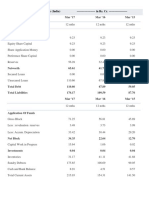

Ratio Analysis of Mahindra N Mahindra LTD

Ratio Analysis of Mahindra N Mahindra LTD

You might also like

- Home Replication StrategyDocument5 pagesHome Replication StrategyChau Hoang100% (19)

- Applied Mathematics ProjectDocument16 pagesApplied Mathematics ProjectRishi VithlaniNo ratings yet

- A Study On Financial Analysis AmazonDocument49 pagesA Study On Financial Analysis Amazonaurorashiva1100% (1)

- The Role of BHEL in Indian EconomyDocument17 pagesThe Role of BHEL in Indian EconomyNiranjana Nair55% (11)

- A Project On Ratio Analysis of Financial Statements & Working Capital Management at HVTL, Tata Motors, JamshedpurDocument88 pagesA Project On Ratio Analysis of Financial Statements & Working Capital Management at HVTL, Tata Motors, Jamshedpurgopalagarwal238780% (30)

- Project Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis ApproachDocument49 pagesProject Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis Approachsudhanshu jeevtani100% (5)

- Financial Analysis of Mahindra and Mahindra CompanyDocument69 pagesFinancial Analysis of Mahindra and Mahindra CompanyAnjaliNo ratings yet

- Ratio Analysis of Reliance IndustriesDocument27 pagesRatio Analysis of Reliance IndustriesSanjana Kurhade100% (5)

- Project "RATIO ANALYSIS of Tata Power Company Limited"Document47 pagesProject "RATIO ANALYSIS of Tata Power Company Limited"Sagar Zine100% (1)

- LG Ratio Analysis FinanceDocument70 pagesLG Ratio Analysis FinanceAkshay Panwar0% (1)

- Ratio ANALYSIS OF CEAT TYRESDocument37 pagesRatio ANALYSIS OF CEAT TYRESS92_neha100% (1)

- Financial Ratio Analysis of Bharti AirtelDocument19 pagesFinancial Ratio Analysis of Bharti AirtelDivya Patel50% (2)

- Social Relevance Black BookDocument47 pagesSocial Relevance Black BookpavanNo ratings yet

- Summer Training Report File On Topic of Ratio AnalysisDocument94 pagesSummer Training Report File On Topic of Ratio Analysisanshul5410100% (3)

- Ratio Analysis - Ashokleyland SUDHEERDocument83 pagesRatio Analysis - Ashokleyland SUDHEERArun Kumar100% (3)

- A Study On Ratio Analysis in Tata MotorsDocument63 pagesA Study On Ratio Analysis in Tata MotorsMeena Sivasubramanian100% (3)

- Financial Statement Analysis in CCL - Bhawna SinghDocument78 pagesFinancial Statement Analysis in CCL - Bhawna SinghTahir Hussain100% (2)

- Copy Test - SwiggyDocument3 pagesCopy Test - SwiggyShubhra SharmaNo ratings yet

- A Study On The Financial Analysis of Reliance Industries LimitedDocument13 pagesA Study On The Financial Analysis of Reliance Industries LimitedIJAR JOURNAL100% (1)

- Financial Analysis of Wipro LTD PDFDocument101 pagesFinancial Analysis of Wipro LTD PDFAnonymous f7wV1lQKRNo ratings yet

- Ratio Analysis of Bharat Heavy Electricals Limited: Final DraftDocument34 pagesRatio Analysis of Bharat Heavy Electricals Limited: Final DraftVidushi Verma50% (2)

- Comparative and Common Size Financial StatementsDocument24 pagesComparative and Common Size Financial StatementsTanish Bohra100% (2)

- Financial Statement and Ratio Analysis of Tata MotorsDocument120 pagesFinancial Statement and Ratio Analysis of Tata MotorsAMIT K SINGH100% (1)

- Financial Statement Analysis of RIL - MBA ProjectDocument52 pagesFinancial Statement Analysis of RIL - MBA Projectsangeetha j100% (1)

- Accountancy Project Work - XIIDocument41 pagesAccountancy Project Work - XIIkawsarNo ratings yet

- Bharti Airtel FINAL Project ReportDocument27 pagesBharti Airtel FINAL Project ReportHashim Shamsudeen100% (2)

- Economics ProjectDocument14 pagesEconomics ProjectAryan SinghNo ratings yet

- Business Studies Project: Made By: Rahil JainDocument29 pagesBusiness Studies Project: Made By: Rahil JainChirag Kothari0% (1)

- Marketing Project DSLR Camera Brands in IndiaDocument25 pagesMarketing Project DSLR Camera Brands in IndiaAnkit Mehta90% (20)

- BPO Contribution To Business Community and NationDocument10 pagesBPO Contribution To Business Community and NationHemanth Sreeram100% (2)

- Tata MotorsDocument46 pagesTata MotorsAmeya PatilNo ratings yet

- Hons Project 09-02-16Document39 pagesHons Project 09-02-16ayush mohta50% (2)

- Project Mahindra Finance PVT LTDDocument63 pagesProject Mahindra Finance PVT LTDSpandana Shetty75% (4)

- Project Synopsis Of"financial Performance AnalysisDocument5 pagesProject Synopsis Of"financial Performance AnalysisRashmi Ranjan Panigrahi100% (3)

- Final ProjectDocument59 pagesFinal ProjectshelarnamdevNo ratings yet

- Economics Project: TOPIC-Report On The Competition in The Aviation Sector in India With Reference To VistaraDocument14 pagesEconomics Project: TOPIC-Report On The Competition in The Aviation Sector in India With Reference To VistaraMeher SahotaNo ratings yet

- A Project Report On: "Money & Banking"Document57 pagesA Project Report On: "Money & Banking"Tasmay EnterprisesNo ratings yet

- Common Size Income Statement - TATA MOTORS LTDDocument6 pagesCommon Size Income Statement - TATA MOTORS LTDSubrat BiswalNo ratings yet

- IFCI ContributionDocument3 pagesIFCI Contributionshruti.shindeNo ratings yet

- Sip Project On Comparative Analysis of Financial Satatement of Sail With Other Steel Companies in IndiaDocument90 pagesSip Project On Comparative Analysis of Financial Satatement of Sail With Other Steel Companies in IndiaKumar Mayank100% (4)

- Ratio Analysis of TCS (KIIT School of Management)Document28 pagesRatio Analysis of TCS (KIIT School of Management)ShivamKumar83% (18)

- Project Guidelines (Issued by CBSE) : CA. (DR.) G.S. GrewalDocument51 pagesProject Guidelines (Issued by CBSE) : CA. (DR.) G.S. GrewalShruti Yadav0% (1)

- Tech Mahindra Company: A Project Report OnDocument55 pagesTech Mahindra Company: A Project Report OnBhuvaneswari karuturiNo ratings yet

- Analysis Atma-Nirbhar Bharat AbhiyanDocument5 pagesAnalysis Atma-Nirbhar Bharat AbhiyanSoumiki Ghosh67% (3)

- The Bishop's Co-Ed School KalyaninagarDocument24 pagesThe Bishop's Co-Ed School KalyaninagarAryan Singh100% (3)

- Accounts Project - Financial Statement Analysis of Steel Authority of India Limited - by Irfan Ahmad & Manisha YadavDocument18 pagesAccounts Project - Financial Statement Analysis of Steel Authority of India Limited - by Irfan Ahmad & Manisha YadavRavi Jaiswal0% (1)

- Senior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3Document26 pagesSenior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3bhaiyarakeshNo ratings yet

- WIPRO 2021-22 Annual Report AnalysisDocument60 pagesWIPRO 2021-22 Annual Report AnalysisShanmuganayagam RNo ratings yet

- Tata Steel Ir 2022 23Document18 pagesTata Steel Ir 2022 23harshita girdharNo ratings yet

- Cash Management at MarutiDocument68 pagesCash Management at MarutiEshaNo ratings yet

- Ratio Analysis of Asian PaintsDocument34 pagesRatio Analysis of Asian PaintsAmit Pandey25% (4)

- ARUN Aavin-ProjectDocument95 pagesARUN Aavin-ProjectGokul krishnan100% (2)

- Ratio Analysis ProjectDocument40 pagesRatio Analysis ProjectPallavi Satardekar100% (1)

- Certificate Accountancy ProjectDocument3 pagesCertificate Accountancy ProjectAnand Krishna Kumar50% (2)

- Financial Analysis of RelianceDocument51 pagesFinancial Analysis of Reliancekkccommerceproject100% (3)

- Tips RatiosDocument8 pagesTips RatiosMelvin Amoh100% (1)

- Class 12 Solution AccountDocument45 pagesClass 12 Solution AccountChandan ChaudharyNo ratings yet

- Financial Statements Analysis - ReportDocument18 pagesFinancial Statements Analysis - ReportKrissa SustalNo ratings yet

- Ratio analysis_PDFDocument17 pagesRatio analysis_PDFMadhav AggarwalNo ratings yet

- Week 2-4 - AdvanceDocument4 pagesWeek 2-4 - AdvanceAnne Maerick Jersey OteroNo ratings yet

- MGT - Accounting - Imp (1 Unit 3 and 1Document12 pagesMGT - Accounting - Imp (1 Unit 3 and 1Vansh TharejaNo ratings yet

- Financial Ratio AnalysisDocument6 pagesFinancial Ratio Analysis5555-899341No ratings yet

- PFE LicenseDocument2 pagesPFE LicensebakamanezeckielNo ratings yet

- Customer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDocument30 pagesCustomer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDavid Lumaban GatdulaNo ratings yet

- Planning An Audit of Financial Statements8888888Document11 pagesPlanning An Audit of Financial Statements8888888sajedulNo ratings yet

- Tmint Creative - Penelusuran GoogleDocument1 pageTmint Creative - Penelusuran GoogleNur ImanahNo ratings yet

- Multiple Choice: - ComputationalDocument4 pagesMultiple Choice: - ComputationalCarlo ParasNo ratings yet

- Bill of Materials - BOMDocument12 pagesBill of Materials - BOMIbnouachir AbderrazakNo ratings yet

- Karina Market Structure SummaryDocument4 pagesKarina Market Structure SummaryKarina Permata SariNo ratings yet

- Competing With It: Fundamentals of Strategic AdvantageDocument16 pagesCompeting With It: Fundamentals of Strategic Advantagejin_adrianNo ratings yet

- Brief Note On HRIS - Downsizing - VRS - RetrenchmentDocument2 pagesBrief Note On HRIS - Downsizing - VRS - RetrenchmentDanìél Koùichi HajongNo ratings yet

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet

- Strategic Management (BEG499 SM) (Elective)Document2 pagesStrategic Management (BEG499 SM) (Elective)Anil MarsaniNo ratings yet

- Marketing Plan: 1: Define Your BusinessDocument12 pagesMarketing Plan: 1: Define Your Businessdrken3No ratings yet

- 3 DERIVATIVES AND HEDGING ACTIVITIES FinalDocument2 pages3 DERIVATIVES AND HEDGING ACTIVITIES FinalCha ChieNo ratings yet

- Rethinking Foundation of EthicsDocument15 pagesRethinking Foundation of EthicstalentaNo ratings yet

- SCM SlidesDocument15 pagesSCM SlidesAmna NoorNo ratings yet

- Hospice Nurse Job DescriptionDocument5 pagesHospice Nurse Job DescriptionKasia KuzakaNo ratings yet

- Strategy - Creation of A CompanyDocument13 pagesStrategy - Creation of A CompanyJoana ToméNo ratings yet

- Title of The Presentation: BA (Hons) Global Business and Entrepreneurship (Foundation Year) Global Business SchoolDocument9 pagesTitle of The Presentation: BA (Hons) Global Business and Entrepreneurship (Foundation Year) Global Business SchoolVinnie plaaNo ratings yet

- TOT AgreementDocument138 pagesTOT Agreementchinnadurai33No ratings yet

- Job Vacancy Announcement Action Contre La Faim-Myanmar: Head of Project (Nutrition)Document3 pagesJob Vacancy Announcement Action Contre La Faim-Myanmar: Head of Project (Nutrition)draftdelete101 errorNo ratings yet

- Backdoor ListingDocument10 pagesBackdoor ListingAryan HateNo ratings yet

- How To Design A Clothing Store: Interior Design and FunctionalityDocument5 pagesHow To Design A Clothing Store: Interior Design and FunctionalityNamit BaserNo ratings yet

- Sample 4Document97 pagesSample 4Salma FarozeNo ratings yet

- CA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024Document13 pagesCA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024rohit 6375No ratings yet

- Export Finance ProjectDocument67 pagesExport Finance ProjectVinay Singh67% (3)

- Cash FlowsDocument26 pagesCash Flowsvickyprimus100% (1)

- Top 3 Brands: Head and Shoulders Pantene Dove Sachet Sachet SachetDocument11 pagesTop 3 Brands: Head and Shoulders Pantene Dove Sachet Sachet SachetVAIJAYANTI JENANo ratings yet

- Keynote Speech of Secretary Roy A. Cimatu Department of Environment and Natural ResourcesDocument6 pagesKeynote Speech of Secretary Roy A. Cimatu Department of Environment and Natural Resourcesmonkeybike88No ratings yet

Download as docx, pdf, or txt

You might also like

- Home Replication StrategyDocument5 pagesHome Replication StrategyChau Hoang100% (19)

- Applied Mathematics ProjectDocument16 pagesApplied Mathematics ProjectRishi VithlaniNo ratings yet

- A Study On Financial Analysis AmazonDocument49 pagesA Study On Financial Analysis Amazonaurorashiva1100% (1)

- The Role of BHEL in Indian EconomyDocument17 pagesThe Role of BHEL in Indian EconomyNiranjana Nair55% (11)

- A Project On Ratio Analysis of Financial Statements & Working Capital Management at HVTL, Tata Motors, JamshedpurDocument88 pagesA Project On Ratio Analysis of Financial Statements & Working Capital Management at HVTL, Tata Motors, Jamshedpurgopalagarwal238780% (30)

- Project Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis ApproachDocument49 pagesProject Report ON Comparative Analysis of Financial Performance of Zomato: A Ratio Analysis Approachsudhanshu jeevtani100% (5)

- Financial Analysis of Mahindra and Mahindra CompanyDocument69 pagesFinancial Analysis of Mahindra and Mahindra CompanyAnjaliNo ratings yet

- Ratio Analysis of Reliance IndustriesDocument27 pagesRatio Analysis of Reliance IndustriesSanjana Kurhade100% (5)

- Project "RATIO ANALYSIS of Tata Power Company Limited"Document47 pagesProject "RATIO ANALYSIS of Tata Power Company Limited"Sagar Zine100% (1)

- LG Ratio Analysis FinanceDocument70 pagesLG Ratio Analysis FinanceAkshay Panwar0% (1)

- Ratio ANALYSIS OF CEAT TYRESDocument37 pagesRatio ANALYSIS OF CEAT TYRESS92_neha100% (1)

- Financial Ratio Analysis of Bharti AirtelDocument19 pagesFinancial Ratio Analysis of Bharti AirtelDivya Patel50% (2)

- Social Relevance Black BookDocument47 pagesSocial Relevance Black BookpavanNo ratings yet

- Summer Training Report File On Topic of Ratio AnalysisDocument94 pagesSummer Training Report File On Topic of Ratio Analysisanshul5410100% (3)

- Ratio Analysis - Ashokleyland SUDHEERDocument83 pagesRatio Analysis - Ashokleyland SUDHEERArun Kumar100% (3)

- A Study On Ratio Analysis in Tata MotorsDocument63 pagesA Study On Ratio Analysis in Tata MotorsMeena Sivasubramanian100% (3)

- Financial Statement Analysis in CCL - Bhawna SinghDocument78 pagesFinancial Statement Analysis in CCL - Bhawna SinghTahir Hussain100% (2)

- Copy Test - SwiggyDocument3 pagesCopy Test - SwiggyShubhra SharmaNo ratings yet

- A Study On The Financial Analysis of Reliance Industries LimitedDocument13 pagesA Study On The Financial Analysis of Reliance Industries LimitedIJAR JOURNAL100% (1)

- Financial Analysis of Wipro LTD PDFDocument101 pagesFinancial Analysis of Wipro LTD PDFAnonymous f7wV1lQKRNo ratings yet

- Ratio Analysis of Bharat Heavy Electricals Limited: Final DraftDocument34 pagesRatio Analysis of Bharat Heavy Electricals Limited: Final DraftVidushi Verma50% (2)

- Comparative and Common Size Financial StatementsDocument24 pagesComparative and Common Size Financial StatementsTanish Bohra100% (2)

- Financial Statement and Ratio Analysis of Tata MotorsDocument120 pagesFinancial Statement and Ratio Analysis of Tata MotorsAMIT K SINGH100% (1)

- Financial Statement Analysis of RIL - MBA ProjectDocument52 pagesFinancial Statement Analysis of RIL - MBA Projectsangeetha j100% (1)

- Accountancy Project Work - XIIDocument41 pagesAccountancy Project Work - XIIkawsarNo ratings yet

- Bharti Airtel FINAL Project ReportDocument27 pagesBharti Airtel FINAL Project ReportHashim Shamsudeen100% (2)

- Economics ProjectDocument14 pagesEconomics ProjectAryan SinghNo ratings yet

- Business Studies Project: Made By: Rahil JainDocument29 pagesBusiness Studies Project: Made By: Rahil JainChirag Kothari0% (1)

- Marketing Project DSLR Camera Brands in IndiaDocument25 pagesMarketing Project DSLR Camera Brands in IndiaAnkit Mehta90% (20)

- BPO Contribution To Business Community and NationDocument10 pagesBPO Contribution To Business Community and NationHemanth Sreeram100% (2)

- Tata MotorsDocument46 pagesTata MotorsAmeya PatilNo ratings yet

- Hons Project 09-02-16Document39 pagesHons Project 09-02-16ayush mohta50% (2)

- Project Mahindra Finance PVT LTDDocument63 pagesProject Mahindra Finance PVT LTDSpandana Shetty75% (4)

- Project Synopsis Of"financial Performance AnalysisDocument5 pagesProject Synopsis Of"financial Performance AnalysisRashmi Ranjan Panigrahi100% (3)

- Final ProjectDocument59 pagesFinal ProjectshelarnamdevNo ratings yet

- Economics Project: TOPIC-Report On The Competition in The Aviation Sector in India With Reference To VistaraDocument14 pagesEconomics Project: TOPIC-Report On The Competition in The Aviation Sector in India With Reference To VistaraMeher SahotaNo ratings yet

- A Project Report On: "Money & Banking"Document57 pagesA Project Report On: "Money & Banking"Tasmay EnterprisesNo ratings yet

- Common Size Income Statement - TATA MOTORS LTDDocument6 pagesCommon Size Income Statement - TATA MOTORS LTDSubrat BiswalNo ratings yet

- IFCI ContributionDocument3 pagesIFCI Contributionshruti.shindeNo ratings yet

- Sip Project On Comparative Analysis of Financial Satatement of Sail With Other Steel Companies in IndiaDocument90 pagesSip Project On Comparative Analysis of Financial Satatement of Sail With Other Steel Companies in IndiaKumar Mayank100% (4)

- Ratio Analysis of TCS (KIIT School of Management)Document28 pagesRatio Analysis of TCS (KIIT School of Management)ShivamKumar83% (18)

- Project Guidelines (Issued by CBSE) : CA. (DR.) G.S. GrewalDocument51 pagesProject Guidelines (Issued by CBSE) : CA. (DR.) G.S. GrewalShruti Yadav0% (1)

- Tech Mahindra Company: A Project Report OnDocument55 pagesTech Mahindra Company: A Project Report OnBhuvaneswari karuturiNo ratings yet

- Analysis Atma-Nirbhar Bharat AbhiyanDocument5 pagesAnalysis Atma-Nirbhar Bharat AbhiyanSoumiki Ghosh67% (3)

- The Bishop's Co-Ed School KalyaninagarDocument24 pagesThe Bishop's Co-Ed School KalyaninagarAryan Singh100% (3)

- Accounts Project - Financial Statement Analysis of Steel Authority of India Limited - by Irfan Ahmad & Manisha YadavDocument18 pagesAccounts Project - Financial Statement Analysis of Steel Authority of India Limited - by Irfan Ahmad & Manisha YadavRavi Jaiswal0% (1)

- Senior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3Document26 pagesSenior School Certificate Examination March - 2023 Marking Scheme - Business Studies 66/1/1, 66/1/2, 66/1/3bhaiyarakeshNo ratings yet

- WIPRO 2021-22 Annual Report AnalysisDocument60 pagesWIPRO 2021-22 Annual Report AnalysisShanmuganayagam RNo ratings yet

- Tata Steel Ir 2022 23Document18 pagesTata Steel Ir 2022 23harshita girdharNo ratings yet

- Cash Management at MarutiDocument68 pagesCash Management at MarutiEshaNo ratings yet

- Ratio Analysis of Asian PaintsDocument34 pagesRatio Analysis of Asian PaintsAmit Pandey25% (4)

- ARUN Aavin-ProjectDocument95 pagesARUN Aavin-ProjectGokul krishnan100% (2)

- Ratio Analysis ProjectDocument40 pagesRatio Analysis ProjectPallavi Satardekar100% (1)

- Certificate Accountancy ProjectDocument3 pagesCertificate Accountancy ProjectAnand Krishna Kumar50% (2)

- Financial Analysis of RelianceDocument51 pagesFinancial Analysis of Reliancekkccommerceproject100% (3)

- Tips RatiosDocument8 pagesTips RatiosMelvin Amoh100% (1)

- Class 12 Solution AccountDocument45 pagesClass 12 Solution AccountChandan ChaudharyNo ratings yet

- Financial Statements Analysis - ReportDocument18 pagesFinancial Statements Analysis - ReportKrissa SustalNo ratings yet

- Ratio analysis_PDFDocument17 pagesRatio analysis_PDFMadhav AggarwalNo ratings yet

- Week 2-4 - AdvanceDocument4 pagesWeek 2-4 - AdvanceAnne Maerick Jersey OteroNo ratings yet

- MGT - Accounting - Imp (1 Unit 3 and 1Document12 pagesMGT - Accounting - Imp (1 Unit 3 and 1Vansh TharejaNo ratings yet

- Financial Ratio AnalysisDocument6 pagesFinancial Ratio Analysis5555-899341No ratings yet

- PFE LicenseDocument2 pagesPFE LicensebakamanezeckielNo ratings yet

- Customer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDocument30 pagesCustomer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDavid Lumaban GatdulaNo ratings yet

- Planning An Audit of Financial Statements8888888Document11 pagesPlanning An Audit of Financial Statements8888888sajedulNo ratings yet

- Tmint Creative - Penelusuran GoogleDocument1 pageTmint Creative - Penelusuran GoogleNur ImanahNo ratings yet

- Multiple Choice: - ComputationalDocument4 pagesMultiple Choice: - ComputationalCarlo ParasNo ratings yet

- Bill of Materials - BOMDocument12 pagesBill of Materials - BOMIbnouachir AbderrazakNo ratings yet

- Karina Market Structure SummaryDocument4 pagesKarina Market Structure SummaryKarina Permata SariNo ratings yet

- Competing With It: Fundamentals of Strategic AdvantageDocument16 pagesCompeting With It: Fundamentals of Strategic Advantagejin_adrianNo ratings yet

- Brief Note On HRIS - Downsizing - VRS - RetrenchmentDocument2 pagesBrief Note On HRIS - Downsizing - VRS - RetrenchmentDanìél Koùichi HajongNo ratings yet

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet

- Strategic Management (BEG499 SM) (Elective)Document2 pagesStrategic Management (BEG499 SM) (Elective)Anil MarsaniNo ratings yet

- Marketing Plan: 1: Define Your BusinessDocument12 pagesMarketing Plan: 1: Define Your Businessdrken3No ratings yet

- 3 DERIVATIVES AND HEDGING ACTIVITIES FinalDocument2 pages3 DERIVATIVES AND HEDGING ACTIVITIES FinalCha ChieNo ratings yet

- Rethinking Foundation of EthicsDocument15 pagesRethinking Foundation of EthicstalentaNo ratings yet

- SCM SlidesDocument15 pagesSCM SlidesAmna NoorNo ratings yet

- Hospice Nurse Job DescriptionDocument5 pagesHospice Nurse Job DescriptionKasia KuzakaNo ratings yet

- Strategy - Creation of A CompanyDocument13 pagesStrategy - Creation of A CompanyJoana ToméNo ratings yet

- Title of The Presentation: BA (Hons) Global Business and Entrepreneurship (Foundation Year) Global Business SchoolDocument9 pagesTitle of The Presentation: BA (Hons) Global Business and Entrepreneurship (Foundation Year) Global Business SchoolVinnie plaaNo ratings yet

- TOT AgreementDocument138 pagesTOT Agreementchinnadurai33No ratings yet

- Job Vacancy Announcement Action Contre La Faim-Myanmar: Head of Project (Nutrition)Document3 pagesJob Vacancy Announcement Action Contre La Faim-Myanmar: Head of Project (Nutrition)draftdelete101 errorNo ratings yet

- Backdoor ListingDocument10 pagesBackdoor ListingAryan HateNo ratings yet

- How To Design A Clothing Store: Interior Design and FunctionalityDocument5 pagesHow To Design A Clothing Store: Interior Design and FunctionalityNamit BaserNo ratings yet

- Sample 4Document97 pagesSample 4Salma FarozeNo ratings yet

- CA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024Document13 pagesCA Intermediate Advanced Accounting Mock Test 19 - 01 - 2024rohit 6375No ratings yet

- Export Finance ProjectDocument67 pagesExport Finance ProjectVinay Singh67% (3)

- Cash FlowsDocument26 pagesCash Flowsvickyprimus100% (1)

- Top 3 Brands: Head and Shoulders Pantene Dove Sachet Sachet SachetDocument11 pagesTop 3 Brands: Head and Shoulders Pantene Dove Sachet Sachet SachetVAIJAYANTI JENANo ratings yet

- Keynote Speech of Secretary Roy A. Cimatu Department of Environment and Natural ResourcesDocument6 pagesKeynote Speech of Secretary Roy A. Cimatu Department of Environment and Natural Resourcesmonkeybike88No ratings yet