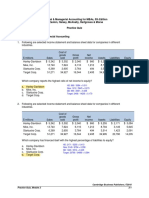

Week 4 TUTE Chapter 3 Questions - 22722924

Week 4 TUTE Chapter 3 Questions - 22722924

You might also like

- Navigating Oil and Gas Securitization TransactionsDocument21 pagesNavigating Oil and Gas Securitization TransactionsEliecer PalaciosNo ratings yet

- ACBP5122wA1 PDFDocument9 pagesACBP5122wA1 PDFAmmarah Ramnarain0% (1)

- Test Bank For Modern Advanced Accounting in Canada 9th by Hilton Full DownloadDocument118 pagesTest Bank For Modern Advanced Accounting in Canada 9th by Hilton Full DownloadnathanielgarciaqznxeafdibNo ratings yet

- ACCT503 W4 Case Study V2Document18 pagesACCT503 W4 Case Study V2AriunaaBoldNo ratings yet

- 000 MergedDocument134 pages000 Mergedhira malikNo ratings yet

- Acc133 PQ4Document2 pagesAcc133 PQ4Karina Barretto Agnes0% (2)

- Reading 21 Financial Analysis Techniques - AnswersDocument72 pagesReading 21 Financial Analysis Techniques - AnswersMohammed GamalNo ratings yet

- AACT 2173 FM Lesson 4 Tutorial (Additional)Document11 pagesAACT 2173 FM Lesson 4 Tutorial (Additional)Ashvin Kaur100% (1)

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- Critical Thinking, Analysis and Decision Making: Week 4 - Renascence CorporationDocument86 pagesCritical Thinking, Analysis and Decision Making: Week 4 - Renascence CorporationxsnoweyxNo ratings yet

- Church Company Completes These Transactions and Events During MarchDocument56 pagesChurch Company Completes These Transactions and Events During Marchlaale dijaanNo ratings yet

- Question # 1: Calculation of EoqDocument3 pagesQuestion # 1: Calculation of EoqUnzila AtiqNo ratings yet

- Disposal of Subsidiary PDFDocument9 pagesDisposal of Subsidiary PDFStavri Makri SmirilliNo ratings yet

- Coca-Cola Residual Income Valuation - STUDENTSDocument7 pagesCoca-Cola Residual Income Valuation - STUDENTSdeepak mishraNo ratings yet

- Layout Plan For RCC Columns and FootingsDocument1 pageLayout Plan For RCC Columns and FootingsHusen GhoriNo ratings yet

- This Study Resource Was: Adjust CreditDocument4 pagesThis Study Resource Was: Adjust CreditJalaj GuptaNo ratings yet

- Question & Answer 28072015 InventoryDocument5 pagesQuestion & Answer 28072015 InventoryGreen StoneNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 2: Accrual Accounting and Income DeterminationDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 2: Accrual Accounting and Income DeterminationDylan AdrianNo ratings yet

- CH 03 - SolutionsDocument17 pagesCH 03 - SolutionsLuong Hoang Vu80% (5)

- When Accounting For The Deconsolidation of A Subsidiary 1Document1 pageWhen Accounting For The Deconsolidation of A Subsidiary 1Louiza Kyla AridaNo ratings yet

- Government Regulation 24/2012Document14 pagesGovernment Regulation 24/2012Adria SaputeroNo ratings yet

- 655 Week 9 Notes PDFDocument75 pages655 Week 9 Notes PDFsanaha786No ratings yet

- AC3103 Seminar 10 AnswersDocument3 pagesAC3103 Seminar 10 AnswersKrithika Naidu0% (1)

- Ch02 SolutionDocument6 pagesCh02 SolutionMalekNo ratings yet

- The Following Data Relate To The Operations of Slick SoftwareDocument2 pagesThe Following Data Relate To The Operations of Slick SoftwareAmit PandeyNo ratings yet

- Saad Karimi (Assignment 1)Document10 pagesSaad Karimi (Assignment 1)pakistan50% (2)

- E5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDocument6 pagesE5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDylan AdrianNo ratings yet

- Beechy7e Vol 1 SM Ch08Document59 pagesBeechy7e Vol 1 SM Ch08Aayush AgarwalNo ratings yet

- Mac006 A T2 2021 FexDocument7 pagesMac006 A T2 2021 FexHaris MalikNo ratings yet

- ACCT551 - Week 7 HomeworkDocument10 pagesACCT551 - Week 7 HomeworkDominickdadNo ratings yet

- Ross 12e PPT Ch06 CalculatorDocument71 pagesRoss 12e PPT Ch06 CalculatorKirthagan SelvamNo ratings yet

- Suggested Answers CAP III - Dec 2018 PDFDocument144 pagesSuggested Answers CAP III - Dec 2018 PDFsarojdawadiNo ratings yet

- t10 2010 Jun QDocument10 pagest10 2010 Jun QAjay TakiarNo ratings yet

- HI5020Document13 pagesHI5020takeshiru000No ratings yet

- Capstone Week 3 AssignmentDocument7 pagesCapstone Week 3 Assignmentleelee0302No ratings yet

- CUAC 408 Group Assignment 1 2021Document6 pagesCUAC 408 Group Assignment 1 2021Blessed Nyama100% (1)

- 1 Insurance ClaimDocument10 pages1 Insurance ClaimBAZINGA100% (1)

- Advanced Taxation Practice Question QuestionDocument8 pagesAdvanced Taxation Practice Question QuestionDanisa NdhlovuNo ratings yet

- Annual Report For Eng (18-19Document396 pagesAnnual Report For Eng (18-19shree salj dugda utpadakNo ratings yet

- Paper Ii, Question 1: Preparing For The 2003 UFE Understanding The Evaluation Methodology June 2002Document16 pagesPaper Ii, Question 1: Preparing For The 2003 UFE Understanding The Evaluation Methodology June 2002xsnoweyxNo ratings yet

- ACCO 420 Final F2020 Version 2Document4 pagesACCO 420 Final F2020 Version 2Wasif SethNo ratings yet

- Accounting For Investment in Variable Income Bearing Securities Lesson 27Document10 pagesAccounting For Investment in Variable Income Bearing Securities Lesson 27Sumantha SahaNo ratings yet

- Section VI: NRV Vs Fair Value: ExampleDocument5 pagesSection VI: NRV Vs Fair Value: ExamplebinuNo ratings yet

- Financial InstrumentsDocument14 pagesFinancial InstrumentsPriya NairNo ratings yet

- Barstow Company Is Contemplating The Acquisition of The Net AssetsDocument1 pageBarstow Company Is Contemplating The Acquisition of The Net AssetsMuhammad ShahidNo ratings yet

- CH 04 - SolutionsDocument17 pagesCH 04 - SolutionsLuong Hoang Vu100% (2)

- Chapter Eight: Cost-Volume-Profit AnalysisDocument34 pagesChapter Eight: Cost-Volume-Profit AnalysisBartholomew SzoldNo ratings yet

- AC2101 SemGrp4 Team6Document34 pagesAC2101 SemGrp4 Team6Kwang Yi JuinNo ratings yet

- CAB AcctDocument9 pagesCAB AcctA.J. ChuaNo ratings yet

- Cottrell Sunningdale SeptDec2023Document3 pagesCottrell Sunningdale SeptDec2023Adilah AzamNo ratings yet

- Bharti AXA Life Insurance Company LimitedDocument8 pagesBharti AXA Life Insurance Company LimitedJinal SanghviNo ratings yet

- Statement of Transaction - Sale or Gift of Motor Vehicle, Trailer, All-Terrain Vehicle (ATV), Vessel (Boat), or SnowmobileDocument2 pagesStatement of Transaction - Sale or Gift of Motor Vehicle, Trailer, All-Terrain Vehicle (ATV), Vessel (Boat), or SnowmobilePramedicaPerdanaPutra100% (1)

- Summarising Analysing DataDocument19 pagesSummarising Analysing DataSanjeev JayaratnaNo ratings yet

- PROBLEMS in ForexDocument2 pagesPROBLEMS in ForexPrethivi RajNo ratings yet

- Financial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizDocument4 pagesFinancial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizLevi AlvesNo ratings yet

- Ratios - Profitability, Market &Document46 pagesRatios - Profitability, Market &Jess AlexNo ratings yet

- Fire Insurance ClaimsDocument43 pagesFire Insurance ClaimsArshad Mohd100% (1)

- Manual 16 Jun 2021 - Part 1Document6 pagesManual 16 Jun 2021 - Part 1Feni AlvitaNo ratings yet

- Calculation - General Mills - PillsburyDocument10 pagesCalculation - General Mills - PillsburyAryan AnandNo ratings yet

- Portfolio Management PDFDocument27 pagesPortfolio Management PDFdwkr giriNo ratings yet

- Test 3 - Chap 24Document7 pagesTest 3 - Chap 24Bhushan Sawant100% (1)

- Week 4 TUTE Chapter 3 QuestionsDocument4 pagesWeek 4 TUTE Chapter 3 QuestionsTom ChanNo ratings yet

- Why Are Financial Statements Important?Document23 pagesWhy Are Financial Statements Important?Dylan AdrianNo ratings yet

- OTC Sponsorship Proposals 2020 - 2021Document4 pagesOTC Sponsorship Proposals 2020 - 2021Dylan AdrianNo ratings yet

- FINA3307 Lecture1Document22 pagesFINA3307 Lecture1Dylan AdrianNo ratings yet

- Non-Linear Forecasting in High Frequency Time SeriesDocument17 pagesNon-Linear Forecasting in High Frequency Time SeriesDylan AdrianNo ratings yet

- (JP Morgan) Relative Value Single Stock VolatilityDocument36 pages(JP Morgan) Relative Value Single Stock VolatilityDylan Adrian100% (1)

- Liquidity and Convergence Trading in IRS SpreadsDocument13 pagesLiquidity and Convergence Trading in IRS SpreadsDylan AdrianNo ratings yet

- Dynamic Model For Forward CurveDocument61 pagesDynamic Model For Forward CurveDylan AdrianNo ratings yet

- Week 2 TUTE Chapter 1 SolutionsDocument6 pagesWeek 2 TUTE Chapter 1 SolutionsDylan AdrianNo ratings yet

- w1 TuteDocument4 pagesw1 TuteDylan AdrianNo ratings yet

- RBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Document11 pagesRBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Dylan AdrianNo ratings yet

- RBCCapitalMarkets RBCRatesStrategy-MuchfortheRBAtoponderafterRBNZholdfire Aug 18 2021Document1 pageRBCCapitalMarkets RBCRatesStrategy-MuchfortheRBAtoponderafterRBNZholdfire Aug 18 2021Dylan AdrianNo ratings yet

- Amplitude Trend CharacteristicsDocument17 pagesAmplitude Trend CharacteristicsDylan AdrianNo ratings yet

- Australian Rates Strategy: Back To The Belly - Looking To Receive 2-5-10s, 2y/2y AU vs. UKDocument5 pagesAustralian Rates Strategy: Back To The Belly - Looking To Receive 2-5-10s, 2y/2y AU vs. UKDylan AdrianNo ratings yet

- ZacksInvestmentResearchInc ZacksMarketStrategy Aug 09 2021Document75 pagesZacksInvestmentResearchInc ZacksMarketStrategy Aug 09 2021Dylan AdrianNo ratings yet

- E5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDocument6 pagesE5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDylan AdrianNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 4: Structure of The Balance Sheet and Statement of Cash FlowsDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 4: Structure of The Balance Sheet and Statement of Cash FlowsDylan AdrianNo ratings yet

- Free Decision Tree Diagram TemplateDocument8 pagesFree Decision Tree Diagram TemplateBadrun TamanNo ratings yet

- Assignment 2: I. Complete All Problems and Applications at The End of Chapter 23Document6 pagesAssignment 2: I. Complete All Problems and Applications at The End of Chapter 23Phước Đào QuangNo ratings yet

- II Puc Economics Mind Maps For 2023 ExamDocument14 pagesII Puc Economics Mind Maps For 2023 Examm2699291No ratings yet

- Dr. Nick Marasigan AccountsDocument11 pagesDr. Nick Marasigan AccountsNicole SarmientoNo ratings yet

- Potentialities of Capitalistic Growth (IGNOU)Document5 pagesPotentialities of Capitalistic Growth (IGNOU)saqueeb111No ratings yet

- V890Document1 pageV890Arcadie ApostolNo ratings yet

- Spink Auction World Vanknotes 23231Document188 pagesSpink Auction World Vanknotes 23231Nikola KukrikaNo ratings yet

- Cost AccountingDocument16 pagesCost AccountingDennis LacsonNo ratings yet

- MR Notice To Shipping No. N-7-2005 To: Steamship Agents, Owners and Operators Subject: Panama Canal Transit Reservation SystemDocument17 pagesMR Notice To Shipping No. N-7-2005 To: Steamship Agents, Owners and Operators Subject: Panama Canal Transit Reservation Systemsaurav naskarNo ratings yet

- (A) Regress Log of Wages On A Constant and The Female Dummy. Paste Output HereDocument5 pages(A) Regress Log of Wages On A Constant and The Female Dummy. Paste Output Hereakshay patriNo ratings yet

- CHB Back-Up ComputationDocument36 pagesCHB Back-Up Computationkhim tugasNo ratings yet

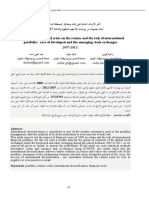

- تأثير الأزمات المالية على عائد ومخاطر المحفظة المالية الدولية - - حالة مجموعة من بورصات الأسهم المتطورة والناشئة 2007-2012 -Document16 pagesتأثير الأزمات المالية على عائد ومخاطر المحفظة المالية الدولية - - حالة مجموعة من بورصات الأسهم المتطورة والناشئة 2007-2012 -MohamedNo ratings yet

- Econ Premium Fe-Test Certificate Iso 15848-1 Co1 - Co3 and Ta-Luft-RtDocument3 pagesEcon Premium Fe-Test Certificate Iso 15848-1 Co1 - Co3 and Ta-Luft-Rtemperor_vamsiNo ratings yet

- Flat Sale in EnglishDocument7 pagesFlat Sale in EnglishDeep HiraniNo ratings yet

- Most Expensive Currency - Google SearchDocument1 pageMost Expensive Currency - Google SearchAbdulla JamalNo ratings yet

- Ventura, Marymickaellar Chapter6 (2,3,4,20,21)Document2 pagesVentura, Marymickaellar Chapter6 (2,3,4,20,21)Mary VenturaNo ratings yet

- F26a.0 - F30cy.0 - F32a.0 - F40B.0Document16 pagesF26a.0 - F30cy.0 - F32a.0 - F40B.0Canguro AndadorNo ratings yet

- HX 75Document1 pageHX 75cs gunungparaNo ratings yet

- Solution Practice 1 Share CapitalDocument2 pagesSolution Practice 1 Share CapitalMya Hmuu KhinNo ratings yet

- Unit-6 Subsidiary Books PDFDocument52 pagesUnit-6 Subsidiary Books PDFShiva AggarwalNo ratings yet

- Dongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891Document10 pagesDongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891shirley100% (57)

- Sample Requistion For Jay Vijay LLP Godrej Site DATED 23 JAN 2024Document4 pagesSample Requistion For Jay Vijay LLP Godrej Site DATED 23 JAN 2024kiranmisale7No ratings yet

- Chapter 5 Summary NotesDocument1 pageChapter 5 Summary Notesali aknarNo ratings yet

- Regulation No 332 2014 Establishment and Determination of The Procedure of The Accounting and Auditing Board of EthiopiaDocument20 pagesRegulation No 332 2014 Establishment and Determination of The Procedure of The Accounting and Auditing Board of EthiopiajemalNo ratings yet

- Investasi Dan Pasar ModalDocument19 pagesInvestasi Dan Pasar ModalKrisna AdithaNo ratings yet

- 2023-2024 Fix B PTS KELAS 12Document8 pages2023-2024 Fix B PTS KELAS 12milatrikanti80No ratings yet

- Multiple Choice Questions (MCQ) Q.1 - Q.10 Carry ONE Mark EachDocument34 pagesMultiple Choice Questions (MCQ) Q.1 - Q.10 Carry ONE Mark EachKaran KumarNo ratings yet

- Week 8 Media and The AudienceDocument3 pagesWeek 8 Media and The AudienceADMATEZA UNGGUINo ratings yet

- Warehouses and Headquarters Addresses and Price List TemplateDocument22 pagesWarehouses and Headquarters Addresses and Price List TemplateTudor FlorinNo ratings yet

Download as docx, pdf, or txt

You might also like

- Navigating Oil and Gas Securitization TransactionsDocument21 pagesNavigating Oil and Gas Securitization TransactionsEliecer PalaciosNo ratings yet

- ACBP5122wA1 PDFDocument9 pagesACBP5122wA1 PDFAmmarah Ramnarain0% (1)

- Test Bank For Modern Advanced Accounting in Canada 9th by Hilton Full DownloadDocument118 pagesTest Bank For Modern Advanced Accounting in Canada 9th by Hilton Full DownloadnathanielgarciaqznxeafdibNo ratings yet

- ACCT503 W4 Case Study V2Document18 pagesACCT503 W4 Case Study V2AriunaaBoldNo ratings yet

- 000 MergedDocument134 pages000 Mergedhira malikNo ratings yet

- Acc133 PQ4Document2 pagesAcc133 PQ4Karina Barretto Agnes0% (2)

- Reading 21 Financial Analysis Techniques - AnswersDocument72 pagesReading 21 Financial Analysis Techniques - AnswersMohammed GamalNo ratings yet

- AACT 2173 FM Lesson 4 Tutorial (Additional)Document11 pagesAACT 2173 FM Lesson 4 Tutorial (Additional)Ashvin Kaur100% (1)

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 1: Introduction To Financial Statement AnalysisDylan AdrianNo ratings yet

- Critical Thinking, Analysis and Decision Making: Week 4 - Renascence CorporationDocument86 pagesCritical Thinking, Analysis and Decision Making: Week 4 - Renascence CorporationxsnoweyxNo ratings yet

- Church Company Completes These Transactions and Events During MarchDocument56 pagesChurch Company Completes These Transactions and Events During Marchlaale dijaanNo ratings yet

- Question # 1: Calculation of EoqDocument3 pagesQuestion # 1: Calculation of EoqUnzila AtiqNo ratings yet

- Disposal of Subsidiary PDFDocument9 pagesDisposal of Subsidiary PDFStavri Makri SmirilliNo ratings yet

- Coca-Cola Residual Income Valuation - STUDENTSDocument7 pagesCoca-Cola Residual Income Valuation - STUDENTSdeepak mishraNo ratings yet

- Layout Plan For RCC Columns and FootingsDocument1 pageLayout Plan For RCC Columns and FootingsHusen GhoriNo ratings yet

- This Study Resource Was: Adjust CreditDocument4 pagesThis Study Resource Was: Adjust CreditJalaj GuptaNo ratings yet

- Question & Answer 28072015 InventoryDocument5 pagesQuestion & Answer 28072015 InventoryGreen StoneNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 2: Accrual Accounting and Income DeterminationDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 2: Accrual Accounting and Income DeterminationDylan AdrianNo ratings yet

- CH 03 - SolutionsDocument17 pagesCH 03 - SolutionsLuong Hoang Vu80% (5)

- When Accounting For The Deconsolidation of A Subsidiary 1Document1 pageWhen Accounting For The Deconsolidation of A Subsidiary 1Louiza Kyla AridaNo ratings yet

- Government Regulation 24/2012Document14 pagesGovernment Regulation 24/2012Adria SaputeroNo ratings yet

- 655 Week 9 Notes PDFDocument75 pages655 Week 9 Notes PDFsanaha786No ratings yet

- AC3103 Seminar 10 AnswersDocument3 pagesAC3103 Seminar 10 AnswersKrithika Naidu0% (1)

- Ch02 SolutionDocument6 pagesCh02 SolutionMalekNo ratings yet

- The Following Data Relate To The Operations of Slick SoftwareDocument2 pagesThe Following Data Relate To The Operations of Slick SoftwareAmit PandeyNo ratings yet

- Saad Karimi (Assignment 1)Document10 pagesSaad Karimi (Assignment 1)pakistan50% (2)

- E5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDocument6 pagesE5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDylan AdrianNo ratings yet

- Beechy7e Vol 1 SM Ch08Document59 pagesBeechy7e Vol 1 SM Ch08Aayush AgarwalNo ratings yet

- Mac006 A T2 2021 FexDocument7 pagesMac006 A T2 2021 FexHaris MalikNo ratings yet

- ACCT551 - Week 7 HomeworkDocument10 pagesACCT551 - Week 7 HomeworkDominickdadNo ratings yet

- Ross 12e PPT Ch06 CalculatorDocument71 pagesRoss 12e PPT Ch06 CalculatorKirthagan SelvamNo ratings yet

- Suggested Answers CAP III - Dec 2018 PDFDocument144 pagesSuggested Answers CAP III - Dec 2018 PDFsarojdawadiNo ratings yet

- t10 2010 Jun QDocument10 pagest10 2010 Jun QAjay TakiarNo ratings yet

- HI5020Document13 pagesHI5020takeshiru000No ratings yet

- Capstone Week 3 AssignmentDocument7 pagesCapstone Week 3 Assignmentleelee0302No ratings yet

- CUAC 408 Group Assignment 1 2021Document6 pagesCUAC 408 Group Assignment 1 2021Blessed Nyama100% (1)

- 1 Insurance ClaimDocument10 pages1 Insurance ClaimBAZINGA100% (1)

- Advanced Taxation Practice Question QuestionDocument8 pagesAdvanced Taxation Practice Question QuestionDanisa NdhlovuNo ratings yet

- Annual Report For Eng (18-19Document396 pagesAnnual Report For Eng (18-19shree salj dugda utpadakNo ratings yet

- Paper Ii, Question 1: Preparing For The 2003 UFE Understanding The Evaluation Methodology June 2002Document16 pagesPaper Ii, Question 1: Preparing For The 2003 UFE Understanding The Evaluation Methodology June 2002xsnoweyxNo ratings yet

- ACCO 420 Final F2020 Version 2Document4 pagesACCO 420 Final F2020 Version 2Wasif SethNo ratings yet

- Accounting For Investment in Variable Income Bearing Securities Lesson 27Document10 pagesAccounting For Investment in Variable Income Bearing Securities Lesson 27Sumantha SahaNo ratings yet

- Section VI: NRV Vs Fair Value: ExampleDocument5 pagesSection VI: NRV Vs Fair Value: ExamplebinuNo ratings yet

- Financial InstrumentsDocument14 pagesFinancial InstrumentsPriya NairNo ratings yet

- Barstow Company Is Contemplating The Acquisition of The Net AssetsDocument1 pageBarstow Company Is Contemplating The Acquisition of The Net AssetsMuhammad ShahidNo ratings yet

- CH 04 - SolutionsDocument17 pagesCH 04 - SolutionsLuong Hoang Vu100% (2)

- Chapter Eight: Cost-Volume-Profit AnalysisDocument34 pagesChapter Eight: Cost-Volume-Profit AnalysisBartholomew SzoldNo ratings yet

- AC2101 SemGrp4 Team6Document34 pagesAC2101 SemGrp4 Team6Kwang Yi JuinNo ratings yet

- CAB AcctDocument9 pagesCAB AcctA.J. ChuaNo ratings yet

- Cottrell Sunningdale SeptDec2023Document3 pagesCottrell Sunningdale SeptDec2023Adilah AzamNo ratings yet

- Bharti AXA Life Insurance Company LimitedDocument8 pagesBharti AXA Life Insurance Company LimitedJinal SanghviNo ratings yet

- Statement of Transaction - Sale or Gift of Motor Vehicle, Trailer, All-Terrain Vehicle (ATV), Vessel (Boat), or SnowmobileDocument2 pagesStatement of Transaction - Sale or Gift of Motor Vehicle, Trailer, All-Terrain Vehicle (ATV), Vessel (Boat), or SnowmobilePramedicaPerdanaPutra100% (1)

- Summarising Analysing DataDocument19 pagesSummarising Analysing DataSanjeev JayaratnaNo ratings yet

- PROBLEMS in ForexDocument2 pagesPROBLEMS in ForexPrethivi RajNo ratings yet

- Financial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizDocument4 pagesFinancial & Managerial Accounting For Mbas, 5Th Edition by Easton, Halsey, Mcanally, Hartgraves & Morse Practice QuizLevi AlvesNo ratings yet

- Ratios - Profitability, Market &Document46 pagesRatios - Profitability, Market &Jess AlexNo ratings yet

- Fire Insurance ClaimsDocument43 pagesFire Insurance ClaimsArshad Mohd100% (1)

- Manual 16 Jun 2021 - Part 1Document6 pagesManual 16 Jun 2021 - Part 1Feni AlvitaNo ratings yet

- Calculation - General Mills - PillsburyDocument10 pagesCalculation - General Mills - PillsburyAryan AnandNo ratings yet

- Portfolio Management PDFDocument27 pagesPortfolio Management PDFdwkr giriNo ratings yet

- Test 3 - Chap 24Document7 pagesTest 3 - Chap 24Bhushan Sawant100% (1)

- Week 4 TUTE Chapter 3 QuestionsDocument4 pagesWeek 4 TUTE Chapter 3 QuestionsTom ChanNo ratings yet

- Why Are Financial Statements Important?Document23 pagesWhy Are Financial Statements Important?Dylan AdrianNo ratings yet

- OTC Sponsorship Proposals 2020 - 2021Document4 pagesOTC Sponsorship Proposals 2020 - 2021Dylan AdrianNo ratings yet

- FINA3307 Lecture1Document22 pagesFINA3307 Lecture1Dylan AdrianNo ratings yet

- Non-Linear Forecasting in High Frequency Time SeriesDocument17 pagesNon-Linear Forecasting in High Frequency Time SeriesDylan AdrianNo ratings yet

- (JP Morgan) Relative Value Single Stock VolatilityDocument36 pages(JP Morgan) Relative Value Single Stock VolatilityDylan Adrian100% (1)

- Liquidity and Convergence Trading in IRS SpreadsDocument13 pagesLiquidity and Convergence Trading in IRS SpreadsDylan AdrianNo ratings yet

- Dynamic Model For Forward CurveDocument61 pagesDynamic Model For Forward CurveDylan AdrianNo ratings yet

- Week 2 TUTE Chapter 1 SolutionsDocument6 pagesWeek 2 TUTE Chapter 1 SolutionsDylan AdrianNo ratings yet

- w1 TuteDocument4 pagesw1 TuteDylan AdrianNo ratings yet

- RBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Document11 pagesRBCCapitalMarkets RBAminutesleavespacefortaperingU-turn Aug 17 2021Dylan AdrianNo ratings yet

- RBCCapitalMarkets RBCRatesStrategy-MuchfortheRBAtoponderafterRBNZholdfire Aug 18 2021Document1 pageRBCCapitalMarkets RBCRatesStrategy-MuchfortheRBAtoponderafterRBNZholdfire Aug 18 2021Dylan AdrianNo ratings yet

- Amplitude Trend CharacteristicsDocument17 pagesAmplitude Trend CharacteristicsDylan AdrianNo ratings yet

- Australian Rates Strategy: Back To The Belly - Looking To Receive 2-5-10s, 2y/2y AU vs. UKDocument5 pagesAustralian Rates Strategy: Back To The Belly - Looking To Receive 2-5-10s, 2y/2y AU vs. UKDylan AdrianNo ratings yet

- ZacksInvestmentResearchInc ZacksMarketStrategy Aug 09 2021Document75 pagesZacksInvestmentResearchInc ZacksMarketStrategy Aug 09 2021Dylan AdrianNo ratings yet

- E5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDocument6 pagesE5-4 Assessing Receivable and Inventory Turnover Aicpa AdaptedDylan AdrianNo ratings yet

- ACCT3302 Financial Statement Analysis Tutorial 4: Structure of The Balance Sheet and Statement of Cash FlowsDocument3 pagesACCT3302 Financial Statement Analysis Tutorial 4: Structure of The Balance Sheet and Statement of Cash FlowsDylan AdrianNo ratings yet

- Free Decision Tree Diagram TemplateDocument8 pagesFree Decision Tree Diagram TemplateBadrun TamanNo ratings yet

- Assignment 2: I. Complete All Problems and Applications at The End of Chapter 23Document6 pagesAssignment 2: I. Complete All Problems and Applications at The End of Chapter 23Phước Đào QuangNo ratings yet

- II Puc Economics Mind Maps For 2023 ExamDocument14 pagesII Puc Economics Mind Maps For 2023 Examm2699291No ratings yet

- Dr. Nick Marasigan AccountsDocument11 pagesDr. Nick Marasigan AccountsNicole SarmientoNo ratings yet

- Potentialities of Capitalistic Growth (IGNOU)Document5 pagesPotentialities of Capitalistic Growth (IGNOU)saqueeb111No ratings yet

- V890Document1 pageV890Arcadie ApostolNo ratings yet

- Spink Auction World Vanknotes 23231Document188 pagesSpink Auction World Vanknotes 23231Nikola KukrikaNo ratings yet

- Cost AccountingDocument16 pagesCost AccountingDennis LacsonNo ratings yet

- MR Notice To Shipping No. N-7-2005 To: Steamship Agents, Owners and Operators Subject: Panama Canal Transit Reservation SystemDocument17 pagesMR Notice To Shipping No. N-7-2005 To: Steamship Agents, Owners and Operators Subject: Panama Canal Transit Reservation Systemsaurav naskarNo ratings yet

- (A) Regress Log of Wages On A Constant and The Female Dummy. Paste Output HereDocument5 pages(A) Regress Log of Wages On A Constant and The Female Dummy. Paste Output Hereakshay patriNo ratings yet

- CHB Back-Up ComputationDocument36 pagesCHB Back-Up Computationkhim tugasNo ratings yet

- تأثير الأزمات المالية على عائد ومخاطر المحفظة المالية الدولية - - حالة مجموعة من بورصات الأسهم المتطورة والناشئة 2007-2012 -Document16 pagesتأثير الأزمات المالية على عائد ومخاطر المحفظة المالية الدولية - - حالة مجموعة من بورصات الأسهم المتطورة والناشئة 2007-2012 -MohamedNo ratings yet

- Econ Premium Fe-Test Certificate Iso 15848-1 Co1 - Co3 and Ta-Luft-RtDocument3 pagesEcon Premium Fe-Test Certificate Iso 15848-1 Co1 - Co3 and Ta-Luft-Rtemperor_vamsiNo ratings yet

- Flat Sale in EnglishDocument7 pagesFlat Sale in EnglishDeep HiraniNo ratings yet

- Most Expensive Currency - Google SearchDocument1 pageMost Expensive Currency - Google SearchAbdulla JamalNo ratings yet

- Ventura, Marymickaellar Chapter6 (2,3,4,20,21)Document2 pagesVentura, Marymickaellar Chapter6 (2,3,4,20,21)Mary VenturaNo ratings yet

- F26a.0 - F30cy.0 - F32a.0 - F40B.0Document16 pagesF26a.0 - F30cy.0 - F32a.0 - F40B.0Canguro AndadorNo ratings yet

- HX 75Document1 pageHX 75cs gunungparaNo ratings yet

- Solution Practice 1 Share CapitalDocument2 pagesSolution Practice 1 Share CapitalMya Hmuu KhinNo ratings yet

- Unit-6 Subsidiary Books PDFDocument52 pagesUnit-6 Subsidiary Books PDFShiva AggarwalNo ratings yet

- Dongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891Document10 pagesDongyang 1926 Parts Catalog Watermark 150625104921 Lva1 App 6891shirley100% (57)

- Sample Requistion For Jay Vijay LLP Godrej Site DATED 23 JAN 2024Document4 pagesSample Requistion For Jay Vijay LLP Godrej Site DATED 23 JAN 2024kiranmisale7No ratings yet

- Chapter 5 Summary NotesDocument1 pageChapter 5 Summary Notesali aknarNo ratings yet

- Regulation No 332 2014 Establishment and Determination of The Procedure of The Accounting and Auditing Board of EthiopiaDocument20 pagesRegulation No 332 2014 Establishment and Determination of The Procedure of The Accounting and Auditing Board of EthiopiajemalNo ratings yet

- Investasi Dan Pasar ModalDocument19 pagesInvestasi Dan Pasar ModalKrisna AdithaNo ratings yet

- 2023-2024 Fix B PTS KELAS 12Document8 pages2023-2024 Fix B PTS KELAS 12milatrikanti80No ratings yet

- Multiple Choice Questions (MCQ) Q.1 - Q.10 Carry ONE Mark EachDocument34 pagesMultiple Choice Questions (MCQ) Q.1 - Q.10 Carry ONE Mark EachKaran KumarNo ratings yet

- Week 8 Media and The AudienceDocument3 pagesWeek 8 Media and The AudienceADMATEZA UNGGUINo ratings yet

- Warehouses and Headquarters Addresses and Price List TemplateDocument22 pagesWarehouses and Headquarters Addresses and Price List TemplateTudor FlorinNo ratings yet