Value For Money Article

Value For Money Article

You might also like

- Tire City IncDocument3 pagesTire City IncAlberto RcNo ratings yet

- Insights From The Balanced Scorecard An Introduction To The Enterprise Risk ScorecardDocument11 pagesInsights From The Balanced Scorecard An Introduction To The Enterprise Risk ScorecardEngMohamedReyadHelesyNo ratings yet

- Activity Based Costing ProjectDocument26 pagesActivity Based Costing Projectm_lohani100% (2)

- Value and RiskmanagementDocument11 pagesValue and RiskmanagementShonette ThomasNo ratings yet

- 2010 Lean Knowledge MGMNT The Problem of ValueDocument10 pages2010 Lean Knowledge MGMNT The Problem of Valuenetcat72984No ratings yet

- KPK - Research - Digest - VE - and - VM - Any - Difference - July - 2012 PDFDocument4 pagesKPK - Research - Digest - VE - and - VM - Any - Difference - July - 2012 PDFravibc9367No ratings yet

- González-Prida2019 Chapter AnApproachToQuantifyValueProviDocument8 pagesGonzález-Prida2019 Chapter AnApproachToQuantifyValueProviRosendo LopezNo ratings yet

- Facility Management Value Dimensions FroDocument15 pagesFacility Management Value Dimensions FroMUBANGIZI FELEXNo ratings yet

- Achieving Value For Money (VFM) in Construction ProjectsDocument11 pagesAchieving Value For Money (VFM) in Construction Projectsolatos4jesusNo ratings yet

- KPK Research Digest VE and VM Any Difference July 2012Document4 pagesKPK Research Digest VE and VM Any Difference July 2012danijulianaNo ratings yet

- Portfolio Decision QualityDocument25 pagesPortfolio Decision QualityDiegoNo ratings yet

- Operations in BankingDocument20 pagesOperations in BankingRakshit Chandra Shekhar JoshiNo ratings yet

- 01 - Zwikael - Project - Benefit - Management - 2014Document15 pages01 - Zwikael - Project - Benefit - Management - 2014Carlos BocanegraNo ratings yet

- Managing Project Investments Irreversibility by Accounting RelationsDocument9 pagesManaging Project Investments Irreversibility by Accounting RelationsNoviansyah PamungkasNo ratings yet

- Статья 3 хорошаяDocument18 pagesСтатья 3 хорошаяМаксим НовакNo ratings yet

- This Paper Is Short-Version of My Thesis. Full Thesis Is Available atDocument47 pagesThis Paper Is Short-Version of My Thesis. Full Thesis Is Available atjuz_nurulNo ratings yet

- JPM QES 2016 Harvard PDFDocument16 pagesJPM QES 2016 Harvard PDFSrinivas NemaniNo ratings yet

- Capital Budgeting TheoryDocument9 pagesCapital Budgeting TheoryyayaNo ratings yet

- Benchmarking Uk Government Procurement Performance in Construction ProjectsDocument9 pagesBenchmarking Uk Government Procurement Performance in Construction ProjectsmaazizNo ratings yet

- Knowledge Management For Small Occasional Construction Industry ClientsDocument9 pagesKnowledge Management For Small Occasional Construction Industry ClientsSonmar SonmarNo ratings yet

- Benefits of EvmDocument12 pagesBenefits of EvmMiraj ShahidNo ratings yet

- BRE-Whole Life Value-Sustainable Design in The Built EnvironmentDocument4 pagesBRE-Whole Life Value-Sustainable Design in The Built EnvironmentRoger MaierNo ratings yet

- Value For MoneyDocument6 pagesValue For Moneyselepelehlohonolo93No ratings yet

- Capital Budgeting Paper 2Document9 pagesCapital Budgeting Paper 2Abdul Rafay ButtNo ratings yet

- 7 Equity Valuation Using DCFDocument18 pages7 Equity Valuation Using DCFHuicai MaiNo ratings yet

- Warranty Cost Models State-Of-Art A Practical ReviewDocument10 pagesWarranty Cost Models State-Of-Art A Practical Reviewniketa engineerNo ratings yet

- Strategic Value Management - Michael ThiryDocument8 pagesStrategic Value Management - Michael ThiryJaime González-Capitel - ITM PlatformNo ratings yet

- Linking Strategic Objectives To Operations: Towards A More Effective Supply Chain Decision MakingDocument9 pagesLinking Strategic Objectives To Operations: Towards A More Effective Supply Chain Decision Makingtgupta_17No ratings yet

- Towards Developing Competency-Based Measures For Construction Project Managers: Should Contextual Behaviours Be Distinguished From Task Behaviours?Document15 pagesTowards Developing Competency-Based Measures For Construction Project Managers: Should Contextual Behaviours Be Distinguished From Task Behaviours?Adel AshyapNo ratings yet

- Customer Lifetime Value ModelsDocument50 pagesCustomer Lifetime Value Modelspraveen_bpgcNo ratings yet

- The Behavior of CostsDocument34 pagesThe Behavior of Costsharshjain.24No ratings yet

- Leading Industry Tools We Mean Commercially Available Tools That Have Been ValidatedDocument9 pagesLeading Industry Tools We Mean Commercially Available Tools That Have Been ValidatedSwapnil JaiswalNo ratings yet

- Sustainable Business Model Archetypes For The Banking IndustryDocument20 pagesSustainable Business Model Archetypes For The Banking IndustryLili AnaNo ratings yet

- Evaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiDocument12 pagesEvaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiRoshanNo ratings yet

- Value World Summer 2008Document30 pagesValue World Summer 2008Muhammad Alfanny SetiawanNo ratings yet

- Value Management Research Paper DF FinalDocument16 pagesValue Management Research Paper DF FinalDavid FinnieNo ratings yet

- How To Evaluate CapitalDocument15 pagesHow To Evaluate Capitalkumarashish21No ratings yet

- 35 Projectsuccess BJM Smyrk 2012Document45 pages35 Projectsuccess BJM Smyrk 2012Christy BinuNo ratings yet

- 2012 Dynamic Foresight EvaluationDocument15 pages2012 Dynamic Foresight EvaluationAdhityo Nugraha BarseiNo ratings yet

- NPV and Others - IsraelDocument18 pagesNPV and Others - IsraelSharanjit KaurNo ratings yet

- Archetypes in Cost AccountingDocument14 pagesArchetypes in Cost AccountingJosé Jair Campos ReisNo ratings yet

- 1 s2.0 S2212567115013441 MainDocument10 pages1 s2.0 S2212567115013441 MainChartika UlyNo ratings yet

- Use Risk Breakdown StructureDocument5 pagesUse Risk Breakdown StructureBela UlicsakNo ratings yet

- ACC307AT3 AssignementDocument10 pagesACC307AT3 AssignementKevin HuiNo ratings yet

- BUSN602 Week 6 Evaluation Methods For Capital Budgeting DecisionsDocument8 pagesBUSN602 Week 6 Evaluation Methods For Capital Budgeting Decisionsjwbizz08No ratings yet

- MFM Project CBADocument83 pagesMFM Project CBAVishal GorNo ratings yet

- Value Management - Creating Functional Value For Construction Projects An Exploratory Study - OluwatosinDocument20 pagesValue Management - Creating Functional Value For Construction Projects An Exploratory Study - Oluwatosinolatos4jesusNo ratings yet

- Ijsmr05 105Document15 pagesIjsmr05 105akanyare49No ratings yet

- Re examiningProjectAppraisalandControlIJPM 01Document10 pagesRe examiningProjectAppraisalandControlIJPM 01abdiNo ratings yet

- Investment Management 543..Document36 pagesInvestment Management 543..yajuvendrarathoreNo ratings yet

- Lecture Notes - Value ManagementDocument9 pagesLecture Notes - Value ManagementsympathhiaNo ratings yet

- Cachanosky 2016Document8 pagesCachanosky 2016André M. TrottaNo ratings yet

- Klakegg Et Al (2008) Governance Frameworks For Public Project Development and EstimationDocument16 pagesKlakegg Et Al (2008) Governance Frameworks For Public Project Development and EstimationFelipe E. Zaldivia FuenzalidaNo ratings yet

- Kanghwa 2010Document9 pagesKanghwa 2010adie.fyNo ratings yet

- V2 Camiros-Cost Benefit Analysis PresentationDocument35 pagesV2 Camiros-Cost Benefit Analysis PresentationAngel FerrerNo ratings yet

- Unit 14. Valuation & Construction EconomicsDocument52 pagesUnit 14. Valuation & Construction EconomicsAchu UnnikrishnanNo ratings yet

- Bennett Nalewaik CE PM QS 201204Document15 pagesBennett Nalewaik CE PM QS 201204MichaelKipronoNo ratings yet

- Cost & Management Acct II ModuleDocument170 pagesCost & Management Acct II ModuleMekoya TerefeNo ratings yet

- Financial Performance Measures and Value Creation: the State of the ArtFrom EverandFinancial Performance Measures and Value Creation: the State of the ArtNo ratings yet

- Fixed-Income Portfolio Analytics: A Practical Guide to Implementing, Monitoring and Understanding Fixed-Income PortfoliosFrom EverandFixed-Income Portfolio Analytics: A Practical Guide to Implementing, Monitoring and Understanding Fixed-Income PortfoliosRating: 3.5 out of 5 stars3.5/5 (1)

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Academic TalkDocument2 pagesAcademic TalkMzhfr IzzatNo ratings yet

- IRB 6640 Product Manual 3HAC026876-001 - Rev - en - LibraryDocument413 pagesIRB 6640 Product Manual 3HAC026876-001 - Rev - en - Libraryloscarma50% (2)

- Asif Sohail Banking PresentationDocument57 pagesAsif Sohail Banking PresentationAsif Sohail100% (1)

- Ceylon Investment PLC: A Carson Cumberbatch CompanyDocument11 pagesCeylon Investment PLC: A Carson Cumberbatch CompanygirihellNo ratings yet

- Aligning The Organization For Successful Digital TransformationDocument28 pagesAligning The Organization For Successful Digital TransformationEduardo PintoNo ratings yet

- What Is Test Method QualificationDocument11 pagesWhat Is Test Method Qualificationvg_vvgNo ratings yet

- Geography School Based Assessment: Investigation of The Decline of The Bauxite Mining Industry in Mandeville, ManchesterDocument19 pagesGeography School Based Assessment: Investigation of The Decline of The Bauxite Mining Industry in Mandeville, ManchesterTJPlayzNo ratings yet

- Tata MotorsDocument49 pagesTata MotorsDeepak ModiNo ratings yet

- Ingersoll-Rand 2006 Sustainability ReportDocument40 pagesIngersoll-Rand 2006 Sustainability ReportdevilsharmaNo ratings yet

- Rhina Calimlim Worksheet and Fin StatementsDocument11 pagesRhina Calimlim Worksheet and Fin StatementsDianna Rose MenorNo ratings yet

- SPM Chapter 2Document18 pagesSPM Chapter 2Saravanan KrishNo ratings yet

- Bodie Investments 12e IM CH18Document4 pagesBodie Investments 12e IM CH18lexon_kbNo ratings yet

- Margin of Safety and Operating LeverageDocument1 pageMargin of Safety and Operating LeverageMeng Dan100% (1)

- G Gailtenders Writereaddata Tender RFQ For Procurement of Laptop 20090610 154843Document15 pagesG Gailtenders Writereaddata Tender RFQ For Procurement of Laptop 20090610 154843AbhisheNo ratings yet

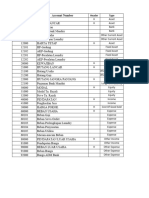

- List AkunDocument1 pageList AkunAyuna KhairunnisaNo ratings yet

- SAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingDocument17 pagesSAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingVEERANo ratings yet

- R-806 S. 2007 Amending Section 3c4 of IRR To Govern Section 18 of RA 7279Document3 pagesR-806 S. 2007 Amending Section 3c4 of IRR To Govern Section 18 of RA 7279hlurb ntrNo ratings yet

- Project Report On Study of Mutual Funds IndustryDocument64 pagesProject Report On Study of Mutual Funds IndustryRUSHENDRA TARTE65% (48)

- 2000 Econ. Paper 2 (Original)Document20 pages2000 Econ. Paper 2 (Original)peter wongNo ratings yet

- Comm Cir 224 MERC-SoP-Regulation-2014 3Document1 pageComm Cir 224 MERC-SoP-Regulation-2014 3RohitNo ratings yet

- 1000 4425 1 PBDocument11 pages1000 4425 1 PBKuro HigeNo ratings yet

- en The Effect of Packaging Satisfaction andDocument9 pagesen The Effect of Packaging Satisfaction andJanet MuisNo ratings yet

- Statistics With R SpecializationDocument15 pagesStatistics With R Specializationduc anhNo ratings yet

- GFSI - Global Markets OverviewDocument1 pageGFSI - Global Markets OverviewSatya Pradeep PulakurthiNo ratings yet

- 4c Advancedspreadsheetskills 171214023623 PDFDocument28 pages4c Advancedspreadsheetskills 171214023623 PDFRainier DoctoleroNo ratings yet

- Ni Hsin - Annual Report 2019Document116 pagesNi Hsin - Annual Report 2019Goh Zai PengNo ratings yet

- Insulator and Conductor Fittings For Overhead Power Lines - : Part 1: Performance and General RequirementsDocument26 pagesInsulator and Conductor Fittings For Overhead Power Lines - : Part 1: Performance and General RequirementsMohamed Ahmed Afifi100% (1)

- Chapter 7 Electronic Business Systems: Author: O'BrienDocument22 pagesChapter 7 Electronic Business Systems: Author: O'BrienOmar Fahim Khan 1911758030No ratings yet

- Call Center System PanaPro - Webinary - FinalDocument39 pagesCall Center System PanaPro - Webinary - FinalAurelian CretuNo ratings yet

Download as pdf or txt

You might also like

- Tire City IncDocument3 pagesTire City IncAlberto RcNo ratings yet

- Insights From The Balanced Scorecard An Introduction To The Enterprise Risk ScorecardDocument11 pagesInsights From The Balanced Scorecard An Introduction To The Enterprise Risk ScorecardEngMohamedReyadHelesyNo ratings yet

- Activity Based Costing ProjectDocument26 pagesActivity Based Costing Projectm_lohani100% (2)

- Value and RiskmanagementDocument11 pagesValue and RiskmanagementShonette ThomasNo ratings yet

- 2010 Lean Knowledge MGMNT The Problem of ValueDocument10 pages2010 Lean Knowledge MGMNT The Problem of Valuenetcat72984No ratings yet

- KPK - Research - Digest - VE - and - VM - Any - Difference - July - 2012 PDFDocument4 pagesKPK - Research - Digest - VE - and - VM - Any - Difference - July - 2012 PDFravibc9367No ratings yet

- González-Prida2019 Chapter AnApproachToQuantifyValueProviDocument8 pagesGonzález-Prida2019 Chapter AnApproachToQuantifyValueProviRosendo LopezNo ratings yet

- Facility Management Value Dimensions FroDocument15 pagesFacility Management Value Dimensions FroMUBANGIZI FELEXNo ratings yet

- Achieving Value For Money (VFM) in Construction ProjectsDocument11 pagesAchieving Value For Money (VFM) in Construction Projectsolatos4jesusNo ratings yet

- KPK Research Digest VE and VM Any Difference July 2012Document4 pagesKPK Research Digest VE and VM Any Difference July 2012danijulianaNo ratings yet

- Portfolio Decision QualityDocument25 pagesPortfolio Decision QualityDiegoNo ratings yet

- Operations in BankingDocument20 pagesOperations in BankingRakshit Chandra Shekhar JoshiNo ratings yet

- 01 - Zwikael - Project - Benefit - Management - 2014Document15 pages01 - Zwikael - Project - Benefit - Management - 2014Carlos BocanegraNo ratings yet

- Managing Project Investments Irreversibility by Accounting RelationsDocument9 pagesManaging Project Investments Irreversibility by Accounting RelationsNoviansyah PamungkasNo ratings yet

- Статья 3 хорошаяDocument18 pagesСтатья 3 хорошаяМаксим НовакNo ratings yet

- This Paper Is Short-Version of My Thesis. Full Thesis Is Available atDocument47 pagesThis Paper Is Short-Version of My Thesis. Full Thesis Is Available atjuz_nurulNo ratings yet

- JPM QES 2016 Harvard PDFDocument16 pagesJPM QES 2016 Harvard PDFSrinivas NemaniNo ratings yet

- Capital Budgeting TheoryDocument9 pagesCapital Budgeting TheoryyayaNo ratings yet

- Benchmarking Uk Government Procurement Performance in Construction ProjectsDocument9 pagesBenchmarking Uk Government Procurement Performance in Construction ProjectsmaazizNo ratings yet

- Knowledge Management For Small Occasional Construction Industry ClientsDocument9 pagesKnowledge Management For Small Occasional Construction Industry ClientsSonmar SonmarNo ratings yet

- Benefits of EvmDocument12 pagesBenefits of EvmMiraj ShahidNo ratings yet

- BRE-Whole Life Value-Sustainable Design in The Built EnvironmentDocument4 pagesBRE-Whole Life Value-Sustainable Design in The Built EnvironmentRoger MaierNo ratings yet

- Value For MoneyDocument6 pagesValue For Moneyselepelehlohonolo93No ratings yet

- Capital Budgeting Paper 2Document9 pagesCapital Budgeting Paper 2Abdul Rafay ButtNo ratings yet

- 7 Equity Valuation Using DCFDocument18 pages7 Equity Valuation Using DCFHuicai MaiNo ratings yet

- Warranty Cost Models State-Of-Art A Practical ReviewDocument10 pagesWarranty Cost Models State-Of-Art A Practical Reviewniketa engineerNo ratings yet

- Strategic Value Management - Michael ThiryDocument8 pagesStrategic Value Management - Michael ThiryJaime González-Capitel - ITM PlatformNo ratings yet

- Linking Strategic Objectives To Operations: Towards A More Effective Supply Chain Decision MakingDocument9 pagesLinking Strategic Objectives To Operations: Towards A More Effective Supply Chain Decision Makingtgupta_17No ratings yet

- Towards Developing Competency-Based Measures For Construction Project Managers: Should Contextual Behaviours Be Distinguished From Task Behaviours?Document15 pagesTowards Developing Competency-Based Measures For Construction Project Managers: Should Contextual Behaviours Be Distinguished From Task Behaviours?Adel AshyapNo ratings yet

- Customer Lifetime Value ModelsDocument50 pagesCustomer Lifetime Value Modelspraveen_bpgcNo ratings yet

- The Behavior of CostsDocument34 pagesThe Behavior of Costsharshjain.24No ratings yet

- Leading Industry Tools We Mean Commercially Available Tools That Have Been ValidatedDocument9 pagesLeading Industry Tools We Mean Commercially Available Tools That Have Been ValidatedSwapnil JaiswalNo ratings yet

- Sustainable Business Model Archetypes For The Banking IndustryDocument20 pagesSustainable Business Model Archetypes For The Banking IndustryLili AnaNo ratings yet

- Evaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiDocument12 pagesEvaluating The Identity of Purchasing Amp Supply - 2021 - Journal of PurchasiRoshanNo ratings yet

- Value World Summer 2008Document30 pagesValue World Summer 2008Muhammad Alfanny SetiawanNo ratings yet

- Value Management Research Paper DF FinalDocument16 pagesValue Management Research Paper DF FinalDavid FinnieNo ratings yet

- How To Evaluate CapitalDocument15 pagesHow To Evaluate Capitalkumarashish21No ratings yet

- 35 Projectsuccess BJM Smyrk 2012Document45 pages35 Projectsuccess BJM Smyrk 2012Christy BinuNo ratings yet

- 2012 Dynamic Foresight EvaluationDocument15 pages2012 Dynamic Foresight EvaluationAdhityo Nugraha BarseiNo ratings yet

- NPV and Others - IsraelDocument18 pagesNPV and Others - IsraelSharanjit KaurNo ratings yet

- Archetypes in Cost AccountingDocument14 pagesArchetypes in Cost AccountingJosé Jair Campos ReisNo ratings yet

- 1 s2.0 S2212567115013441 MainDocument10 pages1 s2.0 S2212567115013441 MainChartika UlyNo ratings yet

- Use Risk Breakdown StructureDocument5 pagesUse Risk Breakdown StructureBela UlicsakNo ratings yet

- ACC307AT3 AssignementDocument10 pagesACC307AT3 AssignementKevin HuiNo ratings yet

- BUSN602 Week 6 Evaluation Methods For Capital Budgeting DecisionsDocument8 pagesBUSN602 Week 6 Evaluation Methods For Capital Budgeting Decisionsjwbizz08No ratings yet

- MFM Project CBADocument83 pagesMFM Project CBAVishal GorNo ratings yet

- Value Management - Creating Functional Value For Construction Projects An Exploratory Study - OluwatosinDocument20 pagesValue Management - Creating Functional Value For Construction Projects An Exploratory Study - Oluwatosinolatos4jesusNo ratings yet

- Ijsmr05 105Document15 pagesIjsmr05 105akanyare49No ratings yet

- Re examiningProjectAppraisalandControlIJPM 01Document10 pagesRe examiningProjectAppraisalandControlIJPM 01abdiNo ratings yet

- Investment Management 543..Document36 pagesInvestment Management 543..yajuvendrarathoreNo ratings yet

- Lecture Notes - Value ManagementDocument9 pagesLecture Notes - Value ManagementsympathhiaNo ratings yet

- Cachanosky 2016Document8 pagesCachanosky 2016André M. TrottaNo ratings yet

- Klakegg Et Al (2008) Governance Frameworks For Public Project Development and EstimationDocument16 pagesKlakegg Et Al (2008) Governance Frameworks For Public Project Development and EstimationFelipe E. Zaldivia FuenzalidaNo ratings yet

- Kanghwa 2010Document9 pagesKanghwa 2010adie.fyNo ratings yet

- V2 Camiros-Cost Benefit Analysis PresentationDocument35 pagesV2 Camiros-Cost Benefit Analysis PresentationAngel FerrerNo ratings yet

- Unit 14. Valuation & Construction EconomicsDocument52 pagesUnit 14. Valuation & Construction EconomicsAchu UnnikrishnanNo ratings yet

- Bennett Nalewaik CE PM QS 201204Document15 pagesBennett Nalewaik CE PM QS 201204MichaelKipronoNo ratings yet

- Cost & Management Acct II ModuleDocument170 pagesCost & Management Acct II ModuleMekoya TerefeNo ratings yet

- Financial Performance Measures and Value Creation: the State of the ArtFrom EverandFinancial Performance Measures and Value Creation: the State of the ArtNo ratings yet

- Fixed-Income Portfolio Analytics: A Practical Guide to Implementing, Monitoring and Understanding Fixed-Income PortfoliosFrom EverandFixed-Income Portfolio Analytics: A Practical Guide to Implementing, Monitoring and Understanding Fixed-Income PortfoliosRating: 3.5 out of 5 stars3.5/5 (1)

- Financial Steering: Valuation, KPI Management and the Interaction with IFRSFrom EverandFinancial Steering: Valuation, KPI Management and the Interaction with IFRSNo ratings yet

- Academic TalkDocument2 pagesAcademic TalkMzhfr IzzatNo ratings yet

- IRB 6640 Product Manual 3HAC026876-001 - Rev - en - LibraryDocument413 pagesIRB 6640 Product Manual 3HAC026876-001 - Rev - en - Libraryloscarma50% (2)

- Asif Sohail Banking PresentationDocument57 pagesAsif Sohail Banking PresentationAsif Sohail100% (1)

- Ceylon Investment PLC: A Carson Cumberbatch CompanyDocument11 pagesCeylon Investment PLC: A Carson Cumberbatch CompanygirihellNo ratings yet

- Aligning The Organization For Successful Digital TransformationDocument28 pagesAligning The Organization For Successful Digital TransformationEduardo PintoNo ratings yet

- What Is Test Method QualificationDocument11 pagesWhat Is Test Method Qualificationvg_vvgNo ratings yet

- Geography School Based Assessment: Investigation of The Decline of The Bauxite Mining Industry in Mandeville, ManchesterDocument19 pagesGeography School Based Assessment: Investigation of The Decline of The Bauxite Mining Industry in Mandeville, ManchesterTJPlayzNo ratings yet

- Tata MotorsDocument49 pagesTata MotorsDeepak ModiNo ratings yet

- Ingersoll-Rand 2006 Sustainability ReportDocument40 pagesIngersoll-Rand 2006 Sustainability ReportdevilsharmaNo ratings yet

- Rhina Calimlim Worksheet and Fin StatementsDocument11 pagesRhina Calimlim Worksheet and Fin StatementsDianna Rose MenorNo ratings yet

- SPM Chapter 2Document18 pagesSPM Chapter 2Saravanan KrishNo ratings yet

- Bodie Investments 12e IM CH18Document4 pagesBodie Investments 12e IM CH18lexon_kbNo ratings yet

- Margin of Safety and Operating LeverageDocument1 pageMargin of Safety and Operating LeverageMeng Dan100% (1)

- G Gailtenders Writereaddata Tender RFQ For Procurement of Laptop 20090610 154843Document15 pagesG Gailtenders Writereaddata Tender RFQ For Procurement of Laptop 20090610 154843AbhisheNo ratings yet

- List AkunDocument1 pageList AkunAyuna KhairunnisaNo ratings yet

- SAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingDocument17 pagesSAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingVEERANo ratings yet

- R-806 S. 2007 Amending Section 3c4 of IRR To Govern Section 18 of RA 7279Document3 pagesR-806 S. 2007 Amending Section 3c4 of IRR To Govern Section 18 of RA 7279hlurb ntrNo ratings yet

- Project Report On Study of Mutual Funds IndustryDocument64 pagesProject Report On Study of Mutual Funds IndustryRUSHENDRA TARTE65% (48)

- 2000 Econ. Paper 2 (Original)Document20 pages2000 Econ. Paper 2 (Original)peter wongNo ratings yet

- Comm Cir 224 MERC-SoP-Regulation-2014 3Document1 pageComm Cir 224 MERC-SoP-Regulation-2014 3RohitNo ratings yet

- 1000 4425 1 PBDocument11 pages1000 4425 1 PBKuro HigeNo ratings yet

- en The Effect of Packaging Satisfaction andDocument9 pagesen The Effect of Packaging Satisfaction andJanet MuisNo ratings yet

- Statistics With R SpecializationDocument15 pagesStatistics With R Specializationduc anhNo ratings yet

- GFSI - Global Markets OverviewDocument1 pageGFSI - Global Markets OverviewSatya Pradeep PulakurthiNo ratings yet

- 4c Advancedspreadsheetskills 171214023623 PDFDocument28 pages4c Advancedspreadsheetskills 171214023623 PDFRainier DoctoleroNo ratings yet

- Ni Hsin - Annual Report 2019Document116 pagesNi Hsin - Annual Report 2019Goh Zai PengNo ratings yet

- Insulator and Conductor Fittings For Overhead Power Lines - : Part 1: Performance and General RequirementsDocument26 pagesInsulator and Conductor Fittings For Overhead Power Lines - : Part 1: Performance and General RequirementsMohamed Ahmed Afifi100% (1)

- Chapter 7 Electronic Business Systems: Author: O'BrienDocument22 pagesChapter 7 Electronic Business Systems: Author: O'BrienOmar Fahim Khan 1911758030No ratings yet

- Call Center System PanaPro - Webinary - FinalDocument39 pagesCall Center System PanaPro - Webinary - FinalAurelian CretuNo ratings yet