Download as pdf or txt

You might also like

- Solved For A Given Soil, The Following Are Known Gs 2.74, M...Document1 pageSolved For A Given Soil, The Following Are Known Gs 2.74, M...Cristian A. GarridoNo ratings yet

- Questionnaire ObjectiveDocument9 pagesQuestionnaire Objectiveprasadzinjurde100% (3)

- Curriculum Vitae - Santiago Mark Andrew M Latest As of April 2019Document4 pagesCurriculum Vitae - Santiago Mark Andrew M Latest As of April 2019Drew SantiagoNo ratings yet

- Income Tax MCQ PDFDocument26 pagesIncome Tax MCQ PDFArpita DagliaNo ratings yet

- Mcq's Tax ScannerDocument533 pagesMcq's Tax ScannerSajal DixitNo ratings yet

- Direct Tax MCQDocument320 pagesDirect Tax MCQRam Iyer100% (1)

- Income Tax MCQDocument15 pagesIncome Tax MCQSoni Mishra TiwariNo ratings yet

- Itlp Question BankDocument4 pagesItlp Question BankHimanshu SethiNo ratings yet

- Basics (DT) Revision P Ques Jan 23Document10 pagesBasics (DT) Revision P Ques Jan 23Grave diggerNo ratings yet

- Payment of Bonus ActDocument13 pagesPayment of Bonus Act61Mansi Saraykar100% (3)

- DT NewDocument23 pagesDT NewSanket MhetreNo ratings yet

- Time Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDocument18 pagesTime Allowed: 3 Hours Maximum Mark: 100: Executive ProgrammeDevendra AryaNo ratings yet

- 5 6073471622155600005 PDFDocument235 pages5 6073471622155600005 PDFRajni GouranaNo ratings yet

- MCQ - B.com Semester V - Core Course - Bcm5b09 Income Tax Law and AccountsDocument21 pagesMCQ - B.com Semester V - Core Course - Bcm5b09 Income Tax Law and AccountsAfreen FatimaNo ratings yet

- Paper I ITI Income Tax Law and Computation - 13072009Document15 pagesPaper I ITI Income Tax Law and Computation - 13072009CHANDAN DUTTANo ratings yet

- Test Series: October, 2019 Mock Test Paper 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionDocument12 pagesTest Series: October, 2019 Mock Test Paper 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws and International TaxaxtionANIL JARWALNo ratings yet

- 2nd TAX LAWS MOCK Test TWO JUNE 2018 Students With SolutionDocument15 pages2nd TAX LAWS MOCK Test TWO JUNE 2018 Students With SolutionJasmeet KaurNo ratings yet

- 1602240673847-QB Labour LawsDocument20 pages1602240673847-QB Labour LawsLata Yadav maindadNo ratings yet

- MCQ On Bonus Act 1965Document13 pagesMCQ On Bonus Act 1965MPP CELLNo ratings yet

- MCQ'S Practies: Direct TaxDocument12 pagesMCQ'S Practies: Direct TaxTina AggarwalNo ratings yet

- Mohit Agarwal QP Tax LawsDocument17 pagesMohit Agarwal QP Tax LawsManisha DasNo ratings yet

- (April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Document3 pages(April-19) (MBC-106) Ii Semester Income Tax Law and Practice Time: 3 Hours Max - Marks: 60Bhuvaneswari karuturiNo ratings yet

- Chapter 3 MCQs On Disallowance of PGBPDocument11 pagesChapter 3 MCQs On Disallowance of PGBPDevesh NagilaNo ratings yet

- Law Question Paper Cat Dec 29Document10 pagesLaw Question Paper Cat Dec 29shibin cpNo ratings yet

- MCQ Direct TaxDocument53 pagesMCQ Direct TaxSwetha MalladiNo ratings yet

- MCQ OF CHAPTER 18 To CHAPTER 21Document7 pagesMCQ OF CHAPTER 18 To CHAPTER 21Aman AgarwalNo ratings yet

- INCOME TAX Business & Profession MCQ - TY B COMDocument5 pagesINCOME TAX Business & Profession MCQ - TY B COMMani Kumar Sarvepalli100% (1)

- MCQ BasicsDocument11 pagesMCQ BasicsBharat ThackerNo ratings yet

- Basic Concepts and Residential StatusDocument42 pagesBasic Concepts and Residential Statusdeepak.agarwal.caNo ratings yet

- Income Tax - IntroductionDocument2 pagesIncome Tax - Introductiondubeyshibu743No ratings yet

- 30 Income Tax Objective Type QuestionsDocument25 pages30 Income Tax Objective Type QuestionsRakesh Sharma50% (6)

- 5 - Principles of Taxation07092021Document10 pages5 - Principles of Taxation07092021Jahirul IslamNo ratings yet

- Ca - 17ucc515 Income Tax Law and PracticeDocument34 pagesCa - 17ucc515 Income Tax Law and PracticeNALLASWAMY VPNo ratings yet

- Direct Tax Laws Detail Test 1 May 2024 Test Paper 1702105507Document9 pagesDirect Tax Laws Detail Test 1 May 2024 Test Paper 1702105507shauryagupta20013007No ratings yet

- IosDocument13 pagesIoskhanpattanNo ratings yet

- Objective Questions in Income TaxDocument43 pagesObjective Questions in Income TaxharithraaNo ratings yet

- CA Final Multiple Choice Questions Business & ProfessionDocument14 pagesCA Final Multiple Choice Questions Business & ProfessionRahul SahNo ratings yet

- Income Tax MCQ Question Bank May 2023 (130 Pages)Document130 pagesIncome Tax MCQ Question Bank May 2023 (130 Pages)PRITESH JAIN100% (2)

- Labour Law MCQDocument11 pagesLabour Law MCQShubham RajNo ratings yet

- 25-7-21 611 nf-8175 GST QueDocument4 pages25-7-21 611 nf-8175 GST QueJignesh NagarNo ratings yet

- M.K. Gupta Ca Education Income Tax: Multiple Choice QuestionsDocument5 pagesM.K. Gupta Ca Education Income Tax: Multiple Choice QuestionsSarthak AhujaNo ratings yet

- Income Tax MCQ PDFDocument26 pagesIncome Tax MCQ PDFSachin PanchalNo ratings yet

- MTP 7Document17 pagesMTP 7Deepsikha maitiNo ratings yet

- Income Tax NoteDocument53 pagesIncome Tax NoteAbdi RaxmanNo ratings yet

- DT - Test 2 - D23 - NSDocument3 pagesDT - Test 2 - D23 - NSMadhav TailorNo ratings yet

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument25 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarNo ratings yet

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument25 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxSonu KumarNo ratings yet

- Paper 16Document5 pagesPaper 16VijayaNo ratings yet

- Chapter 14 - Return - NOV - 19 - 1565841689429Document4 pagesChapter 14 - Return - NOV - 19 - 1565841689429Manoj BothraNo ratings yet

- Mega Test PDFDocument73 pagesMega Test PDFFalak HanifNo ratings yet

- Book 62 4A Income Tax MCQ's Material 40e 3Document33 pagesBook 62 4A Income Tax MCQ's Material 40e 3Roshinisai VuppalaNo ratings yet

- Labour-Laws-Ii Solved MCQs (Set-3)Document9 pagesLabour-Laws-Ii Solved MCQs (Set-3)Kamiya Modi100% (1)

- Chapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxDocument28 pagesChapter 1 MCQs On Income Tax Rates and Basic Concept of Income TaxMeenal Luther100% (1)

- Tax Theory Sem-4Document5 pagesTax Theory Sem-4devangshidas2000No ratings yet

- II Mcom - CTLP - Mcq's - II MidDocument7 pagesII Mcom - CTLP - Mcq's - II MidChakravarti ChakriNo ratings yet

- Payment of Tax @icmaifamilyDocument9 pagesPayment of Tax @icmaifamilypriyababu4701No ratings yet

- MCQ OF CHAPTER 12 A & B - Payment of TaxDocument11 pagesMCQ OF CHAPTER 12 A & B - Payment of TaxAman AgarwalNo ratings yet

- PGDTL Paper2 QB1Document17 pagesPGDTL Paper2 QB1SoniJhaNo ratings yet

- MCQ OF CHAPTER 14 To CHAPTER 17Document8 pagesMCQ OF CHAPTER 14 To CHAPTER 17Aman AgarwalNo ratings yet

- ALL MCQS Income TaxDocument33 pagesALL MCQS Income TaxLokesh SinghNo ratings yet

- Chapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxDocument27 pagesChapter 1 Mcqs On Income Tax Rates and Basic Concept of Income TaxSatheesh KannaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Audit Mcqs 150 MergedDocument188 pagesAudit Mcqs 150 MergedKadam KartikeshNo ratings yet

- G. E. Society'S H. P. T. Arts and R. Y. K. Science College, Nasik. T.Y.B.Sc. (Mathematics) Semester Iv MT 341: Complex Analysis Question Bank Multiple Choice QuestionsDocument6 pagesG. E. Society'S H. P. T. Arts and R. Y. K. Science College, Nasik. T.Y.B.Sc. (Mathematics) Semester Iv MT 341: Complex Analysis Question Bank Multiple Choice QuestionsKadam KartikeshNo ratings yet

- Audit Mcqs 150 MergedDocument188 pagesAudit Mcqs 150 MergedKadam KartikeshNo ratings yet

- 49 Ty Costing Iii Chap4 MCQDocument13 pages49 Ty Costing Iii Chap4 MCQKadam KartikeshNo ratings yet

- T.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Document13 pagesT.Y. B. Com Auditing (MCQ'S) by Asst. Prof. Pravin Kad (M. Com., SET, NET) 8788167249 (Kadam KartikeshNo ratings yet

- By Prof. Pankaj Jagtap (Mcom, Net, Set, Gdc&A, DTL) S. M. Joshi College Hadapsar Pune 28Document12 pagesBy Prof. Pankaj Jagtap (Mcom, Net, Set, Gdc&A, DTL) S. M. Joshi College Hadapsar Pune 28Kadam KartikeshNo ratings yet

- 48 Ty Chap3 MCQDocument18 pages48 Ty Chap3 MCQKadam Kartikesh67% (3)

- Bank Final AccountDocument11 pagesBank Final AccountKadam KartikeshNo ratings yet

- Insurance Claim AccountDocument12 pagesInsurance Claim AccountKadam Kartikesh67% (3)

- Term - I MCQ Base QuestionDocument41 pagesTerm - I MCQ Base QuestionKadam Kartikesh100% (3)

- Due Diligence Procedures in Land Transactions in Kenya - Five Steps. - Begi's LawDocument12 pagesDue Diligence Procedures in Land Transactions in Kenya - Five Steps. - Begi's LawMartha MuthokaNo ratings yet

- Reference List Sample For ResumeDocument7 pagesReference List Sample For Resumec2yyr2c3100% (1)

- ASUFRIN, JR., v. SAN MIGUEL CORPORATIONDocument2 pagesASUFRIN, JR., v. SAN MIGUEL CORPORATIONMonica FerilNo ratings yet

- (Nov 2020) Latest Safecustody ListingDocument923 pages(Nov 2020) Latest Safecustody Listingcinta amaniNo ratings yet

- Determinan Nilai PerusahaanDocument20 pagesDeterminan Nilai PerusahaanUtari Tri KusumaNo ratings yet

- Malware Analysis - WikipediaDocument4 pagesMalware Analysis - WikipediaihoneeNo ratings yet

- The Final Research VIVAAN SAXENADocument35 pagesThe Final Research VIVAAN SAXENAPriti DuttaNo ratings yet

- Accra Technical University: Department of Building TechnologyDocument13 pagesAccra Technical University: Department of Building TechnologyKj mingle100% (1)

- 978940180663C SMPLDocument22 pages978940180663C SMPLVi PhươngNo ratings yet

- Distribution Products - Pricelist (September) .2022)Document64 pagesDistribution Products - Pricelist (September) .2022)Gokul MenonNo ratings yet

- International Accounting Standard 7 Statement of Cash FlowsDocument8 pagesInternational Accounting Standard 7 Statement of Cash Flowsইবনুল মাইজভাণ্ডারীNo ratings yet

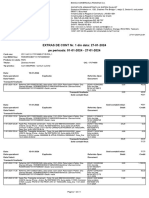

- Pe Perioada: 01-01-2024 - 27-01-2024 EXTRAS DE CONT Nr. 1 Din Data: 27-01-2024Document4 pagesPe Perioada: 01-01-2024 - 27-01-2024 EXTRAS DE CONT Nr. 1 Din Data: 27-01-2024andrei.zbercea04No ratings yet

- Jib Service Crane For RTG-Terminal 2Document7 pagesJib Service Crane For RTG-Terminal 2YasirNo ratings yet

- AVE On Azure: Julio Dominguez Sr. SE DPDDocument8 pagesAVE On Azure: Julio Dominguez Sr. SE DPDIsrael Mayen NavaNo ratings yet

- Unit III - Bahasa InggrisDocument8 pagesUnit III - Bahasa InggrisInes Tasya Eunike DimuNo ratings yet

- Bamboo Processing Factory ProposalDocument46 pagesBamboo Processing Factory ProposalNana Kofi Bimpong IINo ratings yet

- Introduction in Port ManagementDocument41 pagesIntroduction in Port ManagementAlifa Alma Adlina80% (5)

- Taco 230803PF00985414 2Document1 pageTaco 230803PF00985414 2roy.somnath.wkNo ratings yet

- Read Me TXT 100323Document18 pagesRead Me TXT 100323Viraf ChichgarNo ratings yet

- Activity TitleDocument3 pagesActivity TitledNo ratings yet

- M.C. Mehta and Anr Vs Union of India & Ors On 20 December, 1986 Equivalent Citations: 1987 AIR 1086, 1987 SCR (1) 819 Bench: Bhagwati, P.N. (CJ)Document3 pagesM.C. Mehta and Anr Vs Union of India & Ors On 20 December, 1986 Equivalent Citations: 1987 AIR 1086, 1987 SCR (1) 819 Bench: Bhagwati, P.N. (CJ)Prakher ShuklaNo ratings yet

- Pgdca - Syllabus-1 - 20 8 2010Document19 pagesPgdca - Syllabus-1 - 20 8 2010subeeshup100% (2)

- 25 CRM Analyst Interview Questions and AnswersDocument12 pages25 CRM Analyst Interview Questions and Answersjamilabano1409No ratings yet

- Form 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Document4 pagesForm 26AS: Annual Tax Statement Under Section 203AA of The Income Tax Act, 1961Deeksha SinghNo ratings yet

- 12 Points) : A B: Over Co de Ex Out Down Re Ultra UnderDocument2 pages12 Points) : A B: Over Co de Ex Out Down Re Ultra UnderRobert CalcanNo ratings yet

- Achieving Rapid Internationalization of Sub Saharan Africa - 2020 - Journal of BDocument11 pagesAchieving Rapid Internationalization of Sub Saharan Africa - 2020 - Journal of BErnaNo ratings yet

- Fabrication of PNP TransistorDocument32 pagesFabrication of PNP TransistorRahul RajNo ratings yet

- SatSure Broucher - USA - CompressedDocument4 pagesSatSure Broucher - USA - Compressedsarvesh kuraneNo ratings yet