Download as pdf or txt

You might also like

- HUAWEI SEQ Analyst V300R002 Data DictionaryDocument1,245 pagesHUAWEI SEQ Analyst V300R002 Data DictionarymikenemonicNo ratings yet

- JPM Nigeria Reform Paus 2023-08-17 4491177Document11 pagesJPM Nigeria Reform Paus 2023-08-17 4491177Carl MacaulayNo ratings yet

- Assurance of Discontinuance With Praying Pelicans MissionsDocument25 pagesAssurance of Discontinuance With Praying Pelicans MissionsDuluth News Tribune100% (2)

- ComplaintDocument6 pagesComplaintCarlos AparicioNo ratings yet

- Taxation of Debt InstrumentsDocument15 pagesTaxation of Debt InstrumentsPunyak SatishNo ratings yet

- C20X and C50X Series Manual - EnglishDocument86 pagesC20X and C50X Series Manual - EnglishCheme Plata100% (1)

- Sales Sample Q Sans F 09Document17 pagesSales Sample Q Sans F 09Tay Mon100% (1)

- Negotiable Debt InstrumentsDocument5 pagesNegotiable Debt Instrumentsbrucefarmer89% (9)

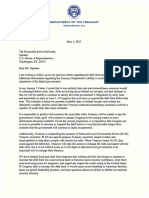

- Sec. Yellen Letter To Speaker McCarthyDocument2 pagesSec. Yellen Letter To Speaker McCarthyDaily Caller News FoundationNo ratings yet

- Government NotesDocument31 pagesGovernment Notesapi-257176789No ratings yet

- ReceivershipDocument11 pagesReceivershipbig_tunaNo ratings yet

- Trust Lesson OneDocument10 pagesTrust Lesson OneFathima RaznaNo ratings yet

- Loan AppDocument1 pageLoan Appapi-289462742No ratings yet

- Purchase Order Policies and Procedures: Herscher Community Unit School District #2Document13 pagesPurchase Order Policies and Procedures: Herscher Community Unit School District #2Bon.AlastoyNo ratings yet

- Beneficial Owner Declaration - Annexure IDocument3 pagesBeneficial Owner Declaration - Annexure ISamkit JainNo ratings yet

- When A Non Bank Issues A Letter of CreditDocument3 pagesWhen A Non Bank Issues A Letter of Creditvodka_taste2882No ratings yet

- LC1Document40 pagesLC1Tran Thi Thu HuongNo ratings yet

- Affidavit For BCDocument3 pagesAffidavit For BCEric Willis100% (1)

- DBA-104-Statutory Durable Power of AttorneyDocument6 pagesDBA-104-Statutory Durable Power of AttorneyIrene HernandezNo ratings yet

- Ptdo Masterplan2017Document84 pagesPtdo Masterplan2017ShanetteNo ratings yet

- Mail - RE - Claim Status - YFAE950884YF PDFDocument3 pagesMail - RE - Claim Status - YFAE950884YF PDFSankalp Suman ChandelNo ratings yet

- BassDrill Alpha - Information MemorandumDocument90 pagesBassDrill Alpha - Information MemorandumAnbuNo ratings yet

- US v. Dunlap Govt Brief Opposing Compassionate ReleaseDocument19 pagesUS v. Dunlap Govt Brief Opposing Compassionate ReleaseWashington Free BeaconNo ratings yet

- Faq 7 CNDocument8 pagesFaq 7 CNakia123No ratings yet

- INSTRUCTIONS - FORM 2848 (On Page 2 and 3) : Participant ID # Usually Starts With PS Followed by 8 DigitsDocument3 pagesINSTRUCTIONS - FORM 2848 (On Page 2 and 3) : Participant ID # Usually Starts With PS Followed by 8 DigitsEstrella Cotrina RojasNo ratings yet

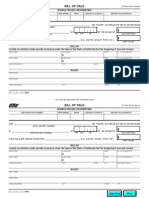

- Bill of SaleDocument1 pageBill of SalelayoNo ratings yet

- Revocable Letter of Credit Can Be Revoked Without The Consent of TheDocument3 pagesRevocable Letter of Credit Can Be Revoked Without The Consent of ThePankaj ThapaNo ratings yet

- StatusDocument1 pageStatusMinisterNo ratings yet

- W8 Instructions PDFDocument15 pagesW8 Instructions PDFKrisdenNo ratings yet

- Legal Notice of Removal: From Municipal Court To Federal Court Pursuant To Title 28 Proper Article Iii JurisdictionDocument25 pagesLegal Notice of Removal: From Municipal Court To Federal Court Pursuant To Title 28 Proper Article Iii JurisdictionElNo ratings yet

- Apostille: CertifiedDocument2 pagesApostille: CertifiedOneNationNo ratings yet

- Banking Law AssignmentDocument11 pagesBanking Law AssignmentTanu Shree SinghNo ratings yet

- Field Operations Directives (FODs) 19-002 Impounded and Stored Vehicles - 4-18-2023Document7 pagesField Operations Directives (FODs) 19-002 Impounded and Stored Vehicles - 4-18-2023MetinnNo ratings yet

- Form 4029Document2 pagesForm 4029Brett BaldwinNo ratings yet

- BondsDocument10 pagesBondsGeorge William100% (1)

- 34 83712 Ex5Document26 pages34 83712 Ex5Troy StrawnNo ratings yet

- Trade AcceptanceDocument1 pageTrade AcceptanceEmilNo ratings yet

- Bill of CostDocument1 pageBill of Costgordon scottNo ratings yet

- Macn-R000130723 - Affidavit of Universal Commerical Code 1 Financing Statement (Vyve Broadband-Mega Broadband InvestmentsDocument6 pagesMacn-R000130723 - Affidavit of Universal Commerical Code 1 Financing Statement (Vyve Broadband-Mega Broadband Investmentstheodore moses antoine beyNo ratings yet

- Discharge of ObligationsDocument2 pagesDischarge of ObligationskamilNo ratings yet

- Loan Modification: Contract & FormsDocument16 pagesLoan Modification: Contract & Formsldobbins2No ratings yet

- Consumer Credit ApplicationDocument1 pageConsumer Credit ApplicationUlrichNo ratings yet

- Private Correspondence Mnuchin USA I MUSTERDocument1 pagePrivate Correspondence Mnuchin USA I MUSTERSebastian WienbreyerNo ratings yet

- Broker Letter Regarding Second BINDQ DistributionDocument15 pagesBroker Letter Regarding Second BINDQ DistributionbuyersstrikewpNo ratings yet

- SS FormDocument2 pagesSS Formblueocean8888100% (1)

- MC 710 Motion For DiscoveryDocument2 pagesMC 710 Motion For Discoveryijennin100% (1)

- Appellation Identity CardDocument2 pagesAppellation Identity CardZubiya Yamina El (All Rights Reserved)No ratings yet

- Indemnification Statement Form 700-ADocument1 pageIndemnification Statement Form 700-AMichael100% (1)

- Letter To ClerkDocument1 pageLetter To ClerkZoeNo ratings yet

- SEC FOIA 2011-6336 - FOIA Office Response - 5.24.2011Document3 pagesSEC FOIA 2011-6336 - FOIA Office Response - 5.24.2011Michael Brozzetti100% (1)

- All Banking Related Questions PDF - Exampundit - SatishDocument49 pagesAll Banking Related Questions PDF - Exampundit - SatishRaj DubeyNo ratings yet

- Private Equity Transactions: Overview of A Buy-Out: International Investor Series No. 9Document20 pagesPrivate Equity Transactions: Overview of A Buy-Out: International Investor Series No. 9CfhunSaatNo ratings yet

- MSB Registration From FinCENDocument1 pageMSB Registration From FinCENCoin FireNo ratings yet

- Money and Monetarism: Unit HighlightsDocument18 pagesMoney and Monetarism: Unit HighlightsprabodhNo ratings yet

- Massive Court Filing - Tieshea Autumn BrifilDocument82 pagesMassive Court Filing - Tieshea Autumn Brifiltieshea autumn brifil tmNo ratings yet

- Ny Lastname Firstname DSRDocument1 pageNy Lastname Firstname DSRAlecia Sterling100% (1)

- Form W-8BEN-E InstructionsDocument15 pagesForm W-8BEN-E InstructionsSteve ThompsonNo ratings yet

- Instruments For Financing Working CapitalDocument6 pagesInstruments For Financing Working CapitalPra SonNo ratings yet

- ICE CDS White PaperDocument21 pagesICE CDS White PaperRajat SharmaNo ratings yet

- Court Trump CardDocument1 pageCourt Trump CardajgtrustNo ratings yet

- Constitution of the State of Minnesota — 1876 VersionFrom EverandConstitution of the State of Minnesota — 1876 VersionNo ratings yet

- QUIZ-12 (Q+S) 2024-25 Mrunal EcoPCB10 KING R QUEEN PDocument62 pagesQUIZ-12 (Q+S) 2024-25 Mrunal EcoPCB10 KING R QUEEN Ptusharchoudhary57037No ratings yet

- Towards A Renovated World Monetary SystemDocument47 pagesTowards A Renovated World Monetary SystemConstitutionReport100% (1)

- International Financial Institutions: MMS (University of Mumbai)Document28 pagesInternational Financial Institutions: MMS (University of Mumbai)asadNo ratings yet

- Term Paper: "Balance of Payment Accounting-Meaning, Principles and Accounting"Document12 pagesTerm Paper: "Balance of Payment Accounting-Meaning, Principles and Accounting"hina4No ratings yet

- Prime Mock 12Document48 pagesPrime Mock 12Janhavi DhingraNo ratings yet

- Strategies of Manipulation in Democratic Societies in A Globalised Age: Transitioning To A Cashless Society in Germany - Master's ThesisDocument150 pagesStrategies of Manipulation in Democratic Societies in A Globalised Age: Transitioning To A Cashless Society in Germany - Master's ThesisMalikaNo ratings yet

- Indian Automobile Industry AnalysisDocument41 pagesIndian Automobile Industry Analysismr.avdheshsharma85% (26)

- The Modern ResearcherDocument404 pagesThe Modern Researcherestudosdoleandro sobretomismoNo ratings yet

- Verso Do Awb - ContratoDocument1 pageVerso Do Awb - ContratoMarouza HainanNo ratings yet

- (9781589061620 - International Monetary Fund Annual Report 2002) International Monetary Fund Annual Report 2002Document233 pages(9781589061620 - International Monetary Fund Annual Report 2002) International Monetary Fund Annual Report 2002Juasadf IesafNo ratings yet

- Bretton Woods PDFDocument20 pagesBretton Woods PDFbusybeefreedomNo ratings yet

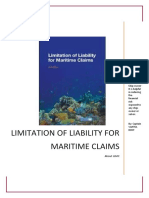

- Limitation of Liability For Maritime ClaimsDocument26 pagesLimitation of Liability For Maritime ClaimsAman GautamNo ratings yet

- XIMB - IF - Group 7 - Yatish AgrawalDocument6 pagesXIMB - IF - Group 7 - Yatish AgrawaljatinNo ratings yet

- The Global Currency Power of The Us Dollar Problems and Prospects 1St Edition Anthony Elson Full ChapterDocument67 pagesThe Global Currency Power of The Us Dollar Problems and Prospects 1St Edition Anthony Elson Full Chapterfrank.meachum914100% (8)

- SDR FinalDocument17 pagesSDR FinalAiswarya VijayanNo ratings yet

- Beepedia Monthly Current Affairs (Beepedia) November 2023Document141 pagesBeepedia Monthly Current Affairs (Beepedia) November 2023Vikram SharmaNo ratings yet

- Hugh Hendry Eclectica Nov09Document8 pagesHugh Hendry Eclectica Nov09marketfolly.comNo ratings yet

- Banking Current Affairs 2014 17Document161 pagesBanking Current Affairs 2014 17laksh048No ratings yet

- Domestic External Debt of PakistanDocument9 pagesDomestic External Debt of PakistanMeeroButtNo ratings yet

- Chapter No.1.Introduction: Special Drawing Rights (SDR)Document25 pagesChapter No.1.Introduction: Special Drawing Rights (SDR)sugandhirajanNo ratings yet

- International Monetary FundDocument10 pagesInternational Monetary Fund777priyankaNo ratings yet

- International Business Law - Chapter 6Document34 pagesInternational Business Law - Chapter 6hnhNo ratings yet

- Public Debt 2014eDocument73 pagesPublic Debt 2014elankaCnewsNo ratings yet

- Research Paper Rupesh Amol 11Document9 pagesResearch Paper Rupesh Amol 11gurjit20No ratings yet

- Imf Annual Report 2019Document108 pagesImf Annual Report 2019MALAY KUMARNo ratings yet

- Bretton Woods InstitutionsDocument8 pagesBretton Woods InstitutionsPradyumn LandgeNo ratings yet

- Philadelphia Trumpet MagazineDocument40 pagesPhiladelphia Trumpet MagazinejoeNo ratings yet