Bba Chapter 3 Revenue and Cost Analysis

Bba Chapter 3 Revenue and Cost Analysis

You might also like

- Paccar LeasingDocument11 pagesPaccar LeasingJennifer67% (3)

- Republic Act No. 10533Document6 pagesRepublic Act No. 10533Jecky Josette AsentistaNo ratings yet

- The Franchisor Feasibility StudyDocument12 pagesThe Franchisor Feasibility StudyLeighgendary CruzNo ratings yet

- Jacksonville Jaguars Media PlanDocument14 pagesJacksonville Jaguars Media PlanOakenshield1100% (1)

- TQM PolaroidDocument36 pagesTQM Polaroiduttam.nift100% (1)

- 04 Activity Based Costing PDFDocument11 pages04 Activity Based Costing PDFPappu LalNo ratings yet

- Marginal Costing and Decision Making PDFDocument79 pagesMarginal Costing and Decision Making PDFKillerbeeNo ratings yet

- Marginal Costing and Cost-Volume-Profit Analysis (CVP)Document65 pagesMarginal Costing and Cost-Volume-Profit Analysis (CVP)Puneesh VikramNo ratings yet

- Joint Products & by Products: Solutions To Assignment ProblemsDocument5 pagesJoint Products & by Products: Solutions To Assignment ProblemsXNo ratings yet

- Assignment Cost Sheet SumsDocument3 pagesAssignment Cost Sheet SumsMamta PrajapatiNo ratings yet

- Decision Making in CostingDocument21 pagesDecision Making in CostingParamjit Sharma67% (3)

- MeaningDocument15 pagesMeaningHimanshuChaurasiaNo ratings yet

- Forex - Problems in Exchange RateDocument26 pagesForex - Problems in Exchange Rateyawehnew23No ratings yet

- Revenue Curves Under Perfect and Imperfect CompetitionDocument32 pagesRevenue Curves Under Perfect and Imperfect CompetitionEsha ChaudharyNo ratings yet

- 333FF2 - Bond Pricing & Bond Pricing Theorems 1Document23 pages333FF2 - Bond Pricing & Bond Pricing Theorems 1Sai PavanNo ratings yet

- Bep NumericalsDocument10 pagesBep NumericalsSachin SahooNo ratings yet

- Ratio AnalysisDocument42 pagesRatio AnalysiskanavNo ratings yet

- Workbook On Derivatives PDFDocument84 pagesWorkbook On Derivatives PDFsapnaofsnehNo ratings yet

- BCOM 3rd and 4th Sem Syallbus NEPDocument37 pagesBCOM 3rd and 4th Sem Syallbus NEPgfgcw yadgirNo ratings yet

- Tugas Individu Akmen Materi ABC PDFDocument3 pagesTugas Individu Akmen Materi ABC PDFtutiNo ratings yet

- Shares and Mutual FundDocument21 pagesShares and Mutual FundHumouRaaj100% (1)

- Contract Process ProblemsDocument24 pagesContract Process ProblemsAakef SiddiquiNo ratings yet

- Internship Report FormatDocument4 pagesInternship Report FormatKokkirala Srinath RaoNo ratings yet

- PPT On Cost SheetDocument16 pagesPPT On Cost SheetShubham VermaNo ratings yet

- Operations Research (OR) : Subject NameDocument13 pagesOperations Research (OR) : Subject NameHarish S M100% (1)

- M/s Alag Pre Post SolutionDocument2 pagesM/s Alag Pre Post SolutionAyush VermaNo ratings yet

- Question Bank Paper: Cost Accounting McqsDocument8 pagesQuestion Bank Paper: Cost Accounting McqsDarmin Kaye PalayNo ratings yet

- Cost Sheet ProblemsDocument2 pagesCost Sheet ProblemsPridhvi Raj ReddyNo ratings yet

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- Baily V de Crespigny: 1869) LR 4 QB 180Document4 pagesBaily V de Crespigny: 1869) LR 4 QB 180TimishaNo ratings yet

- Contract Costing 07Document16 pagesContract Costing 07Kamal BhanushaliNo ratings yet

- Overheads Revision PDFDocument9 pagesOverheads Revision PDFSurajNo ratings yet

- Market Efficiency PDFDocument17 pagesMarket Efficiency PDFBatoul ShokorNo ratings yet

- 9 Partnership Question 21Document11 pages9 Partnership Question 21kautiNo ratings yet

- Unit 1Document80 pagesUnit 1Mohan SharmaNo ratings yet

- Basic EOQ Model: Trial and Error MethodDocument7 pagesBasic EOQ Model: Trial and Error MethodROCKYNo ratings yet

- Ebit - Eps Analysis SolutionsDocument14 pagesEbit - Eps Analysis Solutionsvedhanarayanan2404No ratings yet

- Underwriter AccountDocument9 pagesUnderwriter AccountQuin TimmyNo ratings yet

- 02 Per. Invest 26-30Document5 pages02 Per. Invest 26-30Ritu SahaniNo ratings yet

- Ipcc Cost Accounting RTP Nov2011Document209 pagesIpcc Cost Accounting RTP Nov2011Rakesh VermaNo ratings yet

- Process Costing Questions Sheet AssignmentDocument12 pagesProcess Costing Questions Sheet Assignmentvanshaj juneja0% (1)

- Investment Analysis & Portfolio Management: Equity ValuationDocument5 pagesInvestment Analysis & Portfolio Management: Equity ValuationNitesh Kirar100% (1)

- Paper 8Document40 pagesPaper 8rvee kalraNo ratings yet

- 74767bos60492 cp8Document102 pages74767bos60492 cp8Vignesh VigneshNo ratings yet

- Assignment 04Document8 pagesAssignment 04John MilanNo ratings yet

- Unit 2 Structure of of Options MarketsDocument36 pagesUnit 2 Structure of of Options MarketsTorreus AdhikariNo ratings yet

- GST Assignments For B.com 6TH Sem PDFDocument4 pagesGST Assignments For B.com 6TH Sem PDFAnujyadav Monuyadav100% (1)

- Problems On Flexible BudgetDocument3 pagesProblems On Flexible BudgetsafwanhossainNo ratings yet

- Objectives of The Price PolicyDocument3 pagesObjectives of The Price PolicyPrasanna Hegde100% (1)

- Marginal Costing and Break-Even AnalysisDocument6 pagesMarginal Costing and Break-Even AnalysisPrasanna SharmaNo ratings yet

- Time Value of MoneyDocument62 pagesTime Value of Moneyemmanuel JohnyNo ratings yet

- Marginal Costing: A Management Technique For Profit Planning, Cost Control and Decision MakingDocument17 pagesMarginal Costing: A Management Technique For Profit Planning, Cost Control and Decision Makingdivyesh_variaNo ratings yet

- Cost Accounting 2 Marks QuestionsDocument5 pagesCost Accounting 2 Marks QuestionsEnbathamizhanNo ratings yet

- Standard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDocument7 pagesStandard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDevi ParameshNo ratings yet

- Exim PolicyDocument21 pagesExim PolicyRitu RanjanNo ratings yet

- The Following Financial Data Have Been Furnished by A Ltd. and B LTDDocument10 pagesThe Following Financial Data Have Been Furnished by A Ltd. and B LTDNaveen SatiNo ratings yet

- Purchase Consideration - SolutionDocument16 pagesPurchase Consideration - Solutionsarthak mendirattaNo ratings yet

- Model Question Paper Cost and Management AccountingDocument6 pagesModel Question Paper Cost and Management AccountingSuhas BR100% (1)

- Trends in International ManagementDocument5 pagesTrends in International ManagementAleksandra RudchenkoNo ratings yet

- Capital Structure.Document22 pagesCapital Structure.Puneet ShirahattiNo ratings yet

- Concept of Revenue: Class NotesDocument4 pagesConcept of Revenue: Class NotesANGERR PLAYZNo ratings yet

- REVENUE CURVES (Microeconomics Principles)Document14 pagesREVENUE CURVES (Microeconomics Principles)sp957444No ratings yet

- 4.1 P C: D F: Erfect Ompetition Efining EaturesDocument18 pages4.1 P C: D F: Erfect Ompetition Efining EaturesAakriti JainNo ratings yet

- Revenue Types: Total, Average and Marginal Revenue!Document7 pagesRevenue Types: Total, Average and Marginal Revenue!Nasir KhanNo ratings yet

- Chapter 4Document22 pagesChapter 4abdelamuzemil8No ratings yet

- HR and Payroll ManagementDocument8 pagesHR and Payroll ManagementAmit Anand100% (1)

- Geogonia v. Court of Appeals DigestDocument6 pagesGeogonia v. Court of Appeals DigestJoy RaguindinNo ratings yet

- KAMDAR-Annualreport2009 (1.7MB)Document87 pagesKAMDAR-Annualreport2009 (1.7MB)Kee_Mei_Chwen_2087No ratings yet

- Aca 2024 PlannerDocument1 pageAca 2024 Planneryfarhana2002No ratings yet

- Fundamentals of Corporate Finance Chap 001Document18 pagesFundamentals of Corporate Finance Chap 001tyremiNo ratings yet

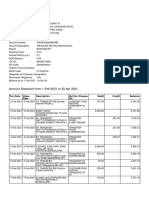

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- Chapter 2 - The Nature of Small BusinessDocument16 pagesChapter 2 - The Nature of Small BusinessChristian AlcaparasNo ratings yet

- Receiving Inspection ProcedureDocument2 pagesReceiving Inspection ProcedureErwin SantosoNo ratings yet

- Benefits of SMEDDocument8 pagesBenefits of SMEDRashmi_Mahavar_674367% (3)

- i-ROOMZ Nakshatra-LRDocument1 pagei-ROOMZ Nakshatra-LRsharadNo ratings yet

- Chapter 5 Accounting For Factory OverheadDocument2 pagesChapter 5 Accounting For Factory OverheadKaren CaelNo ratings yet

- Risk Assumption Letter: Mi Service Centre Co Simran EnterprisesDocument4 pagesRisk Assumption Letter: Mi Service Centre Co Simran EnterprisesHitendra chauhanNo ratings yet

- Day 1 Employee Quickstart Equinix Template v11Document13 pagesDay 1 Employee Quickstart Equinix Template v11Anonymous IFc0l5DLNo ratings yet

- Adr & GDRDocument5 pagesAdr & GDRAsif AliNo ratings yet

- COOPDocument18 pagesCOOPEmanuel LacedaNo ratings yet

- Chapter 3 Irb, Epf, SocsoDocument30 pagesChapter 3 Irb, Epf, SocsoMssLycheeNo ratings yet

- Chapter 5-Dayag-TheorisDocument1 pageChapter 5-Dayag-TheorisMazikeen DeckerNo ratings yet

- DBLDocument3 pagesDBLLeafe MendozaNo ratings yet

- Finance Training ManualDocument94 pagesFinance Training ManualSanju Dani100% (1)

- Velasquez V Solid Bank CorpDocument12 pagesVelasquez V Solid Bank CorpDandolph TanNo ratings yet

- Part 2Document179 pagesPart 2api-253241169No ratings yet

- Arabtec Holding and EmaarDocument5 pagesArabtec Holding and EmaarUmair AijazNo ratings yet

- PT20 27Document7 pagesPT20 27Eric Duku100% (1)

- Tanzim H Choudhury CVDocument2 pagesTanzim H Choudhury CVt_choudhuryNo ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)

Download as pdf or txt

You might also like

- Paccar LeasingDocument11 pagesPaccar LeasingJennifer67% (3)

- Republic Act No. 10533Document6 pagesRepublic Act No. 10533Jecky Josette AsentistaNo ratings yet

- The Franchisor Feasibility StudyDocument12 pagesThe Franchisor Feasibility StudyLeighgendary CruzNo ratings yet

- Jacksonville Jaguars Media PlanDocument14 pagesJacksonville Jaguars Media PlanOakenshield1100% (1)

- TQM PolaroidDocument36 pagesTQM Polaroiduttam.nift100% (1)

- 04 Activity Based Costing PDFDocument11 pages04 Activity Based Costing PDFPappu LalNo ratings yet

- Marginal Costing and Decision Making PDFDocument79 pagesMarginal Costing and Decision Making PDFKillerbeeNo ratings yet

- Marginal Costing and Cost-Volume-Profit Analysis (CVP)Document65 pagesMarginal Costing and Cost-Volume-Profit Analysis (CVP)Puneesh VikramNo ratings yet

- Joint Products & by Products: Solutions To Assignment ProblemsDocument5 pagesJoint Products & by Products: Solutions To Assignment ProblemsXNo ratings yet

- Assignment Cost Sheet SumsDocument3 pagesAssignment Cost Sheet SumsMamta PrajapatiNo ratings yet

- Decision Making in CostingDocument21 pagesDecision Making in CostingParamjit Sharma67% (3)

- MeaningDocument15 pagesMeaningHimanshuChaurasiaNo ratings yet

- Forex - Problems in Exchange RateDocument26 pagesForex - Problems in Exchange Rateyawehnew23No ratings yet

- Revenue Curves Under Perfect and Imperfect CompetitionDocument32 pagesRevenue Curves Under Perfect and Imperfect CompetitionEsha ChaudharyNo ratings yet

- 333FF2 - Bond Pricing & Bond Pricing Theorems 1Document23 pages333FF2 - Bond Pricing & Bond Pricing Theorems 1Sai PavanNo ratings yet

- Bep NumericalsDocument10 pagesBep NumericalsSachin SahooNo ratings yet

- Ratio AnalysisDocument42 pagesRatio AnalysiskanavNo ratings yet

- Workbook On Derivatives PDFDocument84 pagesWorkbook On Derivatives PDFsapnaofsnehNo ratings yet

- BCOM 3rd and 4th Sem Syallbus NEPDocument37 pagesBCOM 3rd and 4th Sem Syallbus NEPgfgcw yadgirNo ratings yet

- Tugas Individu Akmen Materi ABC PDFDocument3 pagesTugas Individu Akmen Materi ABC PDFtutiNo ratings yet

- Shares and Mutual FundDocument21 pagesShares and Mutual FundHumouRaaj100% (1)

- Contract Process ProblemsDocument24 pagesContract Process ProblemsAakef SiddiquiNo ratings yet

- Internship Report FormatDocument4 pagesInternship Report FormatKokkirala Srinath RaoNo ratings yet

- PPT On Cost SheetDocument16 pagesPPT On Cost SheetShubham VermaNo ratings yet

- Operations Research (OR) : Subject NameDocument13 pagesOperations Research (OR) : Subject NameHarish S M100% (1)

- M/s Alag Pre Post SolutionDocument2 pagesM/s Alag Pre Post SolutionAyush VermaNo ratings yet

- Question Bank Paper: Cost Accounting McqsDocument8 pagesQuestion Bank Paper: Cost Accounting McqsDarmin Kaye PalayNo ratings yet

- Cost Sheet ProblemsDocument2 pagesCost Sheet ProblemsPridhvi Raj ReddyNo ratings yet

- Problem Unit 4Document7 pagesProblem Unit 4meenasaratha100% (1)

- Baily V de Crespigny: 1869) LR 4 QB 180Document4 pagesBaily V de Crespigny: 1869) LR 4 QB 180TimishaNo ratings yet

- Contract Costing 07Document16 pagesContract Costing 07Kamal BhanushaliNo ratings yet

- Overheads Revision PDFDocument9 pagesOverheads Revision PDFSurajNo ratings yet

- Market Efficiency PDFDocument17 pagesMarket Efficiency PDFBatoul ShokorNo ratings yet

- 9 Partnership Question 21Document11 pages9 Partnership Question 21kautiNo ratings yet

- Unit 1Document80 pagesUnit 1Mohan SharmaNo ratings yet

- Basic EOQ Model: Trial and Error MethodDocument7 pagesBasic EOQ Model: Trial and Error MethodROCKYNo ratings yet

- Ebit - Eps Analysis SolutionsDocument14 pagesEbit - Eps Analysis Solutionsvedhanarayanan2404No ratings yet

- Underwriter AccountDocument9 pagesUnderwriter AccountQuin TimmyNo ratings yet

- 02 Per. Invest 26-30Document5 pages02 Per. Invest 26-30Ritu SahaniNo ratings yet

- Ipcc Cost Accounting RTP Nov2011Document209 pagesIpcc Cost Accounting RTP Nov2011Rakesh VermaNo ratings yet

- Process Costing Questions Sheet AssignmentDocument12 pagesProcess Costing Questions Sheet Assignmentvanshaj juneja0% (1)

- Investment Analysis & Portfolio Management: Equity ValuationDocument5 pagesInvestment Analysis & Portfolio Management: Equity ValuationNitesh Kirar100% (1)

- Paper 8Document40 pagesPaper 8rvee kalraNo ratings yet

- 74767bos60492 cp8Document102 pages74767bos60492 cp8Vignesh VigneshNo ratings yet

- Assignment 04Document8 pagesAssignment 04John MilanNo ratings yet

- Unit 2 Structure of of Options MarketsDocument36 pagesUnit 2 Structure of of Options MarketsTorreus AdhikariNo ratings yet

- GST Assignments For B.com 6TH Sem PDFDocument4 pagesGST Assignments For B.com 6TH Sem PDFAnujyadav Monuyadav100% (1)

- Problems On Flexible BudgetDocument3 pagesProblems On Flexible BudgetsafwanhossainNo ratings yet

- Objectives of The Price PolicyDocument3 pagesObjectives of The Price PolicyPrasanna Hegde100% (1)

- Marginal Costing and Break-Even AnalysisDocument6 pagesMarginal Costing and Break-Even AnalysisPrasanna SharmaNo ratings yet

- Time Value of MoneyDocument62 pagesTime Value of Moneyemmanuel JohnyNo ratings yet

- Marginal Costing: A Management Technique For Profit Planning, Cost Control and Decision MakingDocument17 pagesMarginal Costing: A Management Technique For Profit Planning, Cost Control and Decision Makingdivyesh_variaNo ratings yet

- Cost Accounting 2 Marks QuestionsDocument5 pagesCost Accounting 2 Marks QuestionsEnbathamizhanNo ratings yet

- Standard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDocument7 pagesStandard Costing - Solutions To Home Work Problems: Question No: 19 Reconciliation With Finished Goods InventoryDevi ParameshNo ratings yet

- Exim PolicyDocument21 pagesExim PolicyRitu RanjanNo ratings yet

- The Following Financial Data Have Been Furnished by A Ltd. and B LTDDocument10 pagesThe Following Financial Data Have Been Furnished by A Ltd. and B LTDNaveen SatiNo ratings yet

- Purchase Consideration - SolutionDocument16 pagesPurchase Consideration - Solutionsarthak mendirattaNo ratings yet

- Model Question Paper Cost and Management AccountingDocument6 pagesModel Question Paper Cost and Management AccountingSuhas BR100% (1)

- Trends in International ManagementDocument5 pagesTrends in International ManagementAleksandra RudchenkoNo ratings yet

- Capital Structure.Document22 pagesCapital Structure.Puneet ShirahattiNo ratings yet

- Concept of Revenue: Class NotesDocument4 pagesConcept of Revenue: Class NotesANGERR PLAYZNo ratings yet

- REVENUE CURVES (Microeconomics Principles)Document14 pagesREVENUE CURVES (Microeconomics Principles)sp957444No ratings yet

- 4.1 P C: D F: Erfect Ompetition Efining EaturesDocument18 pages4.1 P C: D F: Erfect Ompetition Efining EaturesAakriti JainNo ratings yet

- Revenue Types: Total, Average and Marginal Revenue!Document7 pagesRevenue Types: Total, Average and Marginal Revenue!Nasir KhanNo ratings yet

- Chapter 4Document22 pagesChapter 4abdelamuzemil8No ratings yet

- HR and Payroll ManagementDocument8 pagesHR and Payroll ManagementAmit Anand100% (1)

- Geogonia v. Court of Appeals DigestDocument6 pagesGeogonia v. Court of Appeals DigestJoy RaguindinNo ratings yet

- KAMDAR-Annualreport2009 (1.7MB)Document87 pagesKAMDAR-Annualreport2009 (1.7MB)Kee_Mei_Chwen_2087No ratings yet

- Aca 2024 PlannerDocument1 pageAca 2024 Planneryfarhana2002No ratings yet

- Fundamentals of Corporate Finance Chap 001Document18 pagesFundamentals of Corporate Finance Chap 001tyremiNo ratings yet

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- Chapter 2 - The Nature of Small BusinessDocument16 pagesChapter 2 - The Nature of Small BusinessChristian AlcaparasNo ratings yet

- Receiving Inspection ProcedureDocument2 pagesReceiving Inspection ProcedureErwin SantosoNo ratings yet

- Benefits of SMEDDocument8 pagesBenefits of SMEDRashmi_Mahavar_674367% (3)

- i-ROOMZ Nakshatra-LRDocument1 pagei-ROOMZ Nakshatra-LRsharadNo ratings yet

- Chapter 5 Accounting For Factory OverheadDocument2 pagesChapter 5 Accounting For Factory OverheadKaren CaelNo ratings yet

- Risk Assumption Letter: Mi Service Centre Co Simran EnterprisesDocument4 pagesRisk Assumption Letter: Mi Service Centre Co Simran EnterprisesHitendra chauhanNo ratings yet

- Day 1 Employee Quickstart Equinix Template v11Document13 pagesDay 1 Employee Quickstart Equinix Template v11Anonymous IFc0l5DLNo ratings yet

- Adr & GDRDocument5 pagesAdr & GDRAsif AliNo ratings yet

- COOPDocument18 pagesCOOPEmanuel LacedaNo ratings yet

- Chapter 3 Irb, Epf, SocsoDocument30 pagesChapter 3 Irb, Epf, SocsoMssLycheeNo ratings yet

- Chapter 5-Dayag-TheorisDocument1 pageChapter 5-Dayag-TheorisMazikeen DeckerNo ratings yet

- DBLDocument3 pagesDBLLeafe MendozaNo ratings yet

- Finance Training ManualDocument94 pagesFinance Training ManualSanju Dani100% (1)

- Velasquez V Solid Bank CorpDocument12 pagesVelasquez V Solid Bank CorpDandolph TanNo ratings yet

- Part 2Document179 pagesPart 2api-253241169No ratings yet

- Arabtec Holding and EmaarDocument5 pagesArabtec Holding and EmaarUmair AijazNo ratings yet

- PT20 27Document7 pagesPT20 27Eric Duku100% (1)

- Tanzim H Choudhury CVDocument2 pagesTanzim H Choudhury CVt_choudhuryNo ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)