Download as pdf or txt

You might also like

- CHAPTER 13 Solved Problems PDFDocument8 pagesCHAPTER 13 Solved Problems PDF7100507100% (3)

- WORKING CAPITAL Requirement NumericalDocument9 pagesWORKING CAPITAL Requirement Numericalbandgar_00770% (10)

- The Sabat Corporation Manufactures and Sells Two ProductsDocument4 pagesThe Sabat Corporation Manufactures and Sells Two ProductsElliot RichardNo ratings yet

- Working Capital Management 3Document11 pagesWorking Capital Management 3fatimabiriq799No ratings yet

- Working Capital Practical QuestionsDocument8 pagesWorking Capital Practical Questionsfatimabiriq799No ratings yet

- Numericals 1Document6 pagesNumericals 1Amita ChoudharyNo ratings yet

- Working CapitalDocument38 pagesWorking CapitalMonicaNo ratings yet

- Working Capital: R.KasilingamDocument54 pagesWorking Capital: R.Kasilingamvijayadarshini vNo ratings yet

- SBS Mba FM4Document23 pagesSBS Mba FM4deepakNo ratings yet

- Chapter 8 Master BudgetingDocument4 pagesChapter 8 Master BudgetingHanif Khan SrkNo ratings yet

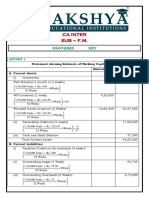

- Ca Inter-F.m.03-07-2023-KeyDocument3 pagesCa Inter-F.m.03-07-2023-KeyChintuNo ratings yet

- BCH 503 SM07Document2 pagesBCH 503 SM07sugandh bajajNo ratings yet

- Financial Management - Notes NumericalsDocument6 pagesFinancial Management - Notes NumericalsSandeep SahadeokarNo ratings yet

- FM New SumsDocument13 pagesFM New SumsINTER SMARTIANSNo ratings yet

- Brewer 6e Practice Exam - Chapter 7Document3 pagesBrewer 6e Practice Exam - Chapter 7real johnNo ratings yet

- GNB14eCh08ExamDocument3 pagesGNB14eCh08ExamFicky ZulandoNo ratings yet

- Net WC QuestionsDocument5 pagesNet WC QuestionsPoonam KhattriNo ratings yet

- Working CapitalDocument3 pagesWorking Capitalfxn fndNo ratings yet

- Existing Working Capital CalculationDocument2 pagesExisting Working Capital CalculationCma Pushparaj KulkarniNo ratings yet

- Solution 6-37Document3 pagesSolution 6-37Tszkwan YuNo ratings yet

- Problems and SolutionsDocument7 pagesProblems and SolutionsMohitAhuja0% (1)

- Dec 21Document26 pagesDec 21Prabhat Kumar GuptaNo ratings yet

- 3 - CostingDocument26 pages3 - Costingamitjaiswal9532No ratings yet

- Solution To WC Requirement Probs On The SlideDocument2 pagesSolution To WC Requirement Probs On The SlideNowshad AyubNo ratings yet

- 18415compsuggans PCC FM Chapter7Document13 pages18415compsuggans PCC FM Chapter7Mukunthan RBNo ratings yet

- Comp. ExamDocument11 pagesComp. ExamProf. Nisaif JasimNo ratings yet

- FN502 Additional ProblemsDocument3 pagesFN502 Additional Problemsdpr7033No ratings yet

- Garrison (Asian Edition) Practice Exam - Chapter 10Document2 pagesGarrison (Asian Edition) Practice Exam - Chapter 10Johnsen PratamaNo ratings yet

- 02 Ratio Analysis Solution FT FileDocument22 pages02 Ratio Analysis Solution FT Filensm2zmvnbbNo ratings yet

- Exercise Working CapitalDocument4 pagesExercise Working CapitalShafiul AzamNo ratings yet

- Management Accounting (Acct 321) P2 PT 2ND Trimester 2017Document5 pagesManagement Accounting (Acct 321) P2 PT 2ND Trimester 2017Nodeh Deh SpartaNo ratings yet

- Intermediate - FM - Suggested Answer PaperDocument4 pagesIntermediate - FM - Suggested Answer Paperchromabooka111No ratings yet

- Estimation of Working Capital Requirement: Vineet Jogalekar 1PT10MBA84Document10 pagesEstimation of Working Capital Requirement: Vineet Jogalekar 1PT10MBA84Vineet JogalekarNo ratings yet

- Assignment 1 SolutionDocument2 pagesAssignment 1 Solutiondivya kalyaniNo ratings yet

- Working Capital Management PDFDocument46 pagesWorking Capital Management PDFNizar AhamedNo ratings yet

- Costing Full Length 2 - May 24 (Solution) 8-4Document16 pagesCosting Full Length 2 - May 24 (Solution) 8-4Jyoti ManwaniNo ratings yet

- 09 Treasury & Cash Management 7CDocument7 pages09 Treasury & Cash Management 7CChartered Accountant YASHNo ratings yet

- (Lower of Production / Market Demand) (I × II) : © The Institute of Chartered Accountants of IndiaDocument14 pages(Lower of Production / Market Demand) (I × II) : © The Institute of Chartered Accountants of IndiaAnkitaNo ratings yet

- MTP 19 53 Answers 1713511058Document19 pagesMTP 19 53 Answers 1713511058prathammishra1809No ratings yet

- 2020-06 Icmab FL 001 Pac Year Question June 2020Document3 pages2020-06 Icmab FL 001 Pac Year Question June 2020Mohammad ShahidNo ratings yet

- Management AccountingDocument7 pagesManagement AccountingNageshwar singhNo ratings yet

- AD32 Fundamentals of Management Accounting - Pilot Question Paper-1Document3 pagesAD32 Fundamentals of Management Accounting - Pilot Question Paper-1benard owinoNo ratings yet

- Faculty of Business and Management BBA/DBA 211 Managerial AccountingDocument4 pagesFaculty of Business and Management BBA/DBA 211 Managerial AccountingMichael AronNo ratings yet

- Incomplete RecordsDocument32 pagesIncomplete RecordsSunil KumarNo ratings yet

- IAS 16 MCQs SolutionsDocument3 pagesIAS 16 MCQs SolutionsAhmad SaleemNo ratings yet

- Cost Accounting 2 Fourth Year Second Semester 2020-2021 Review Questions CH (7) & CH (8) Part (Dr. El Ghareeb) (5) Presented By: Dr. Ahmed MokhtarDocument11 pagesCost Accounting 2 Fourth Year Second Semester 2020-2021 Review Questions CH (7) & CH (8) Part (Dr. El Ghareeb) (5) Presented By: Dr. Ahmed Mokhtarمحمود احمدNo ratings yet

- 6a. Cash BudgetDocument4 pages6a. Cash BudgetMadiha JamalNo ratings yet

- BAFINMAX Learning Activity 1 Finals - With Answers - StudentsDocument5 pagesBAFINMAX Learning Activity 1 Finals - With Answers - Studentsfaye pantiNo ratings yet

- Budgets 2 exercisesDocument4 pagesBudgets 2 exerciseshannyhosnyNo ratings yet

- Chapter 4 Management of WCDocument15 pagesChapter 4 Management of WCAbhishek TiwariNo ratings yet

- Working Capital ManagementDocument2 pagesWorking Capital ManagementAnkit ThakkarNo ratings yet

- Uneeso Ent P2Document4 pagesUneeso Ent P2Otai Ezra100% (1)

- Standard CostingDocument1 pageStandard CostingPrasad NaikNo ratings yet

- Ex 5Document9 pagesEx 5farahamin359No ratings yet

- Accountancy Practical 2023-24-1Document2 pagesAccountancy Practical 2023-24-1uzmazeeshan10No ratings yet

- BASTRCSX Learning Activity 5 - With AnswersDocument10 pagesBASTRCSX Learning Activity 5 - With AnswersChel EscuetaNo ratings yet

- Case Analysis (1 30)Document3 pagesCase Analysis (1 30)manishadaaNo ratings yet

- Fofm Word File Roll No 381 To 390Document26 pagesFofm Word File Roll No 381 To 390Spandan ThakkarNo ratings yet

- Economics Word File Roll No 381 To 390Document19 pagesEconomics Word File Roll No 381 To 390Spandan ThakkarNo ratings yet

- Fom Word File of Batch-6Document25 pagesFom Word File of Batch-6Spandan ThakkarNo ratings yet

- Sem 2 - Theory Assgn - 2020-21Document8 pagesSem 2 - Theory Assgn - 2020-21Spandan ThakkarNo ratings yet

- English AssignmentDocument15 pagesEnglish AssignmentSpandan ThakkarNo ratings yet

- Sem-1 Economics (D) 381-390Document25 pagesSem-1 Economics (D) 381-390Spandan ThakkarNo ratings yet

- Pankti Mittal ShethDocument17 pagesPankti Mittal ShethSpandan ThakkarNo ratings yet

- 5 Industrial Report On Cadila HealthDocument50 pages5 Industrial Report On Cadila HealthSpandan ThakkarNo ratings yet

- SpectrumDocument1 pageSpectrumSpandan ThakkarNo ratings yet

- Production Management - Practical AssignmentDocument6 pagesProduction Management - Practical AssignmentSpandan ThakkarNo ratings yet

- Capacitor ManufacturerDocument14 pagesCapacitor ManufacturerSpandan ThakkarNo ratings yet

- Indexing Table ManufacturerDocument8 pagesIndexing Table ManufacturerSpandan ThakkarNo ratings yet

- Income EffectDocument3 pagesIncome EffectSpandan Thakkar100% (1)