Download as docx, pdf, or txt

You might also like

- Internal Control Manual - BankDocument12 pagesInternal Control Manual - Bankrafael amparoNo ratings yet

- MAEDocument9 pagesMAEArjen PaderogNo ratings yet

- Answer-1 A. Permanent FileDocument11 pagesAnswer-1 A. Permanent FileYoosuf Mohamed IrsathNo ratings yet

- Unit 1Document8 pagesUnit 1FantayNo ratings yet

- Financial Accounting 1 Unit 1Document8 pagesFinancial Accounting 1 Unit 1chuchuNo ratings yet

- Internal Control and Cash Management Manual and Questionnaires November 1995Document18 pagesInternal Control and Cash Management Manual and Questionnaires November 1995Anonymous VtsflLix1100% (2)

- Accounting Information For Managers - Chapter OneDocument2 pagesAccounting Information For Managers - Chapter Onegumtree472No ratings yet

- Process Financial TNXN TTLM Nigussie BDocument40 pagesProcess Financial TNXN TTLM Nigussie Bnigus50% (2)

- Ethiopian Gov't AssignmentDocument7 pagesEthiopian Gov't AssignmentHasen Yib0% (1)

- Consideration of Internal ControlDocument7 pagesConsideration of Internal Controlemc2_mcv100% (1)

- Internal Control: Auditing TheoryDocument7 pagesInternal Control: Auditing Theoryrandom17341No ratings yet

- FA Iof 1Document15 pagesFA Iof 1weyessagetuNo ratings yet

- Financial ManagementDocument18 pagesFinancial ManagementAemro TadeleNo ratings yet

- FIN 612 Notes PDFDocument34 pagesFIN 612 Notes PDFIvy Bucks WanjikuNo ratings yet

- AAT Paper 2 FinanceDocument4 pagesAAT Paper 2 FinanceRay LaiNo ratings yet

- At 14 Internal Control CompressDocument13 pagesAt 14 Internal Control Compressmariakate LeeNo ratings yet

- Internal Control Policy (1) AustraliaDocument8 pagesInternal Control Policy (1) AustraliabulmezNo ratings yet

- Management Information SystemsDocument6 pagesManagement Information SystemsMohalaf naeemNo ratings yet

- Accounting PolicyDocument19 pagesAccounting PolicySayali shenkarNo ratings yet

- Module 12Document5 pagesModule 12AstxilNo ratings yet

- Draft APDocument6 pagesDraft APhchi7171No ratings yet

- FABM1TGhandouts L23BranchesOfAcctgDocument2 pagesFABM1TGhandouts L23BranchesOfAcctgKarl Vincent DulayNo ratings yet

- Chapter 1 AccDocument6 pagesChapter 1 AccMarta Fdez-FournierNo ratings yet

- Financial Accounting and Reporting 03Document6 pagesFinancial Accounting and Reporting 03Nuah SilvestreNo ratings yet

- SCM ModulesDocument16 pagesSCM ModulesAbby SantosNo ratings yet

- UNIT 1 Fundamentals of Financial AccountingDocument17 pagesUNIT 1 Fundamentals of Financial AccountingPavithraNo ratings yet

- MODULE 7 - Internal Control System Evaluation QUIZZERDocument27 pagesMODULE 7 - Internal Control System Evaluation QUIZZERRufina B VerdeNo ratings yet

- Chapter 1Document8 pagesChapter 1Bēkām BūllōōNo ratings yet

- Nature and Purpose of Internal ControlDocument16 pagesNature and Purpose of Internal ControlJeric Lagyaban AstrologioNo ratings yet

- At-14-Internal-Control ReviewerDocument14 pagesAt-14-Internal-Control ReviewerHI HelloNo ratings yet

- Internal Control Is The Process Designed and Effected by Those Charged With Governance, Management andDocument12 pagesInternal Control Is The Process Designed and Effected by Those Charged With Governance, Management andglaide lojeroNo ratings yet

- Glory Full ProjectDocument58 pagesGlory Full ProjectinisamagencyNo ratings yet

- Chapter 2-Textbook (Accounting An Introduction)Document34 pagesChapter 2-Textbook (Accounting An Introduction)Jimmy MulokoshiNo ratings yet

- M1 Handout 4 Conceptual Framework of AccountingDocument9 pagesM1 Handout 4 Conceptual Framework of AccountingAmelia TaylorNo ratings yet

- At - (14) Internal ControlDocument13 pagesAt - (14) Internal ControlLorena Joy Aggabao100% (2)

- Auditing Theory - Risk AssessmentDocument10 pagesAuditing Theory - Risk AssessmentYenelyn Apistar CambarijanNo ratings yet

- Conceptual Framework & Accounting Standards: Three Important ActivitiesDocument12 pagesConceptual Framework & Accounting Standards: Three Important ActivitiesKendiNo ratings yet

- Guide On in - Year Management, Monitoring and ReportingDocument49 pagesGuide On in - Year Management, Monitoring and ReportingriaanNo ratings yet

- AT - (14) Internal ControlDocument16 pagesAT - (14) Internal ControlCarla TañecaNo ratings yet

- FinAcc Chapter 1Document8 pagesFinAcc Chapter 1IrmaNo ratings yet

- Chapter 1audi 2015 DUDocument10 pagesChapter 1audi 2015 DUMoti BekeleNo ratings yet

- Ten Essential Elements of A Successful Electronic Records Retention and Destruction ProgramDocument4 pagesTen Essential Elements of A Successful Electronic Records Retention and Destruction Programquickmelt03No ratings yet

- W2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1Document6 pagesW2 Module 3 Conceptual Framework Andtheoretical Structure of Financial Accounting and Reporting Part 1Rose RaboNo ratings yet

- Roles and Organizational Aspects of Controlling: Mgr. Andrea Gažová, PHDDocument29 pagesRoles and Organizational Aspects of Controlling: Mgr. Andrea Gažová, PHDRoberto SanchezNo ratings yet

- 9.internal ControlDocument13 pages9.internal ControlNairobi SalazarNo ratings yet

- FA FOR BADM Unit 2Document17 pagesFA FOR BADM Unit 2GUDATA ABARANo ratings yet

- IT in Accounting and FinanceDocument6 pagesIT in Accounting and FinanceHarshk JainNo ratings yet

- Accounting FrameworkDocument50 pagesAccounting FrameworkmohitNo ratings yet

- Management Accounting EssayDocument3 pagesManagement Accounting EssayUsman KhanNo ratings yet

- Historical Overview of Ethiopian Government Accounting SystemDocument20 pagesHistorical Overview of Ethiopian Government Accounting Systemnegamedhane58100% (3)

- Summary of Accounting Information SystemsDocument5 pagesSummary of Accounting Information SystemsScribdTranslationsNo ratings yet

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"From Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"No ratings yet

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Dollars and Sense: Demystifying Financial Records for Business OwnersFrom EverandDollars and Sense: Demystifying Financial Records for Business OwnersNo ratings yet

- Mastering Bookkeeping: Unveiling the Key to Financial SuccessFrom EverandMastering Bookkeeping: Unveiling the Key to Financial SuccessNo ratings yet

- Universty of Gonder: College of Business and EconomicsDocument9 pagesUniversty of Gonder: College of Business and EconomicsJossi AbuleNo ratings yet

- Buget 2018Document299 pagesBuget 2018Jossi AbuleNo ratings yet

- A Research Proposal Submitted in Partial Fulfilment of The Requirements For The Degree of Marketing ManagementDocument40 pagesA Research Proposal Submitted in Partial Fulfilment of The Requirements For The Degree of Marketing ManagementJossi AbuleNo ratings yet

- Business ConceptDocument22 pagesBusiness ConceptJossi AbuleNo ratings yet

- A Black Man Ponders His Powers To Alter Public SpaceDocument3 pagesA Black Man Ponders His Powers To Alter Public SpacerailamutukaNo ratings yet

- 21-05-14 VLSI Opposition To Intel's Rule 52 Motion (Unclean Hands)Document27 pages21-05-14 VLSI Opposition To Intel's Rule 52 Motion (Unclean Hands)Florian MuellerNo ratings yet

- Corporate Governance - A Global Perspective PDFDocument47 pagesCorporate Governance - A Global Perspective PDFAsham SharmaNo ratings yet

- Int Acc 1Document49 pagesInt Acc 1kookie bunnyNo ratings yet

- 翻查Document40 pages翻查bomif45831No ratings yet

- Input Data Sheet For E-Class Record: Region Division District School Name School Id School YearDocument21 pagesInput Data Sheet For E-Class Record: Region Division District School Name School Id School YearElma Clarissa ToscanoNo ratings yet

- Let's Make A Deal TV Show TicketsDocument3 pagesLet's Make A Deal TV Show TicketsJennifer CarleyNo ratings yet

- Umsc-Constitution 231130 124045Document28 pagesUmsc-Constitution 231130 124045ibrasebsNo ratings yet

- Marx's Theory of History.Document4 pagesMarx's Theory of History.Ayeni KhemiNo ratings yet

- 2CL BRAGANCIA (Sec C) - CASE DIGEST (Gudani V Senga)Document4 pages2CL BRAGANCIA (Sec C) - CASE DIGEST (Gudani V Senga)Ian Joseph BraganciaNo ratings yet

- Revilla v. Office of The Ombudsman20170125-898-5i1u8sDocument76 pagesRevilla v. Office of The Ombudsman20170125-898-5i1u8sAngelicaNo ratings yet

- Developing Professionals For The Lifting Equipment IndustryDocument199 pagesDeveloping Professionals For The Lifting Equipment IndustryYoussef DaoudNo ratings yet

- Brief From Seattle School Board Director Chandra Hampson in Reply To Seattle School District No. 1's BriefDocument14 pagesBrief From Seattle School Board Director Chandra Hampson in Reply To Seattle School District No. 1's BriefMel WestbrookNo ratings yet

- Ifla Poster SdgsDocument1 pageIfla Poster SdgsLouise Ian T. de los Reyes-AquinoNo ratings yet

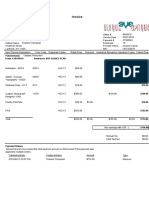

- Invoice: Patient Name: Order # 28798120 Insurance: VSP CHOICE PLANDocument2 pagesInvoice: Patient Name: Order # 28798120 Insurance: VSP CHOICE PLANUniqueEye OptiqueNo ratings yet

- Federal Criminal Complaint Against Jared LoughnerDocument6 pagesFederal Criminal Complaint Against Jared LoughnerVOA NewsNo ratings yet

- Principles and Lawful Basis Governing Data Protection in NigeriaDocument8 pagesPrinciples and Lawful Basis Governing Data Protection in Nigerialeke oyeniranNo ratings yet

- Contract Cheating TeqsaDocument11 pagesContract Cheating TeqsaTeacher Test AccountNo ratings yet

- Notice Pay Rent or QuitDocument3 pagesNotice Pay Rent or QuitSmart SaravananNo ratings yet

- 010a - Annexure 10a - SOP For Fixed Assets - 311018Document3 pages010a - Annexure 10a - SOP For Fixed Assets - 311018MahabubnubNo ratings yet

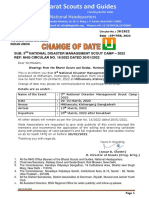

- Circular No. 30 3rd National Disaster Management Scout Camp - 2022Document1 pageCircular No. 30 3rd National Disaster Management Scout Camp - 2022Om SolankiNo ratings yet

- Jawaban English ACC 5EDocument7 pagesJawaban English ACC 5EAndre HabibNo ratings yet

- Polity E-BookDocument192 pagesPolity E-Bookpainfighter3No ratings yet

- Ecf3121 AssignmentDocument3 pagesEcf3121 AssignmentCharl PontillaNo ratings yet

- Privilege What Does It Mean HandoutDocument3 pagesPrivilege What Does It Mean Handoutanayaa agarwalNo ratings yet

- India Today - 1909Document68 pagesIndia Today - 1909dev guptaNo ratings yet

- Asan NamazDocument33 pagesAsan Namazsaamir_naeem67% (3)

- The Pacific War 1941-45: Empire of The SunDocument56 pagesThe Pacific War 1941-45: Empire of The SunIvánNo ratings yet

- Analyzing The Role of Social Media in Crime PreventionDocument3 pagesAnalyzing The Role of Social Media in Crime PreventionBERAMO, LIZA MARIENo ratings yet

- Vlog On SuccessionsDocument2 pagesVlog On SuccessionsJosephineFadulNo ratings yet