Download as pdf or txt

You might also like

- Buffets Bid For Media GeneralDocument23 pagesBuffets Bid For Media GeneralTerence TayNo ratings yet

- HOFACKER - Big Data and Consumer Behavior - Imminent OpportunitiesDocument12 pagesHOFACKER - Big Data and Consumer Behavior - Imminent OpportunitiesAngélica Azevedo100% (1)

- Selections in The Present EconomyDocument3 pagesSelections in The Present EconomyNeil100% (3)

- A Contribution To The Empirics of Economic GrowthDocument39 pagesA Contribution To The Empirics of Economic GrowthJamesNo ratings yet

- Cpi 122016Document3 pagesCpi 122016tripleeventNo ratings yet

- Monthly Coffee Market Report March 2015 Coffee Market Settles Lower But Demand Remains BuoyantDocument5 pagesMonthly Coffee Market Report March 2015 Coffee Market Settles Lower But Demand Remains BuoyantOvidioMartínezNo ratings yet

- Cpi 082017Document3 pagesCpi 082017tripleeventNo ratings yet

- Kenya National Bureau of StatisticsDocument3 pagesKenya National Bureau of Statisticsuet22No ratings yet

- Ucda Monthly Report January 2010Document6 pagesUcda Monthly Report January 2010api-26533189No ratings yet

- November 2021 - CPIDocument3 pagesNovember 2021 - CPIVikiCheruKoechNo ratings yet

- December 2021 - CPIDocument3 pagesDecember 2021 - CPIVikiCheruKoechNo ratings yet

- Cpi 082018Document3 pagesCpi 082018tripleeventNo ratings yet

- Comparative Export StatementApril Oct2021Document1 pageComparative Export StatementApril Oct2021Mudassir KhanNo ratings yet

- Consumer Price Index - Feb15-Jan16Document331 pagesConsumer Price Index - Feb15-Jan16dpmgumtiNo ratings yet

- CMO April 2021 ForecastsDocument4 pagesCMO April 2021 ForecastsbouttakNo ratings yet

- Xls321 Xls EngDocument16 pagesXls321 Xls EngERIC GREY SOLANO LEVANONo ratings yet

- ICO Composite Indicator Colombian Milds Other Milds Brazilian Naturals RobustasDocument1 pageICO Composite Indicator Colombian Milds Other Milds Brazilian Naturals RobustasGemechis BidoNo ratings yet

- December 2022 CPIDocument3 pagesDecember 2022 CPIAlloye UtaNo ratings yet

- Year Month Closing PriceDocument9 pagesYear Month Closing PriceOmer PashaNo ratings yet

- Cpi 122015Document3 pagesCpi 122015tripleeventNo ratings yet

- Bisauli PPT 24.01.2023Document19 pagesBisauli PPT 24.01.2023Dilip PayaNo ratings yet

- Kenya National Bureau of Statistics: Table 1: One Month and Twelve Months' Changes in The Price IndicesDocument3 pagesKenya National Bureau of Statistics: Table 1: One Month and Twelve Months' Changes in The Price IndicesLYDIAHNo ratings yet

- Quarterly Beverage Forecast Report Indonesia q4 20 CoffeeDocument41 pagesQuarterly Beverage Forecast Report Indonesia q4 20 CoffeeKeken SonyriscaNo ratings yet

- For Sugar (MMT) 69.0 122.3 174.8 176.7 For Khandsari (MMT) 10.5 13.2 10.0 11.0 For Gur (MMT) 71.6 76.6 67.3 72.5 For Seed (MMT) 20.6 28.9 30.1 35.5Document6 pagesFor Sugar (MMT) 69.0 122.3 174.8 176.7 For Khandsari (MMT) 10.5 13.2 10.0 11.0 For Gur (MMT) 71.6 76.6 67.3 72.5 For Seed (MMT) 20.6 28.9 30.1 35.5dangmilanNo ratings yet

- Kenya Consumer Price Indices and Inflation Rates April 2024Document3 pagesKenya Consumer Price Indices and Inflation Rates April 2024o.j.dumbo0No ratings yet

- Joes Running Tracker v1xDocument16 pagesJoes Running Tracker v1xulissesju7No ratings yet

- CMO April 2023 ForecastsDocument2 pagesCMO April 2023 ForecastsDEPRI AFRIAN LAMBUTONo ratings yet

- CMO October 2022 ForecastsDocument1 pageCMO October 2022 ForecastsAnthony FloresNo ratings yet

- Πληθωρισμός ΕΖDocument2 pagesΠληθωρισμός ΕΖLeonNo ratings yet

- Special Release. 2-2018 - Guimaras Inflation RateDocument4 pagesSpecial Release. 2-2018 - Guimaras Inflation RateMary Joy VillegasNo ratings yet

- CSO February 2009 CPI Press ReleaseDocument6 pagesCSO February 2009 CPI Press ReleaseChola Mukanga100% (1)

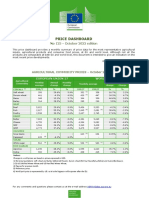

- Price Dashboard: No 116 - January 2022 EditionDocument9 pagesPrice Dashboard: No 116 - January 2022 EditionNebojsa RadulovicNo ratings yet

- Economic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Document3 pagesEconomic Highlights - Fuel and Sugar Prices Were Raised To Reduce - 16/7/2010Rhb InvestNo ratings yet

- DownloadDocument1 pageDownloadRhettNo ratings yet

- Naeb Monthly Report For January 2016: CoffeeDocument5 pagesNaeb Monthly Report For January 2016: CoffeenachoNo ratings yet

- World Bank Commodities Price Forecast (Nominal US Dollars)Document4 pagesWorld Bank Commodities Price Forecast (Nominal US Dollars)rad1962No ratings yet

- Managerial Economics - Trend Analysis of Petroleum ProductsDocument5 pagesManagerial Economics - Trend Analysis of Petroleum ProductsTaha SuhailNo ratings yet

- A2-Task 2-Budget Futura - Restaurant - BarDocument3 pagesA2-Task 2-Budget Futura - Restaurant - BarStanley ChandraNo ratings yet

- A2-Task 2-Budget Futura - Restaurant - BarDocument3 pagesA2-Task 2-Budget Futura - Restaurant - BarManoj GhimireNo ratings yet

- A2-Task 2-Budget Futura - Restaurant - BarDocument3 pagesA2-Task 2-Budget Futura - Restaurant - BarManoj GhimireNo ratings yet

- 11.2 US2.v4Document126 pages11.2 US2.v4Abraham Dawson machachaNo ratings yet

- Cmo October 2017 ForecastsDocument4 pagesCmo October 2017 Forecastsyan energiaNo ratings yet

- Cmo April 2019 ForecastsDocument4 pagesCmo April 2019 ForecastsYanuar KurniawanNo ratings yet

- Corn RoadmapDocument32 pagesCorn RoadmapSetup Dost Region IINo ratings yet

- PRIL - Investor Update - Q3 FY 2011Document6 pagesPRIL - Investor Update - Q3 FY 2011ankigoelNo ratings yet

- Grapes MRKG-KPI Report OctDocument16 pagesGrapes MRKG-KPI Report Oct_Siraj_Ahmad_6538No ratings yet

- 4.3 Inflation in BangladeshDocument5 pages4.3 Inflation in BangladeshArju LubnaNo ratings yet

- Consumer Price IndexDocument8 pagesConsumer Price IndexDeborah ChiramboNo ratings yet

- Commodity Price Dashboard 2022 11 enDocument9 pagesCommodity Price Dashboard 2022 11 enoscarNo ratings yet

- A Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaDocument17 pagesA Comparative Analysis of GDP Patterns in Bangladesh and Sri LankaBlah BlahNo ratings yet

- World Bank Commodities Price Forecast (Nominal US Dollars)Document4 pagesWorld Bank Commodities Price Forecast (Nominal US Dollars)marceloNo ratings yet

- WELLDocument8 pagesWELLChristian CabacunganNo ratings yet

- Australian Readership Results June 2018Document7 pagesAustralian Readership Results June 2018rodeimeNo ratings yet

- Adidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanDocument27 pagesAdidas/Reebok Merger: Collin Shaw Kelly Truesdale Michael Rockette Benedikte Schmidt SaravanansadaiyappanUdipta DasNo ratings yet

- NOVEMBER, 2020: National Urban RuralDocument3 pagesNOVEMBER, 2020: National Urban Ruralmadiha darNo ratings yet

- Sugar Annual Manila Philippines 4-12-2012Document11 pagesSugar Annual Manila Philippines 4-12-2012Shaira DaleNo ratings yet

- 2010 Unctad - Commodity Price Bulletin - SeptDocument9 pages2010 Unctad - Commodity Price Bulletin - SeptMarcosNo ratings yet

- Inflació 1Document2 pagesInflació 1Maria José RodríguezNo ratings yet

- Ucda Report May 2009Document8 pagesUcda Report May 2009api-26533189No ratings yet

- SK 121201Document29 pagesSK 121201BoomdayNo ratings yet

- Cpi Report October 2011Document8 pagesCpi Report October 2011binzNo ratings yet

- NOVEMBER, 2021: Press Release On Consumer Price Index (Cpi) Inflation For The Month of IndicatorsDocument3 pagesNOVEMBER, 2021: Press Release On Consumer Price Index (Cpi) Inflation For The Month of Indicatorsmadiha darNo ratings yet

- United States Census Figures Back to 1630From EverandUnited States Census Figures Back to 1630No ratings yet

- Sls Out LierDocument29 pagesSls Out LierAngélica AzevedoNo ratings yet

- 1993 - Eui WP - Eco - 016Document40 pages1993 - Eui WP - Eco - 016Angélica AzevedoNo ratings yet

- Globalisation and National Trends in Nutrition and Health - A Grouped Fixed-Effects Approach To Inter-Country HeterogeneityDocument51 pagesGlobalisation and National Trends in Nutrition and Health - A Grouped Fixed-Effects Approach To Inter-Country HeterogeneityAngélica AzevedoNo ratings yet

- Evidence Informed Decision Making: The Use of "Colloquial Evidence" at NICEDocument10 pagesEvidence Informed Decision Making: The Use of "Colloquial Evidence" at NICEAngélica AzevedoNo ratings yet

- The Evolution of Global Trading Patterns and Its Implications For The WTODocument30 pagesThe Evolution of Global Trading Patterns and Its Implications For The WTOAngélica AzevedoNo ratings yet

- Making A Space For Taste - Contextand Discourse in The Specialty Coffee SceneDocument8 pagesMaking A Space For Taste - Contextand Discourse in The Specialty Coffee SceneAngélica AzevedoNo ratings yet

- Coase 1988 - The Nature of Firm - InfluenceDocument16 pagesCoase 1988 - The Nature of Firm - InfluenceAngélica AzevedoNo ratings yet

- COASE 1984 - The New Institutional EconomicsDocument4 pagesCOASE 1984 - The New Institutional EconomicsAngélica AzevedoNo ratings yet

- Sustainable Design N Constn - 2nd Penang Bridge-PUODocument75 pagesSustainable Design N Constn - 2nd Penang Bridge-PUORakesh Kapoor100% (3)

- Department of Labor: Cepr102105Document2 pagesDepartment of Labor: Cepr102105USA_DepartmentOfLaborNo ratings yet

- 14 3 IndepthDocument7 pages14 3 Indepthapi-263088756No ratings yet

- Acct Statement - XX9665 - 17082022Document53 pagesAcct Statement - XX9665 - 17082022nosNo ratings yet

- Final ProjectDocument72 pagesFinal ProjectParvinder BaathNo ratings yet

- The European Union Summary On A MapDocument4 pagesThe European Union Summary On A MapAkin IyiNo ratings yet

- NewMont Mining Corp - MainDocument6 pagesNewMont Mining Corp - MainFrenzy FrenesisNo ratings yet

- Adobe Scan Aug 03, 2022Document1 pageAdobe Scan Aug 03, 2022Kumar adi officialNo ratings yet

- Managerial Economics in A Global Economy: Cost Theory and EstimationDocument23 pagesManagerial Economics in A Global Economy: Cost Theory and EstimationArif DarmawanNo ratings yet

- Internship FinalDocument20 pagesInternship FinalKrish JaiswalNo ratings yet

- LabelsDocument52 pagesLabels29vishutiktokNo ratings yet

- Job SatisfactionDocument120 pagesJob SatisfactionPooja ShelarNo ratings yet

- 0 Joint Action Plan Construction Proposals For The Year 2013Document13 pages0 Joint Action Plan Construction Proposals For The Year 2013Madhu KurmiNo ratings yet

- MA Public EconomicsDocument300 pagesMA Public EconomicsashishNo ratings yet

- Multibagger - Sarda Energy & MineralsDocument2 pagesMultibagger - Sarda Energy & MineralsjitenfuriaNo ratings yet

- Impact of Exchange Rate On Balance of PaymentDocument24 pagesImpact of Exchange Rate On Balance of PaymentSyazwani KhalidNo ratings yet

- InterAction Member Activity Report WEST BANK/ GAZADocument44 pagesInterAction Member Activity Report WEST BANK/ GAZAInterActionNo ratings yet

- JVA JuryDocument22 pagesJVA JuryYogesh SharmaNo ratings yet

- Group 3 (International Financial Management)Document12 pagesGroup 3 (International Financial Management)Rakibul Hasan RockyNo ratings yet

- Salvatore Ch03Document30 pagesSalvatore Ch03tadesse-w100% (1)

- Canada Oil CompaniesDocument24 pagesCanada Oil Companiesa81m97m13No ratings yet

- Production Planning and ControlDocument22 pagesProduction Planning and ControlPravah Shukla100% (1)

- SsachartDocument1 pageSsachartFreeman Lawyer100% (1)

- US Internal Revenue Service: f2210 - 1994Document3 pagesUS Internal Revenue Service: f2210 - 1994IRSNo ratings yet

- Training For Work Scholarship Program (TWSP) Techvoc Skills Inc. Carlo E. Grebialde 82 Hours Tile Setting NC Ii 181813061200581Document2 pagesTraining For Work Scholarship Program (TWSP) Techvoc Skills Inc. Carlo E. Grebialde 82 Hours Tile Setting NC Ii 181813061200581ChristianNo ratings yet

- Econ 11 Problem Set 4Document5 pagesEcon 11 Problem Set 4DadedidoduNo ratings yet

- Brazilian StagflationDocument1 pageBrazilian StagflationNadella HemanthNo ratings yet

- (Media Statement Office of The Executive Mayor) Mayoral Committe Announcement Media Briefing - Cilliers BrinkDocument3 pages(Media Statement Office of The Executive Mayor) Mayoral Committe Announcement Media Briefing - Cilliers BrinkMmangaliso KhumaloNo ratings yet