Download as docx, pdf, or txt

You might also like

- Zeta Spenza Project: GivenDocument26 pagesZeta Spenza Project: GivenMashaal FNo ratings yet

- Rajaneesh Company - Cash FlowsDocument3 pagesRajaneesh Company - Cash FlowsAyushi Aggarwal0% (2)

- Chapter 3 - Investments in Debt Securities and Other Non-Current Financial AssetsDocument56 pagesChapter 3 - Investments in Debt Securities and Other Non-Current Financial AssetsYel75% (4)

- Module 8 - Bonds PayableDocument6 pagesModule 8 - Bonds PayableLui100% (2)

- 2019 Level II CFA Mock Exam Answers AMDocument49 pages2019 Level II CFA Mock Exam Answers AMHelloWorldNowNo ratings yet

- IA Chap. 19, 20, and 22Document31 pagesIA Chap. 19, 20, and 22Pitel O'shoppeNo ratings yet

- Chapter 19 - Financial Asset at Amortized Cost Bond InvestmentDocument8 pagesChapter 19 - Financial Asset at Amortized Cost Bond InvestmentmercyvienhoNo ratings yet

- Chapter 9Document18 pagesChapter 9Rubén ZúñigaNo ratings yet

- Smes - Assets Inventories Basic Financial Instruments Investment in Associate Investment PropertyDocument21 pagesSmes - Assets Inventories Basic Financial Instruments Investment in Associate Investment PropertyToni Rose Hernandez LualhatiNo ratings yet

- Bond InvestmentDocument2 pagesBond InvestmentPat RFNo ratings yet

- Module 5-InvestmentsDocument27 pagesModule 5-InvestmentsJane Clarisse SantosNo ratings yet

- Accounting For Investments in Debt Securities and Other Non-Current Financial AssetsDocument57 pagesAccounting For Investments in Debt Securities and Other Non-Current Financial AssetsMarriel Fate CullanoNo ratings yet

- PFRS 9, Paragraph 4.1.2, Provides That A Financial Asset Shall MeasuredDocument3 pagesPFRS 9, Paragraph 4.1.2, Provides That A Financial Asset Shall MeasuredSwai RosendeNo ratings yet

- InvestmentsDocument2 pagesInvestmentsAlora EuNo ratings yet

- Exam NotesDocument9 pagesExam NotesEven JayNo ratings yet

- Financial Instrument NotesDocument53 pagesFinancial Instrument NotesKhadija HasanNo ratings yet

- Intacc 1Document12 pagesIntacc 1Mycka Joy HernandezNo ratings yet

- Accounting For InvestmentsDocument17 pagesAccounting For InvestmentsPradeep Gupta100% (1)

- Accounting For InvestmentsDocument7 pagesAccounting For InvestmentsPaolo Immanuel OlanoNo ratings yet

- AC78 Chapter 3 Investment in Debt Securities Other Non Current Financial AssetsDocument78 pagesAC78 Chapter 3 Investment in Debt Securities Other Non Current Financial AssetsmerryNo ratings yet

- Ifrs 9 - Financial Instruments Ias 38 and Ifrs 7Document43 pagesIfrs 9 - Financial Instruments Ias 38 and Ifrs 7JaaNo ratings yet

- 161 14 PFRS 9 Financial Instrument Investment in Financial AssetDocument5 pages161 14 PFRS 9 Financial Instrument Investment in Financial AssetRegina Gregoria SalasNo ratings yet

- Financial InstrumentsDocument3 pagesFinancial InstrumentsSHIENA TECSONNo ratings yet

- Financial Assets at Amortized CostDocument8 pagesFinancial Assets at Amortized CostbluemajaNo ratings yet

- Group 3 Synthesis Report ContentDocument6 pagesGroup 3 Synthesis Report ContentCELRennNo ratings yet

- QoenfoqienfoiqnefqefDocument5 pagesQoenfoqienfoiqnefqefCharmaine Mari OlmosNo ratings yet

- LECTURE I InvestmentDocument5 pagesLECTURE I Investmentrodell pabloNo ratings yet

- Investments and AcquisitionsDocument5 pagesInvestments and AcquisitionsBurhan Al MessiNo ratings yet

- Investment NotesDocument12 pagesInvestment NotesLenrey CobachaNo ratings yet

- As 13Document11 pagesAs 13Avinash YadavNo ratings yet

- IntAcc1.3LN Investments in Debt Equity InstrumentsDocument4 pagesIntAcc1.3LN Investments in Debt Equity InstrumentsJohn AlbateraNo ratings yet

- Module 17-Bonds-PayableDocument12 pagesModule 17-Bonds-PayableJehPoyNo ratings yet

- Module 1 - Bonds Payable: Dalubhasaan NG Lungsod NG Lucena Intercompany Accounting Part 3 Faye Margaret P. Rocero, CPADocument3 pagesModule 1 - Bonds Payable: Dalubhasaan NG Lungsod NG Lucena Intercompany Accounting Part 3 Faye Margaret P. Rocero, CPABrein Symon DialaNo ratings yet

- Week 05 - 01 - Module 10 - Financial Assets at Fair ValueDocument11 pagesWeek 05 - 01 - Module 10 - Financial Assets at Fair Value지마리No ratings yet

- Gialogo, Jessie LynDocument2 pagesGialogo, Jessie LynMeidrick Rheeyonie Gialogo AlbaNo ratings yet

- 06B Investment in Debt SecuritiesDocument4 pages06B Investment in Debt Securitiesrandomlungs121223No ratings yet

- Financial Management Unit 2Document10 pagesFinancial Management Unit 2Janardhan VNo ratings yet

- Chapter 10 Investments in Debt SecuritiesDocument24 pagesChapter 10 Investments in Debt SecuritiesChristian Jade Lumasag NavaNo ratings yet

- IFRS 9 Theory PDFDocument19 pagesIFRS 9 Theory PDFAbbas AliNo ratings yet

- IA Downloaded From GoogleDocument5 pagesIA Downloaded From Googlearnold espiniliNo ratings yet

- Ifrs 9Document2 pagesIfrs 9MuhammadNo ratings yet

- 2009 F-5 Class NotesDocument3 pages2009 F-5 Class NotesChris Tian FlorendoNo ratings yet

- Lesson 1 (Week 1) - Financial Assets at Fair Value and Investment in BondsDocument14 pagesLesson 1 (Week 1) - Financial Assets at Fair Value and Investment in BondsMonica MonicaNo ratings yet

- CH 9 Lecture NotesDocument14 pagesCH 9 Lecture NotesraveenaatNo ratings yet

- Investment AccountsDocument10 pagesInvestment AccountsMani kandan.GNo ratings yet

- Financial AssetsDocument6 pagesFinancial AssetsJhen VillanuevaNo ratings yet

- Financial Instrument - (NEW)Document11 pagesFinancial Instrument - (NEW)AS Gaming100% (1)

- Pfrs 9 Financial Instruments Summary Financial Assets Financial Liabilities and Equity InstrumentsDocument6 pagesPfrs 9 Financial Instruments Summary Financial Assets Financial Liabilities and Equity InstrumentsSHARON SAMSONNo ratings yet

- Bonds PayableDocument3 pagesBonds PayableKimberly ZafraNo ratings yet

- Financial Accounting and Reporting - InvestmentsDocument10 pagesFinancial Accounting and Reporting - InvestmentsLuisitoNo ratings yet

- 1 IFRS 9 - Financial InstrumentsDocument31 pages1 IFRS 9 - Financial InstrumentsSharmaineMirandaNo ratings yet

- NOTES On PFRS 9 Financial InstrumentsDocument11 pagesNOTES On PFRS 9 Financial Instrumentsjsus22100% (1)

- M3 Accele 4Document15 pagesM3 Accele 4Julie Marie Anne LUBINo ratings yet

- UBL AnalysisDocument19 pagesUBL Analysismuhammad akramNo ratings yet

- What Does The DFL of 3 Times Imply?Document7 pagesWhat Does The DFL of 3 Times Imply?Sushil ShresthaNo ratings yet

- Investment Strategy Analysis Level 3 - Ifrs 9,10,3,11 & Ias 28Document11 pagesInvestment Strategy Analysis Level 3 - Ifrs 9,10,3,11 & Ias 28Richie BoomaNo ratings yet

- Financial Investments OverviewDocument9 pagesFinancial Investments OverviewPat RFNo ratings yet

- Subject No 16J Corporate Financial Management Pilot Paper Suggested AnswersDocument14 pagesSubject No 16J Corporate Financial Management Pilot Paper Suggested Answerstata-lohNo ratings yet

- Chapter 17Document14 pagesChapter 17TruyenLeNo ratings yet

- CH 5 Cost of Capital Theory (510139)Document10 pagesCH 5 Cost of Capital Theory (510139)Syeda AtikNo ratings yet

- InvestmentDocument39 pagesInvestmentJames R JunioNo ratings yet

- Summary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingFrom EverandSummary of Michael J. Mauboussin & Alfred Rappaport's Expectations InvestingNo ratings yet

- Assignment Discussions On Interim Financial ReportingDocument3 pagesAssignment Discussions On Interim Financial ReportingAllysa Jane FajilagmagoNo ratings yet

- INTACCDocument7 pagesINTACCAllysa Jane FajilagmagoNo ratings yet

- ScienceDocument1 pageScienceAllysa Jane FajilagmagoNo ratings yet

- Cooking Up A Great YearDocument4 pagesCooking Up A Great YearAllysa Jane FajilagmagoNo ratings yet

- Romblon State University Graduate Education and Professional StudiesDocument13 pagesRomblon State University Graduate Education and Professional StudiesAllysa Jane FajilagmagoNo ratings yet

- Criminology 5Document32 pagesCriminology 5Allysa Jane FajilagmagoNo ratings yet

- Criminology 2: Criminal Justice System By: Poly D. Banagan Criminal Justice System DefinedDocument13 pagesCriminology 2: Criminal Justice System By: Poly D. Banagan Criminal Justice System DefinedAllysa Jane FajilagmagoNo ratings yet

- Criminology 4Document19 pagesCriminology 4Allysa Jane FajilagmagoNo ratings yet

- Criminology 3 Police Ethics and Community Relations By: Poly D. BanaganDocument16 pagesCriminology 3 Police Ethics and Community Relations By: Poly D. BanaganAllysa Jane FajilagmagoNo ratings yet

- 2017 The Secret Trader EbookDocument71 pages2017 The Secret Trader EbookAdnan Wasim100% (3)

- NSE - Forex & Derivatives Quiz 1 QuestionsDocument3 pagesNSE - Forex & Derivatives Quiz 1 QuestionsDHRUV SONAGARANo ratings yet

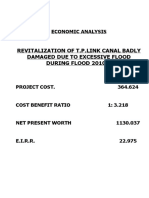

- Revitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Document4 pagesRevitalization of T.P.Link Canal Badly Damaged Due To Excessive Flood During Flood 2010"Xshf AkNo ratings yet

- 2 - A. Problems - Property Plant and EquipmentDocument59 pages2 - A. Problems - Property Plant and EquipmentsbibandiganNo ratings yet

- FinMod 2022-2023 Tutorial Exercise + Answers Week 5Document36 pagesFinMod 2022-2023 Tutorial Exercise + Answers Week 5jjpasemperNo ratings yet

- Consumer LoansDocument44 pagesConsumer LoansReign Angela Abcidee TembliqueNo ratings yet

- Advanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (29-35)Document1 pageAdvanced Accounting - Dayag 2015 - Chapter 15 - Multiple Choice Solution (29-35)John Carlos Doringo100% (1)

- International Capital MovementDocument14 pagesInternational Capital MovementRohan NairNo ratings yet

- SMA H1 Trading SystemDocument5 pagesSMA H1 Trading SystemChrisLaw123No ratings yet

- MKTM511 SyllabusDocument2 pagesMKTM511 Syllabusastitvaawasthi33No ratings yet

- Risk and Rate of Returns in Financial ManagementDocument50 pagesRisk and Rate of Returns in Financial ManagementReaderNo ratings yet

- LCCI Level 2 Certificate in Bookkeeping and Accounting ASE20093 RB Jul 2018Document8 pagesLCCI Level 2 Certificate in Bookkeeping and Accounting ASE20093 RB Jul 2018Ei Ei TheintNo ratings yet

- Tutorial JOCDocument5 pagesTutorial JOCainfarhanaNo ratings yet

- Fundamentals of Accountancy, Business and Management 2 (First Quarter)Document48 pagesFundamentals of Accountancy, Business and Management 2 (First Quarter)Bernard BaruizNo ratings yet

- Market EfficiencyDocument32 pagesMarket Efficiencyrobi atmajayaNo ratings yet

- C. Worksheet 1 - Liquidation - B List of ContributoriesDocument7 pagesC. Worksheet 1 - Liquidation - B List of ContributoriesSnigdha RohillaNo ratings yet

- Parliament of The Republic of Ghana - Non-Bank Financial Institutions Act 2008 - Act 774Document30 pagesParliament of The Republic of Ghana - Non-Bank Financial Institutions Act 2008 - Act 774sam mammoNo ratings yet

- Garcia Vs Thio Case DigestDocument2 pagesGarcia Vs Thio Case DigestJet Siang100% (2)

- 2023 JanDocument64 pages2023 Janbass67% (3)

- Corporate RestructuringDocument46 pagesCorporate RestructuringMilu Mathew MoorkkattilNo ratings yet

- Interpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions ManualDocument38 pagesInterpreting and Analyzing Financial Statements 6th Edition Schoenebeck Solutions Manualhudsoncolepiu100% (19)

- Financial Analysis 2Document17 pagesFinancial Analysis 2Lovely Bordaje dela FuenteNo ratings yet

- IAS 1 Presentation of Financial Statements (2021)Document17 pagesIAS 1 Presentation of Financial Statements (2021)Tawanda Tatenda Herbert100% (1)

- Asset Backed SecuritiesDocument22 pagesAsset Backed Securitieskah53100% (2)

- Lecture Session 8 - Currency Option Contingency GraphsDocument9 pagesLecture Session 8 - Currency Option Contingency Graphsapi-19974928No ratings yet

- PWS Calculator Guide HP 17bIIDocument21 pagesPWS Calculator Guide HP 17bIIKeijo SalonenNo ratings yet

- Group II RTP Dec 2012Document173 pagesGroup II RTP Dec 2012Prekshit KalashdharNo ratings yet