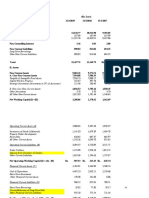

MK Financial Analysis Q2

MK Financial Analysis Q2

You might also like

- Resume of Suhas Karadkhedkar Civil Engineer Over 20 Years ExperienceDocument3 pagesResume of Suhas Karadkhedkar Civil Engineer Over 20 Years Experiencenksuhas191100% (5)

- W. W. Grainger, Inc., Is A Leading Supplier of Maintenance, Repair, and Operating (MRO) Products To Businesses and Institutions in The UnitedDocument3 pagesW. W. Grainger, Inc., Is A Leading Supplier of Maintenance, Repair, and Operating (MRO) Products To Businesses and Institutions in The UnitedJalaj GuptaNo ratings yet

- A Report On Silver River Manufacturing CompanyDocument59 pagesA Report On Silver River Manufacturing CompanyManish JaiswalNo ratings yet

- 2015 Part 2 Question Book CMA ExamDocument173 pages2015 Part 2 Question Book CMA ExamSwathi AshokNo ratings yet

- James Hall CH 1Document21 pagesJames Hall CH 1ANNE PAMELA TIUNo ratings yet

- PVH Financial Analysis - Q1Document7 pagesPVH Financial Analysis - Q1Dulakshi RanadeeraNo ratings yet

- Aditya Birla Fashion and Retail: Business Rebounds Impressively Records Highest Ever Standalone EBITDADocument3 pagesAditya Birla Fashion and Retail: Business Rebounds Impressively Records Highest Ever Standalone EBITDASuman SarkarNo ratings yet

- Performance Task 4 - Abm 12-2Document15 pagesPerformance Task 4 - Abm 12-2Pauleene AdelinoNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Management Report: Dear ShareholdersDocument2 pagesManagement Report: Dear ShareholdersCleyton AlvesNo ratings yet

- Business Management Assignment 121eDocument16 pagesBusiness Management Assignment 121eZowvuyour Zow Zow MazuluNo ratings yet

- V-Mart Retail R 02032020Document8 pagesV-Mart Retail R 02032020Yusuf MalikNo ratings yet

- AKR Industries 19mar2020Document8 pagesAKR Industries 19mar2020Karthikeyan RK Swamy100% (1)

- Group Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)Document8 pagesGroup Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)BonBonNo ratings yet

- Centuryply IP Q1FY24Document30 pagesCenturyply IP Q1FY24Sanjeev GoswamiNo ratings yet

- Arman F-Q2FY21Document22 pagesArman F-Q2FY21Forall PainNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Final H Investor Day Press ReleaseDocument9 pagesFinal H Investor Day Press ReleaseseanNo ratings yet

- Kalyan Jewellers India LTD IPO: All You Need To Know AboutDocument8 pagesKalyan Jewellers India LTD IPO: All You Need To Know AboutRaghul RaghulNo ratings yet

- Exercise Lecture 3Document3 pagesExercise Lecture 3ryanlee190502No ratings yet

- M12 Jun 21questionDocument8 pagesM12 Jun 21questionChoi WoNo ratings yet

- The Bombay Dyeing & Manufacturing Company LimitedDocument5 pagesThe Bombay Dyeing & Manufacturing Company LimitedvaishnaviNo ratings yet

- Senior High SchoolDocument9 pagesSenior High SchoolCharlyn CastroNo ratings yet

- Rating Action Moodys Downgrades Altice 15jun2023 PR 477712Document7 pagesRating Action Moodys Downgrades Altice 15jun2023 PR 477712xdemarleNo ratings yet

- PolarSports Solution PDFDocument8 pagesPolarSports Solution PDFaotorres99No ratings yet

- O.M. Scott & SonsDocument7 pagesO.M. Scott & Sonsstig2lufetNo ratings yet

- Draft CooperDocument3 pagesDraft CooperRitveek GargNo ratings yet

- NB Annual Report 2023Document72 pagesNB Annual Report 2023mad eye moodyNo ratings yet

- Financial Statement Analysis - Marks & SpencerDocument8 pagesFinancial Statement Analysis - Marks & Spencermuhammad.salmankhanofficial01No ratings yet

- Kitex Garments Limited - R - 11112020Document8 pagesKitex Garments Limited - R - 11112020Positive ThinkerNo ratings yet

- Tenda 4T23Document33 pagesTenda 4T23Flavya PereiraNo ratings yet

- Alliance ConcreteDocument11 pagesAlliance ConcreteAijaz AslamNo ratings yet

- Chapter 5 Financial Accounting LibbyDocument6 pagesChapter 5 Financial Accounting Libbymr. fiveNo ratings yet

- Cvs FinalpapermaheshDocument15 pagesCvs Finalpapermaheshnaikm3239No ratings yet

- Shareholder Letter Q3 2022 11.8.22 FINALDocument36 pagesShareholder Letter Q3 2022 11.8.22 FINALAlexNo ratings yet

- Irrecoverable Debts & Provision For Irrecoverables DebtsDocument5 pagesIrrecoverable Debts & Provision For Irrecoverables DebtsYomi AmvNo ratings yet

- Silver Crest Clothing Private LimitedDocument7 pagesSilver Crest Clothing Private Limitedsyedyaseenpasha9292No ratings yet

- Kota FibresDocument10 pagesKota FibresShishirNo ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- ACI Worldwide, Inc - ACIW - Q3 20Document10 pagesACI Worldwide, Inc - ACIW - Q3 20Saurabh SharmaNo ratings yet

- Tài Chính Công TyDocument14 pagesTài Chính Công Typttd154No ratings yet

- Barbeque Nation Hospitality LimitedDocument7 pagesBarbeque Nation Hospitality Limitednayabrasul208No ratings yet

- Champion Commercial Company LimitedDocument7 pagesChampion Commercial Company LimitedCedric KerkettaNo ratings yet

- Mohan Meakin LimitedDocument8 pagesMohan Meakin LimitedBithal PrasadNo ratings yet

- Case Study 1 Muhammad JanjuaDocument6 pagesCase Study 1 Muhammad JanjuaAmeer Hamza JanjuaNo ratings yet

- Sunsuria BHD (Written Report)Document6 pagesSunsuria BHD (Written Report)Monoliza PhilipsNo ratings yet

- SH-2023-Q4-1-ICRA-Housing Finance StatisticsDocument9 pagesSH-2023-Q4-1-ICRA-Housing Finance Statisticsshivay bhatejaNo ratings yet

- Khadim India Limited - ICRA Feb 2020 PDFDocument7 pagesKhadim India Limited - ICRA Feb 2020 PDFPuneet367No ratings yet

- Zaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Document23 pagesZaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Zaini ZainNo ratings yet

- Cash Flow StatementDocument5 pagesCash Flow Statementphamkhanh22072003No ratings yet

- 4Q20 Shareholder LetterDocument28 pages4Q20 Shareholder LettermfajsemNo ratings yet

- Zodiac Clothing Company Limited: Rating Revised To (ICRA) A2 From (ICRA) A2+ Summary of Rating ActionDocument8 pagesZodiac Clothing Company Limited: Rating Revised To (ICRA) A2 From (ICRA) A2+ Summary of Rating ActionmanenderNo ratings yet

- Ap A2.1Document15 pagesAp A2.1Minh PhíNo ratings yet

- Bank Decision MakingDocument3 pagesBank Decision Makingjob_deloitte7440No ratings yet

- Sakthi Finance Limited R 20022020Document9 pagesSakthi Finance Limited R 20022020Elan ChelianNo ratings yet

- BFM Group 1 AssignmentDocument30 pagesBFM Group 1 AssignmentnurinNo ratings yet

- P7int 2013 Jun A PDFDocument17 pagesP7int 2013 Jun A PDFhiruspoonNo ratings yet

- Godrej Properties LimitedDocument11 pagesGodrej Properties Limitedkitono5817No ratings yet

- FNNB213 Group AssignmentDocument12 pagesFNNB213 Group AssignmentSyazwan Lagenda Bola SepakNo ratings yet

- 2022-01-13 BAC 4Q Earnings CallDocument22 pages2022-01-13 BAC 4Q Earnings CallPeople PeopleNo ratings yet

- Science in Sport PLC Results 2022 RNS 29.06.23Document21 pagesScience in Sport PLC Results 2022 RNS 29.06.23a.andrade.egiNo ratings yet

- Big Bags International PVT LTDDocument7 pagesBig Bags International PVT LTDnayabrasul208No ratings yet

- Question 5 of 10 - Chapter 4 HomeworkDocument4 pagesQuestion 5 of 10 - Chapter 4 HomeworkDulakshi RanadeeraNo ratings yet

- TCP Financial Analysis Q1Document7 pagesTCP Financial Analysis Q1Dulakshi RanadeeraNo ratings yet

- PVH Financial Analysis - Q1Document7 pagesPVH Financial Analysis - Q1Dulakshi RanadeeraNo ratings yet

- Market Share Has Made The Biggest Leap: Winners and LosersDocument3 pagesMarket Share Has Made The Biggest Leap: Winners and LosersDulakshi RanadeeraNo ratings yet

- Department of Accountancy: Inventory EstimationDocument2 pagesDepartment of Accountancy: Inventory EstimationAiza S. Maca-umbosNo ratings yet

- Plant Simulation Fact Sheet Book HQ-ilovepdf-compressed PDFDocument87 pagesPlant Simulation Fact Sheet Book HQ-ilovepdf-compressed PDFМануэль МендосаNo ratings yet

- Job Costing: I. Learning ObjectivesDocument8 pagesJob Costing: I. Learning ObjectivesKerby Gail RulonaNo ratings yet

- Chapter 2 - Cost TermsDocument35 pagesChapter 2 - Cost TermsCarina Carollo MalinaoNo ratings yet

- The Balanced ScorecardDocument6 pagesThe Balanced ScorecardRamana VaitlaNo ratings yet

- Food and BeverageDocument35 pagesFood and BeverageLyn Escano50% (2)

- 5 Year Ratio Analysis For RENATA LIMITED PDFDocument47 pages5 Year Ratio Analysis For RENATA LIMITED PDFDhruv singhNo ratings yet

- Seven Eleven CaseDocument5 pagesSeven Eleven CaseKarthikSureshNo ratings yet

- Share Capital Other Equity: B. Non-Core Non-Current AssetsDocument17 pagesShare Capital Other Equity: B. Non-Core Non-Current AssetsAksa DindeNo ratings yet

- Stardew Valley CommandsDocument3 pagesStardew Valley Commandskun hajimeNo ratings yet

- Unit 1 - InventoriesDocument76 pagesUnit 1 - InventoriesZamarhadebe SilosamahlubiNo ratings yet

- IBM Maximo Asset Management V6.2 ImplementationDocument41 pagesIBM Maximo Asset Management V6.2 ImplementationtareqcccccNo ratings yet

- Full 2012 CatalogFFRDocument620 pagesFull 2012 CatalogFFRsixela19No ratings yet

- SCM - Idc, G25Document9 pagesSCM - Idc, G25kuldeep singhNo ratings yet

- Wilkins A Zurn Company Demand ForecastinDocument16 pagesWilkins A Zurn Company Demand ForecastinYogendra RathoreNo ratings yet

- Cost ClassificationDocument24 pagesCost ClassificationElla Mae IragaNo ratings yet

- Manual para Uso Del Sistema OperaDocument144 pagesManual para Uso Del Sistema Operadanarg2286No ratings yet

- Strategic Benefits of A Global Trade Management Software SystemDocument4 pagesStrategic Benefits of A Global Trade Management Software SystemSileaLaurentiuNo ratings yet

- SCM 2021 Supply Chain Distribution Network Design - Part 1Document33 pagesSCM 2021 Supply Chain Distribution Network Design - Part 1Vikash Kumar Ojha100% (1)

- ITT AutoDocument4 pagesITT AutoKarthik ArumughamNo ratings yet

- Materials ManagementDocument438 pagesMaterials ManagementnpunnyNo ratings yet

- Shukrullah Assignment No 2Document4 pagesShukrullah Assignment No 2Shukrullah JanNo ratings yet

- Acca f2 Notes j15Document188 pagesAcca f2 Notes j15opentuitionID100% (1)

- Quản Trị Mua HàngDocument28 pagesQuản Trị Mua Hànghoangtruc07902No ratings yet

- CMR Institute of Technology: A Project ReportDocument73 pagesCMR Institute of Technology: A Project ReportKishor KumarNo ratings yet

- Prestige Bella VistaDocument27 pagesPrestige Bella VistaArun RajagopalNo ratings yet

- Answers Chapter 5 Quiz.s13Document2 pagesAnswers Chapter 5 Quiz.s13qwerty17327No ratings yet

Download as docx, pdf, or txt

You might also like

- Resume of Suhas Karadkhedkar Civil Engineer Over 20 Years ExperienceDocument3 pagesResume of Suhas Karadkhedkar Civil Engineer Over 20 Years Experiencenksuhas191100% (5)

- W. W. Grainger, Inc., Is A Leading Supplier of Maintenance, Repair, and Operating (MRO) Products To Businesses and Institutions in The UnitedDocument3 pagesW. W. Grainger, Inc., Is A Leading Supplier of Maintenance, Repair, and Operating (MRO) Products To Businesses and Institutions in The UnitedJalaj GuptaNo ratings yet

- A Report On Silver River Manufacturing CompanyDocument59 pagesA Report On Silver River Manufacturing CompanyManish JaiswalNo ratings yet

- 2015 Part 2 Question Book CMA ExamDocument173 pages2015 Part 2 Question Book CMA ExamSwathi AshokNo ratings yet

- James Hall CH 1Document21 pagesJames Hall CH 1ANNE PAMELA TIUNo ratings yet

- PVH Financial Analysis - Q1Document7 pagesPVH Financial Analysis - Q1Dulakshi RanadeeraNo ratings yet

- Aditya Birla Fashion and Retail: Business Rebounds Impressively Records Highest Ever Standalone EBITDADocument3 pagesAditya Birla Fashion and Retail: Business Rebounds Impressively Records Highest Ever Standalone EBITDASuman SarkarNo ratings yet

- Performance Task 4 - Abm 12-2Document15 pagesPerformance Task 4 - Abm 12-2Pauleene AdelinoNo ratings yet

- Ratio Analysis: Mari Perolum Company LimitiedDocument5 pagesRatio Analysis: Mari Perolum Company LimitiedNuman AhmedNo ratings yet

- Management Report: Dear ShareholdersDocument2 pagesManagement Report: Dear ShareholdersCleyton AlvesNo ratings yet

- Business Management Assignment 121eDocument16 pagesBusiness Management Assignment 121eZowvuyour Zow Zow MazuluNo ratings yet

- V-Mart Retail R 02032020Document8 pagesV-Mart Retail R 02032020Yusuf MalikNo ratings yet

- AKR Industries 19mar2020Document8 pagesAKR Industries 19mar2020Karthikeyan RK Swamy100% (1)

- Group Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)Document8 pagesGroup Information: Dien Quang Lamp Joint Stock Company Công ty Cổ phần Bóng đèn Điện Quang (DQC)BonBonNo ratings yet

- Centuryply IP Q1FY24Document30 pagesCenturyply IP Q1FY24Sanjeev GoswamiNo ratings yet

- Arman F-Q2FY21Document22 pagesArman F-Q2FY21Forall PainNo ratings yet

- Sun Home Appliances Private - R - 25082020Document7 pagesSun Home Appliances Private - R - 25082020DarshanNo ratings yet

- Final H Investor Day Press ReleaseDocument9 pagesFinal H Investor Day Press ReleaseseanNo ratings yet

- Kalyan Jewellers India LTD IPO: All You Need To Know AboutDocument8 pagesKalyan Jewellers India LTD IPO: All You Need To Know AboutRaghul RaghulNo ratings yet

- Exercise Lecture 3Document3 pagesExercise Lecture 3ryanlee190502No ratings yet

- M12 Jun 21questionDocument8 pagesM12 Jun 21questionChoi WoNo ratings yet

- The Bombay Dyeing & Manufacturing Company LimitedDocument5 pagesThe Bombay Dyeing & Manufacturing Company LimitedvaishnaviNo ratings yet

- Senior High SchoolDocument9 pagesSenior High SchoolCharlyn CastroNo ratings yet

- Rating Action Moodys Downgrades Altice 15jun2023 PR 477712Document7 pagesRating Action Moodys Downgrades Altice 15jun2023 PR 477712xdemarleNo ratings yet

- PolarSports Solution PDFDocument8 pagesPolarSports Solution PDFaotorres99No ratings yet

- O.M. Scott & SonsDocument7 pagesO.M. Scott & Sonsstig2lufetNo ratings yet

- Draft CooperDocument3 pagesDraft CooperRitveek GargNo ratings yet

- NB Annual Report 2023Document72 pagesNB Annual Report 2023mad eye moodyNo ratings yet

- Financial Statement Analysis - Marks & SpencerDocument8 pagesFinancial Statement Analysis - Marks & Spencermuhammad.salmankhanofficial01No ratings yet

- Kitex Garments Limited - R - 11112020Document8 pagesKitex Garments Limited - R - 11112020Positive ThinkerNo ratings yet

- Tenda 4T23Document33 pagesTenda 4T23Flavya PereiraNo ratings yet

- Alliance ConcreteDocument11 pagesAlliance ConcreteAijaz AslamNo ratings yet

- Chapter 5 Financial Accounting LibbyDocument6 pagesChapter 5 Financial Accounting Libbymr. fiveNo ratings yet

- Cvs FinalpapermaheshDocument15 pagesCvs Finalpapermaheshnaikm3239No ratings yet

- Shareholder Letter Q3 2022 11.8.22 FINALDocument36 pagesShareholder Letter Q3 2022 11.8.22 FINALAlexNo ratings yet

- Irrecoverable Debts & Provision For Irrecoverables DebtsDocument5 pagesIrrecoverable Debts & Provision For Irrecoverables DebtsYomi AmvNo ratings yet

- Silver Crest Clothing Private LimitedDocument7 pagesSilver Crest Clothing Private Limitedsyedyaseenpasha9292No ratings yet

- Kota FibresDocument10 pagesKota FibresShishirNo ratings yet

- Zinka Logistics Solutions - R-25092020Document8 pagesZinka Logistics Solutions - R-25092020Atiqur Rahman BarbhuiyaNo ratings yet

- ACI Worldwide, Inc - ACIW - Q3 20Document10 pagesACI Worldwide, Inc - ACIW - Q3 20Saurabh SharmaNo ratings yet

- Tài Chính Công TyDocument14 pagesTài Chính Công Typttd154No ratings yet

- Barbeque Nation Hospitality LimitedDocument7 pagesBarbeque Nation Hospitality Limitednayabrasul208No ratings yet

- Champion Commercial Company LimitedDocument7 pagesChampion Commercial Company LimitedCedric KerkettaNo ratings yet

- Mohan Meakin LimitedDocument8 pagesMohan Meakin LimitedBithal PrasadNo ratings yet

- Case Study 1 Muhammad JanjuaDocument6 pagesCase Study 1 Muhammad JanjuaAmeer Hamza JanjuaNo ratings yet

- Sunsuria BHD (Written Report)Document6 pagesSunsuria BHD (Written Report)Monoliza PhilipsNo ratings yet

- SH-2023-Q4-1-ICRA-Housing Finance StatisticsDocument9 pagesSH-2023-Q4-1-ICRA-Housing Finance Statisticsshivay bhatejaNo ratings yet

- Khadim India Limited - ICRA Feb 2020 PDFDocument7 pagesKhadim India Limited - ICRA Feb 2020 PDFPuneet367No ratings yet

- Zaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Document23 pagesZaini Zain (BAF2009012) Adv. Fin. Acc Group Assignment (UPDATED)Zaini ZainNo ratings yet

- Cash Flow StatementDocument5 pagesCash Flow Statementphamkhanh22072003No ratings yet

- 4Q20 Shareholder LetterDocument28 pages4Q20 Shareholder LettermfajsemNo ratings yet

- Zodiac Clothing Company Limited: Rating Revised To (ICRA) A2 From (ICRA) A2+ Summary of Rating ActionDocument8 pagesZodiac Clothing Company Limited: Rating Revised To (ICRA) A2 From (ICRA) A2+ Summary of Rating ActionmanenderNo ratings yet

- Ap A2.1Document15 pagesAp A2.1Minh PhíNo ratings yet

- Bank Decision MakingDocument3 pagesBank Decision Makingjob_deloitte7440No ratings yet

- Sakthi Finance Limited R 20022020Document9 pagesSakthi Finance Limited R 20022020Elan ChelianNo ratings yet

- BFM Group 1 AssignmentDocument30 pagesBFM Group 1 AssignmentnurinNo ratings yet

- P7int 2013 Jun A PDFDocument17 pagesP7int 2013 Jun A PDFhiruspoonNo ratings yet

- Godrej Properties LimitedDocument11 pagesGodrej Properties Limitedkitono5817No ratings yet

- FNNB213 Group AssignmentDocument12 pagesFNNB213 Group AssignmentSyazwan Lagenda Bola SepakNo ratings yet

- 2022-01-13 BAC 4Q Earnings CallDocument22 pages2022-01-13 BAC 4Q Earnings CallPeople PeopleNo ratings yet

- Science in Sport PLC Results 2022 RNS 29.06.23Document21 pagesScience in Sport PLC Results 2022 RNS 29.06.23a.andrade.egiNo ratings yet

- Big Bags International PVT LTDDocument7 pagesBig Bags International PVT LTDnayabrasul208No ratings yet

- Question 5 of 10 - Chapter 4 HomeworkDocument4 pagesQuestion 5 of 10 - Chapter 4 HomeworkDulakshi RanadeeraNo ratings yet

- TCP Financial Analysis Q1Document7 pagesTCP Financial Analysis Q1Dulakshi RanadeeraNo ratings yet

- PVH Financial Analysis - Q1Document7 pagesPVH Financial Analysis - Q1Dulakshi RanadeeraNo ratings yet

- Market Share Has Made The Biggest Leap: Winners and LosersDocument3 pagesMarket Share Has Made The Biggest Leap: Winners and LosersDulakshi RanadeeraNo ratings yet

- Department of Accountancy: Inventory EstimationDocument2 pagesDepartment of Accountancy: Inventory EstimationAiza S. Maca-umbosNo ratings yet

- Plant Simulation Fact Sheet Book HQ-ilovepdf-compressed PDFDocument87 pagesPlant Simulation Fact Sheet Book HQ-ilovepdf-compressed PDFМануэль МендосаNo ratings yet

- Job Costing: I. Learning ObjectivesDocument8 pagesJob Costing: I. Learning ObjectivesKerby Gail RulonaNo ratings yet

- Chapter 2 - Cost TermsDocument35 pagesChapter 2 - Cost TermsCarina Carollo MalinaoNo ratings yet

- The Balanced ScorecardDocument6 pagesThe Balanced ScorecardRamana VaitlaNo ratings yet

- Food and BeverageDocument35 pagesFood and BeverageLyn Escano50% (2)

- 5 Year Ratio Analysis For RENATA LIMITED PDFDocument47 pages5 Year Ratio Analysis For RENATA LIMITED PDFDhruv singhNo ratings yet

- Seven Eleven CaseDocument5 pagesSeven Eleven CaseKarthikSureshNo ratings yet

- Share Capital Other Equity: B. Non-Core Non-Current AssetsDocument17 pagesShare Capital Other Equity: B. Non-Core Non-Current AssetsAksa DindeNo ratings yet

- Stardew Valley CommandsDocument3 pagesStardew Valley Commandskun hajimeNo ratings yet

- Unit 1 - InventoriesDocument76 pagesUnit 1 - InventoriesZamarhadebe SilosamahlubiNo ratings yet

- IBM Maximo Asset Management V6.2 ImplementationDocument41 pagesIBM Maximo Asset Management V6.2 ImplementationtareqcccccNo ratings yet

- Full 2012 CatalogFFRDocument620 pagesFull 2012 CatalogFFRsixela19No ratings yet

- SCM - Idc, G25Document9 pagesSCM - Idc, G25kuldeep singhNo ratings yet

- Wilkins A Zurn Company Demand ForecastinDocument16 pagesWilkins A Zurn Company Demand ForecastinYogendra RathoreNo ratings yet

- Cost ClassificationDocument24 pagesCost ClassificationElla Mae IragaNo ratings yet

- Manual para Uso Del Sistema OperaDocument144 pagesManual para Uso Del Sistema Operadanarg2286No ratings yet

- Strategic Benefits of A Global Trade Management Software SystemDocument4 pagesStrategic Benefits of A Global Trade Management Software SystemSileaLaurentiuNo ratings yet

- SCM 2021 Supply Chain Distribution Network Design - Part 1Document33 pagesSCM 2021 Supply Chain Distribution Network Design - Part 1Vikash Kumar Ojha100% (1)

- ITT AutoDocument4 pagesITT AutoKarthik ArumughamNo ratings yet

- Materials ManagementDocument438 pagesMaterials ManagementnpunnyNo ratings yet

- Shukrullah Assignment No 2Document4 pagesShukrullah Assignment No 2Shukrullah JanNo ratings yet

- Acca f2 Notes j15Document188 pagesAcca f2 Notes j15opentuitionID100% (1)

- Quản Trị Mua HàngDocument28 pagesQuản Trị Mua Hànghoangtruc07902No ratings yet

- CMR Institute of Technology: A Project ReportDocument73 pagesCMR Institute of Technology: A Project ReportKishor KumarNo ratings yet

- Prestige Bella VistaDocument27 pagesPrestige Bella VistaArun RajagopalNo ratings yet

- Answers Chapter 5 Quiz.s13Document2 pagesAnswers Chapter 5 Quiz.s13qwerty17327No ratings yet