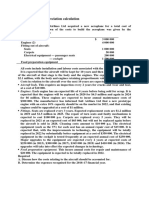

Chapter 5: Property, Plant and Equipment

Chapter 5: Property, Plant and Equipment

You might also like

- Auditing Theory Test BankDocument31 pagesAuditing Theory Test BankLyza96% (53)

- FR QM - Section B PDFDocument74 pagesFR QM - Section B PDFRishi KumaarNo ratings yet

- PpeDocument7 pagesPpeJasmine Marie Ng CheongNo ratings yet

- AP - Ppe, Int. & Invest PropDocument15 pagesAP - Ppe, Int. & Invest PropJolina ManceraNo ratings yet

- Assignment No 7 - Plant Assets & DepreciationDocument12 pagesAssignment No 7 - Plant Assets & DepreciationRehan Memon67% (3)

- 1A Group 1 To 6 Reporting Legal Techniques and LogicDocument36 pages1A Group 1 To 6 Reporting Legal Techniques and LogicJohnson Yaplin100% (1)

- Exercises Ppe PDFDocument6 pagesExercises Ppe PDFمعن الفاعوري100% (1)

- Acct CH.7 H.W.Document8 pagesAcct CH.7 H.W.j8noelNo ratings yet

- Tangible Non-Current Assets: QuestionsDocument5 pagesTangible Non-Current Assets: QuestionsЕкатерина КидяшеваNo ratings yet

- AIS16Exercises SCDocument6 pagesAIS16Exercises SCSarah GherdaouiNo ratings yet

- Lecture # 21Document4 pagesLecture # 21HussainNo ratings yet

- EXERCISES - PPE, Part 2Document5 pagesEXERCISES - PPE, Part 2Meeka CalimagNo ratings yet

- Problem 30-1 (IAA)Document7 pagesProblem 30-1 (IAA)Quinnie Apuli0% (1)

- Ias 16 Ppe ExerciseDocument12 pagesIas 16 Ppe ExerciseMazni Hanisah75% (4)

- Saad SB (Q (4+9) ) FinalDocument4 pagesSaad SB (Q (4+9) ) Finalayazmustafa100% (1)

- Questions 2021Document7 pagesQuestions 2021Bridgett BeeNo ratings yet

- 2 Prod Assignment 5Document2 pages2 Prod Assignment 5Mohamed GamalNo ratings yet

- TasksDocument30 pagesTaskstungotaku23No ratings yet

- Audit of Property, Plant and EquipmentDocument13 pagesAudit of Property, Plant and EquipmentHijabwear BizNo ratings yet

- Exercise Chap 11Document7 pagesExercise Chap 11JF FNo ratings yet

- Mock - Quiz - Intermediate Accounting IDocument2 pagesMock - Quiz - Intermediate Accounting IАйбар КарабековNo ratings yet

- Chapter 13Document8 pagesChapter 13ks1043210No ratings yet

- 2021 COAF 4201 GroupsDocument16 pages2021 COAF 4201 GroupsTawanda Tatenda HerbertNo ratings yet

- Question 1: Tangible Asset Plant Machinery A B C DDocument7 pagesQuestion 1: Tangible Asset Plant Machinery A B C DTrang TranNo ratings yet

- Share Based PaymentsDocument4 pagesShare Based PaymentsGwyneth TorrefloresNo ratings yet

- DepreciationDocument5 pagesDepreciationAnne EstrellaNo ratings yet

- Bai Tap CMQT clc59Document20 pagesBai Tap CMQT clc59Hải AnhNo ratings yet

- Pset 4Document3 pagesPset 4Ahmed AltohamyNo ratings yet

- Audit of PPE ExercisesDocument3 pagesAudit of PPE ExercisesMARCUAP Flora Mel Joy H.No ratings yet

- (Drills - Ppe) Acc.107Document10 pages(Drills - Ppe) Acc.107Boys ShipperNo ratings yet

- Bridge Course Unit 1 AssignmentDocument2 pagesBridge Course Unit 1 AssignmentSrinidhi SrinivasanNo ratings yet

- Review Questions For B2 C1Document12 pagesReview Questions For B2 C1abuumgweno1803No ratings yet

- Chapter 10: Plant Assets, Natural Resources and Intangibles Important TermsDocument2 pagesChapter 10: Plant Assets, Natural Resources and Intangibles Important TermsMarwan DawoodNo ratings yet

- Assessment TasksDocument5 pagesAssessment TasksLDB Ashley Jeremiah Magsino - ABMNo ratings yet

- Intermediate Accounting 1 Property Plant and EquipmentDocument7 pagesIntermediate Accounting 1 Property Plant and EquipmentKristine Jewel MirandaNo ratings yet

- GEN292 - 2 Prod Assignment 4 2023Document2 pagesGEN292 - 2 Prod Assignment 4 2023Mohamed GamalNo ratings yet

- 2014 December Management Accounting L2Document17 pages2014 December Management Accounting L2Dixie CheeloNo ratings yet

- Bs 320 TodayDocument4 pagesBs 320 TodayPrince Daniels TutorNo ratings yet

- 0126financial and Corporate ReportingDocument6 pages0126financial and Corporate ReportingSmag SmagNo ratings yet

- At 1 January 2020Document6 pagesAt 1 January 2020Carl Yry BitzNo ratings yet

- At 1 January 2020Document6 pagesAt 1 January 2020Carl Yry Bitz100% (1)

- Unit: ACC204 - Advanced Financial Accounting: Weighting: Due Date: 13 October, 2017 InstructionsDocument3 pagesUnit: ACC204 - Advanced Financial Accounting: Weighting: Due Date: 13 October, 2017 InstructionsTina BhambbhwaniNo ratings yet

- TestDocument3 pagesTestMehak AliNo ratings yet

- Movement Schedule of Non-Current AssetsDocument6 pagesMovement Schedule of Non-Current AssetsMichael BwireNo ratings yet

- ACCT 321-Magerial AccountingDocument6 pagesACCT 321-Magerial AccountingNodeh Deh SpartaNo ratings yet

- Ac20 Quiz 4 - DGCDocument8 pagesAc20 Quiz 4 - DGCMaricar PinedaNo ratings yet

- Assignment Conceptual Framework of Finasncial ReportingDocument3 pagesAssignment Conceptual Framework of Finasncial ReportingmutasalinnNo ratings yet

- RELEVANT COST CASES and QuestionsDocument21 pagesRELEVANT COST CASES and QuestionsBijay AgrawalNo ratings yet

- Cold Storage PKMDocument13 pagesCold Storage PKMadityairmNo ratings yet

- 2.4 Dec 04 - QDocument9 pages2.4 Dec 04 - Qomarkhalid3000No ratings yet

- Quiz 1 With Correct AnswersDocument10 pagesQuiz 1 With Correct AnswersmarietorianoNo ratings yet

- Component AccountingDocument2 pagesComponent AccountingtouseefNo ratings yet

- Impairment Sample ExerciseDocument4 pagesImpairment Sample Exerciselet me live in peaceNo ratings yet

- Final Exam Intermediate Accounting 2Document2 pagesFinal Exam Intermediate Accounting 2William TabuenaNo ratings yet

- Principles of Accounting Assignment Date of Submission 24 January 2022Document3 pagesPrinciples of Accounting Assignment Date of Submission 24 January 2022Beast aNo ratings yet

- MQ3 Spr08gDocument10 pagesMQ3 Spr08gjhouvanNo ratings yet

- Situation 8 11Document8 pagesSituation 8 11GuinevereNo ratings yet

- Depreciation CalculationDocument29 pagesDepreciation CalculationRavineahNo ratings yet

- SCMPE 2 Question PaperDocument8 pagesSCMPE 2 Question Paperneha manglaniNo ratings yet

- Project EnggDocument30 pagesProject EnggGamechanger SreenivasanNo ratings yet

- Caf-01 Far-I (Mah SS)Document4 pagesCaf-01 Far-I (Mah SS)Abdullah SaberNo ratings yet

- Pr3 Girls Generation 1m4Document12 pagesPr3 Girls Generation 1m4Althea BañaciaNo ratings yet

- Group Histopath 1Document7 pagesGroup Histopath 1SAMMYNo ratings yet

- The Shanghai Cooperation Organization-1Document2 pagesThe Shanghai Cooperation Organization-1Бегимай Нурланбекова МНКОNo ratings yet

- Sources of Income of Barangay and Different Issues in BarangayDocument12 pagesSources of Income of Barangay and Different Issues in BarangayLyndon G TimpugNo ratings yet

- Database of Questions For The Medical Final Examination (LEK) Bioethics & Medical LawDocument41 pagesDatabase of Questions For The Medical Final Examination (LEK) Bioethics & Medical LawSanan QadirNo ratings yet

- World Data SetDocument2 pagesWorld Data SetJ HerbertNo ratings yet

- Full Download Solutions Manual To Accompany Managerial Accounting Decision Making and Motivating Performance PDF Full ChapterDocument10 pagesFull Download Solutions Manual To Accompany Managerial Accounting Decision Making and Motivating Performance PDF Full Chapterlanioidabsolvejy9g100% (21)

- Chamber of Real Estate and Builders Association, Inc. Vs Secretary of Agrarian ReformDocument2 pagesChamber of Real Estate and Builders Association, Inc. Vs Secretary of Agrarian ReformLawrence Y. CapuchinoNo ratings yet

- UM190159 E Rev1Document196 pagesUM190159 E Rev1Tim PopikNo ratings yet

- 14 Dec - Editorials & Articles by Tarun GroverDocument9 pages14 Dec - Editorials & Articles by Tarun GroverpiyushNo ratings yet

- Description of The Business Target Location:: - Nandan Shudh Dudh PowderDocument5 pagesDescription of The Business Target Location:: - Nandan Shudh Dudh PowderFaisal MohdNo ratings yet

- Partial Withdrawal Form Borang Permohonan Pengeluaran SebahagianDocument2 pagesPartial Withdrawal Form Borang Permohonan Pengeluaran SebahagianSh Shaeza50% (2)

- Candidate Statement - ChicagoDocument2 pagesCandidate Statement - ChicagoAlan GordilloNo ratings yet

- Appeal For Review of Legal Advice From DPPDocument8 pagesAppeal For Review of Legal Advice From DPPDavid Hundeyin100% (2)

- OBLICON TSN Based On Galas Syllabus 2022Document176 pagesOBLICON TSN Based On Galas Syllabus 2022Princess May CabanogNo ratings yet

- RA 7942 (Fiscal Provisions)Document3 pagesRA 7942 (Fiscal Provisions)Kit ChampNo ratings yet

- Mia Lee Ling - English SBA.Document23 pagesMia Lee Ling - English SBA.Mia Lee LingNo ratings yet

- MuniDocument3 pagesMuniaeeacd bescomNo ratings yet

- Fs Idxpropert 2023 05Document3 pagesFs Idxpropert 2023 05ray ramadhaniNo ratings yet

- 2016 AICPA Released Questions REGDocument47 pages2016 AICPA Released Questions REG伊藤カイジNo ratings yet

- Some Basics: Democracy-That Is, The Commonly Accepted Way A Group of People ComeDocument5 pagesSome Basics: Democracy-That Is, The Commonly Accepted Way A Group of People ComeTommy MonteroNo ratings yet

- Elc Debate Hand-InDocument11 pagesElc Debate Hand-Inapi-435087107No ratings yet

- Kyambogo University Faculty of Arts and Social Sciences Semester II Examinations Timetable 2019 2020 Final Copy To Be CopiedDocument12 pagesKyambogo University Faculty of Arts and Social Sciences Semester II Examinations Timetable 2019 2020 Final Copy To Be Copied2300807878No ratings yet

- UNFCCC - United Nations Framework Convention On Climate ChangeDocument6 pagesUNFCCC - United Nations Framework Convention On Climate Changeuday KumarNo ratings yet

- Dumindin, Arnaldo - Benevolent Assimilation - Philippine-American War, 1899-1902Document15 pagesDumindin, Arnaldo - Benevolent Assimilation - Philippine-American War, 1899-1902Julia Mae AlbanoNo ratings yet

- Moodle Lec For Jemaa Topic 2Document4 pagesMoodle Lec For Jemaa Topic 2diona macasaquitNo ratings yet

- PROPERTY WeekDocument19 pagesPROPERTY WeekJerico GodoyNo ratings yet

- Petitioners: Third DivisionDocument9 pagesPetitioners: Third DivisionIsabel HigginsNo ratings yet

Download as pdf or txt

You might also like

- Auditing Theory Test BankDocument31 pagesAuditing Theory Test BankLyza96% (53)

- FR QM - Section B PDFDocument74 pagesFR QM - Section B PDFRishi KumaarNo ratings yet

- PpeDocument7 pagesPpeJasmine Marie Ng CheongNo ratings yet

- AP - Ppe, Int. & Invest PropDocument15 pagesAP - Ppe, Int. & Invest PropJolina ManceraNo ratings yet

- Assignment No 7 - Plant Assets & DepreciationDocument12 pagesAssignment No 7 - Plant Assets & DepreciationRehan Memon67% (3)

- 1A Group 1 To 6 Reporting Legal Techniques and LogicDocument36 pages1A Group 1 To 6 Reporting Legal Techniques and LogicJohnson Yaplin100% (1)

- Exercises Ppe PDFDocument6 pagesExercises Ppe PDFمعن الفاعوري100% (1)

- Acct CH.7 H.W.Document8 pagesAcct CH.7 H.W.j8noelNo ratings yet

- Tangible Non-Current Assets: QuestionsDocument5 pagesTangible Non-Current Assets: QuestionsЕкатерина КидяшеваNo ratings yet

- AIS16Exercises SCDocument6 pagesAIS16Exercises SCSarah GherdaouiNo ratings yet

- Lecture # 21Document4 pagesLecture # 21HussainNo ratings yet

- EXERCISES - PPE, Part 2Document5 pagesEXERCISES - PPE, Part 2Meeka CalimagNo ratings yet

- Problem 30-1 (IAA)Document7 pagesProblem 30-1 (IAA)Quinnie Apuli0% (1)

- Ias 16 Ppe ExerciseDocument12 pagesIas 16 Ppe ExerciseMazni Hanisah75% (4)

- Saad SB (Q (4+9) ) FinalDocument4 pagesSaad SB (Q (4+9) ) Finalayazmustafa100% (1)

- Questions 2021Document7 pagesQuestions 2021Bridgett BeeNo ratings yet

- 2 Prod Assignment 5Document2 pages2 Prod Assignment 5Mohamed GamalNo ratings yet

- TasksDocument30 pagesTaskstungotaku23No ratings yet

- Audit of Property, Plant and EquipmentDocument13 pagesAudit of Property, Plant and EquipmentHijabwear BizNo ratings yet

- Exercise Chap 11Document7 pagesExercise Chap 11JF FNo ratings yet

- Mock - Quiz - Intermediate Accounting IDocument2 pagesMock - Quiz - Intermediate Accounting IАйбар КарабековNo ratings yet

- Chapter 13Document8 pagesChapter 13ks1043210No ratings yet

- 2021 COAF 4201 GroupsDocument16 pages2021 COAF 4201 GroupsTawanda Tatenda HerbertNo ratings yet

- Question 1: Tangible Asset Plant Machinery A B C DDocument7 pagesQuestion 1: Tangible Asset Plant Machinery A B C DTrang TranNo ratings yet

- Share Based PaymentsDocument4 pagesShare Based PaymentsGwyneth TorrefloresNo ratings yet

- DepreciationDocument5 pagesDepreciationAnne EstrellaNo ratings yet

- Bai Tap CMQT clc59Document20 pagesBai Tap CMQT clc59Hải AnhNo ratings yet

- Pset 4Document3 pagesPset 4Ahmed AltohamyNo ratings yet

- Audit of PPE ExercisesDocument3 pagesAudit of PPE ExercisesMARCUAP Flora Mel Joy H.No ratings yet

- (Drills - Ppe) Acc.107Document10 pages(Drills - Ppe) Acc.107Boys ShipperNo ratings yet

- Bridge Course Unit 1 AssignmentDocument2 pagesBridge Course Unit 1 AssignmentSrinidhi SrinivasanNo ratings yet

- Review Questions For B2 C1Document12 pagesReview Questions For B2 C1abuumgweno1803No ratings yet

- Chapter 10: Plant Assets, Natural Resources and Intangibles Important TermsDocument2 pagesChapter 10: Plant Assets, Natural Resources and Intangibles Important TermsMarwan DawoodNo ratings yet

- Assessment TasksDocument5 pagesAssessment TasksLDB Ashley Jeremiah Magsino - ABMNo ratings yet

- Intermediate Accounting 1 Property Plant and EquipmentDocument7 pagesIntermediate Accounting 1 Property Plant and EquipmentKristine Jewel MirandaNo ratings yet

- GEN292 - 2 Prod Assignment 4 2023Document2 pagesGEN292 - 2 Prod Assignment 4 2023Mohamed GamalNo ratings yet

- 2014 December Management Accounting L2Document17 pages2014 December Management Accounting L2Dixie CheeloNo ratings yet

- Bs 320 TodayDocument4 pagesBs 320 TodayPrince Daniels TutorNo ratings yet

- 0126financial and Corporate ReportingDocument6 pages0126financial and Corporate ReportingSmag SmagNo ratings yet

- At 1 January 2020Document6 pagesAt 1 January 2020Carl Yry BitzNo ratings yet

- At 1 January 2020Document6 pagesAt 1 January 2020Carl Yry Bitz100% (1)

- Unit: ACC204 - Advanced Financial Accounting: Weighting: Due Date: 13 October, 2017 InstructionsDocument3 pagesUnit: ACC204 - Advanced Financial Accounting: Weighting: Due Date: 13 October, 2017 InstructionsTina BhambbhwaniNo ratings yet

- TestDocument3 pagesTestMehak AliNo ratings yet

- Movement Schedule of Non-Current AssetsDocument6 pagesMovement Schedule of Non-Current AssetsMichael BwireNo ratings yet

- ACCT 321-Magerial AccountingDocument6 pagesACCT 321-Magerial AccountingNodeh Deh SpartaNo ratings yet

- Ac20 Quiz 4 - DGCDocument8 pagesAc20 Quiz 4 - DGCMaricar PinedaNo ratings yet

- Assignment Conceptual Framework of Finasncial ReportingDocument3 pagesAssignment Conceptual Framework of Finasncial ReportingmutasalinnNo ratings yet

- RELEVANT COST CASES and QuestionsDocument21 pagesRELEVANT COST CASES and QuestionsBijay AgrawalNo ratings yet

- Cold Storage PKMDocument13 pagesCold Storage PKMadityairmNo ratings yet

- 2.4 Dec 04 - QDocument9 pages2.4 Dec 04 - Qomarkhalid3000No ratings yet

- Quiz 1 With Correct AnswersDocument10 pagesQuiz 1 With Correct AnswersmarietorianoNo ratings yet

- Component AccountingDocument2 pagesComponent AccountingtouseefNo ratings yet

- Impairment Sample ExerciseDocument4 pagesImpairment Sample Exerciselet me live in peaceNo ratings yet

- Final Exam Intermediate Accounting 2Document2 pagesFinal Exam Intermediate Accounting 2William TabuenaNo ratings yet

- Principles of Accounting Assignment Date of Submission 24 January 2022Document3 pagesPrinciples of Accounting Assignment Date of Submission 24 January 2022Beast aNo ratings yet

- MQ3 Spr08gDocument10 pagesMQ3 Spr08gjhouvanNo ratings yet

- Situation 8 11Document8 pagesSituation 8 11GuinevereNo ratings yet

- Depreciation CalculationDocument29 pagesDepreciation CalculationRavineahNo ratings yet

- SCMPE 2 Question PaperDocument8 pagesSCMPE 2 Question Paperneha manglaniNo ratings yet

- Project EnggDocument30 pagesProject EnggGamechanger SreenivasanNo ratings yet

- Caf-01 Far-I (Mah SS)Document4 pagesCaf-01 Far-I (Mah SS)Abdullah SaberNo ratings yet

- Pr3 Girls Generation 1m4Document12 pagesPr3 Girls Generation 1m4Althea BañaciaNo ratings yet

- Group Histopath 1Document7 pagesGroup Histopath 1SAMMYNo ratings yet

- The Shanghai Cooperation Organization-1Document2 pagesThe Shanghai Cooperation Organization-1Бегимай Нурланбекова МНКОNo ratings yet

- Sources of Income of Barangay and Different Issues in BarangayDocument12 pagesSources of Income of Barangay and Different Issues in BarangayLyndon G TimpugNo ratings yet

- Database of Questions For The Medical Final Examination (LEK) Bioethics & Medical LawDocument41 pagesDatabase of Questions For The Medical Final Examination (LEK) Bioethics & Medical LawSanan QadirNo ratings yet

- World Data SetDocument2 pagesWorld Data SetJ HerbertNo ratings yet

- Full Download Solutions Manual To Accompany Managerial Accounting Decision Making and Motivating Performance PDF Full ChapterDocument10 pagesFull Download Solutions Manual To Accompany Managerial Accounting Decision Making and Motivating Performance PDF Full Chapterlanioidabsolvejy9g100% (21)

- Chamber of Real Estate and Builders Association, Inc. Vs Secretary of Agrarian ReformDocument2 pagesChamber of Real Estate and Builders Association, Inc. Vs Secretary of Agrarian ReformLawrence Y. CapuchinoNo ratings yet

- UM190159 E Rev1Document196 pagesUM190159 E Rev1Tim PopikNo ratings yet

- 14 Dec - Editorials & Articles by Tarun GroverDocument9 pages14 Dec - Editorials & Articles by Tarun GroverpiyushNo ratings yet

- Description of The Business Target Location:: - Nandan Shudh Dudh PowderDocument5 pagesDescription of The Business Target Location:: - Nandan Shudh Dudh PowderFaisal MohdNo ratings yet

- Partial Withdrawal Form Borang Permohonan Pengeluaran SebahagianDocument2 pagesPartial Withdrawal Form Borang Permohonan Pengeluaran SebahagianSh Shaeza50% (2)

- Candidate Statement - ChicagoDocument2 pagesCandidate Statement - ChicagoAlan GordilloNo ratings yet

- Appeal For Review of Legal Advice From DPPDocument8 pagesAppeal For Review of Legal Advice From DPPDavid Hundeyin100% (2)

- OBLICON TSN Based On Galas Syllabus 2022Document176 pagesOBLICON TSN Based On Galas Syllabus 2022Princess May CabanogNo ratings yet

- RA 7942 (Fiscal Provisions)Document3 pagesRA 7942 (Fiscal Provisions)Kit ChampNo ratings yet

- Mia Lee Ling - English SBA.Document23 pagesMia Lee Ling - English SBA.Mia Lee LingNo ratings yet

- MuniDocument3 pagesMuniaeeacd bescomNo ratings yet

- Fs Idxpropert 2023 05Document3 pagesFs Idxpropert 2023 05ray ramadhaniNo ratings yet

- 2016 AICPA Released Questions REGDocument47 pages2016 AICPA Released Questions REG伊藤カイジNo ratings yet

- Some Basics: Democracy-That Is, The Commonly Accepted Way A Group of People ComeDocument5 pagesSome Basics: Democracy-That Is, The Commonly Accepted Way A Group of People ComeTommy MonteroNo ratings yet

- Elc Debate Hand-InDocument11 pagesElc Debate Hand-Inapi-435087107No ratings yet

- Kyambogo University Faculty of Arts and Social Sciences Semester II Examinations Timetable 2019 2020 Final Copy To Be CopiedDocument12 pagesKyambogo University Faculty of Arts and Social Sciences Semester II Examinations Timetable 2019 2020 Final Copy To Be Copied2300807878No ratings yet

- UNFCCC - United Nations Framework Convention On Climate ChangeDocument6 pagesUNFCCC - United Nations Framework Convention On Climate Changeuday KumarNo ratings yet

- Dumindin, Arnaldo - Benevolent Assimilation - Philippine-American War, 1899-1902Document15 pagesDumindin, Arnaldo - Benevolent Assimilation - Philippine-American War, 1899-1902Julia Mae AlbanoNo ratings yet

- Moodle Lec For Jemaa Topic 2Document4 pagesMoodle Lec For Jemaa Topic 2diona macasaquitNo ratings yet

- PROPERTY WeekDocument19 pagesPROPERTY WeekJerico GodoyNo ratings yet

- Petitioners: Third DivisionDocument9 pagesPetitioners: Third DivisionIsabel HigginsNo ratings yet