Download as pdf or txt

You might also like

- Argus Oil Market Discussions: LPGDocument42 pagesArgus Oil Market Discussions: LPGALI ABBASNo ratings yet

- Platt 2018Document15 pagesPlatt 2018Haseen AslamNo ratings yet

- Platts Du 04 Août 2017Document19 pagesPlatts Du 04 Août 2017Wallace Yankoty100% (1)

- Asia-Pacific/Arab Gulf Marketscan: Volume 39 / Issue 71 / April 13, 2020Document23 pagesAsia-Pacific/Arab Gulf Marketscan: Volume 39 / Issue 71 / April 13, 2020Donnie HavierNo ratings yet

- Competitive Study - NexantDocument12 pagesCompetitive Study - NexantHarpreet SinghNo ratings yet

- Copper 2010 ProgramDocument44 pagesCopper 2010 ProgramCecilia Iter100% (1)

- 1.4advanced Financial ManagementDocument206 pages1.4advanced Financial Managementsolstice56756750% (2)

- Dividend Policy and Internal FinancingDocument14 pagesDividend Policy and Internal FinancingMichaela San Diego0% (1)

- Rate AnalysisDocument4 pagesRate Analysisnagaraj_qce3499100% (1)

- LME Monthly Overview July 2021Document26 pagesLME Monthly Overview July 2021JONATHAN D. R. LNo ratings yet

- Argus COA Sample Report Coal (2021!01!19)Document16 pagesArgus COA Sample Report Coal (2021!01!19)郭建麟No ratings yet

- Coal Trader International: Asian Thermal Coal Prices Edge Lower On Demand Pullback From China BuyersDocument17 pagesCoal Trader International: Asian Thermal Coal Prices Edge Lower On Demand Pullback From China BuyersClief SurentuNo ratings yet

- Crude Oil Methodology PDFDocument50 pagesCrude Oil Methodology PDFsolarstuffNo ratings yet

- Crude Oil Methodology and Specifications GuideDocument35 pagesCrude Oil Methodology and Specifications GuideJustyna LipskaNo ratings yet

- Moodys Approach To Rating The Petroleum Industry PDFDocument32 pagesMoodys Approach To Rating The Petroleum Industry PDFMujtabaNo ratings yet

- HSFO ReportDocument17 pagesHSFO ReportAtif IqbalNo ratings yet

- Argus Green Ammonia Strategy Report - SampleDocument14 pagesArgus Green Ammonia Strategy Report - Samplerriveram1299No ratings yet

- EuropeLPGReport Sample02082013Document5 pagesEuropeLPGReport Sample02082013Melody CottonNo ratings yet

- Argus-Sulphuric-Acid PriceDocument9 pagesArgus-Sulphuric-Acid PricesharemwNo ratings yet

- Platts APAG Report 01 09 2015 PDFDocument14 pagesPlatts APAG Report 01 09 2015 PDFSafri IchsanNo ratings yet

- Coal Trader International: Glencore Limiting Coal Output Seen Boosting Fob Newcastle PricesDocument11 pagesCoal Trader International: Glencore Limiting Coal Output Seen Boosting Fob Newcastle PricesI Gede Artha Wijaya100% (1)

- Estimation Showing For Existing Commercial Building RoomDocument1 pageEstimation Showing For Existing Commercial Building RoomDileep Kumar Chintada100% (1)

- PLATTS Crude 20190809Document24 pagesPLATTS Crude 20190809Huixin dong100% (1)

- Cable 2007 IeemaDocument26 pagesCable 2007 Ieemagmat187No ratings yet

- NORTE AMERICA Argus Fertilizer North America Map 2019Document1 pageNORTE AMERICA Argus Fertilizer North America Map 2019rubenpeNo ratings yet

- Rystad Energy Commentary - 3539361 - Australasia 2020 ReviewDocument9 pagesRystad Energy Commentary - 3539361 - Australasia 2020 ReviewRaam WilliamsNo ratings yet

- Ev ThreadDocument1 pageEv ThreadGurjeevAnandNo ratings yet

- CTRM Briefing Note - ENVERUS Trading & RiskDocument2 pagesCTRM Briefing Note - ENVERUS Trading & RiskCTRM CenterNo ratings yet

- Crude Oil MKT WireDocument23 pagesCrude Oil MKT WireAdi SutrisnoNo ratings yet

- PowderRiverBasin Type LogDocument1 pagePowderRiverBasin Type LogPeter Scribd BNo ratings yet

- Advanced Engineering Mathematics With MatlabDocument15 pagesAdvanced Engineering Mathematics With MatlabFauzi MahdyNo ratings yet

- European Marketscan: European Products ($/MT) ICE FuturesDocument10 pagesEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyNo ratings yet

- JSW Steel Ar Full Report 2018-19 12-35Document886 pagesJSW Steel Ar Full Report 2018-19 12-35Rusheel ChavaNo ratings yet

- 06 August 2021 - Coal Market UpdateDocument22 pages06 August 2021 - Coal Market UpdateAlexis Louisse GonzalesNo ratings yet

- Eum 20100401Document8 pagesEum 20100401Anto BejićNo ratings yet

- A Framework of Supply Chain Management LiteratureDocument10 pagesA Framework of Supply Chain Management LiteratureyrperdanaNo ratings yet

- Us 2022 Outlook Oil and GasDocument11 pagesUs 2022 Outlook Oil and GasChib DavidNo ratings yet

- Flexible Electronics: Presented by Ashwin.k 4SN14EC704Document16 pagesFlexible Electronics: Presented by Ashwin.k 4SN14EC704Aswin PrEmrajNo ratings yet

- Analysis of Steel Procurement - FinalDocument23 pagesAnalysis of Steel Procurement - FinalSuvankarNo ratings yet

- Tipos de Tratamientos PDFDocument1 pageTipos de Tratamientos PDFJose PerezNo ratings yet

- Procurement Practices at Tata SteelDocument7 pagesProcurement Practices at Tata SteelPriyanka SinghNo ratings yet

- Methods of CostingDocument21 pagesMethods of CostingsweetashusNo ratings yet

- Steel and Pipes For Africa Price ListDocument1 pageSteel and Pipes For Africa Price ListLazuardhy Vozika Futur100% (1)

- BRS Cost Estimate Summary Feb BallotDocument7 pagesBRS Cost Estimate Summary Feb Ballottfaber2933No ratings yet

- Commercial VehicleDocument12 pagesCommercial VehicleAsif ShaikhNo ratings yet

- Stainless Steel PricelistDocument28 pagesStainless Steel Pricelistmanish422No ratings yet

- APAC Report Issue 234 Mid-August 2023Document23 pagesAPAC Report Issue 234 Mid-August 2023Mohammad AnnasNo ratings yet

- Contract TERMSDocument63 pagesContract TERMSnobo_dhakaNo ratings yet

- Jindal Star Pipes PricelistDocument3 pagesJindal Star Pipes Pricelistgautam guptaNo ratings yet

- Pump TemplateDocument2 pagesPump TemplateamitkrayNo ratings yet

- LME Monthly Overview Report August 2022Document26 pagesLME Monthly Overview Report August 2022Omer MohaideenNo ratings yet

- Liter Tank DetailDocument281 pagesLiter Tank DetailrkpragadeeshNo ratings yet

- Costing Final MindmapDocument1 pageCosting Final MindmapbetsyNo ratings yet

- Coal Trader InternationalDocument18 pagesCoal Trader InternationalI Gede Artha WijayaNo ratings yet

- Inventory TemplateDocument25 pagesInventory TemplatefaxoxNo ratings yet

- BreakdownDocument1 pageBreakdownFrank SantNo ratings yet

- Npi Cdo - Cost MatrixDocument21 pagesNpi Cdo - Cost MatrixGreen AvatarNo ratings yet

- CRU NickelDocument10 pagesCRU NickelDavid Budi SaputraNo ratings yet

- VALE International - Oman Sohar Project PPT MckinseyDocument19 pagesVALE International - Oman Sohar Project PPT MckinseyAmit Ghosh100% (1)

- 7th China Nickel Conference May 2010Document32 pages7th China Nickel Conference May 2010nileshscorpionNo ratings yet

- BIMBSec Corp Day - 2022 OG OutlookDocument9 pagesBIMBSec Corp Day - 2022 OG Outlookmuhammad ihsanNo ratings yet

- Incomes & Home Price (In Oz Au)Document2 pagesIncomes & Home Price (In Oz Au)kettle1No ratings yet

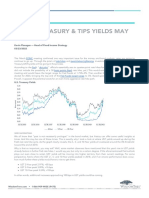

- 5 Key Factors Facing U.S. Treasury Yields - Seeking AlphaDocument12 pages5 Key Factors Facing U.S. Treasury Yields - Seeking AlphaOwm Close CorporationNo ratings yet

- Blog - The WisdomTree Q2 2022 Economic and Market Outlook in 10 Charts or LessDocument11 pagesBlog - The WisdomTree Q2 2022 Economic and Market Outlook in 10 Charts or LessOwm Close CorporationNo ratings yet

- Fed Hikes 50bp With Much More To Come: Economic and Financial AnalysisDocument5 pagesFed Hikes 50bp With Much More To Come: Economic and Financial AnalysisOwm Close CorporationNo ratings yet

- The Flip Side of Large M&A DealsDocument6 pagesThe Flip Side of Large M&A DealsOwm Close CorporationNo ratings yet

- Lithium Exploration Budgets Rebounded in 2021 and Increased 25% Year Over Year To $249 MillionDocument3 pagesLithium Exploration Budgets Rebounded in 2021 and Increased 25% Year Over Year To $249 MillionOwm Close CorporationNo ratings yet

- Gmo Resources Strategy: FactsDocument2 pagesGmo Resources Strategy: FactsOwm Close CorporationNo ratings yet

- ING Think Rates Spark Inflation Reasserts Itself As The Main Driver of Rates 2Document5 pagesING Think Rates Spark Inflation Reasserts Itself As The Main Driver of Rates 2Owm Close CorporationNo ratings yet

- Invasion Effect On PGMS: Base Case Unchanged, But Upside Price RiskDocument4 pagesInvasion Effect On PGMS: Base Case Unchanged, But Upside Price RiskOwm Close CorporationNo ratings yet

- ING Think Us Housing Market Exhibits More Signs of SlowdownDocument6 pagesING Think Us Housing Market Exhibits More Signs of SlowdownOwm Close CorporationNo ratings yet

- ING Think Japanese Investors Turn Cautious On Sovereign Bonds Ahead of Global QTDocument4 pagesING Think Japanese Investors Turn Cautious On Sovereign Bonds Ahead of Global QTOwm Close CorporationNo ratings yet

- Blog - Fed Watch Nifty FiftyDocument3 pagesBlog - Fed Watch Nifty FiftyOwm Close CorporationNo ratings yet

- ING Think Aluminium Caught Up in Nickels Wild RideDocument4 pagesING Think Aluminium Caught Up in Nickels Wild RideOwm Close CorporationNo ratings yet

- En - 20220322 Award of Epcm Contract To AfryDocument4 pagesEn - 20220322 Award of Epcm Contract To AfryOwm Close CorporationNo ratings yet

- An Impressive Start To The Year For Nickel As It Hits 10-Year HighDocument7 pagesAn Impressive Start To The Year For Nickel As It Hits 10-Year HighOwm Close CorporationNo ratings yet

- ING Think The Impact of The War in Ukraine On Food Agri Has Only Just Started To UnravelDocument7 pagesING Think The Impact of The War in Ukraine On Food Agri Has Only Just Started To UnravelOwm Close CorporationNo ratings yet

- Horizonte Furnace - 20220225-Award-Of-Furnace-ContractDocument4 pagesHorizonte Furnace - 20220225-Award-Of-Furnace-ContractOwm Close CorporationNo ratings yet

- ING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerDocument6 pagesING Think Why Us Secs Proposed Climate Disclosure Rules Are A Game ChangerOwm Close CorporationNo ratings yet

- Blog - Where Treasury TIPS Yields May Be HeadedDocument5 pagesBlog - Where Treasury TIPS Yields May Be HeadedOwm Close CorporationNo ratings yet

- Rate Shock Pandemic Spreading - Juggling DynamiteDocument3 pagesRate Shock Pandemic Spreading - Juggling DynamiteOwm Close CorporationNo ratings yet

- News Release: Red Chris Block Cave Pre-Feasibility Study Confirms Low Cost, Long LifeDocument5 pagesNews Release: Red Chris Block Cave Pre-Feasibility Study Confirms Low Cost, Long LifeOwm Close CorporationNo ratings yet

- Nomad Royalty Company Acquires $75 Million Gold Stream On Ivanhoe Mines' Platreef PGM ProjectDocument6 pagesNomad Royalty Company Acquires $75 Million Gold Stream On Ivanhoe Mines' Platreef PGM ProjectOwm Close CorporationNo ratings yet

- ASX Release: Karouni Plant Site Where Construction Commenced in February 2015Document6 pagesASX Release: Karouni Plant Site Where Construction Commenced in February 2015Owm Close CorporationNo ratings yet

- RBPlat Vs Northam BidDocument2 pagesRBPlat Vs Northam BidOwm Close CorporationNo ratings yet

- Presidential Opening of The Aktogay Expansion Project FinalDocument1 pagePresidential Opening of The Aktogay Expansion Project FinalOwm Close CorporationNo ratings yet

- Defective Rule 43 Application - Family LawDocument5 pagesDefective Rule 43 Application - Family LawOwm Close CorporationNo ratings yet

- Acquisition of Ferronickel Processing EquipmentDocument4 pagesAcquisition of Ferronickel Processing EquipmentOwm Close CorporationNo ratings yet

- ING Think Latam FX Outlook 2022 Return of The Pink TideDocument5 pagesING Think Latam FX Outlook 2022 Return of The Pink TideOwm Close CorporationNo ratings yet

- Internship ReportDocument80 pagesInternship ReportAhmed Imran KabirNo ratings yet

- Financial Accounting 4th Edition Spiceland Test Bank 1Document187 pagesFinancial Accounting 4th Edition Spiceland Test Bank 1barbara100% (53)

- Fidic Conditions of Contract As A Model For An International Construction ContractDocument19 pagesFidic Conditions of Contract As A Model For An International Construction Contractazamislam726537No ratings yet

- Muhammad Adeel - Asstt MGR AuditDocument4 pagesMuhammad Adeel - Asstt MGR AuditcdeekyNo ratings yet

- ch9 Solutions PDFDocument38 pagesch9 Solutions PDFHussnain NaneNo ratings yet

- Innovative Climate and Disaster Risk Finance Solutions Resilience Building and Fiscal StrengtheningDocument26 pagesInnovative Climate and Disaster Risk Finance Solutions Resilience Building and Fiscal StrengtheningcarlosNo ratings yet

- Manangement AccountingDocument10 pagesManangement AccountingIshpreet Singh BaggaNo ratings yet

- Small Medium EnterpriseDocument45 pagesSmall Medium EnterpriseSahil MehtaNo ratings yet

- Nielsen VN - Personal Finance Monitor Mid-Year 2010Document42 pagesNielsen VN - Personal Finance Monitor Mid-Year 2010OscarKhuongNo ratings yet

- Balance Sheet As Per New Schedule ViDocument11 pagesBalance Sheet As Per New Schedule ViVelayudham ThiyagarajanNo ratings yet

- Business Plan: Wrexham Football Club & Associated AssetsDocument4 pagesBusiness Plan: Wrexham Football Club & Associated AssetsPedro Secol PanzelliNo ratings yet

- A 17 QuizDocument5 pagesA 17 QuizLei0% (1)

- A Group GameDocument41 pagesA Group GameHenryNo ratings yet

- Business Valuation1Document288 pagesBusiness Valuation1Kapil Bhopatkar100% (1)

- Income Taxation SchemesDocument12 pagesIncome Taxation SchemesargelenNo ratings yet

- Company ProfileDocument9 pagesCompany Profilemohamed mustafaNo ratings yet

- Job Description: To Be The Preferred Provider of Contract Mining ServiceDocument8 pagesJob Description: To Be The Preferred Provider of Contract Mining Servicepamungkas23No ratings yet

- United Food Pakistan Balance Sheet For The Year 2011 To 2020Document34 pagesUnited Food Pakistan Balance Sheet For The Year 2011 To 2020tech& GamingNo ratings yet

- Daimler Q1 2011 Roadshow PresentationDocument84 pagesDaimler Q1 2011 Roadshow Presentationvihangnaik_2007No ratings yet

- Qualified EntitiesDocument44 pagesQualified Entitiesdora tavarezNo ratings yet

- Developing A Housing Microfinance Product - The First Microfinance Banks Experience in AfghanistanDocument32 pagesDeveloping A Housing Microfinance Product - The First Microfinance Banks Experience in AfghanistanBhagyanath MenonNo ratings yet

- Graycliff Exploration Ltd. (CSE:GRAY) - As You Like It: Exploring For High-Grade Au Near SudburyDocument14 pagesGraycliff Exploration Ltd. (CSE:GRAY) - As You Like It: Exploring For High-Grade Au Near SudburyJames HudsonNo ratings yet

- Nigerian Flour Milling Industry Research Report by Lead CapitalDocument13 pagesNigerian Flour Milling Industry Research Report by Lead Capitalexceptionalhighdee100% (1)

- MedicalimDocument1 pageMedicalimsaurabhNo ratings yet

- Engineering Mathematics Engineering Economics and SciencesDocument3 pagesEngineering Mathematics Engineering Economics and SciencesElla Grace Galang100% (1)

- MR MarketDocument64 pagesMR MarketRaymondTuskNo ratings yet

- Intertek Group Annual Report and Accounts 2016 Corporate Governance Compliance StatusDocument23 pagesIntertek Group Annual Report and Accounts 2016 Corporate Governance Compliance StatusProkopNo ratings yet

- FM FinalDocument87 pagesFM FinalGaurav S JadhavNo ratings yet