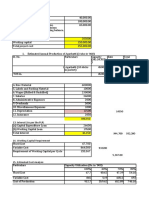

Particulars T U V Y: © The Institute of Chartered Accountants of India

Particulars T U V Y: © The Institute of Chartered Accountants of India

You might also like

- 7166materials Problems-Standard CostingDocument14 pages7166materials Problems-Standard CostingLumina JulieNo ratings yet

- 18-10-SA-V1-S1 Solved Problems SC PDFDocument14 pages18-10-SA-V1-S1 Solved Problems SC PDFAlbsNo ratings yet

- Quality Manual ISO TS 16949 2009Document46 pagesQuality Manual ISO TS 16949 2009spahicdanilo100% (2)

- Management Accounting and Decision Making: Submitted ByDocument12 pagesManagement Accounting and Decision Making: Submitted ByKavisha singhNo ratings yet

- Basic STD CostingDocument5 pagesBasic STD CostingSajidZiaNo ratings yet

- Chapter 12 Standard Costing Nov 2020 2Document112 pagesChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaNo ratings yet

- Textbook of Financial Cost and Management Accounting (PDFDrive) - 642-664 PDFDocument23 pagesTextbook of Financial Cost and Management Accounting (PDFDrive) - 642-664 PDFKola SiriNo ratings yet

- Management Accounting and Decision Making: Cat IiiDocument13 pagesManagement Accounting and Decision Making: Cat IiiKavisha singhNo ratings yet

- Ama Set 40Document6 pagesAma Set 40uroojfatima21299No ratings yet

- P1 Solution CMA JUNE 2020Document5 pagesP1 Solution CMA JUNE 2020Awal ShekNo ratings yet

- Budgeted Statement ExamDocument11 pagesBudgeted Statement ExamNelz KhoNo ratings yet

- TUT 3 - Relevant Information&decision MakingDocument10 pagesTUT 3 - Relevant Information&decision MakingKim Chi LeNo ratings yet

- Bosmtpfinaloldp 5 AnsDocument13 pagesBosmtpfinaloldp 5 AnsharoldpsbNo ratings yet

- 57 Stock BusinessDocument2 pages57 Stock BusinessSandiponNo ratings yet

- Costing Ans 2Document16 pagesCosting Ans 2Shikha SinghNo ratings yet

- Tesr 10 Standard Costing and Variance AnalysisDocument1 pageTesr 10 Standard Costing and Variance AnalysisAnmoul ZahraNo ratings yet

- Management AccountingDocument6 pagesManagement AccountingVerbina BorahNo ratings yet

- Small Scale Industry Tasty BunDocument6 pagesSmall Scale Industry Tasty BunVivek Kumar GuptaNo ratings yet

- Area of Cosquestions PWC: Initial CostDocument18 pagesArea of Cosquestions PWC: Initial CostsarwardbaNo ratings yet

- Part - 2 Costing - 27124255 PDFDocument5 pagesPart - 2 Costing - 27124255 PDFMaharajan GomuNo ratings yet

- 8 Standard CostingDocument10 pages8 Standard CostingLakshay SharmaNo ratings yet

- LU 3 Workbk Solutions 3.1 - 3.4Document4 pagesLU 3 Workbk Solutions 3.1 - 3.4bison3216No ratings yet

- SPK GENAP - Silfina WasrilDocument16 pagesSPK GENAP - Silfina WasrilnanaNo ratings yet

- Cost-Management-Accounting-System 2Document86 pagesCost-Management-Accounting-System 2MollaNo ratings yet

- Board of Studies Academic Chapter 13 Standard Costing Practice Question File 3 1649748588Document29 pagesBoard of Studies Academic Chapter 13 Standard Costing Practice Question File 3 1649748588samueladino876No ratings yet

- Final Test Paper of Standard CostingDocument6 pagesFinal Test Paper of Standard Costingakshaykumarsingh24072005No ratings yet

- Suggested Answers Final Examination - Winter 2014: Management AccounitngDocument5 pagesSuggested Answers Final Examination - Winter 2014: Management AccounitngAbdulAzeemNo ratings yet

- Variance Analysis CW QuestionsDocument14 pagesVariance Analysis CW QuestionsMedhaNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsyanbladeNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsDerrick de los ReyesNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsNeelima Varma NadimpalliNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsAlbsNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsShubham NamdevNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical Problemskiran shettyNo ratings yet

- 18 10 SA V1 S1 Solved Problems SC PDFDocument14 pages18 10 SA V1 S1 Solved Problems SC PDFTheVagabond HarshalNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical Problemsyousuf AhmedNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsAfsahNo ratings yet

- Bab 8 Activity Based CostingDocument25 pagesBab 8 Activity Based CostingsalmaNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsRuchi pariharNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsShruti BannerjeeNo ratings yet

- Agarbatti DPRDocument8 pagesAgarbatti DPRsansiNo ratings yet

- Example 5 FeedbackDocument3 pagesExample 5 FeedbackGrechen UdigengNo ratings yet

- Farm Model of Dairy Unit of 20 Crossbred CowsDocument3 pagesFarm Model of Dairy Unit of 20 Crossbred Cowsbosco100% (1)

- Problem 3 4 Chapter 14Document6 pagesProblem 3 4 Chapter 14freaann03No ratings yet

- Replacement Theory: By-Dr. B. J. MohiteDocument36 pagesReplacement Theory: By-Dr. B. J. MohiteDevaraj AstroNo ratings yet

- Sol Part-2Document209 pagesSol Part-2EmelNo ratings yet

- Part-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)Document33 pagesPart-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)ARIF HUSSAIN AN ENGLISH LECTURER FOR ALL CLASSESNo ratings yet

- EMB 834 Test - Aliyu ObabiOlorunkosi GafaarDocument7 pagesEMB 834 Test - Aliyu ObabiOlorunkosi GafaarAliyu GafaarNo ratings yet

- Standard Costing & Variance AnalysisDocument18 pagesStandard Costing & Variance AnalysisMahesh G VNo ratings yet

- Practical Problems: Fybsc - Semester Ii - Management Accounting - Extra QuestionsDocument4 pagesPractical Problems: Fybsc - Semester Ii - Management Accounting - Extra QuestionsRahul SinghNo ratings yet

- Practice ManualDocument679 pagesPractice ManualSaikrishna AlluNo ratings yet

- Statement - I Cost of Project Particulars Sl. No. Ref. Annex Total CostDocument15 pagesStatement - I Cost of Project Particulars Sl. No. Ref. Annex Total Costsohalsingh1No ratings yet

- Process - Operating CostingDocument3 pagesProcess - Operating CostingShivansh NahataNo ratings yet

- Actual Cost Vs Plan Projection: Your Company NameDocument25 pagesActual Cost Vs Plan Projection: Your Company NameShamsNo ratings yet

- Joint Products and by ProductsDocument27 pagesJoint Products and by ProductsnehaNo ratings yet

- Management Accounting Exams Cedell 1Document7 pagesManagement Accounting Exams Cedell 1Obeng CliffNo ratings yet

- IMAS 2022 Fees ALL CoursesDocument3 pagesIMAS 2022 Fees ALL CoursesCristinaNo ratings yet

- 1643866512121Document3 pages1643866512121S Anjallee KumarNo ratings yet

- Costing - English Answer 23.02.2022Document9 pagesCosting - English Answer 23.02.2022Shubham KuberkarNo ratings yet

- MFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Document9 pagesMFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Mohan sunderNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- MPA703 Management Accounting Semester 2, 2019 AssignmentDocument21 pagesMPA703 Management Accounting Semester 2, 2019 AssignmentrhagitaanggyNo ratings yet

- Rhonda Resume 2009 - 10Document4 pagesRhonda Resume 2009 - 10rhondabitnerNo ratings yet

- Group 2 - 20240422 - 215349 - 0000Document16 pagesGroup 2 - 20240422 - 215349 - 0000forgorontaloNo ratings yet

- Theme 2 HRM & OBDocument394 pagesTheme 2 HRM & OBMilkias MuseNo ratings yet

- Strategic Management 2022-2023Document252 pagesStrategic Management 2022-2023Thảo Thanh100% (1)

- 7 Jo Costing StudentDocument7 pages7 Jo Costing StudentMaria Cristina A. BarrionNo ratings yet

- E17-7-Assessing The Kpi For The Supply ChainDocument4 pagesE17-7-Assessing The Kpi For The Supply ChainAmd BustosNo ratings yet

- Vertical and Horizontal-RelationshipDocument14 pagesVertical and Horizontal-RelationshipUmair AshrafNo ratings yet

- Technical Specification: Iso/Iec TS 17021-5Document6 pagesTechnical Specification: Iso/Iec TS 17021-5Fabrício CavalcanteNo ratings yet

- Accounting and FinanceDocument2 pagesAccounting and FinanceDublin City University, InternationalNo ratings yet

- Chapter One - Introduction To Project-3Document59 pagesChapter One - Introduction To Project-3Mihiret GirmaNo ratings yet

- PESTEL Analysis of Indian Capital MarketDocument4 pagesPESTEL Analysis of Indian Capital MarketRohith50% (2)

- 09 Materials - Controlling, Costing & PlanningDocument20 pages09 Materials - Controlling, Costing & PlanningCloudKielGuiang100% (5)

- Dictionar Termeni Fiabilitate Securitate Calitate, AteDocument55 pagesDictionar Termeni Fiabilitate Securitate Calitate, AtemmanytzaNo ratings yet

- Guardium Fundamentals Level 1 Quiz - Attempt ReviewDocument13 pagesGuardium Fundamentals Level 1 Quiz - Attempt Reviewandzelo88No ratings yet

- Introduction To Logistics ManagementDocument61 pagesIntroduction To Logistics ManagementChâu Anh ĐàoNo ratings yet

- Agility Vs FlexibilityDocument13 pagesAgility Vs FlexibilityDeepakNo ratings yet

- MIS Meaning, Ojective and CharacteristicsDocument10 pagesMIS Meaning, Ojective and CharacteristicsMpangiOmarNo ratings yet

- Evaluating AND Controlling The Performance OF Salespeople: Unit-2Document12 pagesEvaluating AND Controlling The Performance OF Salespeople: Unit-2Mohamed EmaraNo ratings yet

- 1 Executive Summary: 3PL To 4PL Lead Logistics Provider (LLP) Business ModelDocument4 pages1 Executive Summary: 3PL To 4PL Lead Logistics Provider (LLP) Business ModelArora SunnyNo ratings yet

- ERP ReportDocument11 pagesERP ReportZarlish AnumNo ratings yet

- Ankit - Rao Internship Project BBA TYDocument78 pagesAnkit - Rao Internship Project BBA TYYuvraj Tiwari100% (1)

- Finding The Plant Within: The Magazine For Maintenance & Reliability ProfessionalsDocument17 pagesFinding The Plant Within: The Magazine For Maintenance & Reliability ProfessionalsDan MatNo ratings yet

- Course Syllabus/Content Diploma in Quantity SurveyingDocument9 pagesCourse Syllabus/Content Diploma in Quantity SurveyingManoj KumarNo ratings yet

- Case Study HVSDocument3 pagesCase Study HVSDurga ThapaNo ratings yet

- Akhilesh Mewada Sugun Subudhi Ankit Kumar MoonkaDocument22 pagesAkhilesh Mewada Sugun Subudhi Ankit Kumar Moonkasathya priyaNo ratings yet

- What Is A Resilient Supply ChainDocument5 pagesWhat Is A Resilient Supply ChainManel VazquezNo ratings yet

- Europipeline Company Profile 1Document4 pagesEuropipeline Company Profile 1Burhan HandoyoNo ratings yet

- Competency Based InterviewDocument6 pagesCompetency Based Interviewbhupendrasharma00No ratings yet

Download as pdf or txt

You might also like

- 7166materials Problems-Standard CostingDocument14 pages7166materials Problems-Standard CostingLumina JulieNo ratings yet

- 18-10-SA-V1-S1 Solved Problems SC PDFDocument14 pages18-10-SA-V1-S1 Solved Problems SC PDFAlbsNo ratings yet

- Quality Manual ISO TS 16949 2009Document46 pagesQuality Manual ISO TS 16949 2009spahicdanilo100% (2)

- Management Accounting and Decision Making: Submitted ByDocument12 pagesManagement Accounting and Decision Making: Submitted ByKavisha singhNo ratings yet

- Basic STD CostingDocument5 pagesBasic STD CostingSajidZiaNo ratings yet

- Chapter 12 Standard Costing Nov 2020 2Document112 pagesChapter 12 Standard Costing Nov 2020 2Kunal KuvadiaNo ratings yet

- Textbook of Financial Cost and Management Accounting (PDFDrive) - 642-664 PDFDocument23 pagesTextbook of Financial Cost and Management Accounting (PDFDrive) - 642-664 PDFKola SiriNo ratings yet

- Management Accounting and Decision Making: Cat IiiDocument13 pagesManagement Accounting and Decision Making: Cat IiiKavisha singhNo ratings yet

- Ama Set 40Document6 pagesAma Set 40uroojfatima21299No ratings yet

- P1 Solution CMA JUNE 2020Document5 pagesP1 Solution CMA JUNE 2020Awal ShekNo ratings yet

- Budgeted Statement ExamDocument11 pagesBudgeted Statement ExamNelz KhoNo ratings yet

- TUT 3 - Relevant Information&decision MakingDocument10 pagesTUT 3 - Relevant Information&decision MakingKim Chi LeNo ratings yet

- Bosmtpfinaloldp 5 AnsDocument13 pagesBosmtpfinaloldp 5 AnsharoldpsbNo ratings yet

- 57 Stock BusinessDocument2 pages57 Stock BusinessSandiponNo ratings yet

- Costing Ans 2Document16 pagesCosting Ans 2Shikha SinghNo ratings yet

- Tesr 10 Standard Costing and Variance AnalysisDocument1 pageTesr 10 Standard Costing and Variance AnalysisAnmoul ZahraNo ratings yet

- Management AccountingDocument6 pagesManagement AccountingVerbina BorahNo ratings yet

- Small Scale Industry Tasty BunDocument6 pagesSmall Scale Industry Tasty BunVivek Kumar GuptaNo ratings yet

- Area of Cosquestions PWC: Initial CostDocument18 pagesArea of Cosquestions PWC: Initial CostsarwardbaNo ratings yet

- Part - 2 Costing - 27124255 PDFDocument5 pagesPart - 2 Costing - 27124255 PDFMaharajan GomuNo ratings yet

- 8 Standard CostingDocument10 pages8 Standard CostingLakshay SharmaNo ratings yet

- LU 3 Workbk Solutions 3.1 - 3.4Document4 pagesLU 3 Workbk Solutions 3.1 - 3.4bison3216No ratings yet

- SPK GENAP - Silfina WasrilDocument16 pagesSPK GENAP - Silfina WasrilnanaNo ratings yet

- Cost-Management-Accounting-System 2Document86 pagesCost-Management-Accounting-System 2MollaNo ratings yet

- Board of Studies Academic Chapter 13 Standard Costing Practice Question File 3 1649748588Document29 pagesBoard of Studies Academic Chapter 13 Standard Costing Practice Question File 3 1649748588samueladino876No ratings yet

- Final Test Paper of Standard CostingDocument6 pagesFinal Test Paper of Standard Costingakshaykumarsingh24072005No ratings yet

- Suggested Answers Final Examination - Winter 2014: Management AccounitngDocument5 pagesSuggested Answers Final Examination - Winter 2014: Management AccounitngAbdulAzeemNo ratings yet

- Variance Analysis CW QuestionsDocument14 pagesVariance Analysis CW QuestionsMedhaNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsyanbladeNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsDerrick de los ReyesNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsNeelima Varma NadimpalliNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsAlbsNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsShubham NamdevNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical Problemskiran shettyNo ratings yet

- 18 10 SA V1 S1 Solved Problems SC PDFDocument14 pages18 10 SA V1 S1 Solved Problems SC PDFTheVagabond HarshalNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical Problemsyousuf AhmedNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsAfsahNo ratings yet

- Bab 8 Activity Based CostingDocument25 pagesBab 8 Activity Based CostingsalmaNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsRuchi pariharNo ratings yet

- Unit 6 Module 10 Standard Costing: Practical ProblemsDocument14 pagesUnit 6 Module 10 Standard Costing: Practical ProblemsShruti BannerjeeNo ratings yet

- Agarbatti DPRDocument8 pagesAgarbatti DPRsansiNo ratings yet

- Example 5 FeedbackDocument3 pagesExample 5 FeedbackGrechen UdigengNo ratings yet

- Farm Model of Dairy Unit of 20 Crossbred CowsDocument3 pagesFarm Model of Dairy Unit of 20 Crossbred Cowsbosco100% (1)

- Problem 3 4 Chapter 14Document6 pagesProblem 3 4 Chapter 14freaann03No ratings yet

- Replacement Theory: By-Dr. B. J. MohiteDocument36 pagesReplacement Theory: By-Dr. B. J. MohiteDevaraj AstroNo ratings yet

- Sol Part-2Document209 pagesSol Part-2EmelNo ratings yet

- Part-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)Document33 pagesPart-A - Strategic Management Accounting: Multiple Choice Questions (MCQS)ARIF HUSSAIN AN ENGLISH LECTURER FOR ALL CLASSESNo ratings yet

- EMB 834 Test - Aliyu ObabiOlorunkosi GafaarDocument7 pagesEMB 834 Test - Aliyu ObabiOlorunkosi GafaarAliyu GafaarNo ratings yet

- Standard Costing & Variance AnalysisDocument18 pagesStandard Costing & Variance AnalysisMahesh G VNo ratings yet

- Practical Problems: Fybsc - Semester Ii - Management Accounting - Extra QuestionsDocument4 pagesPractical Problems: Fybsc - Semester Ii - Management Accounting - Extra QuestionsRahul SinghNo ratings yet

- Practice ManualDocument679 pagesPractice ManualSaikrishna AlluNo ratings yet

- Statement - I Cost of Project Particulars Sl. No. Ref. Annex Total CostDocument15 pagesStatement - I Cost of Project Particulars Sl. No. Ref. Annex Total Costsohalsingh1No ratings yet

- Process - Operating CostingDocument3 pagesProcess - Operating CostingShivansh NahataNo ratings yet

- Actual Cost Vs Plan Projection: Your Company NameDocument25 pagesActual Cost Vs Plan Projection: Your Company NameShamsNo ratings yet

- Joint Products and by ProductsDocument27 pagesJoint Products and by ProductsnehaNo ratings yet

- Management Accounting Exams Cedell 1Document7 pagesManagement Accounting Exams Cedell 1Obeng CliffNo ratings yet

- IMAS 2022 Fees ALL CoursesDocument3 pagesIMAS 2022 Fees ALL CoursesCristinaNo ratings yet

- 1643866512121Document3 pages1643866512121S Anjallee KumarNo ratings yet

- Costing - English Answer 23.02.2022Document9 pagesCosting - English Answer 23.02.2022Shubham KuberkarNo ratings yet

- MFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Document9 pagesMFA - Assignment 2: Management and Financial Accounting - Individual Assignment 2Mohan sunderNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- MPA703 Management Accounting Semester 2, 2019 AssignmentDocument21 pagesMPA703 Management Accounting Semester 2, 2019 AssignmentrhagitaanggyNo ratings yet

- Rhonda Resume 2009 - 10Document4 pagesRhonda Resume 2009 - 10rhondabitnerNo ratings yet

- Group 2 - 20240422 - 215349 - 0000Document16 pagesGroup 2 - 20240422 - 215349 - 0000forgorontaloNo ratings yet

- Theme 2 HRM & OBDocument394 pagesTheme 2 HRM & OBMilkias MuseNo ratings yet

- Strategic Management 2022-2023Document252 pagesStrategic Management 2022-2023Thảo Thanh100% (1)

- 7 Jo Costing StudentDocument7 pages7 Jo Costing StudentMaria Cristina A. BarrionNo ratings yet

- E17-7-Assessing The Kpi For The Supply ChainDocument4 pagesE17-7-Assessing The Kpi For The Supply ChainAmd BustosNo ratings yet

- Vertical and Horizontal-RelationshipDocument14 pagesVertical and Horizontal-RelationshipUmair AshrafNo ratings yet

- Technical Specification: Iso/Iec TS 17021-5Document6 pagesTechnical Specification: Iso/Iec TS 17021-5Fabrício CavalcanteNo ratings yet

- Accounting and FinanceDocument2 pagesAccounting and FinanceDublin City University, InternationalNo ratings yet

- Chapter One - Introduction To Project-3Document59 pagesChapter One - Introduction To Project-3Mihiret GirmaNo ratings yet

- PESTEL Analysis of Indian Capital MarketDocument4 pagesPESTEL Analysis of Indian Capital MarketRohith50% (2)

- 09 Materials - Controlling, Costing & PlanningDocument20 pages09 Materials - Controlling, Costing & PlanningCloudKielGuiang100% (5)

- Dictionar Termeni Fiabilitate Securitate Calitate, AteDocument55 pagesDictionar Termeni Fiabilitate Securitate Calitate, AtemmanytzaNo ratings yet

- Guardium Fundamentals Level 1 Quiz - Attempt ReviewDocument13 pagesGuardium Fundamentals Level 1 Quiz - Attempt Reviewandzelo88No ratings yet

- Introduction To Logistics ManagementDocument61 pagesIntroduction To Logistics ManagementChâu Anh ĐàoNo ratings yet

- Agility Vs FlexibilityDocument13 pagesAgility Vs FlexibilityDeepakNo ratings yet

- MIS Meaning, Ojective and CharacteristicsDocument10 pagesMIS Meaning, Ojective and CharacteristicsMpangiOmarNo ratings yet

- Evaluating AND Controlling The Performance OF Salespeople: Unit-2Document12 pagesEvaluating AND Controlling The Performance OF Salespeople: Unit-2Mohamed EmaraNo ratings yet

- 1 Executive Summary: 3PL To 4PL Lead Logistics Provider (LLP) Business ModelDocument4 pages1 Executive Summary: 3PL To 4PL Lead Logistics Provider (LLP) Business ModelArora SunnyNo ratings yet

- ERP ReportDocument11 pagesERP ReportZarlish AnumNo ratings yet

- Ankit - Rao Internship Project BBA TYDocument78 pagesAnkit - Rao Internship Project BBA TYYuvraj Tiwari100% (1)

- Finding The Plant Within: The Magazine For Maintenance & Reliability ProfessionalsDocument17 pagesFinding The Plant Within: The Magazine For Maintenance & Reliability ProfessionalsDan MatNo ratings yet

- Course Syllabus/Content Diploma in Quantity SurveyingDocument9 pagesCourse Syllabus/Content Diploma in Quantity SurveyingManoj KumarNo ratings yet

- Case Study HVSDocument3 pagesCase Study HVSDurga ThapaNo ratings yet

- Akhilesh Mewada Sugun Subudhi Ankit Kumar MoonkaDocument22 pagesAkhilesh Mewada Sugun Subudhi Ankit Kumar Moonkasathya priyaNo ratings yet

- What Is A Resilient Supply ChainDocument5 pagesWhat Is A Resilient Supply ChainManel VazquezNo ratings yet

- Europipeline Company Profile 1Document4 pagesEuropipeline Company Profile 1Burhan HandoyoNo ratings yet

- Competency Based InterviewDocument6 pagesCompetency Based Interviewbhupendrasharma00No ratings yet