Download as docx, pdf, or txt

You might also like

- Daily Food CostDocument17 pagesDaily Food CostMuhammad Salihin Jaafar82% (11)

- Class 12 Accounts CA Parag GuptaDocument368 pagesClass 12 Accounts CA Parag GuptaJoel Varghese0% (1)

- Chapter 6 PPT (AIS - James Hall)Document9 pagesChapter 6 PPT (AIS - James Hall)Nur-aima MortabaNo ratings yet

- Chapter 2 Guarantee To PartnersDocument5 pagesChapter 2 Guarantee To PartnersAparna PNo ratings yet

- CBSE Class 12 Accountancy Accounting For Partnership Firms Sure Shot QuestionsDocument6 pagesCBSE Class 12 Accountancy Accounting For Partnership Firms Sure Shot Questionsdakshrwt06No ratings yet

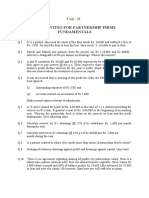

- Unit 2 Partmership Firms FundamentsDocument10 pagesUnit 2 Partmership Firms FundamentsSunlight SirSundeepNo ratings yet

- PartnershipDocument10 pagesPartnershipdora76pataNo ratings yet

- Screenshot 2023-08-14 at 1.31.19 PMDocument4 pagesScreenshot 2023-08-14 at 1.31.19 PMEri ChaNo ratings yet

- RERETESTDocument4 pagesRERETESTshveta0% (1)

- Long Answer Type QuestionDocument75 pagesLong Answer Type Questionincome taxNo ratings yet

- Account Ch-1 Partnership Firm - FundamentalsDocument19 pagesAccount Ch-1 Partnership Firm - Fundamentalsapsonline8585No ratings yet

- Introduction To Partnership AccountsDocument20 pagesIntroduction To Partnership Accountsanon_672065362100% (1)

- Partnership Fundamental 12 (2023)Document3 pagesPartnership Fundamental 12 (2023)Hansika SahuNo ratings yet

- CTF Edited Solved Paper 1Document2 pagesCTF Edited Solved Paper 1Umesh JaiswalNo ratings yet

- 12 Accountancy 2023-24Document37 pages12 Accountancy 2023-24chiragdahiya0602No ratings yet

- Monthly Test - Acc. Aug 2020Document5 pagesMonthly Test - Acc. Aug 2020akash debbarmaNo ratings yet

- Accounting For Partnership Firms - Fundamentals (Revision)Document4 pagesAccounting For Partnership Firms - Fundamentals (Revision)pratham bhagatNo ratings yet

- Class - XII CommerceDocument8 pagesClass - XII CommercehardikNo ratings yet

- Aaaccountancy Ques Paper001Document5 pagesAaaccountancy Ques Paper001sudarshanjha.0001No ratings yet

- ACCOUNTANCY - II MID - Quastion PaperDocument6 pagesACCOUNTANCY - II MID - Quastion PaperveenaNo ratings yet

- Xii Comm Holiday Homework 2020 23Document44 pagesXii Comm Holiday Homework 2020 23Mohit SuryavanshiNo ratings yet

- TB Meningitis Fact Sheet Dec 2017Document13 pagesTB Meningitis Fact Sheet Dec 2017Brix ArriolaNo ratings yet

- STD: 12 First Term MARKS:100 Subject: Accounts Duration:3 HrsDocument4 pagesSTD: 12 First Term MARKS:100 Subject: Accounts Duration:3 HrsAayush PatelNo ratings yet

- Accounts WorksheetDocument3 pagesAccounts Worksheetneeraj sharmaNo ratings yet

- Chapter 2 Capital Account SumsDocument9 pagesChapter 2 Capital Account SumsAparna PNo ratings yet

- 12th MCQDocument17 pages12th MCQkalpbhatia9898No ratings yet

- FND Partnership QuestionDocument3 pagesFND Partnership QuestionShweta BhadauriaNo ratings yet

- Accountancy PB 1 Mock Test PaperDocument10 pagesAccountancy PB 1 Mock Test PaperUjwal Anish ReddyNo ratings yet

- RKG Imp Q (CH 1 & 2) DoneDocument3 pagesRKG Imp Q (CH 1 & 2) Donepriyanshi.bansal25No ratings yet

- FundamentalDocument4 pagesFundamentalPainNo ratings yet

- Accountancy Ques PaperDocument5 pagesAccountancy Ques Papersudarshanjha.0001No ratings yet

- Accounts..std 12Document3 pagesAccounts..std 12Abhishek SharmaNo ratings yet

- Read The Following Hypothetical Text and Answer The Given QuestionsDocument2 pagesRead The Following Hypothetical Text and Answer The Given QuestionsShreekumar MaheshwariNo ratings yet

- RKG Accounts Fundamentals TestDocument4 pagesRKG Accounts Fundamentals TestlovikalarwedswithsNo ratings yet

- 12 Accounts Imp Ch1Document22 pages12 Accounts Imp Ch1Tushar Tyagi100% (1)

- 3hr Paper 4feb 2010Document3 pages3hr Paper 4feb 2010Bhawna BhardwajNo ratings yet

- REVISION 2022 Part A - CH. 2Document5 pagesREVISION 2022 Part A - CH. 2ADAM ABDUL RAZACKNo ratings yet

- Term One Accountancy 12 QP & MSDocument13 pagesTerm One Accountancy 12 QP & MSVarun HurriaNo ratings yet

- 11 Sample PaperDocument40 pages11 Sample Papergaming loverNo ratings yet

- Screenshot 2023-03-11 at 12.52.38 PM PDFDocument56 pagesScreenshot 2023-03-11 at 12.52.38 PM PDFpalak sanghviNo ratings yet

- Assignment On Fundamentals of PartnershipDocument8 pagesAssignment On Fundamentals of Partnershipsainimanish170gmailc100% (1)

- Goodwill: ICM 12 Standard Gautam BeryDocument9 pagesGoodwill: ICM 12 Standard Gautam BeryGautam KhanwaniNo ratings yet

- Accountancy Unit Test 2 - WorksheetDocument12 pagesAccountancy Unit Test 2 - WorksheetFawaz YoosefNo ratings yet

- Economics Pa 1 Class IXDocument2 pagesEconomics Pa 1 Class IXidealNo ratings yet

- G Awa Mil 5 D ADIi FZ DJ HV ADocument10 pagesG Awa Mil 5 D ADIi FZ DJ HV APriyankadevi PrabuNo ratings yet

- Test-chapter-1-Accountancy 12Document5 pagesTest-chapter-1-Accountancy 12Umesh JaiswalNo ratings yet

- Fundamentals Test (17!05!24)Document4 pagesFundamentals Test (17!05!24)MAHEE SHREE MITTALNo ratings yet

- UT_1_PAPER_class_12_SET_A__2024-2025_-Document5 pagesUT_1_PAPER_class_12_SET_A__2024-2025_-deshrajsharma488No ratings yet

- Accounts Holiday HW 1Document4 pagesAccounts Holiday HW 1AlishbaNo ratings yet

- Assessement Test 5 - Admission of PartnerDocument2 pagesAssessement Test 5 - Admission of PartnerShreya PushkarnaNo ratings yet

- Fundamentals of Partnership QuestionsDocument1 pageFundamentals of Partnership Questionsvandu.rekhiNo ratings yet

- Partnership QuestionsDocument11 pagesPartnership QuestionsTRIPTI GUPTANo ratings yet

- Class 12th Paper 2017Document4 pagesClass 12th Paper 2017AkankshaNo ratings yet

- Delhi Public School: ACCOUNTANCY - (Subject Code: 055)Document4 pagesDelhi Public School: ACCOUNTANCY - (Subject Code: 055)AbhishekNo ratings yet

- 12 Account SP 01 PDFDocument24 pages12 Account SP 01 PDFJanvi KushwahaNo ratings yet

- Fundamentals Class Test 2023 1Document2 pagesFundamentals Class Test 2023 1roz.kandulnaNo ratings yet

- 12 Accountancy SQP 4Document11 pages12 Accountancy SQP 4KandaroliNo ratings yet

- 12 Accountancy Ch01 Test Paper 01 Profit and Loss AppropriationDocument3 pages12 Accountancy Ch01 Test Paper 01 Profit and Loss AppropriationHari SharmaNo ratings yet

- Sample Paper 2 G 12 - Accountancy - SUMMER BREAKDocument9 pagesSample Paper 2 G 12 - Accountancy - SUMMER BREAKpriya longaniNo ratings yet

- Xii Acct WDocument11 pagesXii Acct WFree Fire KingNo ratings yet

- Discussions Updated 24.03Document28 pagesDiscussions Updated 24.03rajawatswadheentaNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Peta 3RD QTR Marketing-Sy-21-22Document3 pagesPeta 3RD QTR Marketing-Sy-21-22Kevin GuinsisanaNo ratings yet

- Augustus Softwares Company ProfileDocument5 pagesAugustus Softwares Company ProfileKanishk SinghNo ratings yet

- Channel - Training,, Motivation and Evaluation and EvaluationDocument12 pagesChannel - Training,, Motivation and Evaluation and EvaluationsagarNo ratings yet

- Bus.-Finance LAS 7 QTR 2Document6 pagesBus.-Finance LAS 7 QTR 2lun zagaNo ratings yet

- AjantaDocument17 pagesAjanta156DEBOLINA GUPTANo ratings yet

- Final Project ReportDocument59 pagesFinal Project ReportAdnan HussainNo ratings yet

- Commissionerate of Municipality (CMA), Tamil Nadu Circular About Tender PublicityDocument4 pagesCommissionerate of Municipality (CMA), Tamil Nadu Circular About Tender PublicitykayalonthewebNo ratings yet

- DIB Question Apr 18Document17 pagesDIB Question Apr 18Engr. Thanvir AhmadNo ratings yet

- AI Activated Value Co Creation An Exploratory Stu 2022 Industrial MarketingDocument13 pagesAI Activated Value Co Creation An Exploratory Stu 2022 Industrial MarketingHesham Mohamed YassinNo ratings yet

- MCQ 202324 CibmDocument320 pagesMCQ 202324 Cibmanantthakur1017No ratings yet

- Business Plan - EazypayDocument7 pagesBusiness Plan - EazypayBuchi MadukaNo ratings yet

- Solution - 1.: Calculation of NPV and IrrDocument5 pagesSolution - 1.: Calculation of NPV and IrrVishal DudejaNo ratings yet

- Septiembre 2017 PDFDocument383 pagesSeptiembre 2017 PDFmmoreno_184442No ratings yet

- (2021.05.20) Project Star - Analyst Presentation QuantitativeDocument78 pages(2021.05.20) Project Star - Analyst Presentation QuantitativeVictor ChenNo ratings yet

- Head of Sector Strategy, Knowledge & Learning Unit : in BonnDocument5 pagesHead of Sector Strategy, Knowledge & Learning Unit : in Bonnayman akilNo ratings yet

- 3int - 2007 - Jun - QUS CAT T3Document10 pages3int - 2007 - Jun - QUS CAT T3asad19100% (1)

- Periodical Test EntrepreneurDocument2 pagesPeriodical Test EntrepreneurMiss RonaNo ratings yet

- AB-EB-Unlocking-Operational-Risk-Management-Empower-the-Front Line to-Effectively-Manage-RiskDocument12 pagesAB-EB-Unlocking-Operational-Risk-Management-Empower-the-Front Line to-Effectively-Manage-RiskSirak AynalemNo ratings yet

- The Innovation Value Chain in Advanced Developing Countries: An Empirical Study of Taiwanese Manufacturing IndustryDocument38 pagesThe Innovation Value Chain in Advanced Developing Countries: An Empirical Study of Taiwanese Manufacturing IndustryEmbuhmas BroNo ratings yet

- Purchase OrderDocument7 pagesPurchase OrderRisa IchaNo ratings yet

- ParCor ReviewerDocument6 pagesParCor Reviewerjhean dabatosNo ratings yet

- The Failure of NokiaDocument4 pagesThe Failure of NokiaVictoria Ortiz MoralesNo ratings yet

- Standar GajiDocument28 pagesStandar GajiDimi BerbaNo ratings yet

- Strategy - External EnvironmentDocument61 pagesStrategy - External EnvironmentAman SinhaNo ratings yet

- National Stock Exchange of India Limited Inspection Department CircularDocument4 pagesNational Stock Exchange of India Limited Inspection Department CircularHARISH GROVERNo ratings yet

- The Development of InsuranceDocument3 pagesThe Development of InsuranceMuhd RizzwanNo ratings yet

- MA332 - AGUANTA, PRINCESS NICOLE ALLYSON - Module 1 AssignmentDocument2 pagesMA332 - AGUANTA, PRINCESS NICOLE ALLYSON - Module 1 AssignmentNicole Allyson AguantaNo ratings yet

- Binary Options e BookDocument74 pagesBinary Options e BookDaniel Santos100% (1)