Download as xlsx, pdf, or txt

You might also like

- Special Transactions (2019) by Millan Solman PDFDocument157 pagesSpecial Transactions (2019) by Millan Solman PDFMichael Angelou Raymundo90% (20)

- CH 3 SolutionsDocument37 pagesCH 3 SolutionsRavneet BalNo ratings yet

- Management Science ActivityDocument7 pagesManagement Science ActivityVixen Aaron Enriquez100% (1)

- Advacc 1 Millan 2019 Advac 1 Special Transactions 2019Document11 pagesAdvacc 1 Millan 2019 Advac 1 Special Transactions 2019Charlene BolandresNo ratings yet

- ASSIGNMENTSDocument13 pagesASSIGNMENTSJpzelleNo ratings yet

- PROBLEM 15-1 FinancialDocument14 pagesPROBLEM 15-1 FinancialKezha Calderon100% (1)

- Razor Company Required Debit Credit 2020Document14 pagesRazor Company Required Debit Credit 2020AnonnNo ratings yet

- Chapter 34Document8 pagesChapter 34Shane Ivory ClaudioNo ratings yet

- Intangible Assets Practical AccountingDocument4 pagesIntangible Assets Practical AccountingAshley Nicole HerediaNo ratings yet

- Intangibles Assignment - Valix 2017Document3 pagesIntangibles Assignment - Valix 2017Shinny Jewel VingnoNo ratings yet

- Multiple Choice ProblemsDocument17 pagesMultiple Choice ProblemsDieter LudwigNo ratings yet

- Balance Sheet QUESTIONANSWERDocument19 pagesBalance Sheet QUESTIONANSWERJoyce Ann Agdippa BarcelonaNo ratings yet

- SFP and SCF - Practice QuestionsDocument3 pagesSFP and SCF - Practice QuestionsFazelah YakubNo ratings yet

- Suggested-Solution-2 AUDPROBDocument3 pagesSuggested-Solution-2 AUDPROBRey Josh RicamaraNo ratings yet

- IA Activity 6 AssDocument6 pagesIA Activity 6 AssWeStan LegendsNo ratings yet

- Chapter 33Document7 pagesChapter 33Shane Ivory ClaudioNo ratings yet

- ACCT 410 Candel Financial StatementDocument14 pagesACCT 410 Candel Financial StatementAthia Adams-KerrNo ratings yet

- Problem 1: CA RA: Impairment OccurredDocument11 pagesProblem 1: CA RA: Impairment OccurredFiles OrganizedNo ratings yet

- Asawa Ko Aking Mahal Book Value Fair Value Book Value Fair ValueDocument22 pagesAsawa Ko Aking Mahal Book Value Fair Value Book Value Fair ValueLyka RoguelNo ratings yet

- Pembahasan Genap ACT Genap 2020 19 MarDocument12 pagesPembahasan Genap ACT Genap 2020 19 MarSoca NarendraNo ratings yet

- Example Problems W Solutions in SFP & SCFDocument7 pagesExample Problems W Solutions in SFP & SCFQueen Valle100% (1)

- Buscom-Asset AcquisitionDocument7 pagesBuscom-Asset AcquisitionRenelyn DavidNo ratings yet

- Bus. Combi Probs and SolnDocument3 pagesBus. Combi Probs and SolnRyan Prado AndayaNo ratings yet

- Gov't Grant, Depreciation, Revaluation and ImpairmentDocument6 pagesGov't Grant, Depreciation, Revaluation and Impairment夜晨曦No ratings yet

- Acctg. For INTANGIBLE ASSETSDocument5 pagesAcctg. For INTANGIBLE ASSETSKristine PerezNo ratings yet

- Let's Check (ULO J)Document8 pagesLet's Check (ULO J)Kirei MinaNo ratings yet

- AA 4101 Midterm With AnswersDocument9 pagesAA 4101 Midterm With AnswersAlyssa AnnNo ratings yet

- Minglana-Mitch-T-Answers in Long QuizDocument9 pagesMinglana-Mitch-T-Answers in Long QuizMitch MinglanaNo ratings yet

- ENG - Jawaban Mojakoe Akuntansi Keuangan 1 UAS Genap 2021 - 2022Document8 pagesENG - Jawaban Mojakoe Akuntansi Keuangan 1 UAS Genap 2021 - 2022Reta AzkaNo ratings yet

- Presentation of Properly Classified FSDocument9 pagesPresentation of Properly Classified FSpapa1No ratings yet

- Chapter 1-SolutionsDocument14 pagesChapter 1-SolutionsPrince CalicaNo ratings yet

- Liabilities 31.03.20X1 Rs. 31.03.20X 2 Rs. Assets 31.03.20X 1 Rs. 31.03.20X2 RsDocument3 pagesLiabilities 31.03.20X1 Rs. 31.03.20X 2 Rs. Assets 31.03.20X 1 Rs. 31.03.20X2 RsAmit GodaraNo ratings yet

- Case Study 2023 Set 2Document12 pagesCase Study 2023 Set 2Bosz icon DyliteNo ratings yet

- Accounting For Business Combi SolutionDocument4 pagesAccounting For Business Combi SolutionSophia Anne Margarette NicolasNo ratings yet

- Answer Vidal Jeams E. Long Quiz ApDocument9 pagesAnswer Vidal Jeams E. Long Quiz ApMitch MinglanaNo ratings yet

- Zartiga PrEDocument4 pagesZartiga PrEFritzie Ann ZartigaNo ratings yet

- Kertas Kerja Referensi Akun Debit Credit 3. NERACA SALDO Sebelum PenyesuaianDocument9 pagesKertas Kerja Referensi Akun Debit Credit 3. NERACA SALDO Sebelum Penyesuaianadmin finishyourtaskNo ratings yet

- AFAR1 Chap 1Document7 pagesAFAR1 Chap 1CilNo ratings yet

- S3 BAFS First Term Exam Marking SchemeDocument6 pagesS3 BAFS First Term Exam Marking Schemeharis RehmanNo ratings yet

- Latihan - Aset Tidak Berwujud-JAWABDocument7 pagesLatihan - Aset Tidak Berwujud-JAWABAndreas HottoNo ratings yet

- CH 5Document2 pagesCH 5tigger5191No ratings yet

- Suggested Solutions June 2008Document11 pagesSuggested Solutions June 2008kalowekamoNo ratings yet

- Jawaban Soal UTS Akuntansi Keu - MenengahDocument4 pagesJawaban Soal UTS Akuntansi Keu - MenengahJessinthaNo ratings yet

- Accountancy & Auditing-IDocument4 pagesAccountancy & Auditing-Izaman virkNo ratings yet

- Dhis Special Transactions 2019 by Millan Solman PDFDocument158 pagesDhis Special Transactions 2019 by Millan Solman PDFQueeny Mae Cantre ReutaNo ratings yet

- Suggested Answer CAP III June 2018 PDFDocument155 pagesSuggested Answer CAP III June 2018 PDFRajani Shrestha0% (1)

- Answer Key Q2 PDFDocument6 pagesAnswer Key Q2 PDFNonami AbicoNo ratings yet

- 2019 Vol 2 CH 4 AnswersDocument8 pages2019 Vol 2 CH 4 AnswersElla LopezNo ratings yet

- To Record 600 Shares@ 100 Ordinary Share at 80Document9 pagesTo Record 600 Shares@ 100 Ordinary Share at 80Johanna Raissa CapadaNo ratings yet

- Practice Set 1Document6 pagesPractice Set 1moreNo ratings yet

- Pengakun CH 09Document10 pagesPengakun CH 09nadia salsabilaNo ratings yet

- Accy 101Document5 pagesAccy 101Eunice Ciara Eluna FulgencioNo ratings yet

- Illustrative Example - Cash Flow StatementDocument6 pagesIllustrative Example - Cash Flow StatementNausheenNo ratings yet

- 201.AFA IP.L II December 2020Document4 pages201.AFA IP.L II December 2020leyaketjnuNo ratings yet

- Fin Acc 2 Chap 14Document9 pagesFin Acc 2 Chap 14MkaeDizonNo ratings yet

- Final Account WorksheetDocument4 pagesFinal Account Worksheetravikumarbadass0No ratings yet

- Class Example - Statement of Financial PositionDocument1 pageClass Example - Statement of Financial PositionTia WhoserNo ratings yet

- Accounting For Special Transactions 2019 Ed. MIllan Solution ManualDocument157 pagesAccounting For Special Transactions 2019 Ed. MIllan Solution ManualRaven PicorroNo ratings yet

- How to Find Out About Patents: The Commonwealth and International Library: Libraries and Technical Information DivisionFrom EverandHow to Find Out About Patents: The Commonwealth and International Library: Libraries and Technical Information DivisionNo ratings yet

- Chap 1 & 2Document11 pagesChap 1 & 2Vixen Aaron EnriquezNo ratings yet

- SSS Formula Try LangDocument7 pagesSSS Formula Try LangVixen Aaron EnriquezNo ratings yet

- E MailDocument2 pagesE MailVixen Aaron EnriquezNo ratings yet

- Activity 5Document2 pagesActivity 5Vixen Aaron EnriquezNo ratings yet

- Photo Essay - PILS IssueDocument4 pagesPhoto Essay - PILS IssueVixen Aaron EnriquezNo ratings yet

- Rizal OutputDocument2 pagesRizal OutputVixen Aaron EnriquezNo ratings yet

- CS Manuscript Final Updated Ready For CheckingDocument50 pagesCS Manuscript Final Updated Ready For CheckingVixen Aaron EnriquezNo ratings yet

- Erikson's Psychosocial Theory AssignmentDocument3 pagesErikson's Psychosocial Theory AssignmentVixen Aaron EnriquezNo ratings yet

- Synthesizing ReflectionDocument5 pagesSynthesizing ReflectionVixen Aaron EnriquezNo ratings yet

- Critique PaperDocument4 pagesCritique PaperVixen Aaron EnriquezNo ratings yet

- Activity On The Pursuit of NationhoodDocument2 pagesActivity On The Pursuit of NationhoodVixen Aaron EnriquezNo ratings yet

- Cost Management Output (CA 2)Document4 pagesCost Management Output (CA 2)Vixen Aaron EnriquezNo ratings yet

- Enriquez, Vixen Aaron M. - Assignment On Audit of LiabilitiesDocument8 pagesEnriquez, Vixen Aaron M. - Assignment On Audit of LiabilitiesVixen Aaron EnriquezNo ratings yet

- "Shallow Men Believe in Luck. Strong Men Believe in Cause and Effect." - Ralph Waldo EmersonDocument6 pages"Shallow Men Believe in Luck. Strong Men Believe in Cause and Effect." - Ralph Waldo EmersonVixen Aaron Enriquez100% (1)

- "The Moment We Decide To Fulfill Something, We Can Do Anything." - Greta ThunbergDocument4 pages"The Moment We Decide To Fulfill Something, We Can Do Anything." - Greta ThunbergVixen Aaron EnriquezNo ratings yet

- Quiz 4Document4 pagesQuiz 4Vixen Aaron EnriquezNo ratings yet

- Enriquez, Vixen Aaron M. - Assignment On Market-Based ValuationDocument3 pagesEnriquez, Vixen Aaron M. - Assignment On Market-Based ValuationVixen Aaron EnriquezNo ratings yet

- VATDocument3 pagesVATVixen Aaron EnriquezNo ratings yet

- Exercises On Joint Cost and By-ProductsDocument2 pagesExercises On Joint Cost and By-ProductsVixen Aaron EnriquezNo ratings yet

- Telemedicine Narrative ReportDocument4 pagesTelemedicine Narrative ReportVixen Aaron EnriquezNo ratings yet

- Enriquez, Vixen Aaron M. - Assignment On Audit of InvestmentsDocument2 pagesEnriquez, Vixen Aaron M. - Assignment On Audit of InvestmentsVixen Aaron EnriquezNo ratings yet

- Quiz 1 On Applied AuditingDocument4 pagesQuiz 1 On Applied AuditingVixen Aaron EnriquezNo ratings yet

- The Effects of Media: ViolenceDocument8 pagesThe Effects of Media: ViolenceVixen Aaron EnriquezNo ratings yet

- Negative Feedback Mechanism: Diagram Explanation Diagram ExplanationDocument2 pagesNegative Feedback Mechanism: Diagram Explanation Diagram ExplanationVixen Aaron EnriquezNo ratings yet

- Revised CVPDocument2 pagesRevised CVPVixen Aaron EnriquezNo ratings yet

- FIR - Filed by Sunil AlaghDocument3 pagesFIR - Filed by Sunil Alaghlaw1leoNo ratings yet

- Sukanya Samriddhi Yojana PDFDocument1 pageSukanya Samriddhi Yojana PDFSai SrinivasNo ratings yet

- 507419143 (1)Document2 pages507419143 (1)Gunjan Solanki0% (1)

- FMC UnitedDocument2 pagesFMC UnitedGhulam Murtaza0% (1)

- Case 3 Kota FibresDocument2 pagesCase 3 Kota Fibresmargery_bumagatNo ratings yet

- Motion To Reduce Bail Bond Cambri 4591-92Document2 pagesMotion To Reduce Bail Bond Cambri 4591-92Jholo AlvaradoNo ratings yet

- Company Rescue Under UK Administration and US Chapter 11Document4 pagesCompany Rescue Under UK Administration and US Chapter 11vidovdan9852No ratings yet

- ch19 Accounting Income TaxesDocument102 pagesch19 Accounting Income TaxesIndah SariwatiNo ratings yet

- 01 Alvarez Vs GuingonaDocument2 pages01 Alvarez Vs GuingonaSamantha Ann T. TirthdasNo ratings yet

- TimelineDocument478 pagesTimelineAnonymous wDuVFh0KcxNo ratings yet

- City of BaltimoreDocument4 pagesCity of BaltimoreAnonymous Feglbx5No ratings yet

- Project Reports On Comparative Analysis of Housing Loan Schemes of HDFC LTD - 153135237Document79 pagesProject Reports On Comparative Analysis of Housing Loan Schemes of HDFC LTD - 153135237ishant bhatNo ratings yet

- Mankiw Chapter 12 Mundell Fleming Model Is LM and ErDocument40 pagesMankiw Chapter 12 Mundell Fleming Model Is LM and Erbasirunjie86No ratings yet

- Module - 3 PDFDocument7 pagesModule - 3 PDFKeyur PopatNo ratings yet

- Law 11Document6 pagesLaw 11ram RedNo ratings yet

- Chapter-01: Page - 1Document50 pagesChapter-01: Page - 1Md Khaled NoorNo ratings yet

- Accounting Assignment Chapter 13 Answers - 5Document3 pagesAccounting Assignment Chapter 13 Answers - 5alexie aurelioNo ratings yet

- FS PT Acset 31 Maret 2023Document79 pagesFS PT Acset 31 Maret 2023Nanda WulanNo ratings yet

- Math in Finance MITDocument22 pagesMath in Finance MITkkappaNo ratings yet

- Fitch Monthly July 2014Document1 pageFitch Monthly July 2014jaycamerNo ratings yet

- Competitive Federalism PDFDocument1 pageCompetitive Federalism PDFవన మాలిNo ratings yet

- Week 4 PDFDocument23 pagesWeek 4 PDFKHAKSARNo ratings yet

- Coronavirus and Its Effects On: Pakistan'S EconomyDocument21 pagesCoronavirus and Its Effects On: Pakistan'S EconomymuhammadvaqasNo ratings yet

- Or Other Disposition of All or Substantially All of The Corporate Property and Assets As Provided in The Code andDocument3 pagesOr Other Disposition of All or Substantially All of The Corporate Property and Assets As Provided in The Code andRafael JuicoNo ratings yet

- Brandywine Health Foundation 2014 Community ReportDocument14 pagesBrandywine Health Foundation 2014 Community ReportKen KnickerbockerNo ratings yet

- Funda Manual Chapter 5 ExercisesDocument8 pagesFunda Manual Chapter 5 ExercisesRimuruNo ratings yet

- Chapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Document37 pagesChapter 10 Transactions and Their Analysis As Applied To The Accounting Cycle of A Service Business 1Ian SumastreNo ratings yet

- Guidelines For Extending Equity Support To Housing Finance CompaniesDocument3 pagesGuidelines For Extending Equity Support To Housing Finance CompaniessrirammaliNo ratings yet

- SSC CGL 2015 Capsule PDFDocument153 pagesSSC CGL 2015 Capsule PDFAathi LinNo ratings yet

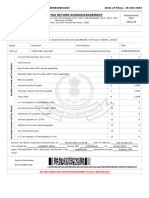

- Hardeep Singh ITR 2023Document1 pageHardeep Singh ITR 2023parwindersingh9066No ratings yet