Cash Flow Statements Study Guide

Cash Flow Statements Study Guide

You might also like

- Question 8 - Preparation of FSDocument4 pagesQuestion 8 - Preparation of FSRax-Nguajandja Kapuire100% (1)

- Cash Flow Statements and Warf Computers Mini CaseDocument6 pagesCash Flow Statements and Warf Computers Mini CaseAshekin MahadiNo ratings yet

- Antique Automotive RestorationDocument8 pagesAntique Automotive Restorationjr4ya100% (5)

- CH 04Document56 pagesCH 04Hiền AnhNo ratings yet

- Quizzes Chapter 3 Acccounting EquationDocument7 pagesQuizzes Chapter 3 Acccounting EquationAmie Jane Miranda100% (2)

- Sawyers - Introduction To Managerial AccountingDocument29 pagesSawyers - Introduction To Managerial AccountingTrisha Mae AlburoNo ratings yet

- In These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsDocument53 pagesIn These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsAshekin MahadiNo ratings yet

- Problems 1-30: Input Boxes in TanDocument37 pagesProblems 1-30: Input Boxes in TanAshekin Mahadi100% (1)

- ECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Document11 pagesECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Ashekin MahadiNo ratings yet

- ECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Document11 pagesECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Ashekin MahadiNo ratings yet

- Exam 3 Study GuideDocument11 pagesExam 3 Study GuideMinh NguyễnNo ratings yet

- IFM10 CH 16 Test BankDocument14 pagesIFM10 CH 16 Test Bankphamngocmai1912No ratings yet

- Gitman IM ch08 PDFDocument17 pagesGitman IM ch08 PDFdmnque pileNo ratings yet

- TFA - Chapter 36 - Property, Plant and EquipmentDocument9 pagesTFA - Chapter 36 - Property, Plant and EquipmentAsi Cas Jav0% (1)

- Introduction To Financial Accounting - Horngren 10-34, 9edition.Document2 pagesIntroduction To Financial Accounting - Horngren 10-34, 9edition.ashish_kumar_881167% (3)

- Template - MIDTERM EXAM INTERMEDIATE 1Document7 pagesTemplate - MIDTERM EXAM INTERMEDIATE 1Rani RahayuNo ratings yet

- Robi-Airtel Merger Analysis by RobiDocument13 pagesRobi-Airtel Merger Analysis by RobiTarek MahmudNo ratings yet

- STR 581 Capstone Final Exam Part Two Latest Question AnswersDocument12 pagesSTR 581 Capstone Final Exam Part Two Latest Question AnswersaarenaddisonNo ratings yet

- Advanced Financial AccountingDocument8 pagesAdvanced Financial AccountingricharddiagmelNo ratings yet

- FINMAN TB Chapter13 Capital Structure and LeverageDocument32 pagesFINMAN TB Chapter13 Capital Structure and Leveragechin mohammadNo ratings yet

- CSR in BDDocument23 pagesCSR in BDSadia HassanNo ratings yet

- Capital Budgeting: Year Cash FlowDocument5 pagesCapital Budgeting: Year Cash FlowNaeem Uddin100% (3)

- FA2Document77 pagesFA2shahreen arshad0% (1)

- Term Paper On The Changes Between IAS 18 and IFRS 15Document18 pagesTerm Paper On The Changes Between IAS 18 and IFRS 15Nion Majumdar100% (6)

- Chapter 4 Analysis of Financial StatementsDocument2 pagesChapter 4 Analysis of Financial StatementsSamantha Siau100% (1)

- Starbucks Financial Statement AnalysisDocument6 pagesStarbucks Financial Statement AnalysisStefani Dian100% (2)

- Report Fin GroupDocument10 pagesReport Fin GroupFATIMAH ZAHRA BINTI ABDUL HADI KAMELNo ratings yet

- Competitive Advantage of Nsu: Project OnDocument41 pagesCompetitive Advantage of Nsu: Project OnTanvir KhanNo ratings yet

- Characteristics of PartnershipDocument2 pagesCharacteristics of Partnershipckarla800% (1)

- MCS Notes (MBA)Document88 pagesMCS Notes (MBA)prashantsmartie100% (20)

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessDocument10 pagesChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosNo ratings yet

- FIN2601-chapter 6Document28 pagesFIN2601-chapter 6Atiqa Aslam100% (1)

- Financial Management - DefinitionDocument13 pagesFinancial Management - DefinitionAmol AgarwalNo ratings yet

- Finance Case StudyDocument8 pagesFinance Case StudyEvans MettoNo ratings yet

- Tuga Ketiga PMMKDocument3 pagesTuga Ketiga PMMKERika PratiwiNo ratings yet

- ProformaDocument4 pagesProformadevanmadeNo ratings yet

- Issues in Corporate GovernanceDocument15 pagesIssues in Corporate GovernanceVandana ŘwţNo ratings yet

- Chapter 13-Planning For The Harvest: True/FalseDocument17 pagesChapter 13-Planning For The Harvest: True/FalseKhang ToNo ratings yet

- Financing S&S Air's Expansion PlansDocument6 pagesFinancing S&S Air's Expansion Plansmone2222100% (1)

- Conventional Versus Non Conventional Cash4079Document10 pagesConventional Versus Non Conventional Cash4079Amna SaeedNo ratings yet

- Corporate Reporting-1Document69 pagesCorporate Reporting-1Najmul IslamNo ratings yet

- Core Principles and Applications of Corporate Finance: Stephen A. RossDocument12 pagesCore Principles and Applications of Corporate Finance: Stephen A. RossAHMED MOHAMED YUSUFNo ratings yet

- ACCA PAPER P4 Advanced Financial Management Module 2Document50 pagesACCA PAPER P4 Advanced Financial Management Module 2123ramboNo ratings yet

- Problem Set #2-Solutions PDFDocument4 pagesProblem Set #2-Solutions PDFLhorene Hope DueñasNo ratings yet

- Du Pont AnalysisDocument5 pagesDu Pont AnalysisBindal HeenaNo ratings yet

- The Dilemma at Day 21Document4 pagesThe Dilemma at Day 21Christian AndreNo ratings yet

- Core and Principle of Corporate FinanceDocument12 pagesCore and Principle of Corporate FinancePermata Ayu WidyasariNo ratings yet

- Chapter 6Document26 pagesChapter 6dshilkarNo ratings yet

- Chapter 2: Stock Investments - Investor Accounting and ReportingDocument36 pagesChapter 2: Stock Investments - Investor Accounting and Reportingnikitarani kikiNo ratings yet

- Case Study of WiproDocument2 pagesCase Study of WiproAbhi ThakurNo ratings yet

- George Foster Financial Statement AnalysisDocument2 pagesGeorge Foster Financial Statement AnalysisdnesudhudhNo ratings yet

- Final Thesis IntanDocument77 pagesFinal Thesis IntanKarina RusmanNo ratings yet

- Family Business Succession A Strategic Planning ModelDocument4 pagesFamily Business Succession A Strategic Planning Modelleopedrazac22No ratings yet

- Chapter 4Document17 pagesChapter 4RBNo ratings yet

- On IFRS, US GAAP and Indian GAAPDocument64 pagesOn IFRS, US GAAP and Indian GAAPrishipath100% (1)

- Chapter 10: Managerial Planning and Control: International Accounting, 6/eDocument25 pagesChapter 10: Managerial Planning and Control: International Accounting, 6/eapi-241660930100% (1)

- Chapter 003 Financial Analysis: True / False QuestionsDocument54 pagesChapter 003 Financial Analysis: True / False QuestionsWinnie GiveraNo ratings yet

- Jan 2018Document34 pagesJan 2018alekhya manneNo ratings yet

- Ch09 Solations Brigham 10th EDocument12 pagesCh09 Solations Brigham 10th ERafay HussainNo ratings yet

- The Human Resource Department of Nestlé Bangladesh Limited and Its Essential Functions and ActivitiesDocument58 pagesThe Human Resource Department of Nestlé Bangladesh Limited and Its Essential Functions and ActivitiesVishesh ShuklaNo ratings yet

- Debt RatioDocument7 pagesDebt RatioAamir BilalNo ratings yet

- Chapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetDocument17 pagesChapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetZunaira ButtNo ratings yet

- Cash Flow Estimation BrighamDocument77 pagesCash Flow Estimation BrighamDianne GalarosaNo ratings yet

- Case Study Ratio AnalysisDocument6 pagesCase Study Ratio Analysisash867240% (1)

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Guide to Management Accounting CCC (Cash Conversion Cycle) for managersFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for managersNo ratings yet

- Do You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessFrom EverandDo You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessNo ratings yet

- Problem 1: Cash Flow Statement (Class Practice)Document2 pagesProblem 1: Cash Flow Statement (Class Practice)ronamiNo ratings yet

- Case 2 Performance Management at Vitality Health Enterprises PDFDocument2 pagesCase 2 Performance Management at Vitality Health Enterprises PDFAshekin MahadiNo ratings yet

- Mgt489 Final Group Report - Udoy Das 1Document24 pagesMgt489 Final Group Report - Udoy Das 1Ashekin MahadiNo ratings yet

- Mid ID#2035038#Md. Hazrat AliDocument11 pagesMid ID#2035038#Md. Hazrat AliAshekin MahadiNo ratings yet

- This Study Resource Was: Performance Management at Vitality Health IncDocument3 pagesThis Study Resource Was: Performance Management at Vitality Health IncAshekin MahadiNo ratings yet

- CF 12th Edition Chapter 02Document38 pagesCF 12th Edition Chapter 02Ashekin MahadiNo ratings yet

- Comtemporary Issues in LeadershipDocument12 pagesComtemporary Issues in LeadershipAshekin MahadiNo ratings yet

- Case Study Vitality Health Discussion Questions 2 PDFDocument2 pagesCase Study Vitality Health Discussion Questions 2 PDFAshekin MahadiNo ratings yet

- Chapter 1Document16 pagesChapter 1Ashekin MahadiNo ratings yet

- Assignment EMB660Document11 pagesAssignment EMB660Ashekin MahadiNo ratings yet

- RWJ Chapter 1 Introduction To Corporate FinanceDocument21 pagesRWJ Chapter 1 Introduction To Corporate FinanceAshekin Mahadi100% (1)

- RWJ Chapter 4 DCF ValuationDocument47 pagesRWJ Chapter 4 DCF ValuationAshekin MahadiNo ratings yet

- 5 Written Questions: Type Your AnswerDocument4 pages5 Written Questions: Type Your AnswerAshekin MahadiNo ratings yet

- 3 Written Questions: Type Your AnswerDocument3 pages3 Written Questions: Type Your AnswerAshekin MahadiNo ratings yet

- Test - Leadership - 123 QuizletDocument7 pagesTest - Leadership - 123 QuizletAshekin MahadiNo ratings yet

- Full Ifrs Vs SmeDocument6 pagesFull Ifrs Vs SmeMina ValenciaNo ratings yet

- Balance Sheet & Profit LossDocument7 pagesBalance Sheet & Profit LossJenny Davidson50% (2)

- Financial Accounting 1 Lesson 3 - SO1 Double Entry - RecordingDocument35 pagesFinancial Accounting 1 Lesson 3 - SO1 Double Entry - RecordingZudjian WarriorNo ratings yet

- Government Accounting Overview: Korbel Foundation College, IncDocument16 pagesGovernment Accounting Overview: Korbel Foundation College, IncRuby Amor DoligosaNo ratings yet

- Long Quiz 2Document8 pagesLong Quiz 2CattleyaNo ratings yet

- Accounting RatiosDocument5 pagesAccounting RatiosNaga NikhilNo ratings yet

- List of 30 Highest Dividend Paying Stocks in IndiaDocument5 pagesList of 30 Highest Dividend Paying Stocks in IndiaPankajNo ratings yet

- Analysis of The Estimation of Working Capital of Bajaj Finance Using TheDocument6 pagesAnalysis of The Estimation of Working Capital of Bajaj Finance Using TheRamasayi GummadiNo ratings yet

- June 2009 AnsDocument16 pagesJune 2009 AnsMacRen Bruce100% (1)

- Partnership Final Accounts PDFDocument97 pagesPartnership Final Accounts PDFKaushik Patel75% (4)

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- FR 2019 Paper FinalDocument58 pagesFR 2019 Paper FinalshashalalaxiangNo ratings yet

- Balance Sheet As of December 2018: JL - Karapitan No.140 BandungDocument1 pageBalance Sheet As of December 2018: JL - Karapitan No.140 BandungNurul patimahNo ratings yet

- Deprival Value Lecture NotesDocument7 pagesDeprival Value Lecture NotesTosin YusufNo ratings yet

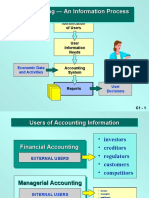

- Accounting - An Information Process Accounting - An Information ProcessDocument58 pagesAccounting - An Information Process Accounting - An Information ProcessBernadette Cunanan RamosNo ratings yet

- Chapter 1 Overview of CostDocument13 pagesChapter 1 Overview of Costnewaybeyene5No ratings yet

- Solved Suppose Morrison Corp S Breakeven Point Is Revenues of 1 100 000 Fixed CostsDocument1 pageSolved Suppose Morrison Corp S Breakeven Point Is Revenues of 1 100 000 Fixed CostsAnbu jaromiaNo ratings yet

- LOVISA V PANDORA FINANCIAL ANALYSIS RATIODocument30 pagesLOVISA V PANDORA FINANCIAL ANALYSIS RATIOpipahNo ratings yet

- Ase20093 01 Results Mark Scheme 20220629 April 2022 SeriesDocument18 pagesAse20093 01 Results Mark Scheme 20220629 April 2022 SeriesEi Ei TheintNo ratings yet

- Excercises MA 2023 1Document4 pagesExcercises MA 2023 1fin.minhtringuyenNo ratings yet

- Week 1 Review of Accounting BasicsDocument34 pagesWeek 1 Review of Accounting BasicsGokul KumarNo ratings yet

- Chapter 9 Notes Question Amp SolutionsDocument5 pagesChapter 9 Notes Question Amp SolutionsPankhuri SinghalNo ratings yet

- Fundamental Concepts of Managerial AccountingDocument45 pagesFundamental Concepts of Managerial AccountingCarlo CanlasNo ratings yet

- Ppe ExerciseDocument8 pagesPpe ExerciseNajihah NordinNo ratings yet

- ch1 Slides Students - ANDocument24 pagesch1 Slides Students - ANakshitnagpal9119No ratings yet

- IAS 38 Intangible AssetsDocument41 pagesIAS 38 Intangible AssetsAbdul RehmanNo ratings yet

Download as pdf or txt

You might also like

- Question 8 - Preparation of FSDocument4 pagesQuestion 8 - Preparation of FSRax-Nguajandja Kapuire100% (1)

- Cash Flow Statements and Warf Computers Mini CaseDocument6 pagesCash Flow Statements and Warf Computers Mini CaseAshekin MahadiNo ratings yet

- Antique Automotive RestorationDocument8 pagesAntique Automotive Restorationjr4ya100% (5)

- CH 04Document56 pagesCH 04Hiền AnhNo ratings yet

- Quizzes Chapter 3 Acccounting EquationDocument7 pagesQuizzes Chapter 3 Acccounting EquationAmie Jane Miranda100% (2)

- Sawyers - Introduction To Managerial AccountingDocument29 pagesSawyers - Introduction To Managerial AccountingTrisha Mae AlburoNo ratings yet

- In These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsDocument53 pagesIn These Spreadsheets, You Will Learn How To Use The Following Excel FunctionsAshekin MahadiNo ratings yet

- Problems 1-30: Input Boxes in TanDocument37 pagesProblems 1-30: Input Boxes in TanAshekin Mahadi100% (1)

- ECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Document11 pagesECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Ashekin MahadiNo ratings yet

- ECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Document11 pagesECN 134: Solution Key To Problem Set 2 Part A: CF Statement. You Are Given The Following Information of XYZ Corporation For 2011Ashekin MahadiNo ratings yet

- Exam 3 Study GuideDocument11 pagesExam 3 Study GuideMinh NguyễnNo ratings yet

- IFM10 CH 16 Test BankDocument14 pagesIFM10 CH 16 Test Bankphamngocmai1912No ratings yet

- Gitman IM ch08 PDFDocument17 pagesGitman IM ch08 PDFdmnque pileNo ratings yet

- TFA - Chapter 36 - Property, Plant and EquipmentDocument9 pagesTFA - Chapter 36 - Property, Plant and EquipmentAsi Cas Jav0% (1)

- Introduction To Financial Accounting - Horngren 10-34, 9edition.Document2 pagesIntroduction To Financial Accounting - Horngren 10-34, 9edition.ashish_kumar_881167% (3)

- Template - MIDTERM EXAM INTERMEDIATE 1Document7 pagesTemplate - MIDTERM EXAM INTERMEDIATE 1Rani RahayuNo ratings yet

- Robi-Airtel Merger Analysis by RobiDocument13 pagesRobi-Airtel Merger Analysis by RobiTarek MahmudNo ratings yet

- STR 581 Capstone Final Exam Part Two Latest Question AnswersDocument12 pagesSTR 581 Capstone Final Exam Part Two Latest Question AnswersaarenaddisonNo ratings yet

- Advanced Financial AccountingDocument8 pagesAdvanced Financial AccountingricharddiagmelNo ratings yet

- FINMAN TB Chapter13 Capital Structure and LeverageDocument32 pagesFINMAN TB Chapter13 Capital Structure and Leveragechin mohammadNo ratings yet

- CSR in BDDocument23 pagesCSR in BDSadia HassanNo ratings yet

- Capital Budgeting: Year Cash FlowDocument5 pagesCapital Budgeting: Year Cash FlowNaeem Uddin100% (3)

- FA2Document77 pagesFA2shahreen arshad0% (1)

- Term Paper On The Changes Between IAS 18 and IFRS 15Document18 pagesTerm Paper On The Changes Between IAS 18 and IFRS 15Nion Majumdar100% (6)

- Chapter 4 Analysis of Financial StatementsDocument2 pagesChapter 4 Analysis of Financial StatementsSamantha Siau100% (1)

- Starbucks Financial Statement AnalysisDocument6 pagesStarbucks Financial Statement AnalysisStefani Dian100% (2)

- Report Fin GroupDocument10 pagesReport Fin GroupFATIMAH ZAHRA BINTI ABDUL HADI KAMELNo ratings yet

- Competitive Advantage of Nsu: Project OnDocument41 pagesCompetitive Advantage of Nsu: Project OnTanvir KhanNo ratings yet

- Characteristics of PartnershipDocument2 pagesCharacteristics of Partnershipckarla800% (1)

- MCS Notes (MBA)Document88 pagesMCS Notes (MBA)prashantsmartie100% (20)

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessDocument10 pagesChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosNo ratings yet

- FIN2601-chapter 6Document28 pagesFIN2601-chapter 6Atiqa Aslam100% (1)

- Financial Management - DefinitionDocument13 pagesFinancial Management - DefinitionAmol AgarwalNo ratings yet

- Finance Case StudyDocument8 pagesFinance Case StudyEvans MettoNo ratings yet

- Tuga Ketiga PMMKDocument3 pagesTuga Ketiga PMMKERika PratiwiNo ratings yet

- ProformaDocument4 pagesProformadevanmadeNo ratings yet

- Issues in Corporate GovernanceDocument15 pagesIssues in Corporate GovernanceVandana ŘwţNo ratings yet

- Chapter 13-Planning For The Harvest: True/FalseDocument17 pagesChapter 13-Planning For The Harvest: True/FalseKhang ToNo ratings yet

- Financing S&S Air's Expansion PlansDocument6 pagesFinancing S&S Air's Expansion Plansmone2222100% (1)

- Conventional Versus Non Conventional Cash4079Document10 pagesConventional Versus Non Conventional Cash4079Amna SaeedNo ratings yet

- Corporate Reporting-1Document69 pagesCorporate Reporting-1Najmul IslamNo ratings yet

- Core Principles and Applications of Corporate Finance: Stephen A. RossDocument12 pagesCore Principles and Applications of Corporate Finance: Stephen A. RossAHMED MOHAMED YUSUFNo ratings yet

- ACCA PAPER P4 Advanced Financial Management Module 2Document50 pagesACCA PAPER P4 Advanced Financial Management Module 2123ramboNo ratings yet

- Problem Set #2-Solutions PDFDocument4 pagesProblem Set #2-Solutions PDFLhorene Hope DueñasNo ratings yet

- Du Pont AnalysisDocument5 pagesDu Pont AnalysisBindal HeenaNo ratings yet

- The Dilemma at Day 21Document4 pagesThe Dilemma at Day 21Christian AndreNo ratings yet

- Core and Principle of Corporate FinanceDocument12 pagesCore and Principle of Corporate FinancePermata Ayu WidyasariNo ratings yet

- Chapter 6Document26 pagesChapter 6dshilkarNo ratings yet

- Chapter 2: Stock Investments - Investor Accounting and ReportingDocument36 pagesChapter 2: Stock Investments - Investor Accounting and Reportingnikitarani kikiNo ratings yet

- Case Study of WiproDocument2 pagesCase Study of WiproAbhi ThakurNo ratings yet

- George Foster Financial Statement AnalysisDocument2 pagesGeorge Foster Financial Statement AnalysisdnesudhudhNo ratings yet

- Final Thesis IntanDocument77 pagesFinal Thesis IntanKarina RusmanNo ratings yet

- Family Business Succession A Strategic Planning ModelDocument4 pagesFamily Business Succession A Strategic Planning Modelleopedrazac22No ratings yet

- Chapter 4Document17 pagesChapter 4RBNo ratings yet

- On IFRS, US GAAP and Indian GAAPDocument64 pagesOn IFRS, US GAAP and Indian GAAPrishipath100% (1)

- Chapter 10: Managerial Planning and Control: International Accounting, 6/eDocument25 pagesChapter 10: Managerial Planning and Control: International Accounting, 6/eapi-241660930100% (1)

- Chapter 003 Financial Analysis: True / False QuestionsDocument54 pagesChapter 003 Financial Analysis: True / False QuestionsWinnie GiveraNo ratings yet

- Jan 2018Document34 pagesJan 2018alekhya manneNo ratings yet

- Ch09 Solations Brigham 10th EDocument12 pagesCh09 Solations Brigham 10th ERafay HussainNo ratings yet

- The Human Resource Department of Nestlé Bangladesh Limited and Its Essential Functions and ActivitiesDocument58 pagesThe Human Resource Department of Nestlé Bangladesh Limited and Its Essential Functions and ActivitiesVishesh ShuklaNo ratings yet

- Debt RatioDocument7 pagesDebt RatioAamir BilalNo ratings yet

- Chapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetDocument17 pagesChapter 16 Budgeting Capital Expenditures Research and Development Expenditures and Cash Pert Cost The Flexible BudgetZunaira ButtNo ratings yet

- Cash Flow Estimation BrighamDocument77 pagesCash Flow Estimation BrighamDianne GalarosaNo ratings yet

- Case Study Ratio AnalysisDocument6 pagesCase Study Ratio Analysisash867240% (1)

- Corporate Financial Analysis with Microsoft ExcelFrom EverandCorporate Financial Analysis with Microsoft ExcelRating: 5 out of 5 stars5/5 (1)

- Guide to Management Accounting CCC (Cash Conversion Cycle) for managersFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for managersNo ratings yet

- Do You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessFrom EverandDo You Want to Be a Digital Entrepreneur? What You Need to Know to Start and Protect Your Knowledge-Based Digital BusinessNo ratings yet

- Problem 1: Cash Flow Statement (Class Practice)Document2 pagesProblem 1: Cash Flow Statement (Class Practice)ronamiNo ratings yet

- Case 2 Performance Management at Vitality Health Enterprises PDFDocument2 pagesCase 2 Performance Management at Vitality Health Enterprises PDFAshekin MahadiNo ratings yet

- Mgt489 Final Group Report - Udoy Das 1Document24 pagesMgt489 Final Group Report - Udoy Das 1Ashekin MahadiNo ratings yet

- Mid ID#2035038#Md. Hazrat AliDocument11 pagesMid ID#2035038#Md. Hazrat AliAshekin MahadiNo ratings yet

- This Study Resource Was: Performance Management at Vitality Health IncDocument3 pagesThis Study Resource Was: Performance Management at Vitality Health IncAshekin MahadiNo ratings yet

- CF 12th Edition Chapter 02Document38 pagesCF 12th Edition Chapter 02Ashekin MahadiNo ratings yet

- Comtemporary Issues in LeadershipDocument12 pagesComtemporary Issues in LeadershipAshekin MahadiNo ratings yet

- Case Study Vitality Health Discussion Questions 2 PDFDocument2 pagesCase Study Vitality Health Discussion Questions 2 PDFAshekin MahadiNo ratings yet

- Chapter 1Document16 pagesChapter 1Ashekin MahadiNo ratings yet

- Assignment EMB660Document11 pagesAssignment EMB660Ashekin MahadiNo ratings yet

- RWJ Chapter 1 Introduction To Corporate FinanceDocument21 pagesRWJ Chapter 1 Introduction To Corporate FinanceAshekin Mahadi100% (1)

- RWJ Chapter 4 DCF ValuationDocument47 pagesRWJ Chapter 4 DCF ValuationAshekin MahadiNo ratings yet

- 5 Written Questions: Type Your AnswerDocument4 pages5 Written Questions: Type Your AnswerAshekin MahadiNo ratings yet

- 3 Written Questions: Type Your AnswerDocument3 pages3 Written Questions: Type Your AnswerAshekin MahadiNo ratings yet

- Test - Leadership - 123 QuizletDocument7 pagesTest - Leadership - 123 QuizletAshekin MahadiNo ratings yet

- Full Ifrs Vs SmeDocument6 pagesFull Ifrs Vs SmeMina ValenciaNo ratings yet

- Balance Sheet & Profit LossDocument7 pagesBalance Sheet & Profit LossJenny Davidson50% (2)

- Financial Accounting 1 Lesson 3 - SO1 Double Entry - RecordingDocument35 pagesFinancial Accounting 1 Lesson 3 - SO1 Double Entry - RecordingZudjian WarriorNo ratings yet

- Government Accounting Overview: Korbel Foundation College, IncDocument16 pagesGovernment Accounting Overview: Korbel Foundation College, IncRuby Amor DoligosaNo ratings yet

- Long Quiz 2Document8 pagesLong Quiz 2CattleyaNo ratings yet

- Accounting RatiosDocument5 pagesAccounting RatiosNaga NikhilNo ratings yet

- List of 30 Highest Dividend Paying Stocks in IndiaDocument5 pagesList of 30 Highest Dividend Paying Stocks in IndiaPankajNo ratings yet

- Analysis of The Estimation of Working Capital of Bajaj Finance Using TheDocument6 pagesAnalysis of The Estimation of Working Capital of Bajaj Finance Using TheRamasayi GummadiNo ratings yet

- June 2009 AnsDocument16 pagesJune 2009 AnsMacRen Bruce100% (1)

- Partnership Final Accounts PDFDocument97 pagesPartnership Final Accounts PDFKaushik Patel75% (4)

- Chapter 10 SolutionsDocument70 pagesChapter 10 SolutionsLy VõNo ratings yet

- FR 2019 Paper FinalDocument58 pagesFR 2019 Paper FinalshashalalaxiangNo ratings yet

- Balance Sheet As of December 2018: JL - Karapitan No.140 BandungDocument1 pageBalance Sheet As of December 2018: JL - Karapitan No.140 BandungNurul patimahNo ratings yet

- Deprival Value Lecture NotesDocument7 pagesDeprival Value Lecture NotesTosin YusufNo ratings yet

- Accounting - An Information Process Accounting - An Information ProcessDocument58 pagesAccounting - An Information Process Accounting - An Information ProcessBernadette Cunanan RamosNo ratings yet

- Chapter 1 Overview of CostDocument13 pagesChapter 1 Overview of Costnewaybeyene5No ratings yet

- Solved Suppose Morrison Corp S Breakeven Point Is Revenues of 1 100 000 Fixed CostsDocument1 pageSolved Suppose Morrison Corp S Breakeven Point Is Revenues of 1 100 000 Fixed CostsAnbu jaromiaNo ratings yet

- LOVISA V PANDORA FINANCIAL ANALYSIS RATIODocument30 pagesLOVISA V PANDORA FINANCIAL ANALYSIS RATIOpipahNo ratings yet

- Ase20093 01 Results Mark Scheme 20220629 April 2022 SeriesDocument18 pagesAse20093 01 Results Mark Scheme 20220629 April 2022 SeriesEi Ei TheintNo ratings yet

- Excercises MA 2023 1Document4 pagesExcercises MA 2023 1fin.minhtringuyenNo ratings yet

- Week 1 Review of Accounting BasicsDocument34 pagesWeek 1 Review of Accounting BasicsGokul KumarNo ratings yet

- Chapter 9 Notes Question Amp SolutionsDocument5 pagesChapter 9 Notes Question Amp SolutionsPankhuri SinghalNo ratings yet

- Fundamental Concepts of Managerial AccountingDocument45 pagesFundamental Concepts of Managerial AccountingCarlo CanlasNo ratings yet

- Ppe ExerciseDocument8 pagesPpe ExerciseNajihah NordinNo ratings yet

- ch1 Slides Students - ANDocument24 pagesch1 Slides Students - ANakshitnagpal9119No ratings yet

- IAS 38 Intangible AssetsDocument41 pagesIAS 38 Intangible AssetsAbdul RehmanNo ratings yet