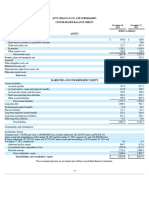

Relationship Between Dividend Policy and Corporate Financial Performance

Relationship Between Dividend Policy and Corporate Financial Performance

You might also like

- Gateway Computers Case InformationDocument5 pagesGateway Computers Case InformationShahrukh FaheemNo ratings yet

- Chapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining AfterDocument12 pagesChapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining Aftermubarek oumerNo ratings yet

- Strengths:: Questions For The Case AnalysysDocument1 pageStrengths:: Questions For The Case AnalysysCesarNo ratings yet

- 1.1 BackgroundDocument11 pages1.1 BackgroundBayalkotee ReshamNo ratings yet

- CFA Level II Cheat Sheet: Equity Fixed IncomeDocument1 pageCFA Level II Cheat Sheet: Equity Fixed Incomeapi-19918095No ratings yet

- Dividend PolicyDocument10 pagesDividend PolicyShivam MalhotraNo ratings yet

- Business Com MM Final LL LLLLLDocument16 pagesBusiness Com MM Final LL LLLLLSamihaSaanNo ratings yet

- Dividend Is That Portion of Profits of A Company Which Is DistributableDocument25 pagesDividend Is That Portion of Profits of A Company Which Is DistributableCma Pushparaj KulkarniNo ratings yet

- Dividend Policy ProposalDocument22 pagesDividend Policy Proposalroman50% (4)

- Question and Answer - 52Document31 pagesQuestion and Answer - 52acc-expertNo ratings yet

- A Critical Analysis On The Impact of Dividend Policy On The Value of The FirmDocument95 pagesA Critical Analysis On The Impact of Dividend Policy On The Value of The Firmnaz100% (3)

- Project On Impact of Dividends PolicyDocument45 pagesProject On Impact of Dividends Policyarjunmba119624100% (1)

- Chapter TwoDocument21 pagesChapter TwoPhilip AsareNo ratings yet

- Dividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeDocument4 pagesDividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeMUZNANo ratings yet

- Dividend Policy of Kumari Bank LimitedDocument6 pagesDividend Policy of Kumari Bank LimitedArjun100% (1)

- CHAPTER 1,2 and 3 GodspowerDocument40 pagesCHAPTER 1,2 and 3 GodspowerprincealaseiworimaNo ratings yet

- 5 005TCY FinalDocument8 pages5 005TCY Finalmaruzaks123No ratings yet

- Chapter-II Literature ReviewDocument32 pagesChapter-II Literature Reviewbikash ranaNo ratings yet

- Project On Impact of Dividends Policy 1Document43 pagesProject On Impact of Dividends Policy 1Soma BanikNo ratings yet

- Dividend PolicyDocument7 pagesDividend PolicyImran AhsanNo ratings yet

- Finance 1 DineshDocument15 pagesFinance 1 Dineshdinesh-mathew-5072No ratings yet

- Impact of Dividend Policy On A Firm PerformanceDocument11 pagesImpact of Dividend Policy On A Firm PerformanceMuhammad AnasNo ratings yet

- Chapter-I: 1.1 Background of The StudyDocument10 pagesChapter-I: 1.1 Background of The StudyAnonymous NpglhCs1JNo ratings yet

- Chapter 6 of SBRDocument88 pagesChapter 6 of SBRAnoj KoiralaNo ratings yet

- Dividend Analysis at India Bulls: Project Report ON " "Document77 pagesDividend Analysis at India Bulls: Project Report ON " "Sankar BukkapatnamNo ratings yet

- Interindustry Dividend Policy Determinants in The Context of An Emerging MarketDocument6 pagesInterindustry Dividend Policy Determinants in The Context of An Emerging MarketChaudhary AliNo ratings yet

- Background On DividendsDocument3 pagesBackground On DividendsGustafaGovachefMotivati0% (1)

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Impact of Firm Specific Variables On Dividend Payout of Nepalese BanksDocument13 pagesImpact of Firm Specific Variables On Dividend Payout of Nepalese BanksMani ManandharNo ratings yet

- Study of Dividend Policy Adopted by Companies: Master of Business AdministrationDocument125 pagesStudy of Dividend Policy Adopted by Companies: Master of Business AdministrationtechcaresystemNo ratings yet

- Firm Performance Paper 4Document10 pagesFirm Performance Paper 4kabir khanNo ratings yet

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342No ratings yet

- Impact of Dividend Policy On Share PricesDocument16 pagesImpact of Dividend Policy On Share PricesAli JarralNo ratings yet

- Impact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorDocument9 pagesImpact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorHarish.PNo ratings yet

- Assignment Pengurusan Kewangan 2Document13 pagesAssignment Pengurusan Kewangan 2william tangNo ratings yet

- 209-2nd ICBER 2011 PG 945-976 Dividend PolicyDocument32 pages209-2nd ICBER 2011 PG 945-976 Dividend PolicyRajita EconomisteNo ratings yet

- My Complete ThesisDocument98 pagesMy Complete ThesisKolabenNo ratings yet

- DD Icici UppalDocument14 pagesDD Icici Uppalferoz khanNo ratings yet

- DividendDocument30 pagesDividendFaruqNo ratings yet

- Dividend Policy of Everest Bank Limited: A Thesis Proposal byDocument9 pagesDividend Policy of Everest Bank Limited: A Thesis Proposal byRam khadkaNo ratings yet

- R Dividend Policy A Comparative Study of UK and Bangladesh Based Companies PDFDocument16 pagesR Dividend Policy A Comparative Study of UK and Bangladesh Based Companies PDFfahim zamanNo ratings yet

- Nnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredDocument20 pagesNnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredismailNo ratings yet

- 34682compilerfinal SFM n03n13 Cp1Document3 pages34682compilerfinal SFM n03n13 Cp1casarokarNo ratings yet

- Factors Affecting Dividend Policy Empirical Study From Pharmaceutical's Companies in PakistanDocument6 pagesFactors Affecting Dividend Policy Empirical Study From Pharmaceutical's Companies in PakistanJkn PalembangNo ratings yet

- Research Project: Prasanna HegdeDocument68 pagesResearch Project: Prasanna Hegdethakur101No ratings yet

- 2) The Effect of Dividend Policy On Corporate Financial PerformanceDocument4 pages2) The Effect of Dividend Policy On Corporate Financial PerformanceolsaNo ratings yet

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanNo ratings yet

- ResearchDocument21 pagesResearchAizaz AliNo ratings yet

- The Effect of Dividend Policy On Stock Price Volatility and Investment DecisionsDocument9 pagesThe Effect of Dividend Policy On Stock Price Volatility and Investment DecisionsPawanNo ratings yet

- Dividend Policy A Comparative Study of UK and Bangladesh Based CompaniesDocument16 pagesDividend Policy A Comparative Study of UK and Bangladesh Based CompaniesMehedi HasanNo ratings yet

- Dividend Policy of Indian Corporate FirmsDocument19 pagesDividend Policy of Indian Corporate FirmsRoads Sub Division-I,PuriNo ratings yet

- Impact of Dividend PolicyDocument12 pagesImpact of Dividend PolicyGarimaNo ratings yet

- The Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDocument34 pagesThe Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDevikaNo ratings yet

- Devidend Policy - Izzah M Sechimil 190810201004Document7 pagesDevidend Policy - Izzah M Sechimil 190810201004izzah mariamiNo ratings yet

- Why Dividends Are PaidDocument6 pagesWhy Dividends Are PaidDeranga De SilvaNo ratings yet

- Determinants of Dividend Policy: A Study of Sensex Incorporated CompaniesDocument7 pagesDeterminants of Dividend Policy: A Study of Sensex Incorporated CompaniesInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Factors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeDocument14 pagesFactors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeWindaNo ratings yet

- Submitted For: Course Title: Course CodeDocument15 pagesSubmitted For: Course Title: Course CodeDedar HossainNo ratings yet

- 4 CB 8Document9 pages4 CB 8maruzaks123No ratings yet

- Pengaruh Struktur Kepemilikan Terhadap Keputusan Keuangan Dan Nilai PerusahaanDocument29 pagesPengaruh Struktur Kepemilikan Terhadap Keputusan Keuangan Dan Nilai PerusahaanFajar ChristianNo ratings yet

- Impact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesDocument4 pagesImpact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesSyed Ameer HayderNo ratings yet

- Report On Impacts of DividendDocument16 pagesReport On Impacts of Dividendtajul1994bd_69738436No ratings yet

- Bajaj FinanceDocument10 pagesBajaj FinanceJeniffer RayenNo ratings yet

- Impactof Capitalstructureon Financial PerformanceanditsdeterminantsDocument11 pagesImpactof Capitalstructureon Financial PerformanceanditsdeterminantsLehar GabaNo ratings yet

- CH 25Document42 pagesCH 25Maybelle BernalNo ratings yet

- Fundamental Concepts of Managerial AccountingDocument45 pagesFundamental Concepts of Managerial AccountingCarlo CanlasNo ratings yet

- IDirect EIH Q3FY22Document9 pagesIDirect EIH Q3FY22Parag SaxenaNo ratings yet

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanNo ratings yet

- Fin315 - Business Finance Chapter 10 and 11 NAME (PLEASE PRINT)Document8 pagesFin315 - Business Finance Chapter 10 and 11 NAME (PLEASE PRINT)Ryan Xuan0% (1)

- Financial Statement Analysis of Jollibee Food Corporation and Max's Group IncDocument17 pagesFinancial Statement Analysis of Jollibee Food Corporation and Max's Group IncRem100% (1)

- Dabur India: Valuations Turn Attractive Upgrade To BuyDocument6 pagesDabur India: Valuations Turn Attractive Upgrade To BuyanirbanmNo ratings yet

- Chapter 2 Corporate LendingDocument24 pagesChapter 2 Corporate LendingRishi SharmaNo ratings yet

- Chapter 9 PDFDocument29 pagesChapter 9 PDFYhunie Nhita Itha50% (2)

- CAPE Accounting 2016 U1 P1Document10 pagesCAPE Accounting 2016 U1 P1DinaNo ratings yet

- Capital Structure: Financial DistressDocument22 pagesCapital Structure: Financial DistressAniket KaushikNo ratings yet

- 4 BSN Micro - I Application Form SPM - APD 070722Document4 pages4 BSN Micro - I Application Form SPM - APD 070722水晶宛宜No ratings yet

- Ece Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Document8 pagesEce Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Tejesh GoudNo ratings yet

- Levi Strauss & Co Fs 2023Document6 pagesLevi Strauss & Co Fs 2023Info Riskma SolutionsNo ratings yet

- Book BuildingDocument19 pagesBook Buildingmonilsonaiya_91No ratings yet

- 1 Financial Statements AnalysisDocument5 pages1 Financial Statements AnalysisMark Lawrence YusiNo ratings yet

- Strategic Cost Management QuizDocument9 pagesStrategic Cost Management Quizctarenas.studentNo ratings yet

- Blue Balance Sheet1Document4 pagesBlue Balance Sheet1shanizaNo ratings yet

- Revision Test Paper CAP II Dec 2017Document163 pagesRevision Test Paper CAP II Dec 2017Dipen AdhikariNo ratings yet

- Pearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test BankDocument45 pagesPearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test Bankloanazura7k6bl100% (32)

- CB Niat 2019 Exam SolutionsDocument14 pagesCB Niat 2019 Exam Solutionsdean garciaNo ratings yet

- Accounting Tutorial 1Document5 pagesAccounting Tutorial 1Sim Pei YingNo ratings yet

- Unit - 1 Topic 3 RevisionDocument27 pagesUnit - 1 Topic 3 RevisionSomebodyNo ratings yet

- Dwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFDocument36 pagesDwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFjayden77evans100% (18)

- Final Report 21BCM1553Document45 pagesFinal Report 21BCM1553Guljeet SinghNo ratings yet

- Discovering A Wealth Creator Portfolio: Article by Maneesh NathDocument4 pagesDiscovering A Wealth Creator Portfolio: Article by Maneesh NathCen ParNo ratings yet

Download as docx, pdf, or txt

You might also like

- Gateway Computers Case InformationDocument5 pagesGateway Computers Case InformationShahrukh FaheemNo ratings yet

- Chapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining AfterDocument12 pagesChapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining Aftermubarek oumerNo ratings yet

- Strengths:: Questions For The Case AnalysysDocument1 pageStrengths:: Questions For The Case AnalysysCesarNo ratings yet

- 1.1 BackgroundDocument11 pages1.1 BackgroundBayalkotee ReshamNo ratings yet

- CFA Level II Cheat Sheet: Equity Fixed IncomeDocument1 pageCFA Level II Cheat Sheet: Equity Fixed Incomeapi-19918095No ratings yet

- Dividend PolicyDocument10 pagesDividend PolicyShivam MalhotraNo ratings yet

- Business Com MM Final LL LLLLLDocument16 pagesBusiness Com MM Final LL LLLLLSamihaSaanNo ratings yet

- Dividend Is That Portion of Profits of A Company Which Is DistributableDocument25 pagesDividend Is That Portion of Profits of A Company Which Is DistributableCma Pushparaj KulkarniNo ratings yet

- Dividend Policy ProposalDocument22 pagesDividend Policy Proposalroman50% (4)

- Question and Answer - 52Document31 pagesQuestion and Answer - 52acc-expertNo ratings yet

- A Critical Analysis On The Impact of Dividend Policy On The Value of The FirmDocument95 pagesA Critical Analysis On The Impact of Dividend Policy On The Value of The Firmnaz100% (3)

- Project On Impact of Dividends PolicyDocument45 pagesProject On Impact of Dividends Policyarjunmba119624100% (1)

- Chapter TwoDocument21 pagesChapter TwoPhilip AsareNo ratings yet

- Dividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeDocument4 pagesDividend Policy and Firm Performance: A Study of Listed Firms On National Stock ExchangeMUZNANo ratings yet

- Dividend Policy of Kumari Bank LimitedDocument6 pagesDividend Policy of Kumari Bank LimitedArjun100% (1)

- CHAPTER 1,2 and 3 GodspowerDocument40 pagesCHAPTER 1,2 and 3 GodspowerprincealaseiworimaNo ratings yet

- 5 005TCY FinalDocument8 pages5 005TCY Finalmaruzaks123No ratings yet

- Chapter-II Literature ReviewDocument32 pagesChapter-II Literature Reviewbikash ranaNo ratings yet

- Project On Impact of Dividends Policy 1Document43 pagesProject On Impact of Dividends Policy 1Soma BanikNo ratings yet

- Dividend PolicyDocument7 pagesDividend PolicyImran AhsanNo ratings yet

- Finance 1 DineshDocument15 pagesFinance 1 Dineshdinesh-mathew-5072No ratings yet

- Impact of Dividend Policy On A Firm PerformanceDocument11 pagesImpact of Dividend Policy On A Firm PerformanceMuhammad AnasNo ratings yet

- Chapter-I: 1.1 Background of The StudyDocument10 pagesChapter-I: 1.1 Background of The StudyAnonymous NpglhCs1JNo ratings yet

- Chapter 6 of SBRDocument88 pagesChapter 6 of SBRAnoj KoiralaNo ratings yet

- Dividend Analysis at India Bulls: Project Report ON " "Document77 pagesDividend Analysis at India Bulls: Project Report ON " "Sankar BukkapatnamNo ratings yet

- Interindustry Dividend Policy Determinants in The Context of An Emerging MarketDocument6 pagesInterindustry Dividend Policy Determinants in The Context of An Emerging MarketChaudhary AliNo ratings yet

- Background On DividendsDocument3 pagesBackground On DividendsGustafaGovachefMotivati0% (1)

- Subba ReddyDocument47 pagesSubba Reddyankitjaipur0% (1)

- Impact of Firm Specific Variables On Dividend Payout of Nepalese BanksDocument13 pagesImpact of Firm Specific Variables On Dividend Payout of Nepalese BanksMani ManandharNo ratings yet

- Study of Dividend Policy Adopted by Companies: Master of Business AdministrationDocument125 pagesStudy of Dividend Policy Adopted by Companies: Master of Business AdministrationtechcaresystemNo ratings yet

- Firm Performance Paper 4Document10 pagesFirm Performance Paper 4kabir khanNo ratings yet

- Dividend Policy As Strategic Tool of Financing in Public Firms: Evidence From NigeriaDocument24 pagesDividend Policy As Strategic Tool of Financing in Public Firms: Evidence From Nigeriay_378602342No ratings yet

- Impact of Dividend Policy On Share PricesDocument16 pagesImpact of Dividend Policy On Share PricesAli JarralNo ratings yet

- Impact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorDocument9 pagesImpact of Dividend Policy On Share Price: A Study On Selected Stocks From Manufacturing SectorHarish.PNo ratings yet

- Assignment Pengurusan Kewangan 2Document13 pagesAssignment Pengurusan Kewangan 2william tangNo ratings yet

- 209-2nd ICBER 2011 PG 945-976 Dividend PolicyDocument32 pages209-2nd ICBER 2011 PG 945-976 Dividend PolicyRajita EconomisteNo ratings yet

- My Complete ThesisDocument98 pagesMy Complete ThesisKolabenNo ratings yet

- DD Icici UppalDocument14 pagesDD Icici Uppalferoz khanNo ratings yet

- DividendDocument30 pagesDividendFaruqNo ratings yet

- Dividend Policy of Everest Bank Limited: A Thesis Proposal byDocument9 pagesDividend Policy of Everest Bank Limited: A Thesis Proposal byRam khadkaNo ratings yet

- R Dividend Policy A Comparative Study of UK and Bangladesh Based Companies PDFDocument16 pagesR Dividend Policy A Comparative Study of UK and Bangladesh Based Companies PDFfahim zamanNo ratings yet

- Nnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredDocument20 pagesNnadi Et Tanna 2011 Multivariate Analyses of Factors Affecting Dividend Policy of AcquiredismailNo ratings yet

- 34682compilerfinal SFM n03n13 Cp1Document3 pages34682compilerfinal SFM n03n13 Cp1casarokarNo ratings yet

- Factors Affecting Dividend Policy Empirical Study From Pharmaceutical's Companies in PakistanDocument6 pagesFactors Affecting Dividend Policy Empirical Study From Pharmaceutical's Companies in PakistanJkn PalembangNo ratings yet

- Research Project: Prasanna HegdeDocument68 pagesResearch Project: Prasanna Hegdethakur101No ratings yet

- 2) The Effect of Dividend Policy On Corporate Financial PerformanceDocument4 pages2) The Effect of Dividend Policy On Corporate Financial PerformanceolsaNo ratings yet

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanNo ratings yet

- ResearchDocument21 pagesResearchAizaz AliNo ratings yet

- The Effect of Dividend Policy On Stock Price Volatility and Investment DecisionsDocument9 pagesThe Effect of Dividend Policy On Stock Price Volatility and Investment DecisionsPawanNo ratings yet

- Dividend Policy A Comparative Study of UK and Bangladesh Based CompaniesDocument16 pagesDividend Policy A Comparative Study of UK and Bangladesh Based CompaniesMehedi HasanNo ratings yet

- Dividend Policy of Indian Corporate FirmsDocument19 pagesDividend Policy of Indian Corporate FirmsRoads Sub Division-I,PuriNo ratings yet

- Impact of Dividend PolicyDocument12 pagesImpact of Dividend PolicyGarimaNo ratings yet

- The Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDocument34 pagesThe Impact of Dividend Policy On Firm Performance Under High or Low Leverage Evidence From PakistanDevikaNo ratings yet

- Devidend Policy - Izzah M Sechimil 190810201004Document7 pagesDevidend Policy - Izzah M Sechimil 190810201004izzah mariamiNo ratings yet

- Why Dividends Are PaidDocument6 pagesWhy Dividends Are PaidDeranga De SilvaNo ratings yet

- Determinants of Dividend Policy: A Study of Sensex Incorporated CompaniesDocument7 pagesDeterminants of Dividend Policy: A Study of Sensex Incorporated CompaniesInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Factors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeDocument14 pagesFactors Affecting Dividend Policy in Manufacturing Companies in Indonesia Stock ExchangeWindaNo ratings yet

- Submitted For: Course Title: Course CodeDocument15 pagesSubmitted For: Course Title: Course CodeDedar HossainNo ratings yet

- 4 CB 8Document9 pages4 CB 8maruzaks123No ratings yet

- Pengaruh Struktur Kepemilikan Terhadap Keputusan Keuangan Dan Nilai PerusahaanDocument29 pagesPengaruh Struktur Kepemilikan Terhadap Keputusan Keuangan Dan Nilai PerusahaanFajar ChristianNo ratings yet

- Impact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesDocument4 pagesImpact of Financial Leverage On Dividend Policy Evidence From Islamabad Stock Exchange Listed CompaniesSyed Ameer HayderNo ratings yet

- Report On Impacts of DividendDocument16 pagesReport On Impacts of Dividendtajul1994bd_69738436No ratings yet

- Bajaj FinanceDocument10 pagesBajaj FinanceJeniffer RayenNo ratings yet

- Impactof Capitalstructureon Financial PerformanceanditsdeterminantsDocument11 pagesImpactof Capitalstructureon Financial PerformanceanditsdeterminantsLehar GabaNo ratings yet

- CH 25Document42 pagesCH 25Maybelle BernalNo ratings yet

- Fundamental Concepts of Managerial AccountingDocument45 pagesFundamental Concepts of Managerial AccountingCarlo CanlasNo ratings yet

- IDirect EIH Q3FY22Document9 pagesIDirect EIH Q3FY22Parag SaxenaNo ratings yet

- "Dividend Decision": Synopsis OnDocument14 pages"Dividend Decision": Synopsis Onferoz khanNo ratings yet

- Fin315 - Business Finance Chapter 10 and 11 NAME (PLEASE PRINT)Document8 pagesFin315 - Business Finance Chapter 10 and 11 NAME (PLEASE PRINT)Ryan Xuan0% (1)

- Financial Statement Analysis of Jollibee Food Corporation and Max's Group IncDocument17 pagesFinancial Statement Analysis of Jollibee Food Corporation and Max's Group IncRem100% (1)

- Dabur India: Valuations Turn Attractive Upgrade To BuyDocument6 pagesDabur India: Valuations Turn Attractive Upgrade To BuyanirbanmNo ratings yet

- Chapter 2 Corporate LendingDocument24 pagesChapter 2 Corporate LendingRishi SharmaNo ratings yet

- Chapter 9 PDFDocument29 pagesChapter 9 PDFYhunie Nhita Itha50% (2)

- CAPE Accounting 2016 U1 P1Document10 pagesCAPE Accounting 2016 U1 P1DinaNo ratings yet

- Capital Structure: Financial DistressDocument22 pagesCapital Structure: Financial DistressAniket KaushikNo ratings yet

- 4 BSN Micro - I Application Form SPM - APD 070722Document4 pages4 BSN Micro - I Application Form SPM - APD 070722水晶宛宜No ratings yet

- Ece Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Document8 pagesEce Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Tejesh GoudNo ratings yet

- Levi Strauss & Co Fs 2023Document6 pagesLevi Strauss & Co Fs 2023Info Riskma SolutionsNo ratings yet

- Book BuildingDocument19 pagesBook Buildingmonilsonaiya_91No ratings yet

- 1 Financial Statements AnalysisDocument5 pages1 Financial Statements AnalysisMark Lawrence YusiNo ratings yet

- Strategic Cost Management QuizDocument9 pagesStrategic Cost Management Quizctarenas.studentNo ratings yet

- Blue Balance Sheet1Document4 pagesBlue Balance Sheet1shanizaNo ratings yet

- Revision Test Paper CAP II Dec 2017Document163 pagesRevision Test Paper CAP II Dec 2017Dipen AdhikariNo ratings yet

- Pearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test BankDocument45 pagesPearsons Federal Taxation 2018 Comprehensive 31st Edition Rupert Test Bankloanazura7k6bl100% (32)

- CB Niat 2019 Exam SolutionsDocument14 pagesCB Niat 2019 Exam Solutionsdean garciaNo ratings yet

- Accounting Tutorial 1Document5 pagesAccounting Tutorial 1Sim Pei YingNo ratings yet

- Unit - 1 Topic 3 RevisionDocument27 pagesUnit - 1 Topic 3 RevisionSomebodyNo ratings yet

- Dwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFDocument36 pagesDwnload Full Cornerstones of Financial Accounting Canadian 1st Edition Rich Solutions Manual PDFjayden77evans100% (18)

- Final Report 21BCM1553Document45 pagesFinal Report 21BCM1553Guljeet SinghNo ratings yet

- Discovering A Wealth Creator Portfolio: Article by Maneesh NathDocument4 pagesDiscovering A Wealth Creator Portfolio: Article by Maneesh NathCen ParNo ratings yet