Download as docx, pdf, or txt

You might also like

- Path To FreedomDocument201 pagesPath To FreedomTobyPhernettonNo ratings yet

- Educational PoliciesDocument3 pagesEducational PoliciesListo Ndeshipanda ChaBoisen100% (2)

- 2017 06 14 DGS Contracting and Personnel Report by Mary ChehDocument57 pages2017 06 14 DGS Contracting and Personnel Report by Mary ChehAaron SchwartzNo ratings yet

- Banking Law Assignment - ViswanathanDocument6 pagesBanking Law Assignment - ViswanathanViswa NathanNo ratings yet

- Test Question (General Banking)Document43 pagesTest Question (General Banking)siddiqur rahmanNo ratings yet

- Chapter-4 Banker and The CustomerDocument8 pagesChapter-4 Banker and The CustomerSamuel DebebeNo ratings yet

- (Insert Your Firm's Name Here) : Guide FromDocument5 pages(Insert Your Firm's Name Here) : Guide FromHussein SeetalNo ratings yet

- Power of Attorney and Declaration of RepresentativeDocument2 pagesPower of Attorney and Declaration of Representativepreston_402003No ratings yet

- Form 1199aDocument4 pagesForm 1199aCesc SurdykNo ratings yet

- Banking Law AssignmentDocument11 pagesBanking Law AssignmentTanu Shree SinghNo ratings yet

- The General Relationship Between Bank and Its CustomerDocument9 pagesThe General Relationship Between Bank and Its CustomerAnkit AgarwalNo ratings yet

- Fms AssignmentDocument6 pagesFms AssignmentGloir StoriesNo ratings yet

- 27four Tax Free Savings New Investment FormDocument8 pages27four Tax Free Savings New Investment FormLord OversightNo ratings yet

- Bank Regulation and Deposit InsuranceDocument7 pagesBank Regulation and Deposit InsuranceZainur Nadia100% (1)

- Treasury Bills - ppt1Document10 pagesTreasury Bills - ppt1Deepak BajpaiNo ratings yet

- Payment SystemsDocument14 pagesPayment SystemsdestinysandeepNo ratings yet

- Debtor - Creditor AgreementDocument19 pagesDebtor - Creditor AgreementGeorgeNo ratings yet

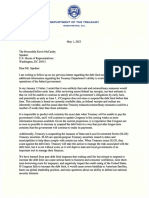

- Sec. Yellen Letter To Speaker McCarthyDocument2 pagesSec. Yellen Letter To Speaker McCarthyDaily Caller News FoundationNo ratings yet

- Mail - RE - Claim Status - YFAE950884YF PDFDocument3 pagesMail - RE - Claim Status - YFAE950884YF PDFSankalp Suman ChandelNo ratings yet

- Discharge of Contract, Breach and RemediesDocument21 pagesDischarge of Contract, Breach and RemediesWajid AliNo ratings yet

- Different Modes of Charging Securities: HypothecationDocument4 pagesDifferent Modes of Charging Securities: Hypothecationdinesh khatriNo ratings yet

- Banking Law B.com - Docx LatestDocument38 pagesBanking Law B.com - Docx LatestViraja GuruNo ratings yet

- I1099 Int - and - Oid 2022 01 00Document64 pagesI1099 Int - and - Oid 2022 01 00Alex LagunesNo ratings yet

- Non Life Insurance Companies & Life Insurance CompaniesDocument38 pagesNon Life Insurance Companies & Life Insurance CompaniesSyedFaisalHasanShahNo ratings yet

- Money and BankingDocument11 pagesMoney and BankingSyed Salman AbbasNo ratings yet

- Areas Covered in FPRDocument4 pagesAreas Covered in FPRNikunj BhatnagarNo ratings yet

- Negotiable InstrumentsDocument18 pagesNegotiable InstrumentsBrahmanand ShetNo ratings yet

- Notes On Negotiable Instrument Act 1881Document6 pagesNotes On Negotiable Instrument Act 1881Pranjal SrivastavaNo ratings yet

- Company Law FoundationDocument17 pagesCompany Law FoundationVanshika chalwaNo ratings yet

- Meaning of Banker and Customer Meaning of Banker and CustomerDocument14 pagesMeaning of Banker and Customer Meaning of Banker and CustomerSaiful IslamNo ratings yet

- Loan AppDocument1 pageLoan Appapi-289462742No ratings yet

- Bills Discounting: Dr. Sarbesh Mishra, Finance AreaDocument9 pagesBills Discounting: Dr. Sarbesh Mishra, Finance AreaDr Sarbesh MishraNo ratings yet

- Negotiable Instruments LawDocument9 pagesNegotiable Instruments LawjannahNo ratings yet

- Weintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Document12 pagesWeintraub v. QUICKEN LOANS, INC, 594 F.3d 270, 4th Cir. (2010)Scribd Government DocsNo ratings yet

- Unsecured PNDocument4 pagesUnsecured PNDoctrine ChurchNo ratings yet

- Legal Notice of Removal: From Municipal Court To Federal Court Pursuant To Title 28 Proper Article Iii JurisdictionDocument25 pagesLegal Notice of Removal: From Municipal Court To Federal Court Pursuant To Title 28 Proper Article Iii JurisdictionElNo ratings yet

- How To Open Letter of CreditDocument2 pagesHow To Open Letter of Credit✬ SHANZA MALIK ✬No ratings yet

- IMF Special Drawing RightsDocument3 pagesIMF Special Drawing RightsJialu Liu100% (1)

- Law of Banking and Negotiabl InsrumentsDocument23 pagesLaw of Banking and Negotiabl Insrumentsfocus moreNo ratings yet

- Government NotesDocument31 pagesGovernment Notesapi-257176789No ratings yet

- Quitclaim DeedDocument4 pagesQuitclaim Deedjusmathoughts2No ratings yet

- BY: 37 MBA 09 43 MBA 09: Venika Saini Anuj GuptaDocument31 pagesBY: 37 MBA 09 43 MBA 09: Venika Saini Anuj GuptaaditibakshiNo ratings yet

- Glossary Investment TermsDocument15 pagesGlossary Investment TermsBehroozRaadNo ratings yet

- A Group Presentation of Business Law OnDocument43 pagesA Group Presentation of Business Law OnvakhariajimmyNo ratings yet

- Account Closure Request Form (MCX)Document1 pageAccount Closure Request Form (MCX)Deepak ThakurNo ratings yet

- Corp BankingDocument132 pagesCorp BankingPravah ShuklaNo ratings yet

- RBC Mortgage Discharge - LienDocument14 pagesRBC Mortgage Discharge - Liencondomadness13No ratings yet

- Request For Taxpayer Identification Number and CertificationDocument4 pagesRequest For Taxpayer Identification Number and Certificationapi-259574251No ratings yet

- 8 Get Your Finances & Credit in OrderDocument15 pages8 Get Your Finances & Credit in OrdercropdownunderNo ratings yet

- Necessity To Determine Relationship Between Banker and CustomerDocument3 pagesNecessity To Determine Relationship Between Banker and CustomerKrishna PratapNo ratings yet

- All The Things The IRS Can Take Even Retirement Accounts!Document5 pagesAll The Things The IRS Can Take Even Retirement Accounts!NoelNo ratings yet

- General Overview of Tender OfferDocument1 pageGeneral Overview of Tender OfferSafitri KusumawardhaniNo ratings yet

- Relationship Between Banker and CustomerDocument10 pagesRelationship Between Banker and Customerswagat098No ratings yet

- Discount Window: Rate, or Rate, and Is Separate and Distinct From TheDocument4 pagesDiscount Window: Rate, or Rate, and Is Separate and Distinct From TheDisgruntled Borrower100% (1)

- Zero Coupon BondsDocument26 pagesZero Coupon BondsPrashant SinghNo ratings yet

- Chapter 4 - Co-Ownership, Estates and TrustsDocument8 pagesChapter 4 - Co-Ownership, Estates and TrustsLiRose SmithNo ratings yet

- Scrutiny of Export DocumentsDocument5 pagesScrutiny of Export DocumentsAmanNo ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Constitution of the State of Minnesota — 1974 VersionFrom EverandConstitution of the State of Minnesota — 1974 VersionNo ratings yet

- Globe Mackay v. CA 176 SCRA 778 (August 25, 1989) Facts: Restituto M. Tobias, The Private Respondent, WasDocument41 pagesGlobe Mackay v. CA 176 SCRA 778 (August 25, 1989) Facts: Restituto M. Tobias, The Private Respondent, WasGina Portuguese GawonNo ratings yet

- Landicho Vs RelovaDocument6 pagesLandicho Vs Relovakikhay11No ratings yet

- TMP - Hotel - Agreement - 1000519211 - Domestic Hotels Agreement - 230424-08 - 31 - 22 PDFDocument5 pagesTMP - Hotel - Agreement - 1000519211 - Domestic Hotels Agreement - 230424-08 - 31 - 22 PDFvishalp9415No ratings yet

- Winding Up of CompaniesDocument5 pagesWinding Up of CompaniesDickson Tk Chuma Jr.No ratings yet

- Petitioners: en BancDocument10 pagesPetitioners: en BancMark Christian TagapiaNo ratings yet

- Statement of Jurisdiction.: 10 M. K. Nambyar Memorial National Level Moot Court CompetitionDocument19 pagesStatement of Jurisdiction.: 10 M. K. Nambyar Memorial National Level Moot Court CompetitionAnu RautNo ratings yet

- MUNICIPAL ORDINANCE NO. 26-2020 Frontliners Protection Ordinance of The Municipality of Carmen, Agusan Del NorteDocument4 pagesMUNICIPAL ORDINANCE NO. 26-2020 Frontliners Protection Ordinance of The Municipality of Carmen, Agusan Del NorteJason LapeNo ratings yet

- Voluntary Petition For Non-Individuals Filing For BankruptcyDocument89 pagesVoluntary Petition For Non-Individuals Filing For BankruptcyAnonymous lTRXIIVnyNo ratings yet

- Industrial Refractories Vs CaDocument5 pagesIndustrial Refractories Vs CaPhrexilyn PajarilloNo ratings yet

- Castro Vs CADocument3 pagesCastro Vs CAnatnat02No ratings yet

- Meaning and Scope of GovernanceDocument13 pagesMeaning and Scope of GovernanceDen Marc BalubalNo ratings yet

- Naguiat v. NLRCDocument1 pageNaguiat v. NLRCNico NuñezNo ratings yet

- Legal Form Activity No. 4-A - Contract of SaleDocument5 pagesLegal Form Activity No. 4-A - Contract of SaleAJ FHNo ratings yet

- F002 Admin. PRCDocument24 pagesF002 Admin. PRCLeolaida AragonNo ratings yet

- Elecon Debenture Trust DeedDocument102 pagesElecon Debenture Trust DeedVijay Kajave VkNo ratings yet

- Lecture Notes 4Document33 pagesLecture Notes 4ian_ling_2No ratings yet

- Guidelines For TEV Consultant PDFDocument6 pagesGuidelines For TEV Consultant PDFSatyanarayana Moorthy PiratlaNo ratings yet

- Subpoena From Lawyers For Former South Burlington Police Cpl. Jack O'ConnorDocument3 pagesSubpoena From Lawyers For Former South Burlington Police Cpl. Jack O'ConnorBurlington FreePressNo ratings yet

- Power of The High Courts To Transfer CasesDocument2 pagesPower of The High Courts To Transfer CasesShweta ChauhanNo ratings yet

- Bavisetti Venkata Surya Rao Vs Nandipati Muthayya On 14 June 1963Document10 pagesBavisetti Venkata Surya Rao Vs Nandipati Muthayya On 14 June 1963PrathamNo ratings yet

- BFP Cert of OccupancyDocument2 pagesBFP Cert of OccupancyBayani ParagasNo ratings yet

- BBUN2103Document14 pagesBBUN2103mawarnimasNo ratings yet

- NCG Consent Form and Approval Form TemplateDocument1 pageNCG Consent Form and Approval Form Templateapi-659173473No ratings yet

- TerrorismDocument14 pagesTerrorismsaurav249No ratings yet

- G.R. No. 162784 Nha V AlmeidaDocument2 pagesG.R. No. 162784 Nha V AlmeidaRogie ToriagaNo ratings yet

- Right Issue Resolution of Board MeetingDocument2 pagesRight Issue Resolution of Board MeetingSavoir PenNo ratings yet

- Re-Marking Policy and Process (Effective 25 November 2016)Document2 pagesRe-Marking Policy and Process (Effective 25 November 2016)Nimraj PatelNo ratings yet

- Torts Midterm Exam ReviewerDocument16 pagesTorts Midterm Exam ReviewerMary Ann LeuterioNo ratings yet