Download as docx, pdf, or txt

You might also like

- Stock Exchanges - Function, Organisation, Method of TrainingDocument12 pagesStock Exchanges - Function, Organisation, Method of TrainingSahida ParveenNo ratings yet

- Form CPFLMDocument4 pagesForm CPFLMKrishnan JayaramanNo ratings yet

- Customs ActDocument43 pagesCustoms ActAbhishek AgarwalNo ratings yet

- Foreign Trade Policy: - Listing and Describing of Incentives Provided For Exports FromDocument9 pagesForeign Trade Policy: - Listing and Describing of Incentives Provided For Exports FromShubham SinghNo ratings yet

- Export Promotion SchemesDocument3 pagesExport Promotion SchemesJyotiChothwaniNo ratings yet

- India Export PromotionDocument8 pagesIndia Export PromotionUdit PradeepNo ratings yet

- Export Import Policy of IndiaDocument34 pagesExport Import Policy of IndiabarkhavermaNo ratings yet

- Export Certification AgenciesDocument14 pagesExport Certification AgenciespardeepNo ratings yet

- Principles of Taxation Law Internal AssignmentDocument23 pagesPrinciples of Taxation Law Internal AssignmentJakeNo ratings yet

- Financing Methods For Import of Capital Goods in India: Presented By, S.K.Aneesha Iimbaa 11PBA108Document13 pagesFinancing Methods For Import of Capital Goods in India: Presented By, S.K.Aneesha Iimbaa 11PBA108Aneesha KasimNo ratings yet

- Basic Constitutional Provisions Regarding Regulation of Business in IndiaDocument11 pagesBasic Constitutional Provisions Regarding Regulation of Business in Indiamonirba48100% (1)

- How To Start A Firm in IndiaDocument15 pagesHow To Start A Firm in IndiaAnonymous bAoFyANo ratings yet

- Com.Document24 pagesCom.MALAYALY100% (1)

- Export Promotion: By: Rajeev Kumar Ap NitkDocument24 pagesExport Promotion: By: Rajeev Kumar Ap NitkPriyanka AnejaNo ratings yet

- Import Export BusinessDocument14 pagesImport Export BusinessOmkar HindujaNo ratings yet

- TrainingDocument35 pagesTrainingAshok Kumar100% (2)

- Summer Report On Import Export ProcedureDocument56 pagesSummer Report On Import Export ProcedureBalakrishna ChakaliNo ratings yet

- Ambush MarketingDocument11 pagesAmbush MarketingShailesh GururaniNo ratings yet

- Exim PolicyDocument21 pagesExim PolicyRitu RanjanNo ratings yet

- Tybbi Fra TheoryDocument5 pagesTybbi Fra TheoryNavin Saraf100% (1)

- Typical Job Description Import - Export - ManagerDocument2 pagesTypical Job Description Import - Export - ManagerHOSAM HUSSEINNo ratings yet

- Export and Import FinanceDocument16 pagesExport and Import FinanceFebin.Simon1820 MBANo ratings yet

- BBK Electronics Strategy - Oppo, Vivo, OnePlus, Realme - Pritesh Pawar PDFDocument14 pagesBBK Electronics Strategy - Oppo, Vivo, OnePlus, Realme - Pritesh Pawar PDFsachinchoupalNo ratings yet

- Currency Convertibility and Its Impact On BOPDocument34 pagesCurrency Convertibility and Its Impact On BOPAditya Avasare100% (3)

- Raymond Brochure FY20Document39 pagesRaymond Brochure FY20ShivangiNo ratings yet

- BoP, CAD and Fiscal DeficitDocument10 pagesBoP, CAD and Fiscal DeficitPalak MehtaNo ratings yet

- Case IDocument4 pagesCase IVivek Patil0% (1)

- 9 Role of Customs in Regulating International TradeDocument36 pages9 Role of Customs in Regulating International Tradesukriti bajpaiNo ratings yet

- Institutional Set Up For Export Promotion in IndiaDocument7 pagesInstitutional Set Up For Export Promotion in IndiaSammir MalhotraNo ratings yet

- Concep To Export PromotionDocument30 pagesConcep To Export PromotionshailendraNo ratings yet

- Unit 1 Electronic Commerce: What Is E-Commerce Explain The Types of E-Commerce?Document53 pagesUnit 1 Electronic Commerce: What Is E-Commerce Explain The Types of E-Commerce?Mustafa TatiwalaNo ratings yet

- Buy-Back of SharesDocument19 pagesBuy-Back of SharesChirag VashishtaNo ratings yet

- Evaluation of EDPDocument33 pagesEvaluation of EDPKiran Gujamagadi100% (1)

- Export and Import ManagementDocument29 pagesExport and Import Managementcatchrekhacool100% (6)

- FEMADocument51 pagesFEMAChinmay Shirsat50% (2)

- Export Trade CycleDocument4 pagesExport Trade Cyclepankaj_desarda100% (1)

- Management Notes 1Document104 pagesManagement Notes 1Swati RajNo ratings yet

- Placement Process-For PPT and BroucherDocument7 pagesPlacement Process-For PPT and BroucherGurpreet SharmaNo ratings yet

- The Companies Act, 2013Document152 pagesThe Companies Act, 2013sheharban sulaimanNo ratings yet

- Export ManagementDocument34 pagesExport ManagementAkram Islam50% (2)

- 1.1 Export Import of India and Classification (Audio)Document33 pages1.1 Export Import of India and Classification (Audio)Abhishek kumarNo ratings yet

- The Comprehensive Analysis of Mcdowells No1Document46 pagesThe Comprehensive Analysis of Mcdowells No1Pradipta Mukherjee100% (1)

- Investment in Tax Saving Products An Overview: Year of Submission: June, 2020Document66 pagesInvestment in Tax Saving Products An Overview: Year of Submission: June, 2020Mruna TupeNo ratings yet

- India GST For Beginners by Jayaram Hiregange, Deepak RaoDocument108 pagesIndia GST For Beginners by Jayaram Hiregange, Deepak Raonarasimma8313No ratings yet

- NISM Series XIXA Alternative Investment Fund Category I and II Distributors Workbook Jan 2021Document263 pagesNISM Series XIXA Alternative Investment Fund Category I and II Distributors Workbook Jan 2021jackhack220No ratings yet

- Imports and ExportsDocument8 pagesImports and Exportssuresh yadavNo ratings yet

- HEC Group of Institutions, HARIDWARDocument12 pagesHEC Group of Institutions, HARIDWARSamarth AgarwalNo ratings yet

- Case Study - VCDocument5 pagesCase Study - VCapi-3865133No ratings yet

- Business CycleDocument39 pagesBusiness CycleTanmayThakurNo ratings yet

- Eic FrameworkDocument8 pagesEic FrameworkRiyaNo ratings yet

- Land Reforms in KarnatakaDocument15 pagesLand Reforms in Karnatakapshettigar142No ratings yet

- Iso Systems, Value Engineering and AnalysisDocument24 pagesIso Systems, Value Engineering and AnalysisamitNo ratings yet

- Investment Decision and Portfolio ManagementDocument35 pagesInvestment Decision and Portfolio Managementtarunasha50% (2)

- Essentials of KTPP Act & Rules-1Document34 pagesEssentials of KTPP Act & Rules-1Ravi Kanth M NNo ratings yet

- Export Incentive SchemesDocument7 pagesExport Incentive Schemesnavneet bagriNo ratings yet

- EXIM Project Same But DifferentDocument10 pagesEXIM Project Same But DifferentjajeguviNo ratings yet

- Export IncentivesDocument14 pagesExport IncentivesDhananjana Joshi100% (1)

- How Do Export Incentives Work in IndiaDocument4 pagesHow Do Export Incentives Work in Indiarsharma2910No ratings yet

- Foreign Trade Policy (2015-2020)Document17 pagesForeign Trade Policy (2015-2020)Neha RawalNo ratings yet

- Export IncentivesDocument15 pagesExport IncentivesKarmjit KaurNo ratings yet

- CC F 09052022Document4 pagesCC F 09052022siddhant kohliNo ratings yet

- List of Boiler Manufacturer 2021Document64 pagesList of Boiler Manufacturer 2021siddhant kohli71% (7)

- A Literature Review of Inter-Organizational Sustainability LearningDocument52 pagesA Literature Review of Inter-Organizational Sustainability Learningsiddhant kohliNo ratings yet

- Group4 JSW Energy BC2Document16 pagesGroup4 JSW Energy BC2siddhant kohliNo ratings yet

- Barbeque Nation Hospitality Limited DRHP CompressedDocument515 pagesBarbeque Nation Hospitality Limited DRHP Compressedsiddhant kohliNo ratings yet

- Deforestation in The Hudson River ValleyDocument14 pagesDeforestation in The Hudson River Valleysiddhant kohliNo ratings yet

- Difference Between Logistics and Supply Chain ManagementDocument3 pagesDifference Between Logistics and Supply Chain Managementsiddhant kohliNo ratings yet

- DebateDocument4 pagesDebatesiddhant kohliNo ratings yet

- Chapter 24 Forex OperationsDocument23 pagesChapter 24 Forex Operationsubaid reshiNo ratings yet

- Wellhead Systems: WFT Product CatalogDocument22 pagesWellhead Systems: WFT Product CatalogfarajNo ratings yet

- Learn & Earn Mother CandleDocument3 pagesLearn & Earn Mother CandleSATISHNo ratings yet

- OPERATIONS - SAMPLE OPERATION - Lending BusinessDocument48 pagesOPERATIONS - SAMPLE OPERATION - Lending BusinessRizzaniel BalagotNo ratings yet

- Grade 7 Social StudiesDocument4 pagesGrade 7 Social StudiesGedefaye AdemeNo ratings yet

- PAT Bahasa Inggris Kelas 5 Semester 2 2018 - 2019Document4 pagesPAT Bahasa Inggris Kelas 5 Semester 2 2018 - 2019Rifky Sucipta Soemodilogo100% (1)

- Company Profile PT MASDocument14 pagesCompany Profile PT MASIchsan NNNo ratings yet

- Chapter-5: Replacement AnalysisDocument16 pagesChapter-5: Replacement Analysisprakash pantaNo ratings yet

- Agriculture Vision 2020Document10 pagesAgriculture Vision 20202113713 PRIYANKANo ratings yet

- Secte Du Crane PDFDocument5 pagesSecte Du Crane PDFluminico88No ratings yet

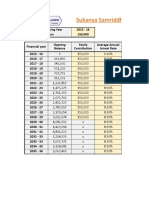

- Sukanya Samriddhi Yojana - CalculatorDocument4 pagesSukanya Samriddhi Yojana - CalculatorIndiran100% (1)

- International Handbook On Teaching and Learning Economics by Gail Mitchell HoytDocument894 pagesInternational Handbook On Teaching and Learning Economics by Gail Mitchell HoytKannan RangaswamiNo ratings yet

- DSGV SME Diagnosis 2019Document44 pagesDSGV SME Diagnosis 2019BodNo ratings yet

- Wondoor BrochureDocument8 pagesWondoor BrochureRahul SrivastavaNo ratings yet

- Foreign Currency TranslationDocument38 pagesForeign Currency TranslationAnmol GulatiNo ratings yet

- Long-Run Consequences of Stabilization PoliciesDocument7 pagesLong-Run Consequences of Stabilization PoliciesPinkyNo ratings yet

- Accounts and Audit of CompanyDocument17 pagesAccounts and Audit of CompanyPriyanshu RaiNo ratings yet

- Poverty Is General Scarcity or The State of One Who Lacks A Certain Amount of Material Possessions or MoneyDocument41 pagesPoverty Is General Scarcity or The State of One Who Lacks A Certain Amount of Material Possessions or MoneyChristian Cañon GenterolaNo ratings yet

- Self-Confidence of Mid-Victorian Age-ArticleDocument4 pagesSelf-Confidence of Mid-Victorian Age-ArticleAdrien BaziretNo ratings yet

- TCS Placement Papers PDF Download 2018 - 2019Document18 pagesTCS Placement Papers PDF Download 2018 - 2019Ashwin KumarNo ratings yet

- Anjle 193 R 2Document1 pageAnjle 193 R 2Mahesh KumarNo ratings yet

- SS Sample Paper 30 UnsolvedDocument8 pagesSS Sample Paper 30 Unsolvedmathavanmuthuraja2005No ratings yet

- Tata Sampoorna Raksha BrochureDocument8 pagesTata Sampoorna Raksha BrochureAnon AnonNo ratings yet

- The Government Game Student WorksheetDocument3 pagesThe Government Game Student WorksheetAnuj Singh BhadoriyaNo ratings yet

- InvoiceDocument1 pageInvoiceManishNo ratings yet

- Case Econ08 PPT 20Document34 pagesCase Econ08 PPT 20Devy RamadhaniNo ratings yet

- Teaching PowerPoint Slides - Chapter 1Document24 pagesTeaching PowerPoint Slides - Chapter 1famin87No ratings yet

- Komin Et Al 2020 COVID 19 and Its Impact On Informal Sector Workers A Case Study of ThailandDocument10 pagesKomin Et Al 2020 COVID 19 and Its Impact On Informal Sector Workers A Case Study of ThailandNURUL HAZWANI BINTI ABU BAKARNo ratings yet

- Minimum Acceptable Rate of ReturnDocument17 pagesMinimum Acceptable Rate of ReturnRalph Galvez100% (1)

- Circular 26 - 2023 21062023Document1 pageCircular 26 - 2023 21062023SueNo ratings yet