Download as docx, pdf, or txt

You might also like

- CPCCWHS2001 Assessment WorkbookDocument70 pagesCPCCWHS2001 Assessment Workbookankit33% (3)

- ReinventingtheOrganization A5Document6 pagesReinventingtheOrganization A5Randi MakmurNo ratings yet

- Buysiness of AdditivcesDocument17 pagesBuysiness of AdditivcesmohammedNo ratings yet

- Project Management Plan Reverse Logistics Midterm PDFDocument10 pagesProject Management Plan Reverse Logistics Midterm PDFramrammithraNo ratings yet

- Chapter 18Document27 pagesChapter 18Dr Bhadrappa HaralayyaNo ratings yet

- Non-Performing Assets, Capital Adequacy and Bank Profitability A Study of Selected Indian Commercial BanksDocument6 pagesNon-Performing Assets, Capital Adequacy and Bank Profitability A Study of Selected Indian Commercial BanksarcherselevatorsNo ratings yet

- Tojqi Paper Technical Efficiency Affecting Factors in Indian Banking Sector An Empirical AnalysisDocument18 pagesTojqi Paper Technical Efficiency Affecting Factors in Indian Banking Sector An Empirical AnalysisDr Bhadrappa HaralayyaNo ratings yet

- Table 1: Indian Bank Association Analysis of Banks, 2003 Year Indian Banks Foreign Banks Total BanksDocument17 pagesTable 1: Indian Bank Association Analysis of Banks, 2003 Year Indian Banks Foreign Banks Total BanksWasil AliNo ratings yet

- Source: Off-Site Returns (Domestic) of Banks, Department of Banking Supervision, RBIDocument4 pagesSource: Off-Site Returns (Domestic) of Banks, Department of Banking Supervision, RBIManikanda Bharathi SNo ratings yet

- Banking and InsuranceDocument12 pagesBanking and InsuranceyaminshaikhNo ratings yet

- Icici Feb 20Document266 pagesIcici Feb 20Ram ChiyeduNo ratings yet

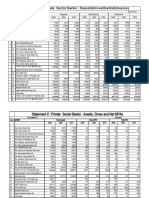

- Statement I: Private Sector Banks: Deposits/Investments/AdvancesDocument8 pagesStatement I: Private Sector Banks: Deposits/Investments/Advancesprakasht_1No ratings yet

- Statement I: Private Sector Banks: Deposits/Investments/AdvancesDocument8 pagesStatement I: Private Sector Banks: Deposits/Investments/AdvancesanandbhawanaNo ratings yet

- Statement I: Private Sector Banks: Deposits/Investments/AdvancesDocument8 pagesStatement I: Private Sector Banks: Deposits/Investments/AdvancesGyanendra AgrawalNo ratings yet

- FIM Final PresentationDocument50 pagesFIM Final Presentationavii boutiqueNo ratings yet

- 4 1 16 PDFDocument18 pages4 1 16 PDFAsawarNo ratings yet

- Miggros - CaseDocument4 pagesMiggros - CasefineksusgroupNo ratings yet

- Automobile Industry Ratio AnalysisDocument71 pagesAutomobile Industry Ratio Analysisakshay50% (2)

- Quantum Leap Forward: Particulars 2007-08 2008-09 2009-2010 A Key IndicatorsDocument7 pagesQuantum Leap Forward: Particulars 2007-08 2008-09 2009-2010 A Key IndicatorsHemant JangidNo ratings yet

- Report Case Study Fin534 Group AssignmentDocument15 pagesReport Case Study Fin534 Group Assignment‘Alya Qistina Mohd ZaimNo ratings yet

- EquityDocument277 pagesEquityhidulfiNo ratings yet

- Bank of AmericaDocument23 pagesBank of AmericaAzər ƏmiraslanNo ratings yet

- Data Analysis: Pradhan Mantri Jan-Dhan Yojana (Pmjdy)Document13 pagesData Analysis: Pradhan Mantri Jan-Dhan Yojana (Pmjdy)vivek adkineNo ratings yet

- Retail Banking in IndiaDocument21 pagesRetail Banking in IndiaAnilSGNo ratings yet

- IJCRT2204055Document5 pagesIJCRT2204055Jay statusNo ratings yet

- Introduction: Financial Inclusion and PMJDYDocument4 pagesIntroduction: Financial Inclusion and PMJDYNakshtra DasNo ratings yet

- Research Analysis: Prepared by Darshan PatiraDocument7 pagesResearch Analysis: Prepared by Darshan Patiradarshan jainNo ratings yet

- Balance Sheet AnalysisDocument8 pagesBalance Sheet Analysisramyashraddha18No ratings yet

- Chapeter 2: Introduction of Pubali Bank LTDDocument16 pagesChapeter 2: Introduction of Pubali Bank LTDMuhammad Hayath ChowdhuryNo ratings yet

- My Bank Has Better NPA Than Your BankDocument7 pagesMy Bank Has Better NPA Than Your Bankhk_scribdNo ratings yet

- Statement I: Public Sector Banks: Deposits/Investments/AdvancesDocument8 pagesStatement I: Public Sector Banks: Deposits/Investments/AdvancesNirmal SinghNo ratings yet

- CMEs Annual Tables 2074-75 FinalDocument73 pagesCMEs Annual Tables 2074-75 FinalDebendra Dev KhanalNo ratings yet

- General BankingDocument167 pagesGeneral BankingSuvasish DasguptaNo ratings yet

- Source: Annual Accounts of BanksDocument6 pagesSource: Annual Accounts of BanksARVIND YADAVNo ratings yet

- Preface: Submitted By:-Jimmy Sachde 08bba038 S.Y.B.B.ADocument27 pagesPreface: Submitted By:-Jimmy Sachde 08bba038 S.Y.B.B.AJimmy SachdeNo ratings yet

- Some Key Indicators of Indian Banking BusinessDocument20 pagesSome Key Indicators of Indian Banking BusinessPratik PatilNo ratings yet

- Economics - Demand ForecastingDocument23 pagesEconomics - Demand ForecastingKLN CHUNo ratings yet

- Banking Report 5Document23 pagesBanking Report 5EMMADI MANIDEEPNo ratings yet

- ICICI Prudential Asset Allocator Fund (FOF)Document4 pagesICICI Prudential Asset Allocator Fund (FOF)maheshgawand144No ratings yet

- The Performance of Cooperative Banking in India.: EconomicsDocument3 pagesThe Performance of Cooperative Banking in India.: EconomicsmovinNo ratings yet

- Capitec Group AR 2010Document152 pagesCapitec Group AR 2010John WilsonNo ratings yet

- Appendix: Table 8.1: Non Performing Assets of Different BanksDocument8 pagesAppendix: Table 8.1: Non Performing Assets of Different Banksshreeya salunkeNo ratings yet

- Performance Benchmarking Report 12 NewDocument46 pagesPerformance Benchmarking Report 12 NewVishal KoulNo ratings yet

- SPI September 2019Document818 pagesSPI September 2019DewiNo ratings yet

- Punjab National Bank Project ReportDocument40 pagesPunjab National Bank Project ReportVarun100% (40)

- Fundamental Analysis Case Study of ICICI BankDocument61 pagesFundamental Analysis Case Study of ICICI BankNirojini Bhat BhanNo ratings yet

- Asset Classsification 2005-10Document2 pagesAsset Classsification 2005-10Anoop MohantyNo ratings yet

- Private Sector Banks in India - A SWOT Analysis 2004Document23 pagesPrivate Sector Banks in India - A SWOT Analysis 2004Prof Dr Chowdari Prasad67% (3)

- Role of Public and Private Sector in Economic Development of IndiaDocument13 pagesRole of Public and Private Sector in Economic Development of IndiaAseem175% (8)

- Chapter 20 Mutual Fund IndustryDocument55 pagesChapter 20 Mutual Fund IndustryrohangonNo ratings yet

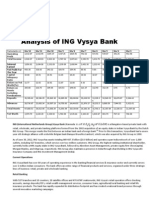

- Analysis of ING Vysya BankDocument2 pagesAnalysis of ING Vysya BankAbhishek JhaveriNo ratings yet

- Document of RecruitmentDocument6 pagesDocument of RecruitmentManjunath BolashettiNo ratings yet

- Chapter 4Document31 pagesChapter 4koushik kumarNo ratings yet

- Segment Reporting On BOBDocument3 pagesSegment Reporting On BOBrajputgiteshNo ratings yet

- Banking Sector Developments in India, 1980-2005: What The Annual Accounts Speak?Document29 pagesBanking Sector Developments in India, 1980-2005: What The Annual Accounts Speak?sg31No ratings yet

- Internship Arif FinalDocument58 pagesInternship Arif Finalটিটন চাকমাNo ratings yet

- BanksDocument29 pagesBanksbanduwgsNo ratings yet

- Metamorphosis of Modern Management - Financial ServicesDocument12 pagesMetamorphosis of Modern Management - Financial ServicesSiva BalajiNo ratings yet

- Sector InformationDocument8 pagesSector InformationarunimaNo ratings yet

- Small Money Big Impact: Fighting Poverty with MicrofinanceFrom EverandSmall Money Big Impact: Fighting Poverty with MicrofinanceNo ratings yet

- Physical Network: Number of Offices: Total Head Office Other Offices 27,957 6,837 21,120 I. 10,020 667 9,353 Banks Mar-14Document1 pagePhysical Network: Number of Offices: Total Head Office Other Offices 27,957 6,837 21,120 I. 10,020 667 9,353 Banks Mar-14Sarah WilliamsNo ratings yet

- Chapter - 5 Regional Rural BanksDocument11 pagesChapter - 5 Regional Rural Banksbaby0310No ratings yet

- Financial Analysis: A Study of J & K Bank Limited: AbhinavDocument6 pagesFinancial Analysis: A Study of J & K Bank Limited: AbhinavSanjay SaqlainNo ratings yet

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeFrom EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNo ratings yet

- How To Effectively Manage - PaperDocument16 pagesHow To Effectively Manage - PaperescibedNo ratings yet

- 203-04a - PROJECT COST CONTROL AND PLANNINGDocument12 pages203-04a - PROJECT COST CONTROL AND PLANNINGYusufNo ratings yet

- Unit 1 (1) - MergedDocument25 pagesUnit 1 (1) - MergedSumit BaghelNo ratings yet

- Corporate Presentation: January 2022Document67 pagesCorporate Presentation: January 2022vishwas pandithNo ratings yet

- Specifications: PartsDocument1 pageSpecifications: PartsSaul UribeNo ratings yet

- How To Use Import Export InformationDocument3 pagesHow To Use Import Export InformationTSEDEKENo ratings yet

- Contract Management (Chapter 19)Document13 pagesContract Management (Chapter 19)Discord YtNo ratings yet

- BRS eCMR - v1.0Document11 pagesBRS eCMR - v1.0Karim GharbiNo ratings yet

- Factor Momentum Everywhere JPM Quant 19Document26 pagesFactor Momentum Everywhere JPM Quant 19Henry HNo ratings yet

- CH 06Document22 pagesCH 06Xinjie MaNo ratings yet

- 4 POLE MOTOR (1500 RPM) - I/50Hz: Denominacion Referencia Diam (MM) in (A) Wins (KW) LPA (DB (A) ) Q Max (CMH) PVP ( )Document1 page4 POLE MOTOR (1500 RPM) - I/50Hz: Denominacion Referencia Diam (MM) in (A) Wins (KW) LPA (DB (A) ) Q Max (CMH) PVP ( )abdulNo ratings yet

- Project To Product TransformationDocument98 pagesProject To Product TransformationFrenzyPanda100% (1)

- DWP 2007Document82 pagesDWP 2007Gagan AgrawalNo ratings yet

- Risk Accreditation FrameworkDocument2 pagesRisk Accreditation FrameworkSwati ChopraNo ratings yet

- Unileveranalysis 150506052341 Conversion Gate01 DikonversiDocument179 pagesUnileveranalysis 150506052341 Conversion Gate01 DikonversievanshjtNo ratings yet

- 010-Reducing Agent SwitchingDocument91 pages010-Reducing Agent Switchingasri nurulNo ratings yet

- Guide 8 Steps Problem SolvingDocument13 pagesGuide 8 Steps Problem SolvingAbrahamNdewingoNo ratings yet

- SME and SE ParagraphDocument2 pagesSME and SE ParagraphAimee CuteNo ratings yet

- 005 Pam enDocument104 pages005 Pam enNasif FattahNo ratings yet

- Saputo IncDocument2 pagesSaputo IncDarryl GrossauerNo ratings yet

- Amendments To BD Cathlab Issued 2-05-24Document34 pagesAmendments To BD Cathlab Issued 2-05-24sharc nightNo ratings yet

- APT+exercises+post 1Document6 pagesAPT+exercises+post 1Karan GambhirNo ratings yet

- Principles of Accounting, Volume 2: Managerial AccountingDocument59 pagesPrinciples of Accounting, Volume 2: Managerial AccountingVo VeraNo ratings yet

- Philip T. Kotler Gary Armstrong Principles of Marketing Pearson 2017Document3 pagesPhilip T. Kotler Gary Armstrong Principles of Marketing Pearson 2017bachln22416cNo ratings yet

- MRM FormatDocument3 pagesMRM FormatPk NimiwalNo ratings yet

- Job Description - IP Backhaul & MPLS EngineerDocument2 pagesJob Description - IP Backhaul & MPLS EngineerTameta DadaNo ratings yet