Download as pdf or txt

You might also like

- Orix Geoscience Scaling Up Employee EngagementDocument10 pagesOrix Geoscience Scaling Up Employee EngagementGabriela Ojeda RebazaNo ratings yet

- Bose-Grp9Document13 pagesBose-Grp9tarun778750% (2)

- BAFS 2020-2025 Strategic Plan - 12.15Document111 pagesBAFS 2020-2025 Strategic Plan - 12.15John Vincent Valencia100% (2)

- CASE STUDY #1 ALMA ELECTRONICS: I'll Dream of YouDocument3 pagesCASE STUDY #1 ALMA ELECTRONICS: I'll Dream of YouGlenda Candedeir79% (14)

- Construction Non DoctronialDocument7 pagesConstruction Non Doctronialankur vikasNo ratings yet

- Wa0021.Document10 pagesWa0021.SnekaNo ratings yet

- Impact of GST Law On Real EstateDocument14 pagesImpact of GST Law On Real EstateHumanyu KabeerNo ratings yet

- GST On Real Estate Converted 1Document4 pagesGST On Real Estate Converted 1jvnraoNo ratings yet

- Research Methodology ProjectDocument19 pagesResearch Methodology Projectswapnil_022No ratings yet

- Decision Taken by GST Council - 34th MeetingDocument3 pagesDecision Taken by GST Council - 34th MeetingLakshmi PriyaNo ratings yet

- Vat Construction Real Estate 201301 v2Document20 pagesVat Construction Real Estate 201301 v2sankuj5354No ratings yet

- Real Estae Project (REP)Document6 pagesReal Estae Project (REP)dinesh kasnNo ratings yet

- GST Lon Landowner ShareDocument6 pagesGST Lon Landowner ShareJigmeNo ratings yet

- 34th GST CouncilDocument3 pages34th GST CouncilYashwanth PrasadNo ratings yet

- GST Real Estate SectorDocument66 pagesGST Real Estate SectorSelvakumar MuthurajNo ratings yet

- Handbook GST Real EstateDocument92 pagesHandbook GST Real EstateABC 123No ratings yet

- Taxability of Real Estate Transactions Under GST: Particulars Applicability Rate of TaxDocument5 pagesTaxability of Real Estate Transactions Under GST: Particulars Applicability Rate of Taxnastaeenbaig1No ratings yet

- Impact of GST On Real Estate SectorDocument22 pagesImpact of GST On Real Estate SectorjunaidNo ratings yet

- Impact of GST On Construction CompaniesDocument66 pagesImpact of GST On Construction CompaniesChandan Srivastava100% (6)

- Gst-Sem ViDocument61 pagesGst-Sem ViSOURAV SHARMANo ratings yet

- Central Taxes Replaced by GSTDocument6 pagesCentral Taxes Replaced by GSTBijosh ThomasNo ratings yet

- Effect of RERA & GST On Real Estate IndustryDocument14 pagesEffect of RERA & GST On Real Estate IndustrySakshee BhaiswarNo ratings yet

- TDS On Real Estate IndustryDocument5 pagesTDS On Real Estate IndustryKirti SanghaviNo ratings yet

- GST On Redevelopment Projects - Taxguru - inDocument4 pagesGST On Redevelopment Projects - Taxguru - inTejas SodhaNo ratings yet

- GST Issues Real Estate Sector Yashwant KasarDocument49 pagesGST Issues Real Estate Sector Yashwant KasarSaikrishna AlluNo ratings yet

- Influence of GSTDocument3 pagesInfluence of GSTarvindNo ratings yet

- FAQ (II) Real Estate Sector 1405Document9 pagesFAQ (II) Real Estate Sector 1405raj pandeyNo ratings yet

- GST On Real Estate SectorDocument30 pagesGST On Real Estate SectorRajanNo ratings yet

- taxguru.in-GST शासतर Joint Development Agreement Taxability other aspectsDocument6 pagestaxguru.in-GST शासतर Joint Development Agreement Taxability other aspectsinspira buildersNo ratings yet

- GST On Real EstateDocument37 pagesGST On Real EstateRupali GuptaNo ratings yet

- Overview of Realestate Industry in IndiaDocument32 pagesOverview of Realestate Industry in IndiaPritam AnantaNo ratings yet

- GSTDocument19 pagesGSTPRANAV GOSWAMINo ratings yet

- Consumer Perception Towards Supertech Limited Devyanshi 14 SecDocument85 pagesConsumer Perception Towards Supertech Limited Devyanshi 14 SecShobhit GoswamiNo ratings yet

- Faq¬e (28 08 12) PDFDocument16 pagesFaq¬e (28 08 12) PDFYogesh KamalapureNo ratings yet

- GST Cheque Return LetterDocument6 pagesGST Cheque Return Letterz2824No ratings yet

- GST Housing Sector Affordable HousingDocument3 pagesGST Housing Sector Affordable HousingschaktenNo ratings yet

- RealEstate Construction PoV 2014Document8 pagesRealEstate Construction PoV 2014Manish KumarNo ratings yet

- GST Cheque Return LetterDocument5 pagesGST Cheque Return Letterz2824No ratings yet

- Project ReportDocument42 pagesProject ReportRahul KumarNo ratings yet

- Horizon Real EstateDocument72 pagesHorizon Real EstateShobhit GoswamiNo ratings yet

- GST To Present Realty With RealityDocument3 pagesGST To Present Realty With RealityHarday GuptaNo ratings yet

- Amendment Final N2020 BGSirDocument30 pagesAmendment Final N2020 BGSirAfnan KhanNo ratings yet

- Budget 2012: What's in It For The Real Estate SectorDocument4 pagesBudget 2012: What's in It For The Real Estate SectorsimmishwetaNo ratings yet

- Changes in GSTDocument4 pagesChanges in GSTRanjodh KaurNo ratings yet

- Rajni (1957)Document37 pagesRajni (1957)PAL GENERAL STORE SHERPURNo ratings yet

- Horizon Real EstateDocument71 pagesHorizon Real EstateAshutoshSharmaNo ratings yet

- Goods and Service TaxDocument7 pagesGoods and Service TaxNitheesh BNo ratings yet

- FOURTH SEMESTER GSTDocument6 pagesFOURTH SEMESTER GSTKenny PhilipsNo ratings yet

- Imapct of Goods and Services TaxDocument12 pagesImapct of Goods and Services TaxSwetank SrivastavaNo ratings yet

- Mutual FundsDocument12 pagesMutual FundsLakshmiRengarajanNo ratings yet

- Ijreiss 2915 35074Document5 pagesIjreiss 2915 35074Rahul KumarNo ratings yet

- Report On IMPACT OF GST ON REAL ESTATE INDUSTRYDocument31 pagesReport On IMPACT OF GST ON REAL ESTATE INDUSTRYsamNo ratings yet

- Report On IMPACT OF GST ON REAL ESTATE INDUSTRYDocument31 pagesReport On IMPACT OF GST ON REAL ESTATE INDUSTRYsamNo ratings yet

- QuickRef GST Changes JDA 1Document8 pagesQuickRef GST Changes JDA 1umesh bagwaleNo ratings yet

- Ijreiss 2915 35074Document5 pagesIjreiss 2915 35074Darshan JoshiNo ratings yet

- Telecom Sector - GST Project - Group M - Sec (C)Document37 pagesTelecom Sector - GST Project - Group M - Sec (C)0443GomathinayagamNo ratings yet

- Assignment - Fiscal and Corporate LawsDocument19 pagesAssignment - Fiscal and Corporate LawsPriyaNo ratings yet

- K HUSGBUDocument39 pagesK HUSGBUkhushbushaleshNo ratings yet

- Taxation Direct and Indirect NMIMS AssignmentDocument6 pagesTaxation Direct and Indirect NMIMS AssignmentN. Karthik UdupaNo ratings yet

- Task 8Document23 pagesTask 8Anooja SajeevNo ratings yet

- Tax SanjogDocument9 pagesTax SanjogSanjog DewanNo ratings yet

- GST - Concern in New RegimeDocument7 pagesGST - Concern in New RegimeArnab PhonglosaNo ratings yet

- B.R. NANDA, Gandhi and His Critics, Delhi, Oxford University PressDocument3 pagesB.R. NANDA, Gandhi and His Critics, Delhi, Oxford University PressAyushi PanditNo ratings yet

- Jason M. Pobjoy, The Child in International Refugee Law Book ReviewDocument5 pagesJason M. Pobjoy, The Child in International Refugee Law Book ReviewAyushi PanditNo ratings yet

- History Rough Draft 2Document15 pagesHistory Rough Draft 2Ayushi PanditNo ratings yet

- Hazara vs. Pashtuns.. - For MergeDocument11 pagesHazara vs. Pashtuns.. - For MergeAyushi PanditNo ratings yet

- Delivery - Westlaw IndiaDocument16 pagesDelivery - Westlaw IndiaAyushi PanditNo ratings yet

- History and Effects of War and Terrorism in AfghanistanDocument12 pagesHistory and Effects of War and Terrorism in AfghanistanAyushi PanditNo ratings yet

- OMP (I) (COMM.) 55/2015 Simplex Infrastructure Ltd. v. Energo Engineering Projects LTDDocument4 pagesOMP (I) (COMM.) 55/2015 Simplex Infrastructure Ltd. v. Energo Engineering Projects LTDAyushi PanditNo ratings yet

- IBC - The Journey So Far - Part IDocument19 pagesIBC - The Journey So Far - Part IAyushi PanditNo ratings yet

- IDBI Bank Limited Vs Prakash Chandra SharmaDocument12 pagesIDBI Bank Limited Vs Prakash Chandra SharmaAyushi PanditNo ratings yet

- 2016 SCC Online Bom 9019 in The High Court of BombayDocument21 pages2016 SCC Online Bom 9019 in The High Court of BombayAyushi PanditNo ratings yet

- LLC vs. Future Retail Limited & Ors.Document54 pagesLLC vs. Future Retail Limited & Ors.Ayushi PanditNo ratings yet

- C Requirement For A Stronger Regulatory RegimeDocument14 pagesC Requirement For A Stronger Regulatory RegimeAyushi PanditNo ratings yet

- Radha Krishan Industries Vs State of Himachal Pradesh Supreme Court of IndiaDocument61 pagesRadha Krishan Industries Vs State of Himachal Pradesh Supreme Court of IndiaAyushi PanditNo ratings yet

- C Escrows and Specific Capital Account Regulations - A Brief StudyDocument24 pagesC Escrows and Specific Capital Account Regulations - A Brief StudyAyushi PanditNo ratings yet

- Kihoto HolohonDocument59 pagesKihoto HolohonAyushi PanditNo ratings yet

- End of The Post Colonial StateDocument28 pagesEnd of The Post Colonial StateOpie UmsgoodNo ratings yet

- He Said She Said - The RCBC Money Laundering ScandalDocument7 pagesHe Said She Said - The RCBC Money Laundering ScandalKrizel rochaNo ratings yet

- Midori Hotel BUSINESS PLANDocument32 pagesMidori Hotel BUSINESS PLANJesesNo ratings yet

- Meaning of Responsibility CenterDocument18 pagesMeaning of Responsibility CenterSuman Preet KaurNo ratings yet

- Agriculture Marketing Lec No 6Document27 pagesAgriculture Marketing Lec No 6MUZAMMIL GHORINo ratings yet

- Day Trading by Matthew MayburyDocument52 pagesDay Trading by Matthew MayburyXRM09090% (1)

- Stage Gate For Product Development - Cooper EdgettDocument6 pagesStage Gate For Product Development - Cooper EdgettjohniglesiaNo ratings yet

- Bond ValuationDocument2 pagesBond ValuationIkram Ul Haq0% (1)

- History of Insurance Legislation in IndiaDocument17 pagesHistory of Insurance Legislation in IndiaSagar Bhadrige83% (6)

- Leadership Case StudyDocument2 pagesLeadership Case StudyAnish KrishnanNo ratings yet

- International Law Office of Ake & Associates Co., LTD.: Advocates - Solicitors - NotariesDocument6 pagesInternational Law Office of Ake & Associates Co., LTD.: Advocates - Solicitors - NotariesNuansnit ChNo ratings yet

- Risk in SCM: Procurement: AssignmentDocument4 pagesRisk in SCM: Procurement: AssignmentBhavya K BalanNo ratings yet

- COMPANY INTRODUCTION CiplaDocument2 pagesCOMPANY INTRODUCTION CiplaHoney AliNo ratings yet

- MINE1x Course SyllabusDocument6 pagesMINE1x Course Syllabusik43207No ratings yet

- Director of Sales in Sacramento CA Resume Boyd SheetsDocument3 pagesDirector of Sales in Sacramento CA Resume Boyd SheetsBoydSheetsNo ratings yet

- CLN 101Document12 pagesCLN 101akshdeep singhNo ratings yet

- Carbon Dioxide Capture and Storage in Geological Formations As Clean Development Mechanism Project ActivitiesDocument3 pagesCarbon Dioxide Capture and Storage in Geological Formations As Clean Development Mechanism Project ActivitiesztamanNo ratings yet

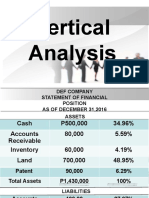

- Vertical AnalysisDocument8 pagesVertical AnalysisHannah Mae BautistaNo ratings yet

- Sawhney Lampert Paper 2016Document33 pagesSawhney Lampert Paper 2016PURVA BORKARNo ratings yet

- Production and Operations Management: Chapter: 05. Inventory ControlDocument5 pagesProduction and Operations Management: Chapter: 05. Inventory ControlSN AdnanNo ratings yet

- S - Ch7 - Long Term Objectives and StrategiesDocument31 pagesS - Ch7 - Long Term Objectives and StrategiesYion LekNo ratings yet

- PRACTICE Quiz 4 - CFASDocument4 pagesPRACTICE Quiz 4 - CFASLing lingNo ratings yet

- AKKU Annual Report 2016Document141 pagesAKKU Annual Report 2016Doli Dui TilfaNo ratings yet

- Chapter 6 Designing Global Supply Chain NetworksDocument22 pagesChapter 6 Designing Global Supply Chain NetworksRashadafaneh100% (1)

- QuestionnaireDocument4 pagesQuestionnaireJoyal JosephNo ratings yet

- Contract DraftingDocument2 pagesContract DraftingSineepa PLOYNo ratings yet