InvestmentDocument93 pagesPersonal InvestmentPratham Poovaiah MalavandaNo ratings yet

- Executive Order No. 201 Salary Standardization LawDocument9 pagesExecutive Order No. 201 Salary Standardization LawDiosdado Cabo-Contiga AdolfoNo ratings yet

- If The Interest Rate Is 10 Percent, Then The Future Value in 2 Years of $100 Today Would Be?Document15 pagesIf The Interest Rate Is 10 Percent, Then The Future Value in 2 Years of $100 Today Would Be?Saumil PatelNo ratings yet

- Time Value of Money: AppendixDocument4 pagesTime Value of Money: AppendixnurlaeliyahrahayuNo ratings yet

- E.O. 201Document13 pagesE.O. 201SakuraCardCaptorNo ratings yet

- Corona Kavach Policy-Oriental Insurance - Rate Chart - RRDocument2 pagesCorona Kavach Policy-Oriental Insurance - Rate Chart - RRNagaraj BVNo ratings yet

- Executive Order No. 201, S. 2016 - Official Gazette of The Republic of The PhilippinesDocument15 pagesExecutive Order No. 201, S. 2016 - Official Gazette of The Republic of The PhilippinesDesiugsid DneirfNo ratings yet

- Chart 100078979Document5 pagesChart 100078979Huy ĐoànNo ratings yet

- Introduction To Stock Markets: ZerodhaDocument104 pagesIntroduction To Stock Markets: ZerodhakosurugNo ratings yet

- Table I-1:: Compound Interest Tables and FormulaeDocument4 pagesTable I-1:: Compound Interest Tables and FormulaeFauzan PrabowoNo ratings yet

- Table I-1:: Compound Interest Tables and FormulaeDocument4 pagesTable I-1:: Compound Interest Tables and FormulaeFauzan PrabowoNo ratings yet

- Commutation Values For A Pension of Re. 1 Per Annum: Explanatory NoteDocument1 pageCommutation Values For A Pension of Re. 1 Per Annum: Explanatory NoteSreekumar U DileepNo ratings yet

- FINS1613 File 04 - All 3 Topics Practice Questions PDFDocument16 pagesFINS1613 File 04 - All 3 Topics Practice Questions PDFisy campbellNo ratings yet

- MRK - Ipani NewDocument24 pagesMRK - Ipani NewAgie Ramdiansyah NurrahmanNo ratings yet

- Present Value of An AnnuityDocument3 pagesPresent Value of An AnnuityMotivational QuotesNo ratings yet

- Corona Kavach Policy-Oriental Insurance - Rate ChartDocument3 pagesCorona Kavach Policy-Oriental Insurance - Rate ChartAnand KesarkarNo ratings yet

- Distribui A A o NormalDocument8 pagesDistribui A A o NormalJBWarriorNo ratings yet

- Executive Order No. 201, S. 2016: February 19, 2016Document12 pagesExecutive Order No. 201, S. 2016: February 19, 2016Jude MaiquezNo ratings yet

- Corporate Finance AssignmentDocument16 pagesCorporate Finance AssignmentHekmat JanNo ratings yet

- Bang Gia Tri Thong KeDocument12 pagesBang Gia Tri Thong KeHồng NhungNo ratings yet

- Top Glove LatestDocument3 pagesTop Glove LatestAishiterru Gurl'sNo ratings yet

- Bang Gia Tri Thong KeDocument12 pagesBang Gia Tri Thong KeKim ChiiNo ratings yet

- Bang Gia Tri Thong KeDocument12 pagesBang Gia Tri Thong KeHồng NhungNo ratings yet

- Irr On Project and Irr On Equity: by Krigan CapitalDocument6 pagesIrr On Project and Irr On Equity: by Krigan CapitalAziz SaputraNo ratings yet

- Policy Status ReportDocument6 pagesPolicy Status ReportBenson BennyNo ratings yet

- 10.-Bang TraDocument12 pages10.-Bang TraMinNo ratings yet

- Tabel ProgramDocument1 pageTabel Programmapping.pklNo ratings yet

- Tata BAF - 6%Document1 pageTata BAF - 6%Samrat FuriaNo ratings yet

- Hitungan ACC 2021 PBUN SalinanDocument6 pagesHitungan ACC 2021 PBUN SalinanFarid Ruskanda BasyarahilNo ratings yet

- M Naufal Fawwaz - 2112070059 - Latihan MKL Amortized LoanDocument8 pagesM Naufal Fawwaz - 2112070059 - Latihan MKL Amortized LoanNaufal FawwazNo ratings yet

- SHU - Tabelas MANNINGDocument5 pagesSHU - Tabelas MANNINGFabio SabinoNo ratings yet

- EO 201 S 2016 Salary Schedule of Civilian Govt EmployeesDocument15 pagesEO 201 S 2016 Salary Schedule of Civilian Govt EmployeesJonas George S. SorianoNo ratings yet

- Amendment of Salary and Wages Tax 2019 PDFDocument11 pagesAmendment of Salary and Wages Tax 2019 PDFMark WaniNo ratings yet

- IM - Cogent HRDocument14 pagesIM - Cogent HRAaron WilsonNo ratings yet

- Pvfa TableDocument2 pagesPvfa TableschewyNo ratings yet

- Test Programmer PayrollDocument8 pagesTest Programmer PayrollNanda Sholatul AkbarNo ratings yet

- Pension Scheme After 2004 For ChhattisgarhDocument4 pagesPension Scheme After 2004 For ChhattisgarhSaksham SrivastavNo ratings yet

- SB003 Error Code TKDDocument2 pagesSB003 Error Code TKDYakshit JainNo ratings yet

- DataDocument5 pagesDataKaushal GangradeNo ratings yet

- Price 544.43 Shares 935 Q222 MC 509,250 Cash 70,391 Q222 Debt 74,369 Q222 EV 513,228Document6 pagesPrice 544.43 Shares 935 Q222 MC 509,250 Cash 70,391 Q222 Debt 74,369 Q222 EV 513,228egoquuNo ratings yet

- IT IC54232M Malanaruna@Gmail - Com 13-04-2023Document4 pagesIT IC54232M Malanaruna@Gmail - Com 13-04-2023malanarunaNo ratings yet

- FINS1613 File 03 - Decision Rules (With Solutions) Practice QuestionsDocument9 pagesFINS1613 File 03 - Decision Rules (With Solutions) Practice Questionsisy campbellNo ratings yet

- Akansh Arora FM AssignmentDocument17 pagesAkansh Arora FM AssignmentAKANSH ARORANo ratings yet

- HamiltonDocument4 pagesHamiltonMark VanderlindenNo ratings yet

- Triaxal MutikDocument114 pagesTriaxal MutikMuhammad RaflyNo ratings yet

- A Investment Platform for Future: Self Help a Self Operating BankingFrom EverandA Investment Platform for Future: Self Help a Self Operating BankingNo ratings yet

- Joining Report AteaDocument1 pageJoining Report AteaCJ MazualaNo ratings yet

- Atea Skill ExamDocument1 pageAtea Skill ExamCJ MazualaNo ratings yet

- NEET SS 2019 Print TurDocument3 pagesNEET SS 2019 Print TurCJ MazualaNo ratings yet

- Medical Enclave, Ansari Nagar, Mahatma Gandhi Marg, Ring Road, New Delhi - 110029Document1 pageMedical Enclave, Ansari Nagar, Mahatma Gandhi Marg, Ring Road, New Delhi - 110029CJ MazualaNo ratings yet

- Interface Between Customary and Formal Land Management Systems Mizoram, IndiaDocument23 pagesInterface Between Customary and Formal Land Management Systems Mizoram, IndiaCJ MazualaNo ratings yet

- An Interesting Case of Gluteal Swelling - Intramuscular Myxoma (IMM) by DR Zothansanga ZadengDocument3 pagesAn Interesting Case of Gluteal Swelling - Intramuscular Myxoma (IMM) by DR Zothansanga ZadengCJ MazualaNo ratings yet

- Mizodistrict (LandnRevenue) Act, 1956Document9 pagesMizodistrict (LandnRevenue) Act, 1956CJ MazualaNo ratings yet

- Pages 87 Application Form Printmimer10june2019Document2 pagesPages 87 Application Form Printmimer10june2019CJ MazualaNo ratings yet

- The Mizoram (Land Revenue) Act, 2013 (Act No. 5 of 2013)Document33 pagesThe Mizoram (Land Revenue) Act, 2013 (Act No. 5 of 2013)CJ MazualaNo ratings yet

- Australian GST Legislation With Overview Current To 1 January 2019 22nd Edition 9781925894028 1925894029Document1,394 pagesAustralian GST Legislation With Overview Current To 1 January 2019 22nd Edition 9781925894028 1925894029hgkm75nfjvNo ratings yet

- Prefinal Exam - SolutionDocument7 pagesPrefinal Exam - SolutionKarlo PalerNo ratings yet

- IRTSA Charter of Demands For 7th CPC As Adopted by CGBDocument8 pagesIRTSA Charter of Demands For 7th CPC As Adopted by CGBMrityunjay KrNo ratings yet

- Solution Manual For Canadian Income Taxation 2019 2020 22th by BuckwoldDocument53 pagesSolution Manual For Canadian Income Taxation 2019 2020 22th by BuckwoldKeithClarknrjz100% (52)

- Important Abbreviation List - GKmojoDocument3 pagesImportant Abbreviation List - GKmojoMontuNo ratings yet

- Employers Liability Takaful Proposal Form 11102023Document5 pagesEmployers Liability Takaful Proposal Form 11102023Muhamad Izwan Bin HanafiNo ratings yet

- SOPforretirement, Leaveenchashment, AndsubmissionofpensionpapersDocument3 pagesSOPforretirement, Leaveenchashment, AndsubmissionofpensionpapersKiran ShahNo ratings yet

- RetirementDocument6 pagesRetirementWidya AisyahNo ratings yet

- Acc 109 Quiz 1 P3Document2 pagesAcc 109 Quiz 1 P3GargaritanoNo ratings yet

- Social Assistance & Social InsuranceDocument12 pagesSocial Assistance & Social InsuranceMohan Lal100% (2)

- Kaneez FatimaDocument3 pagesKaneez FatimaDaniyal SirajNo ratings yet

- F86407Document2 pagesF86407Abhishek PawarNo ratings yet

- Business Finance 1st Quarter Examination 22-23Document3 pagesBusiness Finance 1st Quarter Examination 22-23Phegiel Honculada MagamayNo ratings yet

- Reviewer Taxation Modules 1 - 3Document11 pagesReviewer Taxation Modules 1 - 3afeiahnaniNo ratings yet

- IC 83 - Compressed-4Document50 pagesIC 83 - Compressed-4purnachandrashee1No ratings yet

- Chapter 3: Introduction To Income Taxation: Item of Gross Income Taxable IncomeDocument39 pagesChapter 3: Introduction To Income Taxation: Item of Gross Income Taxable IncomeSheva Mae Suello0% (1)

- Rise Tax Mock QP With SolutionDocument18 pagesRise Tax Mock QP With SolutionEmperor YasuoNo ratings yet

- DentalEstimate Le 231015Document3 pagesDentalEstimate Le 231015Jiang CuiNo ratings yet

- 03 - Residence and Scope of Total IncomeDocument44 pages03 - Residence and Scope of Total IncomeTushar RathiNo ratings yet

- Circular 566Document2 pagesCircular 566tadilakshmikiranNo ratings yet

- WEEKLY HOME LEARNING PLAN IN Quarter 2 General Math DJDocument2 pagesWEEKLY HOME LEARNING PLAN IN Quarter 2 General Math DJDaniel Jars100% (1)

- Hall Tax Services Hall Tax Professionals Chicago Heights Il 60411Document34 pagesHall Tax Services Hall Tax Professionals Chicago Heights Il 60411Rendy MomoNo ratings yet

- Human Resource Management Chapter 9 ReviewerDocument5 pagesHuman Resource Management Chapter 9 ReviewerNikkson CayananNo ratings yet

- E Filing Income Tax Return OnlineDocument53 pagesE Filing Income Tax Return OnlineMd MisbahNo ratings yet

- Computation of Income Tax LiabilityDocument6 pagesComputation of Income Tax LiabilityAbdullah QureshiNo ratings yet

- Income Tax Payment Challan: PSID #: 35390320Document1 pageIncome Tax Payment Challan: PSID #: 35390320zeshanNo ratings yet

- Fin - 623 Assignment 2Document5 pagesFin - 623 Assignment 2Abdussalam gillNo ratings yet

- FEB-23-Salary SlipDocument1 pageFEB-23-Salary SlipIt's your BhootNo ratings yet

- 2021 Riverside County Pension Advisory Review Committee ReportDocument16 pages2021 Riverside County Pension Advisory Review Committee ReportThe Press-Enterprise / pressenterprise.comNo ratings yet