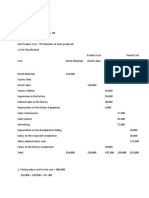

Cost Accumulation + Cost Measurement

Cost Accumulation + Cost Measurement

You might also like

- Comprehensive Synthetic Dreadlock Information Final PDFDocument42 pagesComprehensive Synthetic Dreadlock Information Final PDFmegan_pritchard9016100% (1)

- AME - 2022 - Tutorial 4 - SolutionsDocument24 pagesAME - 2022 - Tutorial 4 - SolutionsjjpasemperNo ratings yet

- ManAcc Quiz 3 - FinalDocument18 pagesManAcc Quiz 3 - FinalDeepannita ChakrabortyNo ratings yet

- Example of CFS IIUM Accounting 2 ReportDocument16 pagesExample of CFS IIUM Accounting 2 ReportSyuhada Rosleen100% (1)

- Cost Accounting AssignmentDocument6 pagesCost Accounting AssignmentRamalu Dinesh ReddyNo ratings yet

- STD 957Document77 pagesSTD 957Erasmo ColonaNo ratings yet

- Tyre ManufacturingDocument57 pagesTyre ManufacturingSahal Babu60% (5)

- WG C2 II C2 Football Production II Management AccountingDocument114 pagesWG C2 II C2 Football Production II Management AccountingSalot DhyeyNo ratings yet

- Execise2 31-34Document5 pagesExecise2 31-34richel sanchezNo ratings yet

- Chapter VII RevisedDocument21 pagesChapter VII RevisedJonabelle C. BiliganNo ratings yet

- Garcia HW Problem SolvingDocument5 pagesGarcia HW Problem SolvingTristan GarciaNo ratings yet

- Estimated Cost SheetDocument3 pagesEstimated Cost SheetJasdeep Singh Deepu100% (1)

- Modul 4 Rafif F PDocument11 pagesModul 4 Rafif F PAkhdan aNo ratings yet

- CH10Document34 pagesCH10sihlemooi3No ratings yet

- Acc 4Document3 pagesAcc 4Izzah NawawiNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- Pricing of A Product:-: 1. Fit and Flare DressDocument5 pagesPricing of A Product:-: 1. Fit and Flare DressAMAN RAJNo ratings yet

- Cases On Activity Based Costing SystemDocument6 pagesCases On Activity Based Costing SystemEnusah PeterNo ratings yet

- Accounting For Managers, IIAM-VizagDocument13 pagesAccounting For Managers, IIAM-VizagDileep DeepuNo ratings yet

- Book 2Document4 pagesBook 2DANASOPHIA LEONARDONo ratings yet

- Case Study - ABC CostingDocument3 pagesCase Study - ABC CostingDaiannaNo ratings yet

- TUTORIAL Manufacturing With SolutionDocument10 pagesTUTORIAL Manufacturing With SolutionmaiNo ratings yet

- SINGH007 Ans Homework Lec 14 To 21Document47 pagesSINGH007 Ans Homework Lec 14 To 21Lau Chun GuiNo ratings yet

- Costing 2 Material - 014417Document40 pagesCosting 2 Material - 014417sirjamtech36No ratings yet

- Chapter 4-Test Material 4 1Document6 pagesChapter 4-Test Material 4 1Marcus MonocayNo ratings yet

- 05 Wilkerson Company Solution - StudentsDocument9 pages05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Fineclad Apparel - Rani Treasa - 2009209Document7 pagesFineclad Apparel - Rani Treasa - 2009209RaniNo ratings yet

- Week 4 - Seminar 3 Trimake Solution A) and B) OnlyDocument3 pagesWeek 4 - Seminar 3 Trimake Solution A) and B) Onlychina xiNo ratings yet

- Skema PSPM 17-18 Aa025Document4 pagesSkema PSPM 17-18 Aa025Dehey KNo ratings yet

- Acc 202 Exercise MyselfDocument5 pagesAcc 202 Exercise Myselfnhidiepnguyet08112004No ratings yet

- University of Finance and MarketingDocument8 pagesUniversity of Finance and MarketingQuế Phương NguyễnNo ratings yet

- Chapter 3 Job Order CostingDocument31 pagesChapter 3 Job Order CostingzamanNo ratings yet

- Acd10403 Solution Tutorial Manufacturing Account 2018Document9 pagesAcd10403 Solution Tutorial Manufacturing Account 2018Atqh ShamsuriNo ratings yet

- Cost and RevenueDocument17 pagesCost and RevenueKalpana MishraNo ratings yet

- HAslam - SolutionDocument12 pagesHAslam - SolutionSANA SAEEDNo ratings yet

- Unit CostingDocument3 pagesUnit CostingAnkit YadavNo ratings yet

- Best Financial Forecast FinalDocument13 pagesBest Financial Forecast Finalitsmethird.26No ratings yet

- Strategic ManagementDocument10 pagesStrategic Managementstk2796No ratings yet

- TUTORIAL 2 Cost ClassificationDocument7 pagesTUTORIAL 2 Cost Classificationsarahayeesha1No ratings yet

- Cost and Management Accounting 01 - Class NotesDocument114 pagesCost and Management Accounting 01 - Class NotessaurabhNo ratings yet

- Overheads Revision PDFDocument9 pagesOverheads Revision PDFSurajNo ratings yet

- Manufacturing AccountsDocument12 pagesManufacturing AccountsAdrian RamsundarNo ratings yet

- COSACC Assignment 2Document3 pagesCOSACC Assignment 2Kenneth Jim HipolitoNo ratings yet

- Maceda Glass and Aluminum Supply Job Order Cost SheetDocument8 pagesMaceda Glass and Aluminum Supply Job Order Cost SheetWarren CabunyagNo ratings yet

- Acc Sem 2Document2 pagesAcc Sem 2Muhammad SyahmiNo ratings yet

- CH 5 ExcelDocument37 pagesCH 5 ExcelssdsNo ratings yet

- Tutor 2Document13 pagesTutor 2francisaustria052623No ratings yet

- Aashutosh Agrawal - Dushyant Singh - 2020MBA027 - 2020MBA013Document8 pagesAashutosh Agrawal - Dushyant Singh - 2020MBA027 - 2020MBA013Ashita PunjabiNo ratings yet

- Session 25 & 26 - Budgeting and VarianceDocument20 pagesSession 25 & 26 - Budgeting and VarianceVinay PandeyNo ratings yet

- 12914sugg Pe2 gp2 1Document33 pages12914sugg Pe2 gp2 1harshrathore17579No ratings yet

- Answers:: Cost of Goods Manufactured Schedule For The Year EndedDocument5 pagesAnswers:: Cost of Goods Manufactured Schedule For The Year EndedAsim boidyaNo ratings yet

- Costing & Profitability: Magiclite Building SolutionsDocument16 pagesCosting & Profitability: Magiclite Building SolutionsPrince AroraNo ratings yet

- Prelim Exam-Boticario D. (SBA)Document5 pagesPrelim Exam-Boticario D. (SBA)Dominic E. BoticarioNo ratings yet

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- Answers To 11 - 16 Assignment in ABC PDFDocument3 pagesAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNo ratings yet

- Ppce Unit-5Document21 pagesPpce Unit-5Jackson ..No ratings yet

- CS Uthkarsh PaiDocument9 pagesCS Uthkarsh Paiankita sahuNo ratings yet

- Wilkerson Case Study Final1Document5 pagesWilkerson Case Study Final1Swapan Kumar Saha100% (1)

- Product Cost From TraditionalDocument5 pagesProduct Cost From TraditionalPrijulNo ratings yet

- Latex Products, Inc.: A Case Review by Group 2 EMBA 16Document16 pagesLatex Products, Inc.: A Case Review by Group 2 EMBA 16Lekan AjirotutuNo ratings yet

- Cost Accounting Notes Fall 19-1Document11 pagesCost Accounting Notes Fall 19-1AnoshiaNo ratings yet

- Lecture-7 Overhead (Part 5) PDFDocument10 pagesLecture-7 Overhead (Part 5) PDFNazmul-Hassan Sumon100% (5)

- Goods and Services Tax (GST) Transition To Sales and Services Tax (SST) : Impact On The Welfare of B40 and M40 Households in MalaysiaDocument9 pagesGoods and Services Tax (GST) Transition To Sales and Services Tax (SST) : Impact On The Welfare of B40 and M40 Households in MalaysiaSugenes CrgalsNo ratings yet

- Writing Portfolio Task 2 - Introductory Paragraph (Outline)Document4 pagesWriting Portfolio Task 2 - Introductory Paragraph (Outline)Sugenes CrgalsNo ratings yet

- Cel2103 - SCL Worksheet 13Document4 pagesCel2103 - SCL Worksheet 13Sugenes CrgalsNo ratings yet

- Cel2103 - SCL Worksheet 12Document3 pagesCel2103 - SCL Worksheet 12Sugenes CrgalsNo ratings yet

- T SR ARMET SIMRIT I II Tape Silicone Rubber Freudenberg NOK Equivalent Electrical InsulationDocument1 pageT SR ARMET SIMRIT I II Tape Silicone Rubber Freudenberg NOK Equivalent Electrical InsulationFábioNo ratings yet

- AdhesiveGuide PVC UK Master2023Document2 pagesAdhesiveGuide PVC UK Master2023YasserNo ratings yet

- Section-6 Bill of Quantities For Works (BOQ)Document2 pagesSection-6 Bill of Quantities For Works (BOQ)rk36266_732077041No ratings yet

- Biotech Gloves - Certifications - OpulentDocument24 pagesBiotech Gloves - Certifications - Opulentsaisridhar99No ratings yet

- Arkema Roof Systems: Featuring Encor Flex Polymers Kynar Aquatec PVDFDocument8 pagesArkema Roof Systems: Featuring Encor Flex Polymers Kynar Aquatec PVDFJose RodríguezNo ratings yet

- 7747-14 Kumho Ca 2015 PDG - FR - Ca - R15 PDFDocument73 pages7747-14 Kumho Ca 2015 PDG - FR - Ca - R15 PDFRichard TuckerNo ratings yet

- Ravago Yakup Ülçer - PAGEV Sustainable Material SolutionsDocument34 pagesRavago Yakup Ülçer - PAGEV Sustainable Material Solutionssara rafieiNo ratings yet

- Technical Details of Bonding ChemicalsDocument18 pagesTechnical Details of Bonding ChemicalsSangeet KarnaNo ratings yet

- DTD 5509 Aircraft Material SpecificationDocument5 pagesDTD 5509 Aircraft Material SpecificationMateen AhmadNo ratings yet

- Loctite® Power Grab® Ultimate Construction Adhesive: DescriptionDocument4 pagesLoctite® Power Grab® Ultimate Construction Adhesive: DescriptionAngieNo ratings yet

- Bobcat Rubber Track BrochureDocument4 pagesBobcat Rubber Track BrochureMartin Veliz100% (1)

- Company Profiles - CHINA GROUPDocument8 pagesCompany Profiles - CHINA GROUPAhmad Mursyidi KamaludinNo ratings yet

- SD Copy of Soft - 140 - JR - Edison - BOM Blue and Coral BlushDocument2 pagesSD Copy of Soft - 140 - JR - Edison - BOM Blue and Coral BlushShibly RahmanNo ratings yet

- Design + Construction Magazine (April To June 2019)Document80 pagesDesign + Construction Magazine (April To June 2019)Dina Jane QuilangNo ratings yet

- Standards For The Aerospace IndustryDocument1 pageStandards For The Aerospace IndustryAirtech AeroNo ratings yet

- Anti Blow Out StemDocument48 pagesAnti Blow Out StemimthiyazmuhammedNo ratings yet

- RubberDocument215 pagesRubberMocerneac Bogdan100% (1)

- Steel Rules PDFDocument20 pagesSteel Rules PDFyahsooyNo ratings yet

- Brazil Anvisa RDC 37 2015 Labeling Rubber Latex enDocument1 pageBrazil Anvisa RDC 37 2015 Labeling Rubber Latex enElaine NascimentoNo ratings yet

- Belts Mishuboshi (Industrial Power Transmission Products)Document90 pagesBelts Mishuboshi (Industrial Power Transmission Products)dangdinhthyNo ratings yet

- Rubber: CPE 728-Primary Processing of Plantation and Special CropsDocument8 pagesRubber: CPE 728-Primary Processing of Plantation and Special CropsMarjun CaguayNo ratings yet

- Method Statement For Concrete Repair Works.Document9 pagesMethod Statement For Concrete Repair Works.Munaku TafadzwaNo ratings yet

- Loxeal InfotechDocument16 pagesLoxeal InfotechAlexNo ratings yet

- Tyre Industry PDFDocument134 pagesTyre Industry PDFAnmol LimpaleNo ratings yet

- Segregated Data Base. (MFG)Document936 pagesSegregated Data Base. (MFG)srinivas100% (1)

- LMI Chemical Resistance GuideDocument8 pagesLMI Chemical Resistance GuideShesharam ChouhanNo ratings yet

Download as docx, pdf, or txt

You might also like

- Comprehensive Synthetic Dreadlock Information Final PDFDocument42 pagesComprehensive Synthetic Dreadlock Information Final PDFmegan_pritchard9016100% (1)

- AME - 2022 - Tutorial 4 - SolutionsDocument24 pagesAME - 2022 - Tutorial 4 - SolutionsjjpasemperNo ratings yet

- ManAcc Quiz 3 - FinalDocument18 pagesManAcc Quiz 3 - FinalDeepannita ChakrabortyNo ratings yet

- Example of CFS IIUM Accounting 2 ReportDocument16 pagesExample of CFS IIUM Accounting 2 ReportSyuhada Rosleen100% (1)

- Cost Accounting AssignmentDocument6 pagesCost Accounting AssignmentRamalu Dinesh ReddyNo ratings yet

- STD 957Document77 pagesSTD 957Erasmo ColonaNo ratings yet

- Tyre ManufacturingDocument57 pagesTyre ManufacturingSahal Babu60% (5)

- WG C2 II C2 Football Production II Management AccountingDocument114 pagesWG C2 II C2 Football Production II Management AccountingSalot DhyeyNo ratings yet

- Execise2 31-34Document5 pagesExecise2 31-34richel sanchezNo ratings yet

- Chapter VII RevisedDocument21 pagesChapter VII RevisedJonabelle C. BiliganNo ratings yet

- Garcia HW Problem SolvingDocument5 pagesGarcia HW Problem SolvingTristan GarciaNo ratings yet

- Estimated Cost SheetDocument3 pagesEstimated Cost SheetJasdeep Singh Deepu100% (1)

- Modul 4 Rafif F PDocument11 pagesModul 4 Rafif F PAkhdan aNo ratings yet

- CH10Document34 pagesCH10sihlemooi3No ratings yet

- Acc 4Document3 pagesAcc 4Izzah NawawiNo ratings yet

- Hassan Exame 21 AugustrDocument4 pagesHassan Exame 21 Augustrsardar hussainNo ratings yet

- Pricing of A Product:-: 1. Fit and Flare DressDocument5 pagesPricing of A Product:-: 1. Fit and Flare DressAMAN RAJNo ratings yet

- Cases On Activity Based Costing SystemDocument6 pagesCases On Activity Based Costing SystemEnusah PeterNo ratings yet

- Accounting For Managers, IIAM-VizagDocument13 pagesAccounting For Managers, IIAM-VizagDileep DeepuNo ratings yet

- Book 2Document4 pagesBook 2DANASOPHIA LEONARDONo ratings yet

- Case Study - ABC CostingDocument3 pagesCase Study - ABC CostingDaiannaNo ratings yet

- TUTORIAL Manufacturing With SolutionDocument10 pagesTUTORIAL Manufacturing With SolutionmaiNo ratings yet

- SINGH007 Ans Homework Lec 14 To 21Document47 pagesSINGH007 Ans Homework Lec 14 To 21Lau Chun GuiNo ratings yet

- Costing 2 Material - 014417Document40 pagesCosting 2 Material - 014417sirjamtech36No ratings yet

- Chapter 4-Test Material 4 1Document6 pagesChapter 4-Test Material 4 1Marcus MonocayNo ratings yet

- 05 Wilkerson Company Solution - StudentsDocument9 pages05 Wilkerson Company Solution - StudentsVinyabhooshan Bajpai PGP 2022-24 Batch100% (1)

- Fineclad Apparel - Rani Treasa - 2009209Document7 pagesFineclad Apparel - Rani Treasa - 2009209RaniNo ratings yet

- Week 4 - Seminar 3 Trimake Solution A) and B) OnlyDocument3 pagesWeek 4 - Seminar 3 Trimake Solution A) and B) Onlychina xiNo ratings yet

- Skema PSPM 17-18 Aa025Document4 pagesSkema PSPM 17-18 Aa025Dehey KNo ratings yet

- Acc 202 Exercise MyselfDocument5 pagesAcc 202 Exercise Myselfnhidiepnguyet08112004No ratings yet

- University of Finance and MarketingDocument8 pagesUniversity of Finance and MarketingQuế Phương NguyễnNo ratings yet

- Chapter 3 Job Order CostingDocument31 pagesChapter 3 Job Order CostingzamanNo ratings yet

- Acd10403 Solution Tutorial Manufacturing Account 2018Document9 pagesAcd10403 Solution Tutorial Manufacturing Account 2018Atqh ShamsuriNo ratings yet

- Cost and RevenueDocument17 pagesCost and RevenueKalpana MishraNo ratings yet

- HAslam - SolutionDocument12 pagesHAslam - SolutionSANA SAEEDNo ratings yet

- Unit CostingDocument3 pagesUnit CostingAnkit YadavNo ratings yet

- Best Financial Forecast FinalDocument13 pagesBest Financial Forecast Finalitsmethird.26No ratings yet

- Strategic ManagementDocument10 pagesStrategic Managementstk2796No ratings yet

- TUTORIAL 2 Cost ClassificationDocument7 pagesTUTORIAL 2 Cost Classificationsarahayeesha1No ratings yet

- Cost and Management Accounting 01 - Class NotesDocument114 pagesCost and Management Accounting 01 - Class NotessaurabhNo ratings yet

- Overheads Revision PDFDocument9 pagesOverheads Revision PDFSurajNo ratings yet

- Manufacturing AccountsDocument12 pagesManufacturing AccountsAdrian RamsundarNo ratings yet

- COSACC Assignment 2Document3 pagesCOSACC Assignment 2Kenneth Jim HipolitoNo ratings yet

- Maceda Glass and Aluminum Supply Job Order Cost SheetDocument8 pagesMaceda Glass and Aluminum Supply Job Order Cost SheetWarren CabunyagNo ratings yet

- Acc Sem 2Document2 pagesAcc Sem 2Muhammad SyahmiNo ratings yet

- CH 5 ExcelDocument37 pagesCH 5 ExcelssdsNo ratings yet

- Tutor 2Document13 pagesTutor 2francisaustria052623No ratings yet

- Aashutosh Agrawal - Dushyant Singh - 2020MBA027 - 2020MBA013Document8 pagesAashutosh Agrawal - Dushyant Singh - 2020MBA027 - 2020MBA013Ashita PunjabiNo ratings yet

- Session 25 & 26 - Budgeting and VarianceDocument20 pagesSession 25 & 26 - Budgeting and VarianceVinay PandeyNo ratings yet

- 12914sugg Pe2 gp2 1Document33 pages12914sugg Pe2 gp2 1harshrathore17579No ratings yet

- Answers:: Cost of Goods Manufactured Schedule For The Year EndedDocument5 pagesAnswers:: Cost of Goods Manufactured Schedule For The Year EndedAsim boidyaNo ratings yet

- Costing & Profitability: Magiclite Building SolutionsDocument16 pagesCosting & Profitability: Magiclite Building SolutionsPrince AroraNo ratings yet

- Prelim Exam-Boticario D. (SBA)Document5 pagesPrelim Exam-Boticario D. (SBA)Dominic E. BoticarioNo ratings yet

- Cost SheetDocument20 pagesCost SheetKeshviNo ratings yet

- Answers To 11 - 16 Assignment in ABC PDFDocument3 pagesAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNo ratings yet

- Ppce Unit-5Document21 pagesPpce Unit-5Jackson ..No ratings yet

- CS Uthkarsh PaiDocument9 pagesCS Uthkarsh Paiankita sahuNo ratings yet

- Wilkerson Case Study Final1Document5 pagesWilkerson Case Study Final1Swapan Kumar Saha100% (1)

- Product Cost From TraditionalDocument5 pagesProduct Cost From TraditionalPrijulNo ratings yet

- Latex Products, Inc.: A Case Review by Group 2 EMBA 16Document16 pagesLatex Products, Inc.: A Case Review by Group 2 EMBA 16Lekan AjirotutuNo ratings yet

- Cost Accounting Notes Fall 19-1Document11 pagesCost Accounting Notes Fall 19-1AnoshiaNo ratings yet

- Lecture-7 Overhead (Part 5) PDFDocument10 pagesLecture-7 Overhead (Part 5) PDFNazmul-Hassan Sumon100% (5)

- Goods and Services Tax (GST) Transition To Sales and Services Tax (SST) : Impact On The Welfare of B40 and M40 Households in MalaysiaDocument9 pagesGoods and Services Tax (GST) Transition To Sales and Services Tax (SST) : Impact On The Welfare of B40 and M40 Households in MalaysiaSugenes CrgalsNo ratings yet

- Writing Portfolio Task 2 - Introductory Paragraph (Outline)Document4 pagesWriting Portfolio Task 2 - Introductory Paragraph (Outline)Sugenes CrgalsNo ratings yet

- Cel2103 - SCL Worksheet 13Document4 pagesCel2103 - SCL Worksheet 13Sugenes CrgalsNo ratings yet

- Cel2103 - SCL Worksheet 12Document3 pagesCel2103 - SCL Worksheet 12Sugenes CrgalsNo ratings yet

- T SR ARMET SIMRIT I II Tape Silicone Rubber Freudenberg NOK Equivalent Electrical InsulationDocument1 pageT SR ARMET SIMRIT I II Tape Silicone Rubber Freudenberg NOK Equivalent Electrical InsulationFábioNo ratings yet

- AdhesiveGuide PVC UK Master2023Document2 pagesAdhesiveGuide PVC UK Master2023YasserNo ratings yet

- Section-6 Bill of Quantities For Works (BOQ)Document2 pagesSection-6 Bill of Quantities For Works (BOQ)rk36266_732077041No ratings yet

- Biotech Gloves - Certifications - OpulentDocument24 pagesBiotech Gloves - Certifications - Opulentsaisridhar99No ratings yet

- Arkema Roof Systems: Featuring Encor Flex Polymers Kynar Aquatec PVDFDocument8 pagesArkema Roof Systems: Featuring Encor Flex Polymers Kynar Aquatec PVDFJose RodríguezNo ratings yet

- 7747-14 Kumho Ca 2015 PDG - FR - Ca - R15 PDFDocument73 pages7747-14 Kumho Ca 2015 PDG - FR - Ca - R15 PDFRichard TuckerNo ratings yet

- Ravago Yakup Ülçer - PAGEV Sustainable Material SolutionsDocument34 pagesRavago Yakup Ülçer - PAGEV Sustainable Material Solutionssara rafieiNo ratings yet

- Technical Details of Bonding ChemicalsDocument18 pagesTechnical Details of Bonding ChemicalsSangeet KarnaNo ratings yet

- DTD 5509 Aircraft Material SpecificationDocument5 pagesDTD 5509 Aircraft Material SpecificationMateen AhmadNo ratings yet

- Loctite® Power Grab® Ultimate Construction Adhesive: DescriptionDocument4 pagesLoctite® Power Grab® Ultimate Construction Adhesive: DescriptionAngieNo ratings yet

- Bobcat Rubber Track BrochureDocument4 pagesBobcat Rubber Track BrochureMartin Veliz100% (1)

- Company Profiles - CHINA GROUPDocument8 pagesCompany Profiles - CHINA GROUPAhmad Mursyidi KamaludinNo ratings yet

- SD Copy of Soft - 140 - JR - Edison - BOM Blue and Coral BlushDocument2 pagesSD Copy of Soft - 140 - JR - Edison - BOM Blue and Coral BlushShibly RahmanNo ratings yet

- Design + Construction Magazine (April To June 2019)Document80 pagesDesign + Construction Magazine (April To June 2019)Dina Jane QuilangNo ratings yet

- Standards For The Aerospace IndustryDocument1 pageStandards For The Aerospace IndustryAirtech AeroNo ratings yet

- Anti Blow Out StemDocument48 pagesAnti Blow Out StemimthiyazmuhammedNo ratings yet

- RubberDocument215 pagesRubberMocerneac Bogdan100% (1)

- Steel Rules PDFDocument20 pagesSteel Rules PDFyahsooyNo ratings yet

- Brazil Anvisa RDC 37 2015 Labeling Rubber Latex enDocument1 pageBrazil Anvisa RDC 37 2015 Labeling Rubber Latex enElaine NascimentoNo ratings yet

- Belts Mishuboshi (Industrial Power Transmission Products)Document90 pagesBelts Mishuboshi (Industrial Power Transmission Products)dangdinhthyNo ratings yet

- Rubber: CPE 728-Primary Processing of Plantation and Special CropsDocument8 pagesRubber: CPE 728-Primary Processing of Plantation and Special CropsMarjun CaguayNo ratings yet

- Method Statement For Concrete Repair Works.Document9 pagesMethod Statement For Concrete Repair Works.Munaku TafadzwaNo ratings yet

- Loxeal InfotechDocument16 pagesLoxeal InfotechAlexNo ratings yet

- Tyre Industry PDFDocument134 pagesTyre Industry PDFAnmol LimpaleNo ratings yet

- Segregated Data Base. (MFG)Document936 pagesSegregated Data Base. (MFG)srinivas100% (1)

- LMI Chemical Resistance GuideDocument8 pagesLMI Chemical Resistance GuideShesharam ChouhanNo ratings yet