Download as pdf or txt

You might also like

- The Essentials of Finance and Accounting for Nonfinancial ManagersFrom EverandThe Essentials of Finance and Accounting for Nonfinancial ManagersRating: 5 out of 5 stars5/5 (1)

- Accounting QBDocument661 pagesAccounting QBTrang VũNo ratings yet

- Chapter 7 Introduction To Regular Income TaxDocument76 pagesChapter 7 Introduction To Regular Income TaxANGELU RANE BAGARES INTOLNo ratings yet

- Case 2 (1-4)Document6 pagesCase 2 (1-4)zikril94No ratings yet

- TBDocument31 pagesTBBenj LadesmaNo ratings yet

- Question and Answer - 3Document31 pagesQuestion and Answer - 3acc-expertNo ratings yet

- Manas Aren 1923224 Final Internship ReportDocument33 pagesManas Aren 1923224 Final Internship Reportmanas arenNo ratings yet

- Exercises of Financial AccountingDocument25 pagesExercises of Financial AccountingSai AlviorNo ratings yet

- Womens Shoe Store Business PlanDocument28 pagesWomens Shoe Store Business PlanShaikha S ADNo ratings yet

- 1801 - Estate Tax ReturnDocument2 pages1801 - Estate Tax ReturnErikajane BolimaNo ratings yet

- Individual Assignment 1A - Aisyah Nuralam 29123362Document4 pagesIndividual Assignment 1A - Aisyah Nuralam 29123362Aisyah NuralamNo ratings yet

- ACC 497 GENIUS Empowering and InspiringDocument34 pagesACC 497 GENIUS Empowering and Inspiringalbert0123No ratings yet

- ACC 497 GENIUS Possible Is EverythingDocument36 pagesACC 497 GENIUS Possible Is Everythingalbert0124No ratings yet

- Chapter 1Document33 pagesChapter 1mburford2006No ratings yet

- HHHHDocument6 pagesHHHHLester Jude Del RosarioNo ratings yet

- Test Bank-Ch01 PDFDocument5 pagesTest Bank-Ch01 PDFSamah Refa'tNo ratings yet

- Trident ACC 201 All Modules Case and SLP - LatestDocument17 pagesTrident ACC 201 All Modules Case and SLP - LatestamybrownNo ratings yet

- Conceptual Framework and Regulatory Framework: Put The Missing WordsDocument5 pagesConceptual Framework and Regulatory Framework: Put The Missing WordsKristenNo ratings yet

- ICAEW Financial Accounting Conceptual and Regulatory Frame WorkDocument40 pagesICAEW Financial Accounting Conceptual and Regulatory Frame WorkhopeaccaNo ratings yet

- Chapter 1 WWW Cases Case 1-7 International Issues: RequiredDocument17 pagesChapter 1 WWW Cases Case 1-7 International Issues: RequiredisnokukoNo ratings yet

- Auditing Arens 14e Chapter 1Document15 pagesAuditing Arens 14e Chapter 15starserviceNo ratings yet

- Reading 8 Intercorporate Investments - AnswersDocument52 pagesReading 8 Intercorporate Investments - AnswersNeerajNo ratings yet

- Chapter 1 - Test Bank Auditing UICDocument15 pagesChapter 1 - Test Bank Auditing UICLana Bustami100% (4)

- Chap 001Document19 pagesChap 001WilliamNo ratings yet

- Testing The Financial Literacy PDFDocument6 pagesTesting The Financial Literacy PDFPramendra7No ratings yet

- Jon ArcDocument5 pagesJon ArcScNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Question and Answer - 1Document31 pagesQuestion and Answer - 1acc-expertNo ratings yet

- Financial Accounting and Accounting StandardsDocument31 pagesFinancial Accounting and Accounting StandardsIrwan JanuarNo ratings yet

- Far KKHDocument35 pagesFar KKHkyawhtetNo ratings yet

- CH 01Document65 pagesCH 01Obeit TrianangNo ratings yet

- BE210 TMA Financial AccountingDocument9 pagesBE210 TMA Financial AccountingMuhammad Yaseen LakhaNo ratings yet

- Chapter 4Document27 pagesChapter 4Annalyn MolinaNo ratings yet

- Kap 1 5th Workbook Se CH 3Document20 pagesKap 1 5th Workbook Se CH 3DakshNo ratings yet

- Financial Accounting and Accounting Standards: Intermediate Accounting, 12th Edition Kieso, Weygandt, and WarfieldDocument31 pagesFinancial Accounting and Accounting Standards: Intermediate Accounting, 12th Edition Kieso, Weygandt, and WarfieldKarunia Utami100% (1)

- Intermediate FA I Mock Exam From Jimma UnvDocument49 pagesIntermediate FA I Mock Exam From Jimma UnvYordanos GetnetNo ratings yet

- Test Bank For New Zealand Financial Accounting 6th Edition by CraigDocument67 pagesTest Bank For New Zealand Financial Accounting 6th Edition by CraigCarolparker100% (1)

- Financial Reporting Disclosure Requirements AND Ethical ResponsibilitiesDocument44 pagesFinancial Reporting Disclosure Requirements AND Ethical ResponsibilitiesSamuel AritonangNo ratings yet

- FA-FFA September 2018 To August 2019Document7 pagesFA-FFA September 2018 To August 2019leylaNo ratings yet

- Chapter 1Document12 pagesChapter 1Na'Tashia Nicole HendersonNo ratings yet

- 20090531143401953Document26 pages20090531143401953kalechiru0% (2)

- A424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsDocument8 pagesA424: Chapter 6 Audit Responsibilities and Objectives Preparation QuestionsNovah Mae Begaso SamarNo ratings yet

- Cpa Sample TestDocument10 pagesCpa Sample TestAnuj Harshwardhan SharmaNo ratings yet

- Cga-Canada External Auditing (Au1) Examination June 2011 Marks Time: 3 HoursDocument14 pagesCga-Canada External Auditing (Au1) Examination June 2011 Marks Time: 3 Hoursyinghan2203031No ratings yet

- Acct 555 Audit Week 4 MidtermDocument6 pagesAcct 555 Audit Week 4 MidtermNatasha DeclanNo ratings yet

- Financial Rep Standards L1Document10 pagesFinancial Rep Standards L1heisenbergNo ratings yet

- Wiley - Chapter 1: Financial Accounting and Accounting StandardsDocument15 pagesWiley - Chapter 1: Financial Accounting and Accounting StandardsIvan BliminseNo ratings yet

- Fra1 CP1 - Q&aDocument4 pagesFra1 CP1 - Q&arafav10100% (1)

- ch17 Financial Reporting Desclosure Requirements and Ethical ResponsibilitiesDocument44 pagesch17 Financial Reporting Desclosure Requirements and Ethical Responsibilitiesmtarawneh941No ratings yet

- Full Download PDF of Test Bank For Auditing and Assurance Services, 14th Edition: Arens All ChapterDocument39 pagesFull Download PDF of Test Bank For Auditing and Assurance Services, 14th Edition: Arens All Chapterefawevlice100% (4)

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- Sen Finance Sen Finance Sen Finance Sen Finance: CFA® Level IDocument31 pagesSen Finance Sen Finance Sen Finance Sen Finance: CFA® Level IPavel LahaNo ratings yet

- Learning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesDocument14 pagesLearning Objective 1-1: Chapter 1 The Demand For Audit and Other Assurance ServicesMark ChouNo ratings yet

- CH 3 - The Statement of Financial Position and Financial DisclosuresDocument37 pagesCH 3 - The Statement of Financial Position and Financial DisclosuresZulqarnain KhokharNo ratings yet

- ExercisesDocument3 pagesExercisesAríesNo ratings yet

- Dip IFR Examiner ReportDocument11 pagesDip IFR Examiner Reportluckyjulie567No ratings yet

- Lectures - Acct 555Document64 pagesLectures - Acct 555PetraNo ratings yet

- Financial Statement Analysis and Valuation 4th Edition Easton Test BankDocument30 pagesFinancial Statement Analysis and Valuation 4th Edition Easton Test BankTroyKnappdpci100% (15)

- Intermediate Accounting Vol 1 Canadian 2nd Edition Lo Test BankDocument24 pagesIntermediate Accounting Vol 1 Canadian 2nd Edition Lo Test BankDarrylWoodsormni100% (17)

- L6 LG Financial Accounting Dec11Document14 pagesL6 LG Financial Accounting Dec11IamThe BossNo ratings yet

- 16 A Financial Reporting Standards - AnswersDocument6 pages16 A Financial Reporting Standards - AnswersNhi Cúnn'ssNo ratings yet

- Accounting for Goodwill and Other Intangible AssetsFrom EverandAccounting for Goodwill and Other Intangible AssetsRating: 4 out of 5 stars4/5 (1)

- International Financial Statement AnalysisFrom EverandInternational Financial Statement AnalysisRating: 1 out of 5 stars1/5 (1)

- Ch.13 Current Liabilities: Exercise 13.01 True or FalseDocument6 pagesCh.13 Current Liabilities: Exercise 13.01 True or FalseFaishal Alghi FariNo ratings yet

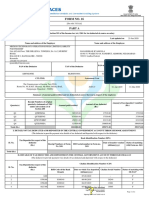

- Form No. 16: Part ADocument10 pagesForm No. 16: Part ARAJASHEKAR KYAROLLANo ratings yet

- C - 22 - Retained Earnings (Dividends, Appropriation, and Quasi-Reorganization) (PDocument14 pagesC - 22 - Retained Earnings (Dividends, Appropriation, and Quasi-Reorganization) (PJoyluxxiNo ratings yet

- Break Even Analysis and Managerial Decision Making: Barnali ChakladerDocument12 pagesBreak Even Analysis and Managerial Decision Making: Barnali ChakladerAshwin DalelaNo ratings yet

- WPC Assignment - FM CaseDocument6 pagesWPC Assignment - FM CaseAhmed AliNo ratings yet

- Accf3114 9Document10 pagesAccf3114 9Krishna 11No ratings yet

- Paper 7-Direct Taxation: Answer To MTP - Intermediate - Syllabus 2016 - June 2020 & December 2020 - Set 1Document21 pagesPaper 7-Direct Taxation: Answer To MTP - Intermediate - Syllabus 2016 - June 2020 & December 2020 - Set 1vikash guptaNo ratings yet

- SABA'SDocument17 pagesSABA'SAbnet BeleteNo ratings yet

- Cost Accounting: T I C A PDocument6 pagesCost Accounting: T I C A PShehrozSTNo ratings yet

- Journal EntryDocument8 pagesJournal EntryAnklesh kumar GuptaNo ratings yet

- Law of Direct TaxationDocument4 pagesLaw of Direct TaxationAshwanth M.SNo ratings yet

- Solutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnDocument84 pagesSolutions To Self-Study Problems: Chapter 1 The Individual Income Tax ReturnTiffy LouiseNo ratings yet

- Training in Difficult Choices: 5 Public Policy Case Studies From SlovakiaDocument101 pagesTraining in Difficult Choices: 5 Public Policy Case Studies From Slovakiascholar786No ratings yet

- Carbios 2022 Annual Results Presentation Vdef 1Document27 pagesCarbios 2022 Annual Results Presentation Vdef 1Med Raslene AlouiNo ratings yet

- 10 Column Worksheet TemplateDocument1 page10 Column Worksheet TemplateEmilia NatashaNo ratings yet

- Statement of Comprehensive Income ProblemsDocument2 pagesStatement of Comprehensive Income ProblemsDarlyn Dalida San PedroNo ratings yet

- FORMAT OF THE TRADING Account With The AdjustmentsDocument2 pagesFORMAT OF THE TRADING Account With The AdjustmentsTajay Kadeem ThomasNo ratings yet

- CHAPTER 2 Statement of Financial PositionDocument4 pagesCHAPTER 2 Statement of Financial PositionGee LacabaNo ratings yet

- Alpha Graphics Company Was Organized On January 1,...Document10 pagesAlpha Graphics Company Was Organized On January 1,...Saima NargisNo ratings yet

- UOP E Assignments: FIN 571 - FIN 571 Final Exam Answers FreeDocument12 pagesUOP E Assignments: FIN 571 - FIN 571 Final Exam Answers FreeuopeassignmentsNo ratings yet

- Data For FROM 1701Document3 pagesData For FROM 1701April Jane YadaoNo ratings yet

- Accounting Process: - The Accounting Process Is Expressed Through Following Stages (Functions) of AccountingDocument36 pagesAccounting Process: - The Accounting Process Is Expressed Through Following Stages (Functions) of AccountingPGNo ratings yet

- Earnings Price Anomaly (Ray Ball, 1992)Document27 pagesEarnings Price Anomaly (Ray Ball, 1992)jeetNo ratings yet

- ReasoningDocument80 pagesReasoningwork workNo ratings yet

- Instructions For Form 1040NR-EZ: Department of The TreasuryDocument11 pagesInstructions For Form 1040NR-EZ: Department of The TreasuryIRSNo ratings yet

- Organisation Study Report Jain UniversityDocument54 pagesOrganisation Study Report Jain Universityneekuj malik100% (1)