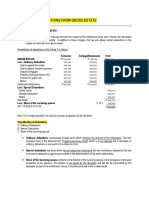

Resident Citizen, Non-Resident Citizen, and Resident Alien Decedents

Resident Citizen, Non-Resident Citizen, and Resident Alien Decedents

You might also like

- Wells Fargo StatementDocument8 pagesWells Fargo StatementJohn Bean100% (3)

- Farfetch 3Document1 pageFarfetch 3Axel Chabloz100% (1)

- August 05Document4 pagesAugust 05Matthew LundstromNo ratings yet

- Chapter Exercises DeductionsDocument11 pagesChapter Exercises DeductionsShaine KeefeNo ratings yet

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- Tax CalculationDocument6 pagesTax CalculationClarencia VeronicaNo ratings yet

- Deductions From Gross EstateDocument34 pagesDeductions From Gross Estatesmosaldana.cvtNo ratings yet

- Chapter 9 Estate Tax DeductionsDocument7 pagesChapter 9 Estate Tax DeductionsEthel Joy Tolentino GamboaNo ratings yet

- Lesson 3Document4 pagesLesson 3Iris Lavigne RojoNo ratings yet

- ACAE 18 - Deduction From Gross EstateDocument4 pagesACAE 18 - Deduction From Gross Estatechen dalitNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPT.Document24 pagesTAX 2 Deductions From The Gross Estate 1PPT.Franz Ana Marie CuaNo ratings yet

- Deductions: Philippines Gross Estate World Gross Estate Deductible LITDocument3 pagesDeductions: Philippines Gross Estate World Gross Estate Deductible LITMaria LopezNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- BusTax - Chapter 3 MODULEDocument8 pagesBusTax - Chapter 3 MODULETimon CarandangNo ratings yet

- Tax 2 4Document9 pagesTax 2 4amlecdeyojNo ratings yet

- X DeductionsDocument11 pagesX Deductionsmariyha PalangganaNo ratings yet

- Estate Tax: Taxation 1Document22 pagesEstate Tax: Taxation 1Jess Guiang CasamorinNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPTDocument24 pagesTAX 2 Deductions From The Gross Estate 1PPTMichael AquinoNo ratings yet

- Estate Tax 3Document50 pagesEstate Tax 3Lea JoaquinNo ratings yet

- Chapter 2 - Deductions From The Gross EstateDocument9 pagesChapter 2 - Deductions From The Gross EstateElla Marie WicoNo ratings yet

- Estate Tax (Exercises)Document3 pagesEstate Tax (Exercises)dimpy dNo ratings yet

- Ordinary DeductionDocument6 pagesOrdinary Deductionar calasangNo ratings yet

- Allowable Deductions in The Gross Estate Under TRADocument7 pagesAllowable Deductions in The Gross Estate Under TRASantiago Joanna MarieNo ratings yet

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDocument18 pagesReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasNo ratings yet

- TRAIN LAW - Estate TAX - SUMMARY OF CHANGESDocument10 pagesTRAIN LAW - Estate TAX - SUMMARY OF CHANGESBon BonsNo ratings yet

- Deductions From Gross EstateDocument46 pagesDeductions From Gross EstateARC SVIORNo ratings yet

- Deductions From Gross EstateDocument112 pagesDeductions From Gross EstateLuna CakesNo ratings yet

- Jessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstateDocument8 pagesJessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstatejessaNo ratings yet

- Activity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsDocument5 pagesActivity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsSara Andrea SantiagoNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- Estate Tax PDFDocument35 pagesEstate Tax PDFRhea Mae Sa-onoyNo ratings yet

- Tax 2 Module1 Estate TaxationDocument28 pagesTax 2 Module1 Estate TaxationXyza JabiliNo ratings yet

- 03 Deductions From Gross EstateDocument4 pages03 Deductions From Gross Estatelemvin121003No ratings yet

- Shall File A Return Under OathDocument17 pagesShall File A Return Under OathMixx MineNo ratings yet

- Taxation Report - Valuation of Properties - Vanishing DeductionDocument49 pagesTaxation Report - Valuation of Properties - Vanishing DeductionAnonymous S6CQnxuJcINo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- TRAIN LAW - Estate TAxSUMMARY OF CHANGESDocument11 pagesTRAIN LAW - Estate TAxSUMMARY OF CHANGESBon BonsNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- Estate TaxDocument7 pagesEstate TaxMarie MAy MagtibayNo ratings yet

- Taxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionDocument7 pagesTaxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionKira Lim100% (1)

- ACT26 - Ch04 - Deduction From The Gross EstateDocument7 pagesACT26 - Ch04 - Deduction From The Gross EstateMark BajacanNo ratings yet

- Taxation On Estates and TrustsDocument31 pagesTaxation On Estates and TrustsAndrea Renice S. FerriolNo ratings yet

- Deductions From Gross EstateDocument3 pagesDeductions From Gross EstateMark Lawrence YusiNo ratings yet

- Taxation 1 Mod 3Document45 pagesTaxation 1 Mod 3Harui Hani-31No ratings yet

- Transfer Estate Tax Chapter 1Document33 pagesTransfer Estate Tax Chapter 1cmaepitoc21No ratings yet

- Transfer TaxesDocument101 pagesTransfer TaxesAngelo IvanNo ratings yet

- HQ11 - Estate TaxationDocument18 pagesHQ11 - Estate TaxationJane Oblena100% (1)

- Estate Tax Payable - 1625701751Document17 pagesEstate Tax Payable - 1625701751T-121-Gutierrez, GwynethNo ratings yet

- Prelim Tax 2Document13 pagesPrelim Tax 2Joseph Mangahas50% (2)

- Chapter 7 Deduction For Gross EstatesDocument19 pagesChapter 7 Deduction For Gross Estatesmendonesmariza2No ratings yet

- Estate TaxDocument5 pagesEstate Taxericamaecarpila0520No ratings yet

- ARTICLE - Death, Real Estate, and Estate TaxesDocument10 pagesARTICLE - Death, Real Estate, and Estate TaxestemporiariNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Put A Mark On The Letter of Your ChoiceDocument5 pagesPut A Mark On The Letter of Your Choicejhell dela cruzNo ratings yet

- Deduction From Gross EstateDocument41 pagesDeduction From Gross EstateDianne Pearl DelfinNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- Module 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Document35 pagesModule 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Venice Marie ArroyoNo ratings yet

- Module 2 - Estate TaxDocument14 pagesModule 2 - Estate TaxHaidee Flavier SabidoNo ratings yet

- 3 - Estate TaxDocument10 pages3 - Estate TaxVernnNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Rs Agarwal BillDocument1 pageRs Agarwal BillrithinNo ratings yet

- BUS 345 CHP 1 Example Exam Questions #1 - #6 - STUDENTSDocument3 pagesBUS 345 CHP 1 Example Exam Questions #1 - #6 - STUDENTSRishab JoshiNo ratings yet

- SAP HR Common Error MessagesDocument20 pagesSAP HR Common Error Messagesbelrosa2150% (2)

- Investment Declaration Form FY 2019-20 v2Document5 pagesInvestment Declaration Form FY 2019-20 v2Rehan ElectronicsNo ratings yet

- RandomDocument2 pagesRandomLakhan PatidarNo ratings yet

- HU 2024 V 8 International Fee - Exchange Rate 1USD To RM4.00 - 23 March 2024Document4 pagesHU 2024 V 8 International Fee - Exchange Rate 1USD To RM4.00 - 23 March 2024uzairwalidarNo ratings yet

- 1PZ2U8Document1 page1PZ2U8algumhyNo ratings yet

- Medicard Philippines v. CIR (G.R. No. 222743, April 5, 2017)Document1 pageMedicard Philippines v. CIR (G.R. No. 222743, April 5, 2017)jobelle barcellanoNo ratings yet

- RCBC ATM (Nationwide Branches) : DateDocument6 pagesRCBC ATM (Nationwide Branches) : DateジョージNo ratings yet

- Dr. Jeannie P. LimDocument38 pagesDr. Jeannie P. LimSHeena MaRie ErAsmoNo ratings yet

- Sending Money With World RemitDocument9 pagesSending Money With World RemitBabatunde toheebNo ratings yet

- ST Harry PDFDocument10 pagesST Harry PDFharjinder singhNo ratings yet

- Maryland Mortgage Program - Recapture TaxDocument12 pagesMaryland Mortgage Program - Recapture TaxNishika JGNo ratings yet

- Master Circular 53Document9 pagesMaster Circular 53KunalSinghNo ratings yet

- Taxation Law II SyllabusDocument9 pagesTaxation Law II SyllabusRio Porto100% (1)

- E PassbookDocument18 pagesE PassbookNilanjan KarmakarNo ratings yet

- Superdoll Trailer Manufacture Co. (T) LTD.: Proforma InvoiceDocument1 pageSuperdoll Trailer Manufacture Co. (T) LTD.: Proforma InvoiceRommel TagalagNo ratings yet

- GST Reg in Case of DeathDocument1 pageGST Reg in Case of DeathUmairaNo ratings yet

- Income Under The Head SalariesDocument21 pagesIncome Under The Head SalariesAnupam BaliNo ratings yet

- Phil Gold Processing & Refining Corp: RF Monthly-Lgm 3Document1 pagePhil Gold Processing & Refining Corp: RF Monthly-Lgm 3bonemarkcosNo ratings yet

- Form16 2018 2019Document10 pagesForm16 2018 2019LogeshwaranNo ratings yet

- Research MethodologyDocument34 pagesResearch MethodologySangeetaLakhesar80% (5)

- RMC 08-90 VAT On DepositsDocument8 pagesRMC 08-90 VAT On DepositsRieland CuevasNo ratings yet

- David Lightman-WPS OfficeDocument33 pagesDavid Lightman-WPS OfficeMikiNo ratings yet

- Display Organization: 10172, Role FI CustomerDocument1 pageDisplay Organization: 10172, Role FI CustomerFarahNo ratings yet

- JIO Bablu Bhai RechargeDocument2 pagesJIO Bablu Bhai RechargeYogesh SaindaneNo ratings yet

Download as pdf or txt

You might also like

- Wells Fargo StatementDocument8 pagesWells Fargo StatementJohn Bean100% (3)

- Farfetch 3Document1 pageFarfetch 3Axel Chabloz100% (1)

- August 05Document4 pagesAugust 05Matthew LundstromNo ratings yet

- Chapter Exercises DeductionsDocument11 pagesChapter Exercises DeductionsShaine KeefeNo ratings yet

- Module 1 - Deductions From Gross EstateDocument68 pagesModule 1 - Deductions From Gross EstateKat Miranda100% (1)

- Tax CalculationDocument6 pagesTax CalculationClarencia VeronicaNo ratings yet

- Deductions From Gross EstateDocument34 pagesDeductions From Gross Estatesmosaldana.cvtNo ratings yet

- Chapter 9 Estate Tax DeductionsDocument7 pagesChapter 9 Estate Tax DeductionsEthel Joy Tolentino GamboaNo ratings yet

- Lesson 3Document4 pagesLesson 3Iris Lavigne RojoNo ratings yet

- ACAE 18 - Deduction From Gross EstateDocument4 pagesACAE 18 - Deduction From Gross Estatechen dalitNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPT.Document24 pagesTAX 2 Deductions From The Gross Estate 1PPT.Franz Ana Marie CuaNo ratings yet

- Deductions: Philippines Gross Estate World Gross Estate Deductible LITDocument3 pagesDeductions: Philippines Gross Estate World Gross Estate Deductible LITMaria LopezNo ratings yet

- Chapter 6 Deductions From The Gross Estate PDFDocument7 pagesChapter 6 Deductions From The Gross Estate PDFDudz MatienzoNo ratings yet

- M5 - Deductions From Gross Estate - Students'Document33 pagesM5 - Deductions From Gross Estate - Students'micaella pasionNo ratings yet

- BusTax - Chapter 3 MODULEDocument8 pagesBusTax - Chapter 3 MODULETimon CarandangNo ratings yet

- Tax 2 4Document9 pagesTax 2 4amlecdeyojNo ratings yet

- X DeductionsDocument11 pagesX Deductionsmariyha PalangganaNo ratings yet

- Estate Tax: Taxation 1Document22 pagesEstate Tax: Taxation 1Jess Guiang CasamorinNo ratings yet

- TAX 2 Deductions From The Gross Estate 1PPTDocument24 pagesTAX 2 Deductions From The Gross Estate 1PPTMichael AquinoNo ratings yet

- Estate Tax 3Document50 pagesEstate Tax 3Lea JoaquinNo ratings yet

- Chapter 2 - Deductions From The Gross EstateDocument9 pagesChapter 2 - Deductions From The Gross EstateElla Marie WicoNo ratings yet

- Estate Tax (Exercises)Document3 pagesEstate Tax (Exercises)dimpy dNo ratings yet

- Ordinary DeductionDocument6 pagesOrdinary Deductionar calasangNo ratings yet

- Allowable Deductions in The Gross Estate Under TRADocument7 pagesAllowable Deductions in The Gross Estate Under TRASantiago Joanna MarieNo ratings yet

- ReSA B42 TAX First PB Exam - Questions, Answers - SolutionsDocument18 pagesReSA B42 TAX First PB Exam - Questions, Answers - SolutionsPearl Mae De VeasNo ratings yet

- TRAIN LAW - Estate TAX - SUMMARY OF CHANGESDocument10 pagesTRAIN LAW - Estate TAX - SUMMARY OF CHANGESBon BonsNo ratings yet

- Deductions From Gross EstateDocument46 pagesDeductions From Gross EstateARC SVIORNo ratings yet

- Deductions From Gross EstateDocument112 pagesDeductions From Gross EstateLuna CakesNo ratings yet

- Jessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstateDocument8 pagesJessa B. Regalario Ms. Tabernilla V-Bsa F. Schedule and Computation of The Tax Estate Tax Imposed On Net EstatejessaNo ratings yet

- Activity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsDocument5 pagesActivity No. 1: Estate Tax (Pages 440-461) : Multiple Choice QuestionsSara Andrea SantiagoNo ratings yet

- Tax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsDocument31 pagesTax 02-Lesson 05 - Estate Tax Credit, Distributable Estate, and Estate Tax ReturnsMama MiyaNo ratings yet

- Vanishing DeductionsDocument3 pagesVanishing DeductionsCyrell AsidNo ratings yet

- Estate Tax PDFDocument35 pagesEstate Tax PDFRhea Mae Sa-onoyNo ratings yet

- Tax 2 Module1 Estate TaxationDocument28 pagesTax 2 Module1 Estate TaxationXyza JabiliNo ratings yet

- 03 Deductions From Gross EstateDocument4 pages03 Deductions From Gross Estatelemvin121003No ratings yet

- Shall File A Return Under OathDocument17 pagesShall File A Return Under OathMixx MineNo ratings yet

- Taxation Report - Valuation of Properties - Vanishing DeductionDocument49 pagesTaxation Report - Valuation of Properties - Vanishing DeductionAnonymous S6CQnxuJcINo ratings yet

- Deductions On Gross Estate Part 1Document19 pagesDeductions On Gross Estate Part 1Angel Clarisse JariolNo ratings yet

- TRAIN LAW - Estate TAxSUMMARY OF CHANGESDocument11 pagesTRAIN LAW - Estate TAxSUMMARY OF CHANGESBon BonsNo ratings yet

- Deduction From The Gross EstateDocument6 pagesDeduction From The Gross EstateEmma Mariz GarciaNo ratings yet

- Estate TaxDocument7 pagesEstate TaxMarie MAy MagtibayNo ratings yet

- Taxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionDocument7 pagesTaxation Atty. Macmod, C.P.A. Estate Tax 2020 EditionKira Lim100% (1)

- ACT26 - Ch04 - Deduction From The Gross EstateDocument7 pagesACT26 - Ch04 - Deduction From The Gross EstateMark BajacanNo ratings yet

- Taxation On Estates and TrustsDocument31 pagesTaxation On Estates and TrustsAndrea Renice S. FerriolNo ratings yet

- Deductions From Gross EstateDocument3 pagesDeductions From Gross EstateMark Lawrence YusiNo ratings yet

- Taxation 1 Mod 3Document45 pagesTaxation 1 Mod 3Harui Hani-31No ratings yet

- Transfer Estate Tax Chapter 1Document33 pagesTransfer Estate Tax Chapter 1cmaepitoc21No ratings yet

- Transfer TaxesDocument101 pagesTransfer TaxesAngelo IvanNo ratings yet

- HQ11 - Estate TaxationDocument18 pagesHQ11 - Estate TaxationJane Oblena100% (1)

- Estate Tax Payable - 1625701751Document17 pagesEstate Tax Payable - 1625701751T-121-Gutierrez, GwynethNo ratings yet

- Prelim Tax 2Document13 pagesPrelim Tax 2Joseph Mangahas50% (2)

- Chapter 7 Deduction For Gross EstatesDocument19 pagesChapter 7 Deduction For Gross Estatesmendonesmariza2No ratings yet

- Estate TaxDocument5 pagesEstate Taxericamaecarpila0520No ratings yet

- ARTICLE - Death, Real Estate, and Estate TaxesDocument10 pagesARTICLE - Death, Real Estate, and Estate TaxestemporiariNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Put A Mark On The Letter of Your ChoiceDocument5 pagesPut A Mark On The Letter of Your Choicejhell dela cruzNo ratings yet

- Deduction From Gross EstateDocument41 pagesDeduction From Gross EstateDianne Pearl DelfinNo ratings yet

- Deductions From Gross EstateDocument20 pagesDeductions From Gross EstateJamaica David100% (2)

- Module 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Document35 pagesModule 2 DEDUCTION FROM GROSS ESTATE AND ESTATE TAX - Part 1Venice Marie ArroyoNo ratings yet

- Module 2 - Estate TaxDocument14 pagesModule 2 - Estate TaxHaidee Flavier SabidoNo ratings yet

- 3 - Estate TaxDocument10 pages3 - Estate TaxVernnNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- Rs Agarwal BillDocument1 pageRs Agarwal BillrithinNo ratings yet

- BUS 345 CHP 1 Example Exam Questions #1 - #6 - STUDENTSDocument3 pagesBUS 345 CHP 1 Example Exam Questions #1 - #6 - STUDENTSRishab JoshiNo ratings yet

- SAP HR Common Error MessagesDocument20 pagesSAP HR Common Error Messagesbelrosa2150% (2)

- Investment Declaration Form FY 2019-20 v2Document5 pagesInvestment Declaration Form FY 2019-20 v2Rehan ElectronicsNo ratings yet

- RandomDocument2 pagesRandomLakhan PatidarNo ratings yet

- HU 2024 V 8 International Fee - Exchange Rate 1USD To RM4.00 - 23 March 2024Document4 pagesHU 2024 V 8 International Fee - Exchange Rate 1USD To RM4.00 - 23 March 2024uzairwalidarNo ratings yet

- 1PZ2U8Document1 page1PZ2U8algumhyNo ratings yet

- Medicard Philippines v. CIR (G.R. No. 222743, April 5, 2017)Document1 pageMedicard Philippines v. CIR (G.R. No. 222743, April 5, 2017)jobelle barcellanoNo ratings yet

- RCBC ATM (Nationwide Branches) : DateDocument6 pagesRCBC ATM (Nationwide Branches) : DateジョージNo ratings yet

- Dr. Jeannie P. LimDocument38 pagesDr. Jeannie P. LimSHeena MaRie ErAsmoNo ratings yet

- Sending Money With World RemitDocument9 pagesSending Money With World RemitBabatunde toheebNo ratings yet

- ST Harry PDFDocument10 pagesST Harry PDFharjinder singhNo ratings yet

- Maryland Mortgage Program - Recapture TaxDocument12 pagesMaryland Mortgage Program - Recapture TaxNishika JGNo ratings yet

- Master Circular 53Document9 pagesMaster Circular 53KunalSinghNo ratings yet

- Taxation Law II SyllabusDocument9 pagesTaxation Law II SyllabusRio Porto100% (1)

- E PassbookDocument18 pagesE PassbookNilanjan KarmakarNo ratings yet

- Superdoll Trailer Manufacture Co. (T) LTD.: Proforma InvoiceDocument1 pageSuperdoll Trailer Manufacture Co. (T) LTD.: Proforma InvoiceRommel TagalagNo ratings yet

- GST Reg in Case of DeathDocument1 pageGST Reg in Case of DeathUmairaNo ratings yet

- Income Under The Head SalariesDocument21 pagesIncome Under The Head SalariesAnupam BaliNo ratings yet

- Phil Gold Processing & Refining Corp: RF Monthly-Lgm 3Document1 pagePhil Gold Processing & Refining Corp: RF Monthly-Lgm 3bonemarkcosNo ratings yet

- Form16 2018 2019Document10 pagesForm16 2018 2019LogeshwaranNo ratings yet

- Research MethodologyDocument34 pagesResearch MethodologySangeetaLakhesar80% (5)

- RMC 08-90 VAT On DepositsDocument8 pagesRMC 08-90 VAT On DepositsRieland CuevasNo ratings yet

- David Lightman-WPS OfficeDocument33 pagesDavid Lightman-WPS OfficeMikiNo ratings yet

- Display Organization: 10172, Role FI CustomerDocument1 pageDisplay Organization: 10172, Role FI CustomerFarahNo ratings yet

- JIO Bablu Bhai RechargeDocument2 pagesJIO Bablu Bhai RechargeYogesh SaindaneNo ratings yet