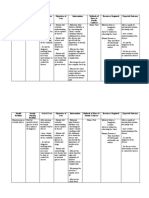

Forms of Business Organization: Fundamentals of Abm 1 SHS 2020-2021 Second Semester

Forms of Business Organization: Fundamentals of Abm 1 SHS 2020-2021 Second Semester

You might also like

- Cochrane J. H. Asset Pricing Solution 2010Document34 pagesCochrane J. H. Asset Pricing Solution 2010ire04100% (3)

- Ordination Syllabus 2020Document4 pagesOrdination Syllabus 2020api-244731229No ratings yet

- Swot Analysis of Organization 2005Document9 pagesSwot Analysis of Organization 2005Jannie WaldorfNo ratings yet

- FPC010 Application For Providnet Benefits ClaimDocument2 pagesFPC010 Application For Providnet Benefits ClaimFe Pastor100% (1)

- Speech About Women in PoliticsDocument1 pageSpeech About Women in PoliticsdevmountNo ratings yet

- Grieving and Mourning For The LostDocument2 pagesGrieving and Mourning For The LostAndrew RongNo ratings yet

- HIS103 Lec 06 Establishment of Awami League 1949 & Formation of United FrontDocument14 pagesHIS103 Lec 06 Establishment of Awami League 1949 & Formation of United FrontTaufiqur AnikNo ratings yet

- Understanding GlobalizationDocument27 pagesUnderstanding GlobalizationGlyzel SaplaNo ratings yet

- Recalling Mass Upsurge DayDocument3 pagesRecalling Mass Upsurge DaySabbir AhmedNo ratings yet

- Chapter2 - GDP and CPI - EngDocument48 pagesChapter2 - GDP and CPI - EngvietzergNo ratings yet

- 03 SWOT Analysis TemplateDocument3 pages03 SWOT Analysis TemplateVignesh NayamozhiNo ratings yet

- Management and Personnel FeasibilityDocument2 pagesManagement and Personnel FeasibilityDIONZON, JOANAH LEIGH, SP.No ratings yet

- Empowerment and Enablement - Measures For SuccessDocument5 pagesEmpowerment and Enablement - Measures For SuccessKK SharmaNo ratings yet

- PMN504 Assessment Item No3 Team Management Plan CRADocument3 pagesPMN504 Assessment Item No3 Team Management Plan CRAJonathan MiersNo ratings yet

- Future Bangladesh: A Comprehensive Analysis GEN226 (Section-9)Document7 pagesFuture Bangladesh: A Comprehensive Analysis GEN226 (Section-9)Farhana Hoque MaheeNo ratings yet

- 2012 Visayas EarthquakeDocument3 pages2012 Visayas EarthquakemariaNo ratings yet

- BE MergedDocument248 pagesBE MergedLkNo ratings yet

- Provident FundsDocument70 pagesProvident FundsSpeed HRNo ratings yet

- Management and Personnel FeasibilityDocument2 pagesManagement and Personnel FeasibilityDIONZON, JOANAH LEIGH, SP.No ratings yet

- Power Procurement (Competitive Bidding Principles)Document28 pagesPower Procurement (Competitive Bidding Principles)Ankur Pathak100% (1)

- Cooperative Business Plan in Alcala PhilDocument24 pagesCooperative Business Plan in Alcala Philmilesdeasis25No ratings yet

- Cooperative Principles, Philosophies, and ValuesDocument52 pagesCooperative Principles, Philosophies, and ValuesJoy GonzalesNo ratings yet

- BureaucraticDocument2 pagesBureaucraticRainabai Alik MaguindraNo ratings yet

- Welcome RemarksDocument2 pagesWelcome Remarksrizalyn axalanNo ratings yet

- Cooperative Reform and Modernization Program CRMPDocument37 pagesCooperative Reform and Modernization Program CRMPteamconsultwork100% (1)

- 05 - The Definition of Graft and Corruption and The Conflict of Ethics and Law PDFDocument20 pages05 - The Definition of Graft and Corruption and The Conflict of Ethics and Law PDFغسهخ یجدNo ratings yet

- Models of Organizational BehaviorDocument54 pagesModels of Organizational BehaviornanettebashangNo ratings yet

- 1 Doing PhilosophyDocument32 pages1 Doing PhilosophyAilener ZednanrehNo ratings yet

- Provident FundDocument9 pagesProvident FundGopalakrishnan KuppuswamyNo ratings yet

- Lateral Entrants MessgeDocument3 pagesLateral Entrants MessgetrickingsNo ratings yet

- Background of Philippine ConstitutionDocument14 pagesBackground of Philippine ConstitutionRandom internet personNo ratings yet

- PowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Document41 pagesPowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Aamir HayatNo ratings yet

- What Is SWOT AnalysisDocument8 pagesWhat Is SWOT AnalysisJo Ann RamboyongNo ratings yet

- Financial PerformanceDocument45 pagesFinancial PerformanceDina WongNo ratings yet

- Bengali Nationalism and Anti-Ayub Movement A Study of The Role of SyudentsDocument14 pagesBengali Nationalism and Anti-Ayub Movement A Study of The Role of SyudentsJobaiyer Alam0% (1)

- Agora Supply ChainDocument14 pagesAgora Supply ChainkmeaNo ratings yet

- Evaluation of Labor LawDocument25 pagesEvaluation of Labor LawmkhanmajlisNo ratings yet

- Concept and Guidelines - The ASEAN Philippines Digital Art Contest 2021Document6 pagesConcept and Guidelines - The ASEAN Philippines Digital Art Contest 2021Honey Avel UrotNo ratings yet

- Week 7, Lecture 10-Mass Movement-1969 of BangladeshDocument4 pagesWeek 7, Lecture 10-Mass Movement-1969 of BangladeshanisNo ratings yet

- Bajaj Auto Financial AnalysisDocument34 pagesBajaj Auto Financial AnalysisTushar BallabhNo ratings yet

- Zero Base BudgetingDocument11 pagesZero Base BudgetingRicha SachanNo ratings yet

- Bidding ProcedureDocument84 pagesBidding ProcedureGretzNo ratings yet

- FsfsfsfsfsDocument3 pagesFsfsfsfsfsJeffrey Constantino PatacsilNo ratings yet

- OWWA Matrix OFWDocument33 pagesOWWA Matrix OFWDesiree GuaschNo ratings yet

- Analysis of Climate ImpactDocument10 pagesAnalysis of Climate ImpactJun Cueva ComerosNo ratings yet

- Liberation WarDocument15 pagesLiberation WarFuhad AhmedNo ratings yet

- Bangko Sentral NG PilipinasDocument59 pagesBangko Sentral NG PilipinasAnn balledosNo ratings yet

- Philippine Bureaucracy and The PersistenDocument16 pagesPhilippine Bureaucracy and The PersistenEthel Jasmine VillanuevaNo ratings yet

- 2016 Memo Circular No.19Document42 pages2016 Memo Circular No.19alicianatalialevisteNo ratings yet

- PhilippinesDocument39 pagesPhilippineswilliamIINo ratings yet

- CH 06Document39 pagesCH 06JOEMAR LEGRESONo ratings yet

- Peoples Budget 2013Document70 pagesPeoples Budget 2013Imperator FuriosaNo ratings yet

- CO-OPERATIVE ManagementDocument18 pagesCO-OPERATIVE ManagementAdil AslamNo ratings yet

- Welcome Remarks Bilang Pagpupugay Sa MagulangDocument1 pageWelcome Remarks Bilang Pagpupugay Sa MagulangRonalyn RodriguezNo ratings yet

- Perfect Competition, Monopoly, Monopolistic and OligopolyDocument42 pagesPerfect Competition, Monopoly, Monopolistic and OligopolyAbhimanyu KotwalNo ratings yet

- Aftab Annual Report 2018 PDFDocument77 pagesAftab Annual Report 2018 PDFTousif GalibNo ratings yet

- Unit-18 Public Utilities PDFDocument9 pagesUnit-18 Public Utilities PDFSatish DasNo ratings yet

- Capital BudgetingDocument4 pagesCapital BudgetingJenny Dela Cruz100% (1)

- Iai Dip Ifrs Ias 33Document29 pagesIai Dip Ifrs Ias 33yukidiwiNo ratings yet

- Modules 1Document4 pagesModules 1JT GalNo ratings yet

- Fundamentals of Accounting ReviewDocument53 pagesFundamentals of Accounting ReviewJericho Pedragosa100% (1)

- Ch1-Fundamental of Financial AccountingDocument40 pagesCh1-Fundamental of Financial AccountingEYENNo ratings yet

- N3 Osha 1994 2019Document123 pagesN3 Osha 1994 2019Suhaila JamaluddinNo ratings yet

- Impacts of Climate Change On Hydropower Generation in China: SciencedirectDocument15 pagesImpacts of Climate Change On Hydropower Generation in China: SciencedirectWaldo LavadoNo ratings yet

- Angel BrokingDocument105 pagesAngel BrokingPankaj SolankiNo ratings yet

- SWOT Analysis For WimpyDocument3 pagesSWOT Analysis For Wimpyandiswambuyazi7No ratings yet

- Final Micro Plan Quality Evaluation, Desk Review and FieldValidation FormsDocument4 pagesFinal Micro Plan Quality Evaluation, Desk Review and FieldValidation Formsmoss4u100% (1)

- Business Studies - ArticlesDocument122 pagesBusiness Studies - Articlesapi-3697361No ratings yet

- State Quality FilinnialDocument3 pagesState Quality FilinnialMichaella Acebuche50% (2)

- Test Bank For Criminal Law and Procedure 7th EditionDocument34 pagesTest Bank For Criminal Law and Procedure 7th Editionnervous.vielle60lnwy100% (52)

- Bacani vs. Nacoco - Case DigestDocument4 pagesBacani vs. Nacoco - Case Digestclaire HipolNo ratings yet

- Liberalism and Idealism and ThoeiresDocument15 pagesLiberalism and Idealism and Thoeiresm.umerfaizan1895No ratings yet

- Week 1 ReadingDocument8 pagesWeek 1 ReadingJenny CorredorNo ratings yet

- FNCPDocument3 pagesFNCPFatima Ysabelle Marie RuizNo ratings yet

- Tan vs. BarriosDocument22 pagesTan vs. BarriosJardine Precious MiroyNo ratings yet

- Keyboard Shortcuts in TallyPrime - 1Document15 pagesKeyboard Shortcuts in TallyPrime - 1perfect printNo ratings yet

- Report 4Document4 pagesReport 4RecordTrac - City of OaklandNo ratings yet

- 15 QuestionsDocument10 pages15 Questionsvirpal-kaur.virpal-kaur100% (1)

- Index Books GroupsDocument356 pagesIndex Books GroupsPedro SampaioNo ratings yet

- Oracle Access Management 11gR2 (11.1.2.x) Frequently Asked Questions (FAQ)Document32 pagesOracle Access Management 11gR2 (11.1.2.x) Frequently Asked Questions (FAQ)madhanNo ratings yet

- Comprehensive School Counseling Program 1Document9 pagesComprehensive School Counseling Program 1api-352239846No ratings yet

- SRC Theology Seminary Formation ProgramDocument4 pagesSRC Theology Seminary Formation ProgramIsrael R OmegaNo ratings yet

- EXCESSIVE FINES Pp. Vs Dacuycuy & Agbanlog vs. Pp.Document3 pagesEXCESSIVE FINES Pp. Vs Dacuycuy & Agbanlog vs. Pp.Cel DelabahanNo ratings yet

- Challenges For Management in A Global EnvironmentDocument2 pagesChallenges For Management in A Global EnvironmentLinh Đặng Thị HuyềnNo ratings yet

- Assigment NutritionDocument10 pagesAssigment NutritionValdemiro NhantumboNo ratings yet

- FA UN PeacekeepingDocument13 pagesFA UN PeacekeepingraesaNo ratings yet

- Lexington County School District One LawsuitDocument17 pagesLexington County School District One LawsuitMayra ParrillaNo ratings yet

- Muñoz PDFDocument225 pagesMuñoz PDFCristián OpazoNo ratings yet

- JMAA Memo Motion For Protective OrderDocument4 pagesJMAA Memo Motion For Protective Orderthe kingfishNo ratings yet

- Rubric For Dramatic ProjectsDocument2 pagesRubric For Dramatic ProjectsReynald CachoNo ratings yet

Download as docx, pdf, or txt

You might also like

- Cochrane J. H. Asset Pricing Solution 2010Document34 pagesCochrane J. H. Asset Pricing Solution 2010ire04100% (3)

- Ordination Syllabus 2020Document4 pagesOrdination Syllabus 2020api-244731229No ratings yet

- Swot Analysis of Organization 2005Document9 pagesSwot Analysis of Organization 2005Jannie WaldorfNo ratings yet

- FPC010 Application For Providnet Benefits ClaimDocument2 pagesFPC010 Application For Providnet Benefits ClaimFe Pastor100% (1)

- Speech About Women in PoliticsDocument1 pageSpeech About Women in PoliticsdevmountNo ratings yet

- Grieving and Mourning For The LostDocument2 pagesGrieving and Mourning For The LostAndrew RongNo ratings yet

- HIS103 Lec 06 Establishment of Awami League 1949 & Formation of United FrontDocument14 pagesHIS103 Lec 06 Establishment of Awami League 1949 & Formation of United FrontTaufiqur AnikNo ratings yet

- Understanding GlobalizationDocument27 pagesUnderstanding GlobalizationGlyzel SaplaNo ratings yet

- Recalling Mass Upsurge DayDocument3 pagesRecalling Mass Upsurge DaySabbir AhmedNo ratings yet

- Chapter2 - GDP and CPI - EngDocument48 pagesChapter2 - GDP and CPI - EngvietzergNo ratings yet

- 03 SWOT Analysis TemplateDocument3 pages03 SWOT Analysis TemplateVignesh NayamozhiNo ratings yet

- Management and Personnel FeasibilityDocument2 pagesManagement and Personnel FeasibilityDIONZON, JOANAH LEIGH, SP.No ratings yet

- Empowerment and Enablement - Measures For SuccessDocument5 pagesEmpowerment and Enablement - Measures For SuccessKK SharmaNo ratings yet

- PMN504 Assessment Item No3 Team Management Plan CRADocument3 pagesPMN504 Assessment Item No3 Team Management Plan CRAJonathan MiersNo ratings yet

- Future Bangladesh: A Comprehensive Analysis GEN226 (Section-9)Document7 pagesFuture Bangladesh: A Comprehensive Analysis GEN226 (Section-9)Farhana Hoque MaheeNo ratings yet

- 2012 Visayas EarthquakeDocument3 pages2012 Visayas EarthquakemariaNo ratings yet

- BE MergedDocument248 pagesBE MergedLkNo ratings yet

- Provident FundsDocument70 pagesProvident FundsSpeed HRNo ratings yet

- Management and Personnel FeasibilityDocument2 pagesManagement and Personnel FeasibilityDIONZON, JOANAH LEIGH, SP.No ratings yet

- Power Procurement (Competitive Bidding Principles)Document28 pagesPower Procurement (Competitive Bidding Principles)Ankur Pathak100% (1)

- Cooperative Business Plan in Alcala PhilDocument24 pagesCooperative Business Plan in Alcala Philmilesdeasis25No ratings yet

- Cooperative Principles, Philosophies, and ValuesDocument52 pagesCooperative Principles, Philosophies, and ValuesJoy GonzalesNo ratings yet

- BureaucraticDocument2 pagesBureaucraticRainabai Alik MaguindraNo ratings yet

- Welcome RemarksDocument2 pagesWelcome Remarksrizalyn axalanNo ratings yet

- Cooperative Reform and Modernization Program CRMPDocument37 pagesCooperative Reform and Modernization Program CRMPteamconsultwork100% (1)

- 05 - The Definition of Graft and Corruption and The Conflict of Ethics and Law PDFDocument20 pages05 - The Definition of Graft and Corruption and The Conflict of Ethics and Law PDFغسهخ یجدNo ratings yet

- Models of Organizational BehaviorDocument54 pagesModels of Organizational BehaviornanettebashangNo ratings yet

- 1 Doing PhilosophyDocument32 pages1 Doing PhilosophyAilener ZednanrehNo ratings yet

- Provident FundDocument9 pagesProvident FundGopalakrishnan KuppuswamyNo ratings yet

- Lateral Entrants MessgeDocument3 pagesLateral Entrants MessgetrickingsNo ratings yet

- Background of Philippine ConstitutionDocument14 pagesBackground of Philippine ConstitutionRandom internet personNo ratings yet

- PowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Document41 pagesPowerPiont Presentation of Project " Analysis of Financial Statements of Glaxosmithkline Pakistan"Aamir HayatNo ratings yet

- What Is SWOT AnalysisDocument8 pagesWhat Is SWOT AnalysisJo Ann RamboyongNo ratings yet

- Financial PerformanceDocument45 pagesFinancial PerformanceDina WongNo ratings yet

- Bengali Nationalism and Anti-Ayub Movement A Study of The Role of SyudentsDocument14 pagesBengali Nationalism and Anti-Ayub Movement A Study of The Role of SyudentsJobaiyer Alam0% (1)

- Agora Supply ChainDocument14 pagesAgora Supply ChainkmeaNo ratings yet

- Evaluation of Labor LawDocument25 pagesEvaluation of Labor LawmkhanmajlisNo ratings yet

- Concept and Guidelines - The ASEAN Philippines Digital Art Contest 2021Document6 pagesConcept and Guidelines - The ASEAN Philippines Digital Art Contest 2021Honey Avel UrotNo ratings yet

- Week 7, Lecture 10-Mass Movement-1969 of BangladeshDocument4 pagesWeek 7, Lecture 10-Mass Movement-1969 of BangladeshanisNo ratings yet

- Bajaj Auto Financial AnalysisDocument34 pagesBajaj Auto Financial AnalysisTushar BallabhNo ratings yet

- Zero Base BudgetingDocument11 pagesZero Base BudgetingRicha SachanNo ratings yet

- Bidding ProcedureDocument84 pagesBidding ProcedureGretzNo ratings yet

- FsfsfsfsfsDocument3 pagesFsfsfsfsfsJeffrey Constantino PatacsilNo ratings yet

- OWWA Matrix OFWDocument33 pagesOWWA Matrix OFWDesiree GuaschNo ratings yet

- Analysis of Climate ImpactDocument10 pagesAnalysis of Climate ImpactJun Cueva ComerosNo ratings yet

- Liberation WarDocument15 pagesLiberation WarFuhad AhmedNo ratings yet

- Bangko Sentral NG PilipinasDocument59 pagesBangko Sentral NG PilipinasAnn balledosNo ratings yet

- Philippine Bureaucracy and The PersistenDocument16 pagesPhilippine Bureaucracy and The PersistenEthel Jasmine VillanuevaNo ratings yet

- 2016 Memo Circular No.19Document42 pages2016 Memo Circular No.19alicianatalialevisteNo ratings yet

- PhilippinesDocument39 pagesPhilippineswilliamIINo ratings yet

- CH 06Document39 pagesCH 06JOEMAR LEGRESONo ratings yet

- Peoples Budget 2013Document70 pagesPeoples Budget 2013Imperator FuriosaNo ratings yet

- CO-OPERATIVE ManagementDocument18 pagesCO-OPERATIVE ManagementAdil AslamNo ratings yet

- Welcome Remarks Bilang Pagpupugay Sa MagulangDocument1 pageWelcome Remarks Bilang Pagpupugay Sa MagulangRonalyn RodriguezNo ratings yet

- Perfect Competition, Monopoly, Monopolistic and OligopolyDocument42 pagesPerfect Competition, Monopoly, Monopolistic and OligopolyAbhimanyu KotwalNo ratings yet

- Aftab Annual Report 2018 PDFDocument77 pagesAftab Annual Report 2018 PDFTousif GalibNo ratings yet

- Unit-18 Public Utilities PDFDocument9 pagesUnit-18 Public Utilities PDFSatish DasNo ratings yet

- Capital BudgetingDocument4 pagesCapital BudgetingJenny Dela Cruz100% (1)

- Iai Dip Ifrs Ias 33Document29 pagesIai Dip Ifrs Ias 33yukidiwiNo ratings yet

- Modules 1Document4 pagesModules 1JT GalNo ratings yet

- Fundamentals of Accounting ReviewDocument53 pagesFundamentals of Accounting ReviewJericho Pedragosa100% (1)

- Ch1-Fundamental of Financial AccountingDocument40 pagesCh1-Fundamental of Financial AccountingEYENNo ratings yet

- N3 Osha 1994 2019Document123 pagesN3 Osha 1994 2019Suhaila JamaluddinNo ratings yet

- Impacts of Climate Change On Hydropower Generation in China: SciencedirectDocument15 pagesImpacts of Climate Change On Hydropower Generation in China: SciencedirectWaldo LavadoNo ratings yet

- Angel BrokingDocument105 pagesAngel BrokingPankaj SolankiNo ratings yet

- SWOT Analysis For WimpyDocument3 pagesSWOT Analysis For Wimpyandiswambuyazi7No ratings yet

- Final Micro Plan Quality Evaluation, Desk Review and FieldValidation FormsDocument4 pagesFinal Micro Plan Quality Evaluation, Desk Review and FieldValidation Formsmoss4u100% (1)

- Business Studies - ArticlesDocument122 pagesBusiness Studies - Articlesapi-3697361No ratings yet

- State Quality FilinnialDocument3 pagesState Quality FilinnialMichaella Acebuche50% (2)

- Test Bank For Criminal Law and Procedure 7th EditionDocument34 pagesTest Bank For Criminal Law and Procedure 7th Editionnervous.vielle60lnwy100% (52)

- Bacani vs. Nacoco - Case DigestDocument4 pagesBacani vs. Nacoco - Case Digestclaire HipolNo ratings yet

- Liberalism and Idealism and ThoeiresDocument15 pagesLiberalism and Idealism and Thoeiresm.umerfaizan1895No ratings yet

- Week 1 ReadingDocument8 pagesWeek 1 ReadingJenny CorredorNo ratings yet

- FNCPDocument3 pagesFNCPFatima Ysabelle Marie RuizNo ratings yet

- Tan vs. BarriosDocument22 pagesTan vs. BarriosJardine Precious MiroyNo ratings yet

- Keyboard Shortcuts in TallyPrime - 1Document15 pagesKeyboard Shortcuts in TallyPrime - 1perfect printNo ratings yet

- Report 4Document4 pagesReport 4RecordTrac - City of OaklandNo ratings yet

- 15 QuestionsDocument10 pages15 Questionsvirpal-kaur.virpal-kaur100% (1)

- Index Books GroupsDocument356 pagesIndex Books GroupsPedro SampaioNo ratings yet

- Oracle Access Management 11gR2 (11.1.2.x) Frequently Asked Questions (FAQ)Document32 pagesOracle Access Management 11gR2 (11.1.2.x) Frequently Asked Questions (FAQ)madhanNo ratings yet

- Comprehensive School Counseling Program 1Document9 pagesComprehensive School Counseling Program 1api-352239846No ratings yet

- SRC Theology Seminary Formation ProgramDocument4 pagesSRC Theology Seminary Formation ProgramIsrael R OmegaNo ratings yet

- EXCESSIVE FINES Pp. Vs Dacuycuy & Agbanlog vs. Pp.Document3 pagesEXCESSIVE FINES Pp. Vs Dacuycuy & Agbanlog vs. Pp.Cel DelabahanNo ratings yet

- Challenges For Management in A Global EnvironmentDocument2 pagesChallenges For Management in A Global EnvironmentLinh Đặng Thị HuyềnNo ratings yet

- Assigment NutritionDocument10 pagesAssigment NutritionValdemiro NhantumboNo ratings yet

- FA UN PeacekeepingDocument13 pagesFA UN PeacekeepingraesaNo ratings yet

- Lexington County School District One LawsuitDocument17 pagesLexington County School District One LawsuitMayra ParrillaNo ratings yet

- Muñoz PDFDocument225 pagesMuñoz PDFCristián OpazoNo ratings yet

- JMAA Memo Motion For Protective OrderDocument4 pagesJMAA Memo Motion For Protective Orderthe kingfishNo ratings yet

- Rubric For Dramatic ProjectsDocument2 pagesRubric For Dramatic ProjectsReynald CachoNo ratings yet