Download as pdf or txt

You might also like

- Buckwold 20ce sm04Document68 pagesBuckwold 20ce sm04Kailash Kumar100% (1)

- Test Bank For Financial Accounting 11th Edition Albrecht DownloadDocument50 pagesTest Bank For Financial Accounting 11th Edition Albrecht Downloadkarenmorrisszqyjrbegn100% (35)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Mahusay - Acc319 - Module 1 Major OutputDocument4 pagesMahusay - Acc319 - Module 1 Major OutputJeth MahusayNo ratings yet

- Employee Benefits Part 1: Name: Date: Professor: Section: Score: Quiz 1Document4 pagesEmployee Benefits Part 1: Name: Date: Professor: Section: Score: Quiz 1Jamie Rose Aragones83% (6)

- Chapter 5 - Employee Benefits Part 1Document7 pagesChapter 5 - Employee Benefits Part 1XienaNo ratings yet

- Major Assessment - Current Liab-MahusayDocument5 pagesMajor Assessment - Current Liab-MahusayJeth Mahusay100% (1)

- DPR Offer Letter PDFDocument4 pagesDPR Offer Letter PDFSohel AnsariNo ratings yet

- FMCC225 - Financial Accounting 3 Final Examination 1 Sem. S/Y 2020-20221 Name: - Section: - Multiple ChoiceDocument3 pagesFMCC225 - Financial Accounting 3 Final Examination 1 Sem. S/Y 2020-20221 Name: - Section: - Multiple ChoiceChristian QuidipNo ratings yet

- Module 4 Assessment Task - Employee BenefitsDocument2 pagesModule 4 Assessment Task - Employee BenefitsRonnah Mae FloresNo ratings yet

- Accounting For Postemplyoment BenefitDocument9 pagesAccounting For Postemplyoment BenefitJoana MarieNo ratings yet

- Postemployment BenefitsDocument22 pagesPostemployment BenefitsChoco ButternutNo ratings yet

- Take Home Activity 3Document6 pagesTake Home Activity 3Justine CruzNo ratings yet

- IND 14 CHP 13 2 Homework Sol RETIREMENT Combined 2014Document8 pagesIND 14 CHP 13 2 Homework Sol RETIREMENT Combined 2014Nada Mucho100% (1)

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- AK1 - PensionDocument4 pagesAK1 - Pensionclara_patricia_2No ratings yet

- Quiz 4Document7 pagesQuiz 4Vivienne Rozenn LaytoNo ratings yet

- Module 1 - Employee BenefitsDocument38 pagesModule 1 - Employee BenefitsMitchie Faustino100% (1)

- Joyce Anne Luna BSA401Document12 pagesJoyce Anne Luna BSA401kathpremsNo ratings yet

- I. Theories. Choose The Letter of The BEST Answer. No Erasures On Final AnswersDocument5 pagesI. Theories. Choose The Letter of The BEST Answer. No Erasures On Final AnswersSheena CalderonNo ratings yet

- Learning Resource 12. Lesson 1Document8 pagesLearning Resource 12. Lesson 1Remedios Capistrano CatacutanNo ratings yet

- 221 ExamsDocument10 pages221 ExamsElla Mae AgoniaNo ratings yet

- Practice Exam For PensionDocument10 pagesPractice Exam For PensionDiandra Aditya KusumawardhaniNo ratings yet

- Accounting 4 - Employee Benefits Computational - PDF - ... : End of PreviewDocument1 pageAccounting 4 - Employee Benefits Computational - PDF - ... : End of Previewfreymart18No ratings yet

- FBT FinalDocument28 pagesFBT Finalmendonesmariza2No ratings yet

- Ia Review Final ExamDocument42 pagesIa Review Final ExamMitchie FaustinoNo ratings yet

- Cfas Quiz Pas 19Document5 pagesCfas Quiz Pas 19Michaella NudoNo ratings yet

- Unit 03Document9 pagesUnit 03bobo tangaNo ratings yet

- Self Employment Guidance - Form 1040 Schedule C IndividualsDocument2 pagesSelf Employment Guidance - Form 1040 Schedule C IndividualsGlenda100% (2)

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsKezNo ratings yet

- CPP EI IT CalculationDocument4 pagesCPP EI IT CalculationirfanNo ratings yet

- Module 12 - PAS 19 Employee BenefitsDocument6 pagesModule 12 - PAS 19 Employee BenefitsAKIO HIROKINo ratings yet

- IAS 19 Employee BenefitsDocument5 pagesIAS 19 Employee Benefitshae1234No ratings yet

- Chapter 5 Employee BenefitsDocument29 pagesChapter 5 Employee BenefitsDudz MatienzoNo ratings yet

- MODULE Midterm FAR 3 EmpBenefitsDocument15 pagesMODULE Midterm FAR 3 EmpBenefitsJohn Mark FernandoNo ratings yet

- Employee Benefits: Cruz, Jerica May A. CBET-01-501EDocument21 pagesEmployee Benefits: Cruz, Jerica May A. CBET-01-501Eclara san miguelNo ratings yet

- Esmerah Lika B. Ilatan BSA-3: Assignment Postemployment BenefitsDocument3 pagesEsmerah Lika B. Ilatan BSA-3: Assignment Postemployment BenefitsKakay AccireNo ratings yet

- Ias 19Document43 pagesIas 19Reever RiverNo ratings yet

- FY12 New Comp PlanDocument6 pagesFY12 New Comp PlanhousingworksNo ratings yet

- IAS 19 Employee BenefitsDocument32 pagesIAS 19 Employee BenefitsTamirat Eshetu WoldeNo ratings yet

- Compensation and Fringe Benefits TaxDocument10 pagesCompensation and Fringe Benefits TaxJane TuazonNo ratings yet

- Instruction: You Will Be Acting As A Junior Tax Accountant Who Has Just Started Working inDocument3 pagesInstruction: You Will Be Acting As A Junior Tax Accountant Who Has Just Started Working inleshz zynNo ratings yet

- Post Retirement BenefitsDocument4 pagesPost Retirement BenefitsWill Emmanuel A PinoyNo ratings yet

- 05M Fringe BenefitDocument4 pages05M Fringe BenefitMarko IllustrisimoNo ratings yet

- Handouts PDFDocument129 pagesHandouts PDFRomulus GarciaNo ratings yet

- 19 Employee Benefits s20 FinalDocument18 pages19 Employee Benefits s20 FinalMalcolmNo ratings yet

- Accounting For Employment BenefitsDocument5 pagesAccounting For Employment BenefitsiamacrusaderNo ratings yet

- LKAS 19 2021 UploadDocument31 pagesLKAS 19 2021 Uploadpriyantha dasanayake100% (2)

- Module 3 Packet: College of CommerceDocument21 pagesModule 3 Packet: College of CommerceDexie Jane MayoNo ratings yet

- Employee BenefitsDocument4 pagesEmployee BenefitsJiberlen MoralesNo ratings yet

- Unit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Other Employee BenefitsDocument7 pagesUnit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Other Employee BenefitsJason MablesNo ratings yet

- IAS 19 NotesDocument15 pagesIAS 19 NotesArsalan AliNo ratings yet

- Group Work #1 With SolutionsDocument3 pagesGroup Work #1 With SolutionsShadi MorakabatiNo ratings yet

- Chapter 17 Ia2 No ProblemsDocument23 pagesChapter 17 Ia2 No ProblemsJM Valonda Villena, CPA, MBANo ratings yet

- Ias 19Document9 pagesIas 19Hammad SarwarNo ratings yet

- 104 Accounting QuizDocument3 pages104 Accounting Quizhyunsuk fhebieNo ratings yet

- M10 Employee BenefitsDocument51 pagesM10 Employee BenefitsbelijobNo ratings yet

- FAR ProblemsDocument7 pagesFAR ProblemsClaire GarciaNo ratings yet

- Name - Course & Yr. - Schedule - Score - Test I. Multiple Choice. Encircle The Letter of The Best Answer in Each of The Given Question/sDocument11 pagesName - Course & Yr. - Schedule - Score - Test I. Multiple Choice. Encircle The Letter of The Best Answer in Each of The Given Question/sAtty CpaNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- Forward Budgeting: A Paperless and Electronic Household Budget SystemFrom EverandForward Budgeting: A Paperless and Electronic Household Budget SystemNo ratings yet

- Law11 - Module 4 - Mahusay, Jeth A.Document4 pagesLaw11 - Module 4 - Mahusay, Jeth A.Jeth MahusayNo ratings yet

- Mahusay Acc3112 Major Output 3Document4 pagesMahusay Acc3112 Major Output 3Jeth MahusayNo ratings yet

- Mahusay Acc3112 Major Output 1Document4 pagesMahusay Acc3112 Major Output 1Jeth MahusayNo ratings yet

- Mahusay Module 1 - Acc4115Document1 pageMahusay Module 1 - Acc4115Jeth MahusayNo ratings yet

- Mahusay Module 2 - Acc4115Document5 pagesMahusay Module 2 - Acc4115Jeth MahusayNo ratings yet

- Mahusay Module 4 - Acc4115Document4 pagesMahusay Module 4 - Acc4115Jeth MahusayNo ratings yet

- Mahusay - Acc319 - Module 2 Major OutputDocument2 pagesMahusay - Acc319 - Module 2 Major OutputJeth MahusayNo ratings yet

- Mahusay-Pe2 Lesson 4Document2 pagesMahusay-Pe2 Lesson 4Jeth MahusayNo ratings yet

- Mahusay Acc227 Module 4Document4 pagesMahusay Acc227 Module 4Jeth MahusayNo ratings yet

- Mahusay - G - Ai, PortfolioDocument15 pagesMahusay - G - Ai, PortfolioJeth MahusayNo ratings yet

- Mahusay-Pe2 Lesson 3Document1 pageMahusay-Pe2 Lesson 3Jeth MahusayNo ratings yet

- Acc 227 Intermediate Accounting 2 CSGDocument58 pagesAcc 227 Intermediate Accounting 2 CSGJeth MahusayNo ratings yet

- Mahusay - G-Ai Module 3Document8 pagesMahusay - G-Ai Module 3Jeth MahusayNo ratings yet

- Mahusay Acc227 Module 2Document9 pagesMahusay Acc227 Module 2Jeth MahusayNo ratings yet

- Mahusay Acc227 Module 1Document12 pagesMahusay Acc227 Module 1Jeth MahusayNo ratings yet

- Mahusay - Acc319 - Module 4 Major OutputDocument3 pagesMahusay - Acc319 - Module 4 Major OutputJeth Mahusay100% (3)

- Mahusay - Acc319 - Module 3 Major OutputDocument4 pagesMahusay - Acc319 - Module 3 Major OutputJeth MahusayNo ratings yet

- MAHUSAYLAW211 REFLECTIVE ESSAY - Module 4Document4 pagesMAHUSAYLAW211 REFLECTIVE ESSAY - Module 4Jeth MahusayNo ratings yet

- One Person CorporationDocument3 pagesOne Person CorporationJeth MahusayNo ratings yet

- Mahusay Law211 Articles of CooperationDocument10 pagesMahusay Law211 Articles of CooperationJeth MahusayNo ratings yet

- MAHUSAYLAW211 REFLECTIVE ESSAY - Module 3Document3 pagesMAHUSAYLAW211 REFLECTIVE ESSAY - Module 3Jeth MahusayNo ratings yet

- MAHUSAYLAW211 REFLECTIVE ESSAY - Formation of PartnershipDocument4 pagesMAHUSAYLAW211 REFLECTIVE ESSAY - Formation of PartnershipJeth MahusayNo ratings yet

- Mahusay Law211 Articles of PartnershipDocument2 pagesMahusay Law211 Articles of PartnershipJeth MahusayNo ratings yet

- MAHUSAYLAW211 REFLECTIVE ESSAY - Module 2Document4 pagesMAHUSAYLAW211 REFLECTIVE ESSAY - Module 2Jeth MahusayNo ratings yet

- Mahusay Law211 Articles of IncorporationDocument4 pagesMahusay Law211 Articles of IncorporationJeth MahusayNo ratings yet

- SCALP Handout 044Document10 pagesSCALP Handout 044Angelica PatagNo ratings yet

- Scale DeductionDocument9 pagesScale DeductionWaqar AhmadNo ratings yet

- Contributions TDocument6 pagesContributions TRena Jocelle NalzaroNo ratings yet

- DTAA With USA PDFDocument23 pagesDTAA With USA PDFDehradun MootNo ratings yet

- PauslipDocument2 pagesPauslipAmanNo ratings yet

- (OPA - 01) Question Paper Limited Departmental Competitive Examination - 2006 For The Post of Chargeman-Gr - Ii (T) & (NT)Document8 pages(OPA - 01) Question Paper Limited Departmental Competitive Examination - 2006 For The Post of Chargeman-Gr - Ii (T) & (NT)Rohit Choudhari100% (1)

- File by Mail Instructions For Your 2020 Federal Tax ReturnDocument18 pagesFile by Mail Instructions For Your 2020 Federal Tax Returnrose owensNo ratings yet

- Income Tax Calulator With Computation of IncomeDocument18 pagesIncome Tax Calulator With Computation of IncomeSurendra DevadigaNo ratings yet

- Private Equity and Venture Capital: Term VDocument3 pagesPrivate Equity and Venture Capital: Term VJitesh Thakur100% (1)

- Accounting For LaborDocument35 pagesAccounting For LaborSophia kissesNo ratings yet

- Inclusions in Gross IncomeDocument4 pagesInclusions in Gross IncomeNaiza Mae R. BinayaoNo ratings yet

- Compensation System & Its ComponentsDocument28 pagesCompensation System & Its ComponentsSeema Pujari0% (1)

- Word Form 1Document2 pagesWord Form 1Đặng Thị QuýNo ratings yet

- Smart Swadhan Supreme Brochure - V01 17th Jan 1Document10 pagesSmart Swadhan Supreme Brochure - V01 17th Jan 1Nitin KumarNo ratings yet

- 401 (K) Planner: Growth of InvestmentDocument1 page401 (K) Planner: Growth of Investmentanon-13887100% (1)

- Basics of Income TaxDocument21 pagesBasics of Income TaxAvNo ratings yet

- Excerpts From The DECS Service Manual Chapter III - CherryDocument5 pagesExcerpts From The DECS Service Manual Chapter III - CherryKhemme Lapor Chu UbialNo ratings yet

- MCQ (Bold Correct Answer)Document13 pagesMCQ (Bold Correct Answer)Gauresh NaikNo ratings yet

- Taxation - Malawi (TX - Mwi) : Applied SkillsDocument15 pagesTaxation - Malawi (TX - Mwi) : Applied SkillsangaNo ratings yet

- Insurance Law ProjectDocument14 pagesInsurance Law ProjectSimran Kaur KhuranaNo ratings yet

- Employee'S Provident Fund Organisation: Electronic Challan Cum Return (Ecr)Document13 pagesEmployee'S Provident Fund Organisation: Electronic Challan Cum Return (Ecr)Suraj Dev MahatoNo ratings yet

- CISF 914 Constable Tradesmen Posts (WWW - Majhinaukri.in)Document40 pagesCISF 914 Constable Tradesmen Posts (WWW - Majhinaukri.in)Pratik YadavNo ratings yet

- Anusha Yenishetty PDFDocument2 pagesAnusha Yenishetty PDFSrinivasa Rao JagarapuNo ratings yet

- Instructions For Form 1040NR-EZ: Department of The TreasuryDocument11 pagesInstructions For Form 1040NR-EZ: Department of The TreasuryIRSNo ratings yet

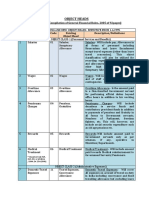

- Object Head List PDFDocument6 pagesObject Head List PDFLal ZahawmaNo ratings yet

- 04-Chap2-Chart of Accounts-2022-2023-S1Document1 page04-Chap2-Chart of Accounts-2022-2023-S1Lilly ChanNo ratings yet

- Business MathematicsDocument2 pagesBusiness MathematicsJoh Na AlvaradoNo ratings yet

- Trifon B. Tumaodos vs. San Miguel Yamamura Packaging Cooperation FactsDocument2 pagesTrifon B. Tumaodos vs. San Miguel Yamamura Packaging Cooperation FactsRajkumari100% (1)

- 2 - CTA Paper IIIDocument18 pages2 - CTA Paper IIIMahmozNo ratings yet