Download as pdf or txt

You might also like

- Dealing With A PresentmentDocument4 pagesDealing With A PresentmentMaryUmbrello-Dressler100% (16)

- CertificateDocument10 pagesCertificateremotepro47No ratings yet

- Corporations Attack OutlineDocument7 pagesCorporations Attack OutlineJoe100% (5)

- Types of Letters of CreditDocument4 pagesTypes of Letters of CreditSudershan Thaiba100% (1)

- FRM Exam Questions Financial Markets and ProductsDocument4 pagesFRM Exam Questions Financial Markets and ProductsEmmanuelDasiNo ratings yet

- When It Comes To Securing Your Loved Ones, Trust Us.: Saral JeevanDocument10 pagesWhen It Comes To Securing Your Loved Ones, Trust Us.: Saral Jeevanjithin jayNo ratings yet

- Saral Jeevan Bima Brochure-BRDocument10 pagesSaral Jeevan Bima Brochure-BRprabuNo ratings yet

- Digishield Plan BrochureDocument48 pagesDigishield Plan BrochureSuraj GawandeNo ratings yet

- Awg BrochureDocument16 pagesAwg BrochureRameshwar RathodNo ratings yet

- HDFC Click2protectlife BrochureDocument25 pagesHDFC Click2protectlife BrochureaaaNo ratings yet

- Secure Your Family Against Uncertainties, With A Plan That Adjusts To Your NeedsDocument25 pagesSecure Your Family Against Uncertainties, With A Plan That Adjusts To Your Needsroxcox216No ratings yet

- HDFC Life Sanchay Plus Retail Brochure Final CTCDocument16 pagesHDFC Life Sanchay Plus Retail Brochure Final CTCPM LOgsNo ratings yet

- HDFCLife SanchayPlus ProductBrochureDocument16 pagesHDFCLife SanchayPlus ProductBrochurecrAzY cHandhUrUNo ratings yet

- HDFC Life Sanchay Plus - Retail - Brochure - Final - CTCDocument16 pagesHDFC Life Sanchay Plus - Retail - Brochure - Final - CTCvkbasavaNo ratings yet

- Tata AIA Click2 Invest-Income ComboDocument24 pagesTata AIA Click2 Invest-Income ComboSubhadip GhoshNo ratings yet

- HDFC Life Brochure-2Document7 pagesHDFC Life Brochure-2Kamal Kannan GNo ratings yet

- I Have Big Plans For My Family.: I Am Glad They Don't Cost BigDocument25 pagesI Have Big Plans For My Family.: I Am Glad They Don't Cost Bigswaraj Vikrant BhosaleNo ratings yet

- ABSLI Poorna Suraksha Kawach Plan V2 BrochureDocument37 pagesABSLI Poorna Suraksha Kawach Plan V2 Brochuregaurav sharmaNo ratings yet

- PWP LeafletDocument4 pagesPWP LeafletsatishbhattNo ratings yet

- Tax-Free Returns: Life's Journey Needs Milestones, Not Tax HurdlesDocument16 pagesTax-Free Returns: Life's Journey Needs Milestones, Not Tax HurdlesAdvocate JaniNo ratings yet

- Max Life Flexi Wealth Advantage Plan_Prospectus_website upload (1) (2)Document41 pagesMax Life Flexi Wealth Advantage Plan_Prospectus_website upload (1) (2)uchihawajidNo ratings yet

- HDFC Life Sanchay Plus - Retail - Brochure - Final - CTC PDFDocument16 pagesHDFC Life Sanchay Plus - Retail - Brochure - Final - CTC PDFabhinav guptaNo ratings yet

- Edelweiss Tokio Life - Income Builder - : OverviewDocument2 pagesEdelweiss Tokio Life - Income Builder - : OverviewarunNo ratings yet

- HDFC Life Brochure-15Document16 pagesHDFC Life Brochure-15nayaksaismritiNo ratings yet

- Edelweiss Tokio Life - Cashflow Protection Plus - : OverviewDocument2 pagesEdelweiss Tokio Life - Cashflow Protection Plus - : OverviewarunNo ratings yet

- SBI Life - Saral Jeevan Bima - BrochureDocument9 pagesSBI Life - Saral Jeevan Bima - BrochureH.O. Rajendra TiwariNo ratings yet

- HDFC Capital GuaranteeDocument34 pagesHDFC Capital GuaranteeRanjan SharmaNo ratings yet

- ABSLI DigiShield Plan Brochure V09Document50 pagesABSLI DigiShield Plan Brochure V09Sanika ChhabraNo ratings yet

- HDFC Life Click 2 InvestDocument7 pagesHDFC Life Click 2 InvestShaik BademiyaNo ratings yet

- Smart Elite V03 Single PagerDocument2 pagesSmart Elite V03 Single PagerAkankshaNo ratings yet

- HDFC Life Click 2 Wealth - Brochure - Retail - V3Document16 pagesHDFC Life Click 2 Wealth - Brochure - Retail - V3a26geniusNo ratings yet

- HDFC Life Sanchay Plus - Retail - Brochure - Final - CTCDocument17 pagesHDFC Life Sanchay Plus - Retail - Brochure - Final - CTCK chandra sekharNo ratings yet

- Saral Jeevan Bima BrochureDocument7 pagesSaral Jeevan Bima BrochureKarthik RamNo ratings yet

- Pramerica Life Rakshak SmartDocument10 pagesPramerica Life Rakshak SmartTraditional SamayalNo ratings yet

- Retire - Smart - Brochure - Brand ReimagineDocument16 pagesRetire - Smart - Brochure - Brand Reimagineneop lopianNo ratings yet

- HDFC Life Sanchay Legacy BrochureDocument36 pagesHDFC Life Sanchay Legacy BrochureRohit RawatNo ratings yet

- In A Life With No Guarantees,: SanchayDocument17 pagesIn A Life With No Guarantees,: SanchaySonu SinghNo ratings yet

- Savings Advantage Plan LeafletDocument2 pagesSavings Advantage Plan LeafletNishanthNo ratings yet

- HDFC Life - Trad - Combo - BrochureDocument33 pagesHDFC Life - Trad - Combo - Brochurea26geniusNo ratings yet

- SBI Life - Retire Smart - Brochure - Ver03Document16 pagesSBI Life - Retire Smart - Brochure - Ver03Vishal kaushalendra Kumar singhNo ratings yet

- Assured Returns.: Our PromiseDocument12 pagesAssured Returns.: Our PromiseVinodkumar ShethNo ratings yet

- Smart Platina Assure - One - Pager FinalDocument2 pagesSmart Platina Assure - One - Pager FinalpankajNo ratings yet

- Smart Platina Assure Brochure FinalDocument12 pagesSmart Platina Assure Brochure Finalsksen007No ratings yet

- Put Your Financial Life On Autopilot With Guaranteed BenefitsDocument16 pagesPut Your Financial Life On Autopilot With Guaranteed BenefitspapaNo ratings yet

- Smart - Wealth - Builder - Brochure - Brand ReimagineDocument20 pagesSmart - Wealth - Builder - Brochure - Brand ReimagineikonmobileshopNo ratings yet

- Secure Your Family's Goals With A Choice of Funds and BenefitsDocument9 pagesSecure Your Family's Goals With A Choice of Funds and BenefitsSainath MundheNo ratings yet

- Retire Smart Product GuideDocument2 pagesRetire Smart Product GuideKathirrvelu SubramanianNo ratings yet

- Future Wealth Gain PDFDocument23 pagesFuture Wealth Gain PDFviswanathbobby8No ratings yet

- Kotak Classic Endowment Plan Brochure1Document12 pagesKotak Classic Endowment Plan Brochure1Kranthi Kumar ReddyNo ratings yet

- SBI Life - Smart Platina Assure - BrochureDocument12 pagesSBI Life - Smart Platina Assure - Brochuresourav agarwalNo ratings yet

- Sanchay PlusDocument31 pagesSanchay PlusiamshonalidixitNo ratings yet

- Aviva Dhan Suraksha 122N132V02Document2 pagesAviva Dhan Suraksha 122N132V02Kamakhya ShaktipeethNo ratings yet

- ABSLI Assured SavingDocument20 pagesABSLI Assured Savingm00162372No ratings yet

- 4906-ICICI Pru-Lakshya-Gold Plan-One Pager-27DecDocument2 pages4906-ICICI Pru-Lakshya-Gold Plan-One Pager-27DecMehul Bajaj100% (1)

- HDFC Life Click 2 Protect Life - Product Brochure PDFDocument24 pagesHDFC Life Click 2 Protect Life - Product Brochure PDFvaibhav kumar KhokharNo ratings yet

- Smart+Platina+Assure+Brochure V05Document12 pagesSmart+Platina+Assure+Brochure V05azad7992No ratings yet

- SBI Life - Smart Platina Assure - BrochureDocument12 pagesSBI Life - Smart Platina Assure - BrochureSanjeev KulkarniNo ratings yet

- Aegon Lifei Term Prime BrochureDocument9 pagesAegon Lifei Term Prime Brochuredaskaran3141No ratings yet

- B.V. Patel Institute of Management, Uka Tarsadia University: Group No.: 8Document12 pagesB.V. Patel Institute of Management, Uka Tarsadia University: Group No.: 8Pankaj RawatNo ratings yet

- Saral Swadhan Supreme - Brochure - V01 15th JanDocument9 pagesSaral Swadhan Supreme - Brochure - V01 15th JanNitin KumarNo ratings yet

- PNB Metlife Saving PlanDocument6 pagesPNB Metlife Saving PlanPurnima PurohitNo ratings yet

- Sanchay Plus - v09 BrochureDocument30 pagesSanchay Plus - v09 BrochureshwetaNo ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- The Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1From EverandThe Basics of Life Insurance: The Answer to What Life Insurance is and How It Works: Personal Finance, #1No ratings yet

- Unit 5 - Indian Partnership Act, 1932Document29 pagesUnit 5 - Indian Partnership Act, 1932Prabhnoor KaurNo ratings yet

- Caltex Philippines Inc. v. CADocument2 pagesCaltex Philippines Inc. v. CAsectionbcoeNo ratings yet

- ﻣ ﺮ ﻛ ﺒ ﺎ ت ﺗ أ ﻣ ﯿ ﻦ ﺷ ﮫ ﺎ د ة Mo To R Insurance CertificateDocument2 pagesﻣ ﺮ ﻛ ﺒ ﺎ ت ﺗ أ ﻣ ﯿ ﻦ ﺷ ﮫ ﺎ د ة Mo To R Insurance CertificateHassan ShahhatNo ratings yet

- Contract and Its KindsDocument4 pagesContract and Its Kinds✬ SHANZA MALIK ✬No ratings yet

- Continuing Corporate GuaranteeDocument19 pagesContinuing Corporate GuaranteeMuhammad DafisNo ratings yet

- Pre Final Quiz 1Document2 pagesPre Final Quiz 1Xiu MinNo ratings yet

- 7 PArtnershipDocument12 pages7 PArtnershipnatsu lolNo ratings yet

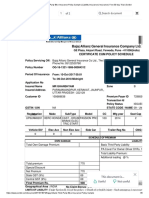

- Tata AIG Motor Policy Schedule - 3184 - 6200120953-00 - Hanun SreedharDocument4 pagesTata AIG Motor Policy Schedule - 3184 - 6200120953-00 - Hanun SreedharHANUNNo ratings yet

- BPO UNIT - 5 Types of Securities Mode of Creating Charge Bank Guarantees Basel NormsDocument61 pagesBPO UNIT - 5 Types of Securities Mode of Creating Charge Bank Guarantees Basel NormsDishank JohriNo ratings yet

- Deed of Retirement: TH NDDocument4 pagesDeed of Retirement: TH NDKushwanth Soft SolutionsNo ratings yet

- Law of Contracts: An IntroductionDocument29 pagesLaw of Contracts: An IntroductionAliasgar BohraNo ratings yet

- Bajaj Allianz Third Party Bike Insurance Policy Sample - Liability Insurance - Insurance - Free 30-Day Trial - ScribdDocument6 pagesBajaj Allianz Third Party Bike Insurance Policy Sample - Liability Insurance - Insurance - Free 30-Day Trial - ScribdIshu Bisht100% (3)

- Insurance Regulatory Framework: Main Reasons For Insurance Regulation IrdaiDocument12 pagesInsurance Regulatory Framework: Main Reasons For Insurance Regulation IrdaiIndeevar SarkarNo ratings yet

- Advanced Accounting Solutions Chapter 7 ProblemsDocument2 pagesAdvanced Accounting Solutions Chapter 7 Problemsjohn carlos doringoNo ratings yet

- Documents of The Title of GoodsDocument23 pagesDocuments of The Title of GoodsAlina TahirNo ratings yet

- Chapter 4-6 - Company LawDocument73 pagesChapter 4-6 - Company LawSu Yi TanNo ratings yet

- United States Design Patent (10) Patent No.: US D467,424 SDocument7 pagesUnited States Design Patent (10) Patent No.: US D467,424 SHugo Mauricio Echeverry HerreraNo ratings yet

- Discharge of A ContractDocument9 pagesDischarge of A ContractGene's100% (1)

- Consideration Section 2d: Nudum Pactum A Nude or Bare Agreement Is VoidDocument17 pagesConsideration Section 2d: Nudum Pactum A Nude or Bare Agreement Is VoidPranay BhardwajNo ratings yet

- Matem Financ - J Rodriguez Franco - E C Rodriguez Jimenez Ed Patria 201401 (Cap 4 Interés Compuesto)Document38 pagesMatem Financ - J Rodriguez Franco - E C Rodriguez Jimenez Ed Patria 201401 (Cap 4 Interés Compuesto)Nadia MaldonadoNo ratings yet

- BLT1 - Dec 6 - QuizDocument1 pageBLT1 - Dec 6 - QuizRoselle AnneNo ratings yet

- Collateral Consistent Derivatives Pricing 2 PDFDocument27 pagesCollateral Consistent Derivatives Pricing 2 PDFshih_kaichihNo ratings yet

- Completion Examination: ND RDDocument5 pagesCompletion Examination: ND RDNicole DeocarisNo ratings yet

- Hertz Vehicle Financing II, 9.30.2015 PDFDocument339 pagesHertz Vehicle Financing II, 9.30.2015 PDFaweinerNo ratings yet

- Obligations and Contracts SyllabusDocument4 pagesObligations and Contracts SyllabusMARYLIZA SAEZNo ratings yet