Nisha Nur Aini - 43219110183 - TM 01 - AKM II

Nisha Nur Aini - 43219110183 - TM 01 - AKM II

You might also like

- E10 7Document7 pagesE10 7fabiarachid100% (1)

- Test Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 6th Edition by StickneyDocument35 pagesTest Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 6th Edition by StickneyTiffany CarswellNo ratings yet

- Soal Debt InvestmentDocument5 pagesSoal Debt InvestmentKyle Kuro0% (1)

- ch17 180206123815 PDFDocument75 pagesch17 180206123815 PDFYeni Amelia100% (1)

- AKM 2 - Forum 7 - Andres - 43220110067Document13 pagesAKM 2 - Forum 7 - Andres - 43220110067tes doangNo ratings yet

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doangNo ratings yet

- Tugas Kel 3 (P14.2, P14.4)Document7 pagesTugas Kel 3 (P14.2, P14.4)Alexandra AmadeaNo ratings yet

- E13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofDocument4 pagesE13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofChupa HesNo ratings yet

- Tugas Jatuh Tempo Sesi 9Document8 pagesTugas Jatuh Tempo Sesi 9Araminta DewatiNo ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- E21 16Document2 pagesE21 16Warmthx0% (1)

- UUbillDocument1 pageUUbillGaby PlayGame0% (1)

- TR 2 IndahDocument3 pagesTR 2 IndahIndahyuliaputriNo ratings yet

- Rika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02Document5 pagesRika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02MARCHO AGUSTANo ratings yet

- Intermediate Accounting: Assignment 2Document2 pagesIntermediate Accounting: Assignment 2Putri SerlyNo ratings yet

- Akuntansi Keuangan Ii Sesi 6Document5 pagesAkuntansi Keuangan Ii Sesi 6vidiamyNo ratings yet

- Problem 21.3Document3 pagesProblem 21.3Fayed Rahman MahendraNo ratings yet

- E7 24Document3 pagesE7 24Muhammad Syafiq Ramadhan100% (1)

- Tugas Latihan Soal EPSDocument4 pagesTugas Latihan Soal EPSNaoya FaldinyNo ratings yet

- Muh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9Document3 pagesMuh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9RismayantiNo ratings yet

- Online Payment MechanismDocument14 pagesOnline Payment MechanismAlan Fletcher WheelerNo ratings yet

- Working 4Document8 pagesWorking 4Hà Lê DuyNo ratings yet

- E14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsDocument3 pagesE14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsAsuna SanNo ratings yet

- Week13 SolutionsDocument14 pagesWeek13 SolutionsRian RorresNo ratings yet

- CH 14Document71 pagesCH 14Febriana Nurul HidayahNo ratings yet

- Nisha Nur Aini - 43219110183 - TM 02 - AKM IIDocument11 pagesNisha Nur Aini - 43219110183 - TM 02 - AKM IInisha nuraini100% (1)

- Erika Christina - LD53 - Latihan KPDocument14 pagesErika Christina - LD53 - Latihan KPNatasha HerlianaNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanNo ratings yet

- Soal Ch. 15Document6 pagesSoal Ch. 15Kyle KuroNo ratings yet

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- E14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanyDocument3 pagesE14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanySandra SholehahNo ratings yet

- Soal Latihan Minggu 4Document9 pagesSoal Latihan Minggu 4Alifia AprizilaNo ratings yet

- Ch. 17 Exercises and Answers - TaggedDocument6 pagesCh. 17 Exercises and Answers - TaggedHaitham Ebrahim100% (1)

- Kelompok 6 Latihan Soal EquityDocument7 pagesKelompok 6 Latihan Soal EquityTria SalzanabillaNo ratings yet

- Tutorial Laporan Arus KasDocument17 pagesTutorial Laporan Arus KasRatna DwiNo ratings yet

- Exercise 18Document9 pagesExercise 18raihan aqilNo ratings yet

- AKM - Kelompok 5Document8 pagesAKM - Kelompok 5lailafitriyani100% (1)

- Zulfitri Handayani - A031191125 (Akkeu P15-3)Document6 pagesZulfitri Handayani - A031191125 (Akkeu P15-3)RismayantiNo ratings yet

- Jawaban TugasDocument7 pagesJawaban TugasRani AdhirasariNo ratings yet

- Exercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueDocument9 pagesExercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueManuel Magadatu100% (1)

- CH 18Document130 pagesCH 18Indah PNo ratings yet

- T4 - (Assets) - Qs and SolutionDocument22 pagesT4 - (Assets) - Qs and SolutionCalvin MaNo ratings yet

- Akuntansi KeuanganDocument11 pagesAkuntansi KeuanganDyan NoviaNo ratings yet

- 13 2Document2 pages13 2Evelyn Roldan100% (7)

- E15-2 (Recording The Issuance of Ordinary and Preference Shares) AbernathyDocument5 pagesE15-2 (Recording The Issuance of Ordinary and Preference Shares) AbernathyAsuna SanNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- CH 21Document48 pagesCH 21Iris MaNo ratings yet

- Jawaban Soal Latihan Ch.11Document2 pagesJawaban Soal Latihan Ch.11Wira DinataNo ratings yet

- Jawaban Tugas Inventory 2Document8 pagesJawaban Tugas Inventory 2wijayaNo ratings yet

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzeNo ratings yet

- Akuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADocument8 pagesAkuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADedep0% (1)

- Ch14 180205115701 Answers For The Practice QuestionsDocument72 pagesCh14 180205115701 Answers For The Practice QuestionsMikaela O.No ratings yet

- Tugas PPE 1Document12 pagesTugas PPE 1Bertha Liona0% (1)

- Week 12Document2 pagesWeek 12intan apriliyaniNo ratings yet

- Presented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019Document2 pagesPresented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019SalsabiilaNo ratings yet

- A311Chapter 10 ProblemsDocument43 pagesA311Chapter 10 ProblemsVibria Rezki Ananda50% (2)

- Tugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareDocument2 pagesTugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareClarissa NastaniaNo ratings yet

- Ch9 ExercisesDocument15 pagesCh9 ExercisesMarshanda Berlianti100% (1)

- PA2 - X - IESP - HW11 - G4 - Yustina Putri DewiDocument7 pagesPA2 - X - IESP - HW11 - G4 - Yustina Putri Dewimellany echa putriNo ratings yet

- 2019 June 23 ACT 701 Chapter 3 Problems and SolutionDocument21 pages2019 June 23 ACT 701 Chapter 3 Problems and SolutionZisanNo ratings yet

- Workbook International Acc1 - C.06Document7 pagesWorkbook International Acc1 - C.06Lam HoàngNo ratings yet

- Presentation of FS With AnsDocument19 pagesPresentation of FS With AnsMichael BongalontaNo ratings yet

- ACCT 551 Week2 PracticeQuestions SolutionsDocument5 pagesACCT 551 Week2 PracticeQuestions SolutionsMD SomratNo ratings yet

- SAP FI Certification Actual QuestionDocument4 pagesSAP FI Certification Actual QuestionkhalidmahmoodqumarNo ratings yet

- Residential Fee Summary 2024 - 0Document2 pagesResidential Fee Summary 2024 - 0Serevinna DewitaNo ratings yet

- CTT Exam Application FormDocument1 pageCTT Exam Application FormLeah MoscareNo ratings yet

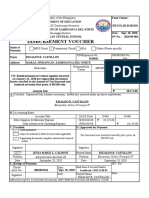

- Disbursement Voucher - Check #101-200Document91 pagesDisbursement Voucher - Check #101-200Jessa Mariz Lecias CalimotNo ratings yet

- 02 Pirovano V CIRDocument1 page02 Pirovano V CIRCP LugoNo ratings yet

- Chapter 2 MCQs On House PropertyDocument24 pagesChapter 2 MCQs On House PropertyRam Iyer100% (1)

- Currency Pairs Cheat SheetDocument2 pagesCurrency Pairs Cheat SheetJozefNo ratings yet

- STMT 00000080066704629 1706962529691Document3 pagesSTMT 00000080066704629 1706962529691pravinpund2002No ratings yet

- 6 April 2023Document7 pages6 April 2023mapondaglodiNo ratings yet

- Soa 0030300152406Document1 pageSoa 0030300152406Maria Theresa LimosNo ratings yet

- C7021-23-0268408 09-05-2023 10-05-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP Virender GaurDocument1 pageC7021-23-0268408 09-05-2023 10-05-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP Virender GaurSabika NaqviNo ratings yet

- Stripe's Guide To Payment MethodsDocument33 pagesStripe's Guide To Payment MethodsYogesh Gutta100% (1)

- DeductionsDocument9 pagesDeductionsSarvar PathanNo ratings yet

- Propertytax BasicsDocument29 pagesPropertytax BasicsO'Connor AssociateNo ratings yet

- Sold To:: FC WB 03269940 X2015400 00000014875 0Document2 pagesSold To:: FC WB 03269940 X2015400 00000014875 0RuodNo ratings yet

- Electronic Contribution Collection List SummaryDocument2 pagesElectronic Contribution Collection List Summary4U Gadgets & Phone Shop ComplianceNo ratings yet

- Public Perception On Cash Less Transactions in IndiaDocument16 pagesPublic Perception On Cash Less Transactions in IndiaMayukh BhattacharjeeNo ratings yet

- Letter Requesting PaymentDocument13 pagesLetter Requesting PaymentBUDINo ratings yet

- Bengaluru North University: Exam Application FormDocument1 pageBengaluru North University: Exam Application FormRoopa S AcharyaNo ratings yet

- TaxationDocument13 pagesTaxationpravas naikNo ratings yet

- Tally Final ProjectDocument124 pagesTally Final Projectmastermind_asia9389100% (2)

- Zomaland Invoice Ce438443Document1 pageZomaland Invoice Ce438443PRANAY SHRIDHARNo ratings yet

- Commissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Document2 pagesCommissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Jennilyn Gulfan YaseNo ratings yet

- Objective of The Course:: NSCI Elearning Course On " Electrical Safety"Document2 pagesObjective of The Course:: NSCI Elearning Course On " Electrical Safety"Himanshu MishraNo ratings yet

- Anita SahgalDocument3 pagesAnita SahgalNaveen AsthanaNo ratings yet

- Ertificat E of D FN Resident For Indone T Withh F R - DGT 2: C O Micile O ON SIA AX Oldin G O M)Document2 pagesErtificat E of D FN Resident For Indone T Withh F R - DGT 2: C O Micile O ON SIA AX Oldin G O M)Reviansyah Machfudin YusufNo ratings yet

- POR Country/port/region POD Country/port/region: Current LevelDocument4 pagesPOR Country/port/region POD Country/port/region: Current LevelNam SầnNo ratings yet

Download as docx, pdf, or txt

You might also like

- E10 7Document7 pagesE10 7fabiarachid100% (1)

- Test Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 6th Edition by StickneyDocument35 pagesTest Bank For Financial Reporting Financial Statement Analysis and Valuation A Strategic Perspective 6th Edition by StickneyTiffany CarswellNo ratings yet

- Soal Debt InvestmentDocument5 pagesSoal Debt InvestmentKyle Kuro0% (1)

- ch17 180206123815 PDFDocument75 pagesch17 180206123815 PDFYeni Amelia100% (1)

- AKM 2 - Forum 7 - Andres - 43220110067Document13 pagesAKM 2 - Forum 7 - Andres - 43220110067tes doangNo ratings yet

- Problem: Andres Adi Putra S 43220110067 AKM2-Forum 6Document17 pagesProblem: Andres Adi Putra S 43220110067 AKM2-Forum 6tes doangNo ratings yet

- Tugas Kel 3 (P14.2, P14.4)Document7 pagesTugas Kel 3 (P14.2, P14.4)Alexandra AmadeaNo ratings yet

- E13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofDocument4 pagesE13.2 (LO 1) (Accounts and Notes Payable) The Following Are Selected 2022 Transactions ofChupa HesNo ratings yet

- Tugas Jatuh Tempo Sesi 9Document8 pagesTugas Jatuh Tempo Sesi 9Araminta DewatiNo ratings yet

- Jawaban BE15 - AKMDocument3 pagesJawaban BE15 - AKMMazz BadruezNo ratings yet

- E21 16Document2 pagesE21 16Warmthx0% (1)

- UUbillDocument1 pageUUbillGaby PlayGame0% (1)

- TR 2 IndahDocument3 pagesTR 2 IndahIndahyuliaputriNo ratings yet

- Rika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02Document5 pagesRika Ristiani - Akuntansi Keuangan Menengah 2 - TM-02MARCHO AGUSTANo ratings yet

- Intermediate Accounting: Assignment 2Document2 pagesIntermediate Accounting: Assignment 2Putri SerlyNo ratings yet

- Akuntansi Keuangan Ii Sesi 6Document5 pagesAkuntansi Keuangan Ii Sesi 6vidiamyNo ratings yet

- Problem 21.3Document3 pagesProblem 21.3Fayed Rahman MahendraNo ratings yet

- E7 24Document3 pagesE7 24Muhammad Syafiq Ramadhan100% (1)

- Tugas Latihan Soal EPSDocument4 pagesTugas Latihan Soal EPSNaoya FaldinyNo ratings yet

- Muh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9Document3 pagesMuh - Syukur (A031191077) Akuntansi Keuangan - Exercise E.12.9RismayantiNo ratings yet

- Online Payment MechanismDocument14 pagesOnline Payment MechanismAlan Fletcher WheelerNo ratings yet

- Working 4Document8 pagesWorking 4Hà Lê DuyNo ratings yet

- E14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsDocument3 pagesE14-3 (Entries For Bond Transactions) Presented Below Are Two Independent SituationsAsuna SanNo ratings yet

- Week13 SolutionsDocument14 pagesWeek13 SolutionsRian RorresNo ratings yet

- CH 14Document71 pagesCH 14Febriana Nurul HidayahNo ratings yet

- Nisha Nur Aini - 43219110183 - TM 02 - AKM IIDocument11 pagesNisha Nur Aini - 43219110183 - TM 02 - AKM IInisha nuraini100% (1)

- Erika Christina - LD53 - Latihan KPDocument14 pagesErika Christina - LD53 - Latihan KPNatasha HerlianaNo ratings yet

- Exercise - Dilutive Securities - AdillaikhsaniDocument4 pagesExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanNo ratings yet

- Soal Ch. 15Document6 pagesSoal Ch. 15Kyle KuroNo ratings yet

- E22-6 (LO 2) Accounting Changes-DepreciationDocument6 pagesE22-6 (LO 2) Accounting Changes-DepreciationRiana DeztianiNo ratings yet

- E14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanyDocument3 pagesE14-8 (Entries and Questions For Bond Transactions) On June 30, 2010, Mackers CompanySandra SholehahNo ratings yet

- Soal Latihan Minggu 4Document9 pagesSoal Latihan Minggu 4Alifia AprizilaNo ratings yet

- Ch. 17 Exercises and Answers - TaggedDocument6 pagesCh. 17 Exercises and Answers - TaggedHaitham Ebrahim100% (1)

- Kelompok 6 Latihan Soal EquityDocument7 pagesKelompok 6 Latihan Soal EquityTria SalzanabillaNo ratings yet

- Tutorial Laporan Arus KasDocument17 pagesTutorial Laporan Arus KasRatna DwiNo ratings yet

- Exercise 18Document9 pagesExercise 18raihan aqilNo ratings yet

- AKM - Kelompok 5Document8 pagesAKM - Kelompok 5lailafitriyani100% (1)

- Zulfitri Handayani - A031191125 (Akkeu P15-3)Document6 pagesZulfitri Handayani - A031191125 (Akkeu P15-3)RismayantiNo ratings yet

- Jawaban TugasDocument7 pagesJawaban TugasRani AdhirasariNo ratings yet

- Exercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueDocument9 pagesExercises: Ex. 9-143-Lower-Of-Cost-Or-Net Realizable ValueManuel Magadatu100% (1)

- CH 18Document130 pagesCH 18Indah PNo ratings yet

- T4 - (Assets) - Qs and SolutionDocument22 pagesT4 - (Assets) - Qs and SolutionCalvin MaNo ratings yet

- Akuntansi KeuanganDocument11 pagesAkuntansi KeuanganDyan NoviaNo ratings yet

- 13 2Document2 pages13 2Evelyn Roldan100% (7)

- E15-2 (Recording The Issuance of Ordinary and Preference Shares) AbernathyDocument5 pagesE15-2 (Recording The Issuance of Ordinary and Preference Shares) AbernathyAsuna SanNo ratings yet

- Nama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure InternalDocument6 pagesNama: Melvina Puhut Siregar Nim: 1932150049 E7-23 (Petty Cash) Mcmann, Inc. Decided To Establish A Petty Cash Fund To Help Ensure Internalmelvina siregarNo ratings yet

- CH 21Document48 pagesCH 21Iris MaNo ratings yet

- Jawaban Soal Latihan Ch.11Document2 pagesJawaban Soal Latihan Ch.11Wira DinataNo ratings yet

- Jawaban Tugas Inventory 2Document8 pagesJawaban Tugas Inventory 2wijayaNo ratings yet

- Pr. 4-146-Income StatementDocument13 pagesPr. 4-146-Income StatementElene SamnidzeNo ratings yet

- Akuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADocument8 pagesAkuntansi Keuangan 1 TUGAS E5.11, E5.12, E5.15 DAN E5.16 Kelas ADedep0% (1)

- Ch14 180205115701 Answers For The Practice QuestionsDocument72 pagesCh14 180205115701 Answers For The Practice QuestionsMikaela O.No ratings yet

- Tugas PPE 1Document12 pagesTugas PPE 1Bertha Liona0% (1)

- Week 12Document2 pagesWeek 12intan apriliyaniNo ratings yet

- Presented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019Document2 pagesPresented Below Is The Trial Balance of Vivaldi Spa at December 31, 2019SalsabiilaNo ratings yet

- A311Chapter 10 ProblemsDocument43 pagesA311Chapter 10 ProblemsVibria Rezki Ananda50% (2)

- Tugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareDocument2 pagesTugas Akuntansi Menengah Ii Dilutive Securities & Earnings Per ShareClarissa NastaniaNo ratings yet

- Ch9 ExercisesDocument15 pagesCh9 ExercisesMarshanda Berlianti100% (1)

- PA2 - X - IESP - HW11 - G4 - Yustina Putri DewiDocument7 pagesPA2 - X - IESP - HW11 - G4 - Yustina Putri Dewimellany echa putriNo ratings yet

- 2019 June 23 ACT 701 Chapter 3 Problems and SolutionDocument21 pages2019 June 23 ACT 701 Chapter 3 Problems and SolutionZisanNo ratings yet

- Workbook International Acc1 - C.06Document7 pagesWorkbook International Acc1 - C.06Lam HoàngNo ratings yet

- Presentation of FS With AnsDocument19 pagesPresentation of FS With AnsMichael BongalontaNo ratings yet

- ACCT 551 Week2 PracticeQuestions SolutionsDocument5 pagesACCT 551 Week2 PracticeQuestions SolutionsMD SomratNo ratings yet

- SAP FI Certification Actual QuestionDocument4 pagesSAP FI Certification Actual QuestionkhalidmahmoodqumarNo ratings yet

- Residential Fee Summary 2024 - 0Document2 pagesResidential Fee Summary 2024 - 0Serevinna DewitaNo ratings yet

- CTT Exam Application FormDocument1 pageCTT Exam Application FormLeah MoscareNo ratings yet

- Disbursement Voucher - Check #101-200Document91 pagesDisbursement Voucher - Check #101-200Jessa Mariz Lecias CalimotNo ratings yet

- 02 Pirovano V CIRDocument1 page02 Pirovano V CIRCP LugoNo ratings yet

- Chapter 2 MCQs On House PropertyDocument24 pagesChapter 2 MCQs On House PropertyRam Iyer100% (1)

- Currency Pairs Cheat SheetDocument2 pagesCurrency Pairs Cheat SheetJozefNo ratings yet

- STMT 00000080066704629 1706962529691Document3 pagesSTMT 00000080066704629 1706962529691pravinpund2002No ratings yet

- 6 April 2023Document7 pages6 April 2023mapondaglodiNo ratings yet

- Soa 0030300152406Document1 pageSoa 0030300152406Maria Theresa LimosNo ratings yet

- C7021-23-0268408 09-05-2023 10-05-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP Virender GaurDocument1 pageC7021-23-0268408 09-05-2023 10-05-2023 Sold by (Pharmacy) Bill To / Ship To (Patient) Healthsaverz Medical LLP Virender GaurSabika NaqviNo ratings yet

- Stripe's Guide To Payment MethodsDocument33 pagesStripe's Guide To Payment MethodsYogesh Gutta100% (1)

- DeductionsDocument9 pagesDeductionsSarvar PathanNo ratings yet

- Propertytax BasicsDocument29 pagesPropertytax BasicsO'Connor AssociateNo ratings yet

- Sold To:: FC WB 03269940 X2015400 00000014875 0Document2 pagesSold To:: FC WB 03269940 X2015400 00000014875 0RuodNo ratings yet

- Electronic Contribution Collection List SummaryDocument2 pagesElectronic Contribution Collection List Summary4U Gadgets & Phone Shop ComplianceNo ratings yet

- Public Perception On Cash Less Transactions in IndiaDocument16 pagesPublic Perception On Cash Less Transactions in IndiaMayukh BhattacharjeeNo ratings yet

- Letter Requesting PaymentDocument13 pagesLetter Requesting PaymentBUDINo ratings yet

- Bengaluru North University: Exam Application FormDocument1 pageBengaluru North University: Exam Application FormRoopa S AcharyaNo ratings yet

- TaxationDocument13 pagesTaxationpravas naikNo ratings yet

- Tally Final ProjectDocument124 pagesTally Final Projectmastermind_asia9389100% (2)

- Zomaland Invoice Ce438443Document1 pageZomaland Invoice Ce438443PRANAY SHRIDHARNo ratings yet

- Commissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Document2 pagesCommissioner of Internal Revenue vs. S.C. Johnson and Sons, Inc. (G.R. No. 127105, June 25, 1999)Jennilyn Gulfan YaseNo ratings yet

- Objective of The Course:: NSCI Elearning Course On " Electrical Safety"Document2 pagesObjective of The Course:: NSCI Elearning Course On " Electrical Safety"Himanshu MishraNo ratings yet

- Anita SahgalDocument3 pagesAnita SahgalNaveen AsthanaNo ratings yet

- Ertificat E of D FN Resident For Indone T Withh F R - DGT 2: C O Micile O ON SIA AX Oldin G O M)Document2 pagesErtificat E of D FN Resident For Indone T Withh F R - DGT 2: C O Micile O ON SIA AX Oldin G O M)Reviansyah Machfudin YusufNo ratings yet

- POR Country/port/region POD Country/port/region: Current LevelDocument4 pagesPOR Country/port/region POD Country/port/region: Current LevelNam SầnNo ratings yet