Download as pdf or txt

You might also like

- HL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11Document2 pagesHL - Pni - V1 - NTR - 3596132948944013913 - NTR - 7818877607244788448 - 11KanakaReddyKannaNo ratings yet

- 004 - NRI - Main Application Form - FillableDocument6 pages004 - NRI - Main Application Form - FillableAnkur MishRraNo ratings yet

- Global Financial Corporation (GFC)Document7 pagesGlobal Financial Corporation (GFC)Fez Research Laboratory100% (2)

- FHFA V NomuraDocument79 pagesFHFA V NomuraMike_DillonNo ratings yet

- Happy Birthday, Bob!Document48 pagesHappy Birthday, Bob!api-26032005No ratings yet

- The Loan AgreementDocument4 pagesThe Loan AgreementblsandcoNo ratings yet

- Most Important Terms and Conditions (Mitc) : 1. Fees and Other ChargesDocument6 pagesMost Important Terms and Conditions (Mitc) : 1. Fees and Other ChargesSpl FriendsNo ratings yet

- MITC Website 1Document7 pagesMITC Website 1Mohit SainiNo ratings yet

- RI AnnexureDocument6 pagesRI Annexurekaizen.hameshaNo ratings yet

- Loan Approval 2Document8 pagesLoan Approval 2satishssharmag34No ratings yet

- Fees and Charges CompensiveDocument1 pageFees and Charges CompensiveGSAINTSSANo ratings yet

- Aadhar Tariff Schedule092021-2 PDFDocument2 pagesAadhar Tariff Schedule092021-2 PDFSamNo ratings yet

- 8 Fees and Charges Revised On 04 08 2016Document2 pages8 Fees and Charges Revised On 04 08 2016M ADITYA REDDYNo ratings yet

- Khushi Home LoansDocument2 pagesKhushi Home LoansGovind JhaNo ratings yet

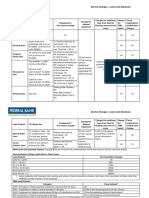

- Schedule of Charges - Master - 16.3.23Document6 pagesSchedule of Charges - Master - 16.3.23mk9778225No ratings yet

- Fees and Charges PLATINUMDocument1 pageFees and Charges PLATINUMLouise Nichole LogartaNo ratings yet

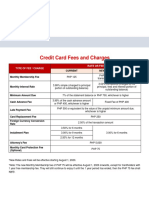

- Credit Card Fees and Charges: Type of Fee / Charge Rate or FeeDocument1 pageCredit Card Fees and Charges: Type of Fee / Charge Rate or FeeKram Yer EtentepmocNo ratings yet

- Home Loan: TCHFL HL MITC Version 17Document4 pagesHome Loan: TCHFL HL MITC Version 17Ali Khan AKNo ratings yet

- Schedule of Charges Version 21.0.0 Dated 1st June 19Document1 pageSchedule of Charges Version 21.0.0 Dated 1st June 19RajivNo ratings yet

- Most Important Terms and Conditions (Mitc) Loan Reference No.Document6 pagesMost Important Terms and Conditions (Mitc) Loan Reference No.prashant gargNo ratings yet

- Mitc PDFDocument6 pagesMitc PDFrocky themountainNo ratings yet

- Loanagainstproperty PDFDocument4 pagesLoanagainstproperty PDFsameer ahmadNo ratings yet

- Schedule-Of-charges Master 27-10-23Document142 pagesSchedule-Of-charges Master 27-10-23xtreameairtelNo ratings yet

- Annexure 2Document77 pagesAnnexure 2Maheshkumar AmulaNo ratings yet

- LoanDocument1 pageLoanPrateek SoniNo ratings yet

- Schedule of Charges and Interest Rates PDFDocument5 pagesSchedule of Charges and Interest Rates PDFAjju PodilaNo ratings yet

- Most Important Terms and ConditionsDocument3 pagesMost Important Terms and ConditionsSaurav SamadhiyaNo ratings yet

- Schedule of Charges - Protium ProtiumDocument1 pageSchedule of Charges - Protium Protiummufcrufc12345No ratings yet

- HL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448Document2 pagesHL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448KanakaReddyKannaNo ratings yet

- IDBI Bank Schedule of Service Charges Home Loan Mortgage Loan 05112012Document3 pagesIDBI Bank Schedule of Service Charges Home Loan Mortgage Loan 05112012Arijit DuttaNo ratings yet

- Taxation of Salary IncomeDocument3 pagesTaxation of Salary IncomebilalNo ratings yet

- Fees and Charges W.E.F. 13th Dec, 2021Document4 pagesFees and Charges W.E.F. 13th Dec, 2021Chandrashekar ReddyNo ratings yet

- Fees and Charges - Home LoanDocument1 pageFees and Charges - Home LoankarthikeyaNo ratings yet

- HL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448Document2 pagesHL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448KanakaReddyKannaNo ratings yet

- Most Important Terms and Conditions: Card - Pdf?Clgproductid 3645560672Document2 pagesMost Important Terms and Conditions: Card - Pdf?Clgproductid 3645560672Nagarjuna DevarakondaNo ratings yet

- Service Charges - Loans and Advances 14 NovDocument21 pagesService Charges - Loans and Advances 14 Novsamuelbihari2012No ratings yet

- Schedule of Charges - Master - 27 10 23 1Document10 pagesSchedule of Charges - Master - 27 10 23 1shuvam0016No ratings yet

- Charges Home NewDocument3 pagesCharges Home Newkirubaharan2022No ratings yet

- Type of Pre-Payment % Age Rate On The Amount Pre-Paid: Rangam de Sarkar Mob-9871112751Document1 pageType of Pre-Payment % Age Rate On The Amount Pre-Paid: Rangam de Sarkar Mob-9871112751Mohet LambaNo ratings yet

- LoanAccountsStructured RetailDocument10 pagesLoanAccountsStructured RetailDeepashree MajhiNo ratings yet

- Personal Loan: Why Avail A Personal Loan From HDFC Bank?Document6 pagesPersonal Loan: Why Avail A Personal Loan From HDFC Bank?Ramana GNo ratings yet

- HL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448 NTR 2643578978408764679 NTR 4658264169499347647Document2 pagesHL Pni V1 NTR 3596132948944013913 NTR 7818877607244788448 NTR 2643578978408764679 NTR 4658264169499347647G “Vijay Ramesh” RameshNo ratings yet

- 6b8565e6ff8511ebb4c0c691ab02ab46Document10 pages6b8565e6ff8511ebb4c0c691ab02ab46Sumit ChakrabortyNo ratings yet

- PersonalLoan SOBC (Jan. 01 To June 30, 2023)Document1 pagePersonalLoan SOBC (Jan. 01 To June 30, 2023)sherazalimemonNo ratings yet

- Zaggle Fee StructureDocument1 pageZaggle Fee StructureVishal TiwariNo ratings yet

- ICICI Mortgage PACustomer 7727036138 7 29 2023Document5 pagesICICI Mortgage PACustomer 7727036138 7 29 2023shubhamkumarrajput92No ratings yet

- Charges 20131130Document3 pagesCharges 20131130SssNo ratings yet

- HBL - Updated Charges Wef From 1-Jan-2018Document3 pagesHBL - Updated Charges Wef From 1-Jan-2018Mubin AshrafNo ratings yet

- 8,9 Employee Compensation PackageDocument37 pages8,9 Employee Compensation PackageAMITESH RANJANNo ratings yet

- Bike LoanDocument1 pageBike LoanKrishna KumarNo ratings yet

- Schedule of Charges: Upfront Charges (Charges Before/During Disbursement)Document2 pagesSchedule of Charges: Upfront Charges (Charges Before/During Disbursement)BharatSharmaNo ratings yet

- Ploan 2 PDFDocument2 pagesPloan 2 PDFmahavirNo ratings yet

- Education Loan SOCDocument2 pagesEducation Loan SOCVinay PandeyNo ratings yet

- Please Read These Loan Terms and Conditions Carefully: S.No Particulars DetailsDocument7 pagesPlease Read These Loan Terms and Conditions Carefully: S.No Particulars DetailsRavishankar PonnadaNo ratings yet

- Othguide For Act Invt Proof Submission - FY 2021-22 - Guide For Act Invt Proof Submission - FY 2021-22Document19 pagesOthguide For Act Invt Proof Submission - FY 2021-22 - Guide For Act Invt Proof Submission - FY 2021-22Dhruv JainNo ratings yet

- Home Loan and Loan Against PropertyDocument4 pagesHome Loan and Loan Against PropertyPraveen KumarNo ratings yet

- Key Fact Sheet (HBL PersonalLoan) - July 2018Document1 pageKey Fact Sheet (HBL PersonalLoan) - July 2018pakistan jobs100% (1)

- Income From Salary (Section 12) : RsDocument8 pagesIncome From Salary (Section 12) : RsKashifNo ratings yet

- Key Fact Sheet (HBL PersonalLoan) - July 2019Document1 pageKey Fact Sheet (HBL PersonalLoan) - July 2019MUHAMMAD ALI RAZANo ratings yet

- Fees and Charges W.E.F. 17th Mar, 2021Document3 pagesFees and Charges W.E.F. 17th Mar, 2021MANOJ PANSENo ratings yet

- Rems of ServicesDocument4 pagesRems of ServicesmamdudurNo ratings yet

- HBL Credit Card - Basic Charges Sheet (Version 2 W.E.F July 01 2019)Document2 pagesHBL Credit Card - Basic Charges Sheet (Version 2 W.E.F July 01 2019)shani908No ratings yet

- Product Disclosure Sheet: HSBC Bank Malaysia Berhad Revolving LoanDocument4 pagesProduct Disclosure Sheet: HSBC Bank Malaysia Berhad Revolving Loanthong_wheiNo ratings yet

- What Is A Financial InstituteDocument7 pagesWhat Is A Financial InstituteRahim RazaNo ratings yet

- DSGDFHFDocument17 pagesDSGDFHFCy PanganibanNo ratings yet

- Bloomberg Cheat Sheets PDFDocument45 pagesBloomberg Cheat Sheets PDFRakesh SuriNo ratings yet

- An Analysis of Interest Rate Spread in Nepalese Commercial BankDocument12 pagesAn Analysis of Interest Rate Spread in Nepalese Commercial BankUday Sharma33% (9)

- Overview of Indian Financial Systems and MarketsDocument17 pagesOverview of Indian Financial Systems and MarketsPremendra SahuNo ratings yet

- Korea Exchange Bank Vs FilkorDocument2 pagesKorea Exchange Bank Vs FilkorsakuraNo ratings yet

- Gallery Exhibition Contract 1Document1 pageGallery Exhibition Contract 1api-275646456No ratings yet

- Faysal Bank of PakistanDocument4 pagesFaysal Bank of PakistanRuba KhanNo ratings yet

- CFD 2004-3 Official StatementDocument265 pagesCFD 2004-3 Official StatementBrian DaviesNo ratings yet

- Assignment #1 Tri Pack Film Limited: Analysis of Solvency RatiosDocument4 pagesAssignment #1 Tri Pack Film Limited: Analysis of Solvency RatiossooperusmanNo ratings yet

- Essentials of Transportation and Public Utilities LawDocument3 pagesEssentials of Transportation and Public Utilities LawAnonymous KgOu1VfNyB0% (8)

- Property Case DigestsDocument142 pagesProperty Case DigestsMarisol RodriguezNo ratings yet

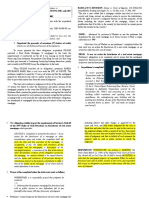

- Foreclosure of Chattel MortgageDocument5 pagesForeclosure of Chattel MortgageElLayynTrga100% (1)

- Library Policies and Procedures 5-2017 EditDocument5 pagesLibrary Policies and Procedures 5-2017 Editapi-288755513No ratings yet

- Compiled Civil Litigation Notes-1Document49 pagesCompiled Civil Litigation Notes-1Brn MurgorNo ratings yet

- Shriram Transport Finance Company LTD, MeghanDocument26 pagesShriram Transport Finance Company LTD, MeghanAnil Bambule100% (1)

- Draft Asset Management RulesDocument38 pagesDraft Asset Management RulesMichael LyttleNo ratings yet

- Acris CodesDocument12 pagesAcris Codesbob dole100% (1)

- ACCT 415 CH 14 Bank (Kind Of)Document4 pagesACCT 415 CH 14 Bank (Kind Of)lascejasNo ratings yet

- DT Hot TipsDocument12 pagesDT Hot TipsChaNo ratings yet

- Case Study - Narmada Dams ControversyDocument26 pagesCase Study - Narmada Dams ControversyGaurav PandeyNo ratings yet

- Heirs of Intac Vs CADocument18 pagesHeirs of Intac Vs CAAngel AmarNo ratings yet

- Ranjini FinanceDocument3 pagesRanjini FinanceAyanleke Julius OluwaseunfunmiNo ratings yet

- PNB V OseteDocument1 pagePNB V OseteBrian DuffyNo ratings yet

- 10000021383Document849 pages10000021383Chapter 11 DocketsNo ratings yet

- ECS-D Mandate FormDocument3 pagesECS-D Mandate FormNeelima DeyNo ratings yet