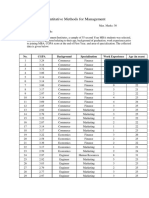

Step #1: Find The Mean Returbn of Each Stocks

Step #1: Find The Mean Returbn of Each Stocks

You might also like

- Fundamentals of Investments Valuation and Management 7th Edition by Jordan ISBN Solution ManualDocument9 pagesFundamentals of Investments Valuation and Management 7th Edition by Jordan ISBN Solution Manualbarbara0% (1)

- 2019 2 QMM AssignmentDocument3 pages2019 2 QMM AssignmentPranav0% (1)

- Key Chapter 7 Ms - TrangDocument6 pagesKey Chapter 7 Ms - TrangHoàng Việt VũNo ratings yet

- Hand Bone Age Atlas - Greulich-Pyle OXFORD RemakeDocument72 pagesHand Bone Age Atlas - Greulich-Pyle OXFORD RemakeSony Sutrisno100% (1)

- ASTM E1950-17 Standard Practice For Reporting Results From Methods of Chemical AnalysisDocument6 pagesASTM E1950-17 Standard Practice For Reporting Results From Methods of Chemical AnalysisDoina MarquezNo ratings yet

- Chapter 11Document25 pagesChapter 11M Eduardo BasantesNo ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Corporate FinanceDocument18 pagesChapter 10: Risk and Return: Lessons From Market History: Corporate FinancePháp NguyễnNo ratings yet

- Chapter 11Document28 pagesChapter 11Khoa LêNo ratings yet

- Corporate Finance Ross 10th Edition Solutions ManualDocument14 pagesCorporate Finance Ross 10th Edition Solutions ManualCatherineJohnsonabpg100% (46)

- Ch10 Solutions 6thedDocument14 pagesCh10 Solutions 6thedMrinmay kunduNo ratings yet

- Chapter 11Document27 pagesChapter 11Sufyan KhanNo ratings yet

- Corporate Finance CHDocument26 pagesCorporate Finance CHSK (아얀)No ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Corporate FinanceDocument15 pagesChapter 10: Risk and Return: Lessons From Market History: Corporate Financeirwan hermantriaNo ratings yet

- Faculty of Higher Education: Assignment Cover SheetDocument11 pagesFaculty of Higher Education: Assignment Cover SheetSyed Ali Hussain BokhariNo ratings yet

- Solutions Manual: Ross, Westerfield, and Jaffe Asia Global EditionDocument14 pagesSolutions Manual: Ross, Westerfield, and Jaffe Asia Global EditionRia FitriyanaNo ratings yet

- Chapter 10Document14 pagesChapter 10Beatrice ReynanciaNo ratings yet

- Chapter 11 &12 Tute SolsDocument9 pagesChapter 11 &12 Tute SolsRakeshNo ratings yet

- Lecture 8: Rate of Return Analysis: Instructional Material ForDocument20 pagesLecture 8: Rate of Return Analysis: Instructional Material ForAziezah PalintaNo ratings yet

- Chapter 10 SolutionDocument13 pagesChapter 10 SolutionPhước NgọcNo ratings yet

- Chapter 7 - ExercisesDocument6 pagesChapter 7 - Exercisesmin - radiseNo ratings yet

- Risk, Return, and The Security Market Line: B. Unsystematic C. D. Unsystematic E. FDocument15 pagesRisk, Return, and The Security Market Line: B. Unsystematic C. D. Unsystematic E. FTú Anh Nguyễn ThịNo ratings yet

- Assignment Capital Market and Portfolio ManagementDocument12 pagesAssignment Capital Market and Portfolio ManagementIshan MohindraNo ratings yet

- Risk & ReturnDocument57 pagesRisk & ReturnAyaz MeerNo ratings yet

- SOLUTION1. Exercise 1 PDFDocument10 pagesSOLUTION1. Exercise 1 PDFVanessa ThuyNo ratings yet

- Problem Set 4 SolutionDocument8 pagesProblem Set 4 SolutionMỹ HạnhNo ratings yet

- Concept of Risk and ReturnDocument40 pagesConcept of Risk and ReturnkomalissinghNo ratings yet

- Chapter 12 (Updated Oct 5)Document29 pagesChapter 12 (Updated Oct 5)Zoe LamNo ratings yet

- FIN437 Answers To The Recommended Questions Portfolio ManagementDocument6 pagesFIN437 Answers To The Recommended Questions Portfolio ManagementSenalNaldoNo ratings yet

- 1.3.2.1 Elaborate Problem Solving AssignmentDocument17 pages1.3.2.1 Elaborate Problem Solving AssignmentYess poooNo ratings yet

- HW12Document7 pagesHW12nma.work173No ratings yet

- Risk and Return: Lessons From Market History: Solutions ManualDocument13 pagesRisk and Return: Lessons From Market History: Solutions ManualPhúc Nguyễn HữuNo ratings yet

- Đ Bích Trâm 1632300129 HW Week 4Document8 pagesĐ Bích Trâm 1632300129 HW Week 4GuruBaluLeoKingNo ratings yet

- Risk and ReturnDocument166 pagesRisk and ReturnShailendra ShresthaNo ratings yet

- Pmlect 2 BDocument24 pagesPmlect 2 BThe Learning Solutions Home TutorsNo ratings yet

- BUS328 Lê-Th Y-Tiên 1632300120 HW W4Document6 pagesBUS328 Lê-Th Y-Tiên 1632300120 HW W4GuruBaluLeoKing0% (1)

- Chap 10-11 PDFDocument41 pagesChap 10-11 PDFmnwongNo ratings yet

- CFA - 2 & 3. Quantitative MethodDocument22 pagesCFA - 2 & 3. Quantitative MethodChan Kwok WanNo ratings yet

- Portfolio RiskDocument24 pagesPortfolio RiskABC DEFNo ratings yet

- Ch11 Solutions 6thedDocument26 pagesCh11 Solutions 6thedMrinmay kunduNo ratings yet

- Extra Practice Exam 2 SolutionsDocument9 pagesExtra Practice Exam 2 SolutionsSteve SmithNo ratings yet

- Risk & ResturnDocument6 pagesRisk & ResturnTashfa AbbasNo ratings yet

- FM - ReportDocument9 pagesFM - ReportPyar Paolo dela CruzNo ratings yet

- IUBFINMAN5555Document25 pagesIUBFINMAN5555Sajan Razzak AkonNo ratings yet

- Financial Marketing Group 4Document31 pagesFinancial Marketing Group 4Emijiano RonquilloNo ratings yet

- Business Finance$ Chapter 6: Interest Rates and Bond ValuationDocument8 pagesBusiness Finance$ Chapter 6: Interest Rates and Bond ValuationRumana SultanaNo ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Answers To End-of-Chapter Problems B-121Document10 pagesChapter 10: Risk and Return: Lessons From Market History: Answers To End-of-Chapter Problems B-121Kaveh ArabpourNo ratings yet

- Week 4 Lecture PDFDocument69 pagesWeek 4 Lecture PDFAkshat TiwariNo ratings yet

- Chap 7Document8 pagesChap 7Dao Viet PhuongNo ratings yet

- Ipm 2Document62 pagesIpm 2Anna Lyssa BatasNo ratings yet

- Fundamentals of Corporate Finance 10th Edition Ross Solutions ManualDocument24 pagesFundamentals of Corporate Finance 10th Edition Ross Solutions Manualstarlikeharrowerexwp5No ratings yet

- Multinational Financial Management 9th Edition Shapiro Solutions ManualDocument12 pagesMultinational Financial Management 9th Edition Shapiro Solutions Manualdecardbudgerowhln100% (37)

- Multinational Financial Management 9Th Edition Shapiro Solutions Manual Full Chapter PDFDocument33 pagesMultinational Financial Management 9Th Edition Shapiro Solutions Manual Full Chapter PDFheadmostzooenule.s8hta6100% (11)

- FINS1613 Business Finance Tutorial Week 7 Solutions (RTBWJ Chapter 9)Document5 pagesFINS1613 Business Finance Tutorial Week 7 Solutions (RTBWJ Chapter 9)Edward YangNo ratings yet

- Exam FRM 2023Document6 pagesExam FRM 2023Slava HANo ratings yet

- Rate of Return Payoff Investment: + 1+discount 0Document10 pagesRate of Return Payoff Investment: + 1+discount 0Jair Azevedo JúniorNo ratings yet

- C+ F P N F+PDocument6 pagesC+ F P N F+PIfka HassanNo ratings yet

- Estimating Risk and Return On AssetDocument53 pagesEstimating Risk and Return On AssetShane Canila100% (2)

- JoseVicente SobrevillaDocument5 pagesJoseVicente Sobrevillasteve bobNo ratings yet

- Ross Chap010Document13 pagesRoss Chap010ravel0115.lopesNo ratings yet

- Rate of Return AnalysisDocument20 pagesRate of Return AnalysisM. Kurnia Sandy 1707113892No ratings yet

- Finance Chapter4 AnswersDocument4 pagesFinance Chapter4 AnswersyumnaNo ratings yet

- Chapter 7 Engineering EconomicsDocument19 pagesChapter 7 Engineering EconomicsharoonNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Eudaimonistic: HappinessDocument2 pagesEudaimonistic: HappinessAii Lyssa UNo ratings yet

- Capital Gains TaxDocument3 pagesCapital Gains TaxAii Lyssa UNo ratings yet

- Cooperative ManagementDocument2 pagesCooperative ManagementAii Lyssa U100% (2)

- Chapter 5Document8 pagesChapter 5Aii Lyssa UNo ratings yet

- What Is Bitcoin?Document3 pagesWhat Is Bitcoin?Aii Lyssa UNo ratings yet

- Risk ManagementDocument2 pagesRisk ManagementAii Lyssa UNo ratings yet

- Application of CryptocurrencyDocument10 pagesApplication of CryptocurrencyAii Lyssa UNo ratings yet

- Personal Finance ReportDocument10 pagesPersonal Finance ReportAii Lyssa UNo ratings yet

- The Change of Harm or Loss (PROBLEMA) Na Pwedeng Mangyayari Sa Business MoDocument6 pagesThe Change of Harm or Loss (PROBLEMA) Na Pwedeng Mangyayari Sa Business MoAii Lyssa UNo ratings yet

- Forever 21 Case Story: University of RichmondDocument14 pagesForever 21 Case Story: University of RichmondAii Lyssa UNo ratings yet

- Educational StatisticsDocument106 pagesEducational StatisticsRico A. Regala100% (1)

- Excercise On CI and Hypothesis TestingDocument10 pagesExcercise On CI and Hypothesis TestingAshadul AdNo ratings yet

- Klintoe PDFDocument31 pagesKlintoe PDFVelmurugan KNo ratings yet

- IMEKO TC3 2005 001uDocument6 pagesIMEKO TC3 2005 001uShokry AlkissyNo ratings yet

- Statistics (Z-Scores) : Burak Doğruyol Associate Professor of PsychologyDocument32 pagesStatistics (Z-Scores) : Burak Doğruyol Associate Professor of Psychologysimi savasNo ratings yet

- Poem Should Be IrreproducibleDocument5 pagesPoem Should Be IrreproducibleSeptian Rivandy LahayNo ratings yet

- Immediate Unrelated WordsDocument13 pagesImmediate Unrelated WordsshrutiNo ratings yet

- AP 2015 StatisticsDocument65 pagesAP 2015 Statisticssam sunNo ratings yet

- Higher Secondary School Students Perception About Online Classes During Pandemic With Reference To Selected Schools in Tiruchirappalli CityDocument5 pagesHigher Secondary School Students Perception About Online Classes During Pandemic With Reference To Selected Schools in Tiruchirappalli CityIJAR JOURNALNo ratings yet

- 5 The Normal DistributionDocument9 pages5 The Normal DistributionIndah PrasetyawatiNo ratings yet

- Aceptance SamplingDocument22 pagesAceptance Samplingjamie04No ratings yet

- Chapter 6 Section 1 Homework A: 6.10 Margin of Error and The Confidence IntervalDocument4 pagesChapter 6 Section 1 Homework A: 6.10 Margin of Error and The Confidence IntervalManishi GuptaNo ratings yet

- PMP Sample QuestionsDocument20 pagesPMP Sample Questionschbhargav99No ratings yet

- Effects of School Facilities On Student's PerformancesDocument101 pagesEffects of School Facilities On Student's PerformancesReliakkuma100% (1)

- SAMPLEDocument16 pagesSAMPLEEden SumilayNo ratings yet

- Ise Elementary Statistics A Step by Step Approach A Brief Version 8E 8Th Edition Allan G Bluman Full ChapterDocument67 pagesIse Elementary Statistics A Step by Step Approach A Brief Version 8E 8Th Edition Allan G Bluman Full Chapterkatelyn.willis396100% (5)

- Assignment 4 Area Under The Stanard Normal CurveDocument7 pagesAssignment 4 Area Under The Stanard Normal CurveAkamonwa KalengaNo ratings yet

- Tuto 2 Tutorial HYPOTHESIS TESTING FOR DIFFERENCE OF 2 POPULATION MEANSDocument3 pagesTuto 2 Tutorial HYPOTHESIS TESTING FOR DIFFERENCE OF 2 POPULATION MEANSSyaiful Ashraf Mohd AshriNo ratings yet

- EXAMPLE 2.13:: Applied Statistics Random Variables and Probability DistributionsDocument23 pagesEXAMPLE 2.13:: Applied Statistics Random Variables and Probability DistributionsAriaNo ratings yet

- Paper III Stastical Methods in EconomicsDocument115 pagesPaper III Stastical Methods in EconomicsghddNo ratings yet

- Inventory Policy Decisions: "Every Management Mistake Ends Up in Inventory." Michael C. BergeracDocument105 pagesInventory Policy Decisions: "Every Management Mistake Ends Up in Inventory." Michael C. Bergeracsurury100% (1)

- Peachtree SecuritiesDocument55 pagesPeachtree SecuritiesLouredaine MalingNo ratings yet

- Variance Guide Appendix C SasDocument55 pagesVariance Guide Appendix C SasIvanNo ratings yet

- Lean Six Sigma Operations Black Belt - Week 1: Sample Size CalculationDocument42 pagesLean Six Sigma Operations Black Belt - Week 1: Sample Size CalculationSteph JoseNo ratings yet

- Lecture-11,12 - Chapter 6 - Continuous Random Variables - Normal DistributionDocument107 pagesLecture-11,12 - Chapter 6 - Continuous Random Variables - Normal DistributionTasmiah HossainNo ratings yet

- Activity #6 SAMPLING DISTRIBUTIONSDocument8 pagesActivity #6 SAMPLING DISTRIBUTIONSleonessa jorban cortes0% (1)

- Quick Guide To Six Sigma StatisticsDocument4 pagesQuick Guide To Six Sigma StatisticsEnrico GambiniNo ratings yet

Download as docx, pdf, or txt

You might also like

- Fundamentals of Investments Valuation and Management 7th Edition by Jordan ISBN Solution ManualDocument9 pagesFundamentals of Investments Valuation and Management 7th Edition by Jordan ISBN Solution Manualbarbara0% (1)

- 2019 2 QMM AssignmentDocument3 pages2019 2 QMM AssignmentPranav0% (1)

- Key Chapter 7 Ms - TrangDocument6 pagesKey Chapter 7 Ms - TrangHoàng Việt VũNo ratings yet

- Hand Bone Age Atlas - Greulich-Pyle OXFORD RemakeDocument72 pagesHand Bone Age Atlas - Greulich-Pyle OXFORD RemakeSony Sutrisno100% (1)

- ASTM E1950-17 Standard Practice For Reporting Results From Methods of Chemical AnalysisDocument6 pagesASTM E1950-17 Standard Practice For Reporting Results From Methods of Chemical AnalysisDoina MarquezNo ratings yet

- Chapter 11Document25 pagesChapter 11M Eduardo BasantesNo ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Corporate FinanceDocument18 pagesChapter 10: Risk and Return: Lessons From Market History: Corporate FinancePháp NguyễnNo ratings yet

- Chapter 11Document28 pagesChapter 11Khoa LêNo ratings yet

- Corporate Finance Ross 10th Edition Solutions ManualDocument14 pagesCorporate Finance Ross 10th Edition Solutions ManualCatherineJohnsonabpg100% (46)

- Ch10 Solutions 6thedDocument14 pagesCh10 Solutions 6thedMrinmay kunduNo ratings yet

- Chapter 11Document27 pagesChapter 11Sufyan KhanNo ratings yet

- Corporate Finance CHDocument26 pagesCorporate Finance CHSK (아얀)No ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Corporate FinanceDocument15 pagesChapter 10: Risk and Return: Lessons From Market History: Corporate Financeirwan hermantriaNo ratings yet

- Faculty of Higher Education: Assignment Cover SheetDocument11 pagesFaculty of Higher Education: Assignment Cover SheetSyed Ali Hussain BokhariNo ratings yet

- Solutions Manual: Ross, Westerfield, and Jaffe Asia Global EditionDocument14 pagesSolutions Manual: Ross, Westerfield, and Jaffe Asia Global EditionRia FitriyanaNo ratings yet

- Chapter 10Document14 pagesChapter 10Beatrice ReynanciaNo ratings yet

- Chapter 11 &12 Tute SolsDocument9 pagesChapter 11 &12 Tute SolsRakeshNo ratings yet

- Lecture 8: Rate of Return Analysis: Instructional Material ForDocument20 pagesLecture 8: Rate of Return Analysis: Instructional Material ForAziezah PalintaNo ratings yet

- Chapter 10 SolutionDocument13 pagesChapter 10 SolutionPhước NgọcNo ratings yet

- Chapter 7 - ExercisesDocument6 pagesChapter 7 - Exercisesmin - radiseNo ratings yet

- Risk, Return, and The Security Market Line: B. Unsystematic C. D. Unsystematic E. FDocument15 pagesRisk, Return, and The Security Market Line: B. Unsystematic C. D. Unsystematic E. FTú Anh Nguyễn ThịNo ratings yet

- Assignment Capital Market and Portfolio ManagementDocument12 pagesAssignment Capital Market and Portfolio ManagementIshan MohindraNo ratings yet

- Risk & ReturnDocument57 pagesRisk & ReturnAyaz MeerNo ratings yet

- SOLUTION1. Exercise 1 PDFDocument10 pagesSOLUTION1. Exercise 1 PDFVanessa ThuyNo ratings yet

- Problem Set 4 SolutionDocument8 pagesProblem Set 4 SolutionMỹ HạnhNo ratings yet

- Concept of Risk and ReturnDocument40 pagesConcept of Risk and ReturnkomalissinghNo ratings yet

- Chapter 12 (Updated Oct 5)Document29 pagesChapter 12 (Updated Oct 5)Zoe LamNo ratings yet

- FIN437 Answers To The Recommended Questions Portfolio ManagementDocument6 pagesFIN437 Answers To The Recommended Questions Portfolio ManagementSenalNaldoNo ratings yet

- 1.3.2.1 Elaborate Problem Solving AssignmentDocument17 pages1.3.2.1 Elaborate Problem Solving AssignmentYess poooNo ratings yet

- HW12Document7 pagesHW12nma.work173No ratings yet

- Risk and Return: Lessons From Market History: Solutions ManualDocument13 pagesRisk and Return: Lessons From Market History: Solutions ManualPhúc Nguyễn HữuNo ratings yet

- Đ Bích Trâm 1632300129 HW Week 4Document8 pagesĐ Bích Trâm 1632300129 HW Week 4GuruBaluLeoKingNo ratings yet

- Risk and ReturnDocument166 pagesRisk and ReturnShailendra ShresthaNo ratings yet

- Pmlect 2 BDocument24 pagesPmlect 2 BThe Learning Solutions Home TutorsNo ratings yet

- BUS328 Lê-Th Y-Tiên 1632300120 HW W4Document6 pagesBUS328 Lê-Th Y-Tiên 1632300120 HW W4GuruBaluLeoKing0% (1)

- Chap 10-11 PDFDocument41 pagesChap 10-11 PDFmnwongNo ratings yet

- CFA - 2 & 3. Quantitative MethodDocument22 pagesCFA - 2 & 3. Quantitative MethodChan Kwok WanNo ratings yet

- Portfolio RiskDocument24 pagesPortfolio RiskABC DEFNo ratings yet

- Ch11 Solutions 6thedDocument26 pagesCh11 Solutions 6thedMrinmay kunduNo ratings yet

- Extra Practice Exam 2 SolutionsDocument9 pagesExtra Practice Exam 2 SolutionsSteve SmithNo ratings yet

- Risk & ResturnDocument6 pagesRisk & ResturnTashfa AbbasNo ratings yet

- FM - ReportDocument9 pagesFM - ReportPyar Paolo dela CruzNo ratings yet

- IUBFINMAN5555Document25 pagesIUBFINMAN5555Sajan Razzak AkonNo ratings yet

- Financial Marketing Group 4Document31 pagesFinancial Marketing Group 4Emijiano RonquilloNo ratings yet

- Business Finance$ Chapter 6: Interest Rates and Bond ValuationDocument8 pagesBusiness Finance$ Chapter 6: Interest Rates and Bond ValuationRumana SultanaNo ratings yet

- Chapter 10: Risk and Return: Lessons From Market History: Answers To End-of-Chapter Problems B-121Document10 pagesChapter 10: Risk and Return: Lessons From Market History: Answers To End-of-Chapter Problems B-121Kaveh ArabpourNo ratings yet

- Week 4 Lecture PDFDocument69 pagesWeek 4 Lecture PDFAkshat TiwariNo ratings yet

- Chap 7Document8 pagesChap 7Dao Viet PhuongNo ratings yet

- Ipm 2Document62 pagesIpm 2Anna Lyssa BatasNo ratings yet

- Fundamentals of Corporate Finance 10th Edition Ross Solutions ManualDocument24 pagesFundamentals of Corporate Finance 10th Edition Ross Solutions Manualstarlikeharrowerexwp5No ratings yet

- Multinational Financial Management 9th Edition Shapiro Solutions ManualDocument12 pagesMultinational Financial Management 9th Edition Shapiro Solutions Manualdecardbudgerowhln100% (37)

- Multinational Financial Management 9Th Edition Shapiro Solutions Manual Full Chapter PDFDocument33 pagesMultinational Financial Management 9Th Edition Shapiro Solutions Manual Full Chapter PDFheadmostzooenule.s8hta6100% (11)

- FINS1613 Business Finance Tutorial Week 7 Solutions (RTBWJ Chapter 9)Document5 pagesFINS1613 Business Finance Tutorial Week 7 Solutions (RTBWJ Chapter 9)Edward YangNo ratings yet

- Exam FRM 2023Document6 pagesExam FRM 2023Slava HANo ratings yet

- Rate of Return Payoff Investment: + 1+discount 0Document10 pagesRate of Return Payoff Investment: + 1+discount 0Jair Azevedo JúniorNo ratings yet

- C+ F P N F+PDocument6 pagesC+ F P N F+PIfka HassanNo ratings yet

- Estimating Risk and Return On AssetDocument53 pagesEstimating Risk and Return On AssetShane Canila100% (2)

- JoseVicente SobrevillaDocument5 pagesJoseVicente Sobrevillasteve bobNo ratings yet

- Ross Chap010Document13 pagesRoss Chap010ravel0115.lopesNo ratings yet

- Rate of Return AnalysisDocument20 pagesRate of Return AnalysisM. Kurnia Sandy 1707113892No ratings yet

- Finance Chapter4 AnswersDocument4 pagesFinance Chapter4 AnswersyumnaNo ratings yet

- Chapter 7 Engineering EconomicsDocument19 pagesChapter 7 Engineering EconomicsharoonNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Eudaimonistic: HappinessDocument2 pagesEudaimonistic: HappinessAii Lyssa UNo ratings yet

- Capital Gains TaxDocument3 pagesCapital Gains TaxAii Lyssa UNo ratings yet

- Cooperative ManagementDocument2 pagesCooperative ManagementAii Lyssa U100% (2)

- Chapter 5Document8 pagesChapter 5Aii Lyssa UNo ratings yet

- What Is Bitcoin?Document3 pagesWhat Is Bitcoin?Aii Lyssa UNo ratings yet

- Risk ManagementDocument2 pagesRisk ManagementAii Lyssa UNo ratings yet

- Application of CryptocurrencyDocument10 pagesApplication of CryptocurrencyAii Lyssa UNo ratings yet

- Personal Finance ReportDocument10 pagesPersonal Finance ReportAii Lyssa UNo ratings yet

- The Change of Harm or Loss (PROBLEMA) Na Pwedeng Mangyayari Sa Business MoDocument6 pagesThe Change of Harm or Loss (PROBLEMA) Na Pwedeng Mangyayari Sa Business MoAii Lyssa UNo ratings yet

- Forever 21 Case Story: University of RichmondDocument14 pagesForever 21 Case Story: University of RichmondAii Lyssa UNo ratings yet

- Educational StatisticsDocument106 pagesEducational StatisticsRico A. Regala100% (1)

- Excercise On CI and Hypothesis TestingDocument10 pagesExcercise On CI and Hypothesis TestingAshadul AdNo ratings yet

- Klintoe PDFDocument31 pagesKlintoe PDFVelmurugan KNo ratings yet

- IMEKO TC3 2005 001uDocument6 pagesIMEKO TC3 2005 001uShokry AlkissyNo ratings yet

- Statistics (Z-Scores) : Burak Doğruyol Associate Professor of PsychologyDocument32 pagesStatistics (Z-Scores) : Burak Doğruyol Associate Professor of Psychologysimi savasNo ratings yet

- Poem Should Be IrreproducibleDocument5 pagesPoem Should Be IrreproducibleSeptian Rivandy LahayNo ratings yet

- Immediate Unrelated WordsDocument13 pagesImmediate Unrelated WordsshrutiNo ratings yet

- AP 2015 StatisticsDocument65 pagesAP 2015 Statisticssam sunNo ratings yet

- Higher Secondary School Students Perception About Online Classes During Pandemic With Reference To Selected Schools in Tiruchirappalli CityDocument5 pagesHigher Secondary School Students Perception About Online Classes During Pandemic With Reference To Selected Schools in Tiruchirappalli CityIJAR JOURNALNo ratings yet

- 5 The Normal DistributionDocument9 pages5 The Normal DistributionIndah PrasetyawatiNo ratings yet

- Aceptance SamplingDocument22 pagesAceptance Samplingjamie04No ratings yet

- Chapter 6 Section 1 Homework A: 6.10 Margin of Error and The Confidence IntervalDocument4 pagesChapter 6 Section 1 Homework A: 6.10 Margin of Error and The Confidence IntervalManishi GuptaNo ratings yet

- PMP Sample QuestionsDocument20 pagesPMP Sample Questionschbhargav99No ratings yet

- Effects of School Facilities On Student's PerformancesDocument101 pagesEffects of School Facilities On Student's PerformancesReliakkuma100% (1)

- SAMPLEDocument16 pagesSAMPLEEden SumilayNo ratings yet

- Ise Elementary Statistics A Step by Step Approach A Brief Version 8E 8Th Edition Allan G Bluman Full ChapterDocument67 pagesIse Elementary Statistics A Step by Step Approach A Brief Version 8E 8Th Edition Allan G Bluman Full Chapterkatelyn.willis396100% (5)

- Assignment 4 Area Under The Stanard Normal CurveDocument7 pagesAssignment 4 Area Under The Stanard Normal CurveAkamonwa KalengaNo ratings yet

- Tuto 2 Tutorial HYPOTHESIS TESTING FOR DIFFERENCE OF 2 POPULATION MEANSDocument3 pagesTuto 2 Tutorial HYPOTHESIS TESTING FOR DIFFERENCE OF 2 POPULATION MEANSSyaiful Ashraf Mohd AshriNo ratings yet

- EXAMPLE 2.13:: Applied Statistics Random Variables and Probability DistributionsDocument23 pagesEXAMPLE 2.13:: Applied Statistics Random Variables and Probability DistributionsAriaNo ratings yet

- Paper III Stastical Methods in EconomicsDocument115 pagesPaper III Stastical Methods in EconomicsghddNo ratings yet

- Inventory Policy Decisions: "Every Management Mistake Ends Up in Inventory." Michael C. BergeracDocument105 pagesInventory Policy Decisions: "Every Management Mistake Ends Up in Inventory." Michael C. Bergeracsurury100% (1)

- Peachtree SecuritiesDocument55 pagesPeachtree SecuritiesLouredaine MalingNo ratings yet

- Variance Guide Appendix C SasDocument55 pagesVariance Guide Appendix C SasIvanNo ratings yet

- Lean Six Sigma Operations Black Belt - Week 1: Sample Size CalculationDocument42 pagesLean Six Sigma Operations Black Belt - Week 1: Sample Size CalculationSteph JoseNo ratings yet

- Lecture-11,12 - Chapter 6 - Continuous Random Variables - Normal DistributionDocument107 pagesLecture-11,12 - Chapter 6 - Continuous Random Variables - Normal DistributionTasmiah HossainNo ratings yet

- Activity #6 SAMPLING DISTRIBUTIONSDocument8 pagesActivity #6 SAMPLING DISTRIBUTIONSleonessa jorban cortes0% (1)

- Quick Guide To Six Sigma StatisticsDocument4 pagesQuick Guide To Six Sigma StatisticsEnrico GambiniNo ratings yet