Download as docx, pdf, or txt

You might also like

- GED (Chapter 1,2 Test) Q With AnswersDocument7 pagesGED (Chapter 1,2 Test) Q With AnswersSapa PynGNo ratings yet

- NCERT Class 12 Accountancy Part 2Document329 pagesNCERT Class 12 Accountancy Part 2KishorVedpathak100% (2)

- Question Bank Answer: UNIT 4: Company FormationDocument5 pagesQuestion Bank Answer: UNIT 4: Company Formationameyk89No ratings yet

- Companies Act 1994 Final PDFDocument7 pagesCompanies Act 1994 Final PDFCryptic LollNo ratings yet

- Memorandum of AssociationDocument9 pagesMemorandum of Associationutkarshmannu.ismsNo ratings yet

- Law Important QuestionsDocument30 pagesLaw Important QuestionsSudarshan TakNo ratings yet

- Acounting RPDocument9 pagesAcounting RPVyshnaviNo ratings yet

- Formation of A Company PPT - 230729 - 143526Document24 pagesFormation of A Company PPT - 230729 - 143526manjushaa1618No ratings yet

- Finalized Business LawDocument13 pagesFinalized Business LawbooksNo ratings yet

- Memorandum and Articles of Association - 1Document6 pagesMemorandum and Articles of Association - 1Lynn XiaoJie0% (1)

- Business LawDocument8 pagesBusiness LawRyhanul IslamNo ratings yet

- Company Unit-2Document6 pagesCompany Unit-2thehackerdude09No ratings yet

- Unit 3 - Companies Act 1. Define CompanyDocument17 pagesUnit 3 - Companies Act 1. Define CompanyDr. S. PRIYA DURGA MBA-STAFFNo ratings yet

- Chapter 29-Formation of A CompanyDocument14 pagesChapter 29-Formation of A CompanyPooja SKNo ratings yet

- Company Law NotesDocument5 pagesCompany Law NotesRanjan BaradurNo ratings yet

- Incorporation MoA AoADocument26 pagesIncorporation MoA AoAFarhanNo ratings yet

- Formation of A CompanyDocument11 pagesFormation of A CompanyGarv GroverNo ratings yet

- Types & Kinds of CompaniesDocument7 pagesTypes & Kinds of Companiesdurgesh varunNo ratings yet

- Class Notes For Company Law and Procedure-Topic 3Document11 pagesClass Notes For Company Law and Procedure-Topic 3nomsa mweetwaNo ratings yet

- Company Law Comprehensive NotesDocument51 pagesCompany Law Comprehensive Noteskrvatsal03No ratings yet

- Business LawDocument67 pagesBusiness LawSaMeia FarhatNo ratings yet

- Memorandum of AssociationDocument13 pagesMemorandum of Associationprathm_patel100% (1)

- Kslu Unit 4 Q & A Company LawDocument33 pagesKslu Unit 4 Q & A Company LawMG MaheshBabuNo ratings yet

- Share and Share Capital-1Document42 pagesShare and Share Capital-1nemewep527No ratings yet

- Memorandum of Association MOA and ArticlDocument13 pagesMemorandum of Association MOA and ArticlNeelakanta ANo ratings yet

- Memorandum of AssociationDocument18 pagesMemorandum of Associationh98hsmcgvqNo ratings yet

- Null 6Document55 pagesNull 6esmytricatiusNo ratings yet

- Business LawDocument15 pagesBusiness LawHimanshi YadavNo ratings yet

- Memorandum of AssociationDocument17 pagesMemorandum of AssociationSandeep MishraNo ratings yet

- Company AccountDocument6 pagesCompany AccountADEYANJU AKEEMNo ratings yet

- Company Law Lecture 15Document47 pagesCompany Law Lecture 15Fahmida HoqueNo ratings yet

- CH 7 Formation of A Company NOTESDocument8 pagesCH 7 Formation of A Company NOTESRiwaanNo ratings yet

- New Blog Post Company LawDocument6 pagesNew Blog Post Company Lawbhavitha birdalaNo ratings yet

- Abbl3144 Tutorial 3 AnswerDocument9 pagesAbbl3144 Tutorial 3 AnswerSooXueJiaNo ratings yet

- Legal Aspects of Business: MBA505BDocument45 pagesLegal Aspects of Business: MBA505BChayan GargNo ratings yet

- Company FNLDocument30 pagesCompany FNLpriyaNo ratings yet

- Company LawDocument4 pagesCompany LawShibu ShashankNo ratings yet

- FAQ On CA 2013Document14 pagesFAQ On CA 2013bbtqwrws78No ratings yet

- Memorandum of AssociationDocument19 pagesMemorandum of AssociationVishal0% (1)

- Borrowing Powers of CompanyDocument37 pagesBorrowing Powers of CompanyRohan NambiarNo ratings yet

- Probable QuestionsDocument15 pagesProbable QuestionsSanjeev RawatNo ratings yet

- Financial Accounting 9Th Edition Hoggett Solutions Manual Full Chapter PDFDocument68 pagesFinancial Accounting 9Th Edition Hoggett Solutions Manual Full Chapter PDFDawnZimmermanxwcq100% (11)

- The Companies Act 2013 29 Chapters, 470 Sections & 7 SchedulesDocument16 pagesThe Companies Act 2013 29 Chapters, 470 Sections & 7 Schedulessuraj ksNo ratings yet

- Legal Aspects - Unit-2Document33 pagesLegal Aspects - Unit-2Vikram VikasNo ratings yet

- Company Law SemesterDocument31 pagesCompany Law Semestersparsh kaushalNo ratings yet

- Business LawDocument6 pagesBusiness Lawshikha singhNo ratings yet

- Figure 9. A Summary of The Positive and Negative Features of The Forms of BusinessDocument48 pagesFigure 9. A Summary of The Positive and Negative Features of The Forms of BusinessMARL VINCENT L LABITADNo ratings yet

- Company Law B.Com 4th Semester UNOMDocument31 pagesCompany Law B.Com 4th Semester UNOMnelace6253100% (4)

- Shares in Company ActDocument5 pagesShares in Company ActMohnish ChaudhariNo ratings yet

- Company LawDocument32 pagesCompany LawAnnonymous JoggerNo ratings yet

- The Companies (Amendment) Act 2015Document29 pagesThe Companies (Amendment) Act 2015Vikram PandyaNo ratings yet

- Symbi Notes II 2013Document91 pagesSymbi Notes II 2013JozosohalNo ratings yet

- Question and AnswerDocument8 pagesQuestion and Answerashish panwarNo ratings yet

- Companies Act 2013 and Consumer Protection ActDocument13 pagesCompanies Act 2013 and Consumer Protection ActNave2n adventurism & art works.No ratings yet

- Topic 6 Accounting For CompaniesDocument55 pagesTopic 6 Accounting For Companiestwahirwajeanpierre50No ratings yet

- Bba Ii Semester III: Subject: Secretarial Practice and Company ManagementDocument12 pagesBba Ii Semester III: Subject: Secretarial Practice and Company ManagementRaghuNo ratings yet

- Lecture6 Coperate FinanceDocument14 pagesLecture6 Coperate FinanceFaint MokgokongNo ratings yet

- LLC: A Complete Guide To Limited Liability Companies And Setting Up Your Own LLCFrom EverandLLC: A Complete Guide To Limited Liability Companies And Setting Up Your Own LLCNo ratings yet

- Textbook of Urgent Care Management: Chapter 6, Business Formation and Entity StructuringFrom EverandTextbook of Urgent Care Management: Chapter 6, Business Formation and Entity StructuringNo ratings yet

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- NII MCQsDocument8 pagesNII MCQsshobha digheNo ratings yet

- Infrastructure Development NotesDocument20 pagesInfrastructure Development Notesshobha digheNo ratings yet

- Land Acquisition Act MCQDocument2 pagesLand Acquisition Act MCQshobha dighe100% (11)

- Private International Law NotesDocument10 pagesPrivate International Law Notesshobha digheNo ratings yet

- IRA MCQsDocument18 pagesIRA MCQsshobha digheNo ratings yet

- Working Capital ManagementDocument56 pagesWorking Capital ManagementVarun KalseNo ratings yet

- Methods of Engineering Valuation - Lecture Material - DR MorakinyoDocument6 pagesMethods of Engineering Valuation - Lecture Material - DR MorakinyoEmmanuel OladeleNo ratings yet

- Asked: QuestionsDocument15 pagesAsked: QuestionsTushar NegiNo ratings yet

- Annual Report 2020 21 VFinalDocument400 pagesAnnual Report 2020 21 VFinalKshitij SrivastavaNo ratings yet

- Advanced Accounting Fischer11e - SMChap21Document24 pagesAdvanced Accounting Fischer11e - SMChap21sellertbsm2014No ratings yet

- PBCom V CA, G.R. No. 118552, February 5, 1996Document6 pagesPBCom V CA, G.R. No. 118552, February 5, 1996ademarNo ratings yet

- Cash and Cash EquivalentsDocument33 pagesCash and Cash EquivalentsJohn kyle Abbago100% (2)

- Consolidated Statement of Financial PositionDocument2 pagesConsolidated Statement of Financial PositionEvita Ayne TapitNo ratings yet

- ICICI Securities Initiating Coverage On Landmark Cars With An UPSIDEDocument19 pagesICICI Securities Initiating Coverage On Landmark Cars With An UPSIDEDusk TilldownNo ratings yet

- C B E M: WWW - Isap.edu - PH Adminoffice@isap - Edu.phDocument5 pagesC B E M: WWW - Isap.edu - PH Adminoffice@isap - Edu.phJohn Mark PalapuzNo ratings yet

- 4&5 AssignmentDocument18 pages4&5 AssignmentQaulan Tsaqila100% (2)

- Stuvia 701062 Advanced Questions On Sa Tax Prescribed Book 2020Document369 pagesStuvia 701062 Advanced Questions On Sa Tax Prescribed Book 2020ConradeNo ratings yet

- Tugas CashFlow - Aura Anggun Permatasari - 21812141027 - A'21Document4 pagesTugas CashFlow - Aura Anggun Permatasari - 21812141027 - A'21Aura Anggun Permatasari auraanggun.2021No ratings yet

- Tutorial 8 - Correction of Error - 42762Document3 pagesTutorial 8 - Correction of Error - 42762Sarah RanduNo ratings yet

- NPTEL Course: Course Title: Security Analysis and Portfolio Management Course Coordinator: Dr. Jitendra MahakudDocument8 pagesNPTEL Course: Course Title: Security Analysis and Portfolio Management Course Coordinator: Dr. Jitendra MahakudAnkit ChawlaNo ratings yet

- Bdos Financial Management and Audit Act, 2007-11Document33 pagesBdos Financial Management and Audit Act, 2007-11DecoMichaelNo ratings yet

- Summative Assessment: Financial Performance ManagementDocument24 pagesSummative Assessment: Financial Performance ManagementAshley WoodNo ratings yet

- U3A2 - Recording Transactions in A Journal - TemplateDocument3 pagesU3A2 - Recording Transactions in A Journal - TemplateJay PatelNo ratings yet

- Chapter 4: Redemption of Pref Share & Debentures Topic: Redemption of Pref Shares. Practice QuestionsDocument34 pagesChapter 4: Redemption of Pref Share & Debentures Topic: Redemption of Pref Shares. Practice QuestionsMercy GamingNo ratings yet

- Power of Attorney (General)Document3 pagesPower of Attorney (General)Banerjee SuvranilNo ratings yet

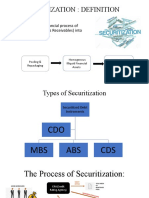

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- Direct and Indirect TaxesDocument14 pagesDirect and Indirect Taxeskratika singhNo ratings yet

- 36 Loss Disallowance Slides and ExamplesDocument51 pages36 Loss Disallowance Slides and ExamplesCourt RobertsNo ratings yet

- 24122405635Document4 pages24122405635Vy Đặng ThảoNo ratings yet

- Factors Influencing Corporate GovernanceDocument5 pagesFactors Influencing Corporate GovernanceShariq Ansari M100% (2)

- ChallanDocument1 pageChallannaresh maddu100% (1)

- Infrastructure Leasing & Financial Service LimitedDocument3 pagesInfrastructure Leasing & Financial Service LimitedShivam MittalNo ratings yet

- General LedgerDocument6 pagesGeneral LedgerErika Sta. AnaNo ratings yet

- ) Price AdjustmentDocument17 pages) Price AdjustmentPalak JainNo ratings yet