Master Document For Family

Master Document For Family

You might also like

- Direct DepositDocument1 pageDirect DepositHakar Qadir GardiNo ratings yet

- MDI Emissions Reporting Guidelines For The Polyurethane IndustryDocument135 pagesMDI Emissions Reporting Guidelines For The Polyurethane Industrydynaflo100% (1)

- Salaam InsuranceDocument23 pagesSalaam InsuranceNur Alia100% (1)

- Dos BankDocument4 pagesDos BankheadpncNo ratings yet

- Ranco Costa Verda ContractDocument21 pagesRanco Costa Verda ContractGregory RussellNo ratings yet

- FoxIT Whitepaper Blackhat WebDocument24 pagesFoxIT Whitepaper Blackhat WebAnonymous Hnv6u54HNo ratings yet

- Boulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Document81 pagesBoulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Sita Anuragamayi Claire100% (1)

- Lee vs. TambagoDocument3 pagesLee vs. TambagoAnj100% (3)

- Federal Bank - Retail Banking - AccountsDocument77 pagesFederal Bank - Retail Banking - AccountsAditya SinghNo ratings yet

- Epayment Form - NewDocument3 pagesEpayment Form - NewVirender SainiNo ratings yet

- 10-02-26 BANK OF AMERICA CORP - DE - (Form - 10-K, Received - 02 - 26 - 2010 07 - 51 - 53 SDocument765 pages10-02-26 BANK OF AMERICA CORP - DE - (Form - 10-K, Received - 02 - 26 - 2010 07 - 51 - 53 SHuman Rights Alert - NGO (RA)No ratings yet

- Gmail - Direct Deposit To PEDRO - $3,500 by 03 - 30Document2 pagesGmail - Direct Deposit To PEDRO - $3,500 by 03 - 30Pedro MartinezNo ratings yet

- Wa0013.Document7 pagesWa0013.viphainhumNo ratings yet

- b2c Authorization Form TemplateDocument2 pagesb2c Authorization Form TemplateshahinaNo ratings yet

- Mailer Jun2014Document3 pagesMailer Jun2014sjplepNo ratings yet

- Nevada Reports 1906-1907 (29 Nev.) PDFDocument420 pagesNevada Reports 1906-1907 (29 Nev.) PDFthadzigsNo ratings yet

- Wells Fargo Advisors Premium Rewards Visa Signature CardDocument13 pagesWells Fargo Advisors Premium Rewards Visa Signature CardRalph YoungNo ratings yet

- Colorado House Bill 13-1114Document20 pagesColorado House Bill 13-1114Medicinal ColoradoNo ratings yet

- Apartemt Lease Agreement ExampleDocument3 pagesApartemt Lease Agreement ExampleLINH PHAMNo ratings yet

- Amerita Vision PlanDocument41 pagesAmerita Vision Planbutt7474No ratings yet

- Direct Deposit Authorization Form Raina MadridDocument1 pageDirect Deposit Authorization Form Raina MadridMatt ManuelNo ratings yet

- Application Certificate DeathDocument2 pagesApplication Certificate DeathAkshayNo ratings yet

- Client Application and AgreementDocument1 pageClient Application and Agreementcrdt4rl100% (1)

- Social Security Numbers For Noncitizens: Does A Noncitizen Need A Social Security Number?Document2 pagesSocial Security Numbers For Noncitizens: Does A Noncitizen Need A Social Security Number?antonioNo ratings yet

- TNC 280Document20 pagesTNC 280naveen.bitsgoa8303No ratings yet

- TRENT COLBY GEERDES ReportDocument36 pagesTRENT COLBY GEERDES ReportYyNo ratings yet

- 00.3.3 - D's 2-619a9 - 79Document121 pages00.3.3 - D's 2-619a9 - 79Christopher LangoneNo ratings yet

- Credit Card Authorization Form: Thomas A. KeelerDocument1 pageCredit Card Authorization Form: Thomas A. KeelerThomas KeelerNo ratings yet

- Merchant Cash Factoring Business Cash LoansDocument2 pagesMerchant Cash Factoring Business Cash LoansMerchantCashinAdvanceNo ratings yet

- Methods of Payment - AIU PDFDocument2 pagesMethods of Payment - AIU PDFMasiko MosesNo ratings yet

- Annexure A Application For MSME Loan Upto Rs.100 LakhDocument6 pagesAnnexure A Application For MSME Loan Upto Rs.100 LakhChayan MajumdarNo ratings yet

- Amex Case Group5Document22 pagesAmex Case Group5skaifNo ratings yet

- Driver License/identification Card and REAL ID ChecklistDocument3 pagesDriver License/identification Card and REAL ID ChecklistMuneeb QayyumNo ratings yet

- Business Loan - Application Form & Document ListDocument5 pagesBusiness Loan - Application Form & Document ListsamaadhuNo ratings yet

- (Company Name) : Direct Deposit Agreement FormDocument1 page(Company Name) : Direct Deposit Agreement FormMalikBeyNo ratings yet

- EMV Issuer Security Guidelines: Emvco, LLCDocument33 pagesEMV Issuer Security Guidelines: Emvco, LLCchinmay451No ratings yet

- Request Form (Request For Modification and Affidavit)Document3 pagesRequest Form (Request For Modification and Affidavit)eagles39100% (1)

- Keywordio Longtail KeywordsDocument8 pagesKeywordio Longtail KeywordsAkshat GroverNo ratings yet

- PenFed Signature PageDocument3 pagesPenFed Signature PageL KNo ratings yet

- Heritage Bank Bank Account Opening FormDocument18 pagesHeritage Bank Bank Account Opening FormJose M AlayetoNo ratings yet

- Schmieding Setup Packet For CarriersDocument28 pagesSchmieding Setup Packet For CarriersFabianNo ratings yet

- Queens 11092021 PDFDocument267 pagesQueens 11092021 PDFOp MassNo ratings yet

- Including The Long Form Fee Disclosure ("List of All Fees.")Document9 pagesIncluding The Long Form Fee Disclosure ("List of All Fees.")Shamara LoganNo ratings yet

- Priority Pass FormDocument2 pagesPriority Pass Formatrish07No ratings yet

- Conventional Bridge Loan FinancingDocument1 pageConventional Bridge Loan FinancingcambridgecapNo ratings yet

- Firstdirect Credit Card Consumer Credit Agreement Signed 180120081401 PDFDocument14 pagesFirstdirect Credit Card Consumer Credit Agreement Signed 180120081401 PDFryanNo ratings yet

- Service Payout Request: Policy FormDocument4 pagesService Payout Request: Policy FormAkshayNo ratings yet

- DR-SM Lipa (Renewal)Document2 pagesDR-SM Lipa (Renewal)Cha DelicaNo ratings yet

- Federal Reserve Consumer Credit-G.19Document3 pagesFederal Reserve Consumer Credit-G.19Jackson SinnenbergNo ratings yet

- W8Document6 pagesW8Muhammad Husnain Ijaz0% (1)

- ID RFID Reader Writer InstructionsDocument2 pagesID RFID Reader Writer InstructionsHamizan Mohd NoorNo ratings yet

- Ebay ReportDocument159 pagesEbay ReportDhananjay Parshuram SawantNo ratings yet

- Social Security Form OnlineDocument5 pagesSocial Security Form OnlineDiego PinedoNo ratings yet

- Security Bank Credit Card Application Form419889820191115Document2 pagesSecurity Bank Credit Card Application Form419889820191115Frances Julianna DangananNo ratings yet

- MCSBG@co - Monterey.ca - Us: County of Monterey Workforce Development Board EmailDocument2 pagesMCSBG@co - Monterey.ca - Us: County of Monterey Workforce Development Board EmailIliana RamosNo ratings yet

- Bottles by Sickles BankruptcyDocument47 pagesBottles by Sickles BankruptcyDennis CarmodyNo ratings yet

- Nacha FormatDocument14 pagesNacha FormatPradeep Kumar ShuklaNo ratings yet

- EFT Request FormDocument2 pagesEFT Request Formekuhni2012No ratings yet

- Master Document For FamilyDocument58 pagesMaster Document For FamilydigiowlmedialabNo ratings yet

- A Presentation On Family Decision MakingDocument23 pagesA Presentation On Family Decision MakingDhruva Jyoti SharmaNo ratings yet

- UIB Care - User ManualDocument10 pagesUIB Care - User ManualParag DekhaneNo ratings yet

- User Manual Doc 1711711657Document11 pagesUser Manual Doc 1711711657kaushik21185No ratings yet

- Diego Gallo Macin Janet Santagada Eac 150 NBQ 09. Mar. 2018 Research Skills AssignmentDocument5 pagesDiego Gallo Macin Janet Santagada Eac 150 NBQ 09. Mar. 2018 Research Skills AssignmentDiego Gallo MacínNo ratings yet

- De002 Fami002 1 Family Insurance Form AnpassungDocument2 pagesDe002 Fami002 1 Family Insurance Form Anpassungnaumkina2000No ratings yet

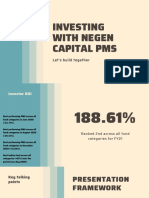

- Investing With Negen Capital PMS: Let's Build TogetherDocument12 pagesInvesting With Negen Capital PMS: Let's Build TogetherSumit SagarNo ratings yet

- NCERT - Principle Basic of Geography XI (Old Edition)Document231 pagesNCERT - Principle Basic of Geography XI (Old Edition)Sumit SagarNo ratings yet

- Course Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallDocument3 pagesCourse Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallSumit SagarNo ratings yet

- Negen Capital: (Portfolio Management Service)Document5 pagesNegen Capital: (Portfolio Management Service)Sumit SagarNo ratings yet

- Earthquakes and LandslidesDocument19 pagesEarthquakes and LandslidesSumit SagarNo ratings yet

- Rock Mass Rating System (After Bieniawski 1989)Document6 pagesRock Mass Rating System (After Bieniawski 1989)Sumit SagarNo ratings yet

- Folding Faulting - NegiDocument31 pagesFolding Faulting - NegiSumit SagarNo ratings yet

- Greystone Capital Pitchbook 7.14.2020Document47 pagesGreystone Capital Pitchbook 7.14.2020Sumit SagarNo ratings yet

- Underground: WaterDocument12 pagesUnderground: WaterSumit Sagar0% (1)

- Critically EndengeredDocument9 pagesCritically EndengeredSumit SagarNo ratings yet

- East Coast 2015 Letter Twin LightsDocument15 pagesEast Coast 2015 Letter Twin LightsSumit SagarNo ratings yet

- Cheetah: SR N O Name Picture Distributi ONDocument5 pagesCheetah: SR N O Name Picture Distributi ONSumit SagarNo ratings yet

- Architecture MCQ (Rohit Kumar Verma 170544)Document8 pagesArchitecture MCQ (Rohit Kumar Verma 170544)Sumit SagarNo ratings yet

- Parag Parikh Pole Star of Value InvestinDocument3 pagesParag Parikh Pole Star of Value InvestinSumit SagarNo ratings yet

- Architecture MCQsDocument8 pagesArchitecture MCQsSumit SagarNo ratings yet

- Architecture MCQS: Dynapoloiscentric MonopolyDocument9 pagesArchitecture MCQS: Dynapoloiscentric MonopolySumit SagarNo ratings yet

- Greystone Capital Introductory LetterDocument3 pagesGreystone Capital Introductory LetterSumit SagarNo ratings yet

- Greystone Capital Founders LetterDocument14 pagesGreystone Capital Founders LetterSumit SagarNo ratings yet

- Ethno ArchaeologyDocument3 pagesEthno ArchaeologySumit SagarNo ratings yet

- Schedule For Vacating The Neel Kanth HostelDocument5 pagesSchedule For Vacating The Neel Kanth HostelSumit SagarNo ratings yet

- Day 6 AssignmentDocument2 pagesDay 6 AssignmentSumit SagarNo ratings yet

- Meaning in Grammatology and SemiologyDocument6 pagesMeaning in Grammatology and SemiologyRandolph DibleNo ratings yet

- White PaperDocument17 pagesWhite Papernanadmyro Photo6No ratings yet

- For Any Reference Visit: Https://sarathi - Parivahan.gov - In/sarathiserviceDocument1 pageFor Any Reference Visit: Https://sarathi - Parivahan.gov - In/sarathiserviceKavan AminNo ratings yet

- NOA Sociology 01Document39 pagesNOA Sociology 01Nazrat AnemNo ratings yet

- Geography Chapter - (Agriculture) Class 8Document5 pagesGeography Chapter - (Agriculture) Class 8Khushi Kumari class 9 adm 664No ratings yet

- College Schedule: Thursday Friday Saturday Sunday MondayDocument5 pagesCollege Schedule: Thursday Friday Saturday Sunday MondayGomv ConsNo ratings yet

- Turn in For LTC MANDAL NCDocument2 pagesTurn in For LTC MANDAL NCMary Anne GamboaNo ratings yet

- Chapter 1Document25 pagesChapter 1Naman PalindromeNo ratings yet

- Distributed PowerDocument3 pagesDistributed PowertibvalNo ratings yet

- The Principle of Human Dignity Rel Ed 6Document22 pagesThe Principle of Human Dignity Rel Ed 6MJ LazaroNo ratings yet

- BSF Lesson 27Document2 pagesBSF Lesson 27nathaniel07No ratings yet

- EL112 SURVEY OF AFRO ReviewerDocument5 pagesEL112 SURVEY OF AFRO ReviewerUkulele PrincessNo ratings yet

- Lzu 1431171 M 7Document24 pagesLzu 1431171 M 7ravitheleoNo ratings yet

- Textile Technology SylaDocument104 pagesTextile Technology SylaMaruti ArkachariNo ratings yet

- Aqyila - Bloom LyricsDocument2 pagesAqyila - Bloom Lyrics9gdbkfmv9yNo ratings yet

- Teacher Toolbox Assignment Example From ShaneDocument2 pagesTeacher Toolbox Assignment Example From Shaned0% (1)

- Internship Report On Performance Appraisal System of Janata Bank LimitedDocument47 pagesInternship Report On Performance Appraisal System of Janata Bank LimitedFahimNo ratings yet

- Exam NotesDocument104 pagesExam NotesJezMillerNo ratings yet

- Dwi Herinanto-Semnas DJ 2021 Old 2Document9 pagesDwi Herinanto-Semnas DJ 2021 Old 2Bernadhita HerindriNo ratings yet

- Set B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDDocument12 pagesSet B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDdini sofiaNo ratings yet

- Saurer Insight 01 2019 ENDocument60 pagesSaurer Insight 01 2019 ENSIVAKUMAR KNo ratings yet

- Intercultural Communication Globalization and Social Justice 2nd Edition Sorrells Test Bank 1Document25 pagesIntercultural Communication Globalization and Social Justice 2nd Edition Sorrells Test Bank 1erinbartlettcbrsgawejx100% (34)

- Transfer Pricing Country Profile BulgariaDocument16 pagesTransfer Pricing Country Profile BulgariaIoanna ZlatevaNo ratings yet

- Latest RFQ (Hospet Bellary Karntaka Dated - 29102010Document69 pagesLatest RFQ (Hospet Bellary Karntaka Dated - 29102010xanblakeNo ratings yet

- FINA 410 - Exercises (NOV)Document7 pagesFINA 410 - Exercises (NOV)said100% (1)

Download as pdf or txt

You might also like

- Direct DepositDocument1 pageDirect DepositHakar Qadir GardiNo ratings yet

- MDI Emissions Reporting Guidelines For The Polyurethane IndustryDocument135 pagesMDI Emissions Reporting Guidelines For The Polyurethane Industrydynaflo100% (1)

- Salaam InsuranceDocument23 pagesSalaam InsuranceNur Alia100% (1)

- Dos BankDocument4 pagesDos BankheadpncNo ratings yet

- Ranco Costa Verda ContractDocument21 pagesRanco Costa Verda ContractGregory RussellNo ratings yet

- FoxIT Whitepaper Blackhat WebDocument24 pagesFoxIT Whitepaper Blackhat WebAnonymous Hnv6u54HNo ratings yet

- Boulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Document81 pagesBoulder Kirtan - Bhakti Shakti Kirtan Chantbook - 2008-01-18Sita Anuragamayi Claire100% (1)

- Lee vs. TambagoDocument3 pagesLee vs. TambagoAnj100% (3)

- Federal Bank - Retail Banking - AccountsDocument77 pagesFederal Bank - Retail Banking - AccountsAditya SinghNo ratings yet

- Epayment Form - NewDocument3 pagesEpayment Form - NewVirender SainiNo ratings yet

- 10-02-26 BANK OF AMERICA CORP - DE - (Form - 10-K, Received - 02 - 26 - 2010 07 - 51 - 53 SDocument765 pages10-02-26 BANK OF AMERICA CORP - DE - (Form - 10-K, Received - 02 - 26 - 2010 07 - 51 - 53 SHuman Rights Alert - NGO (RA)No ratings yet

- Gmail - Direct Deposit To PEDRO - $3,500 by 03 - 30Document2 pagesGmail - Direct Deposit To PEDRO - $3,500 by 03 - 30Pedro MartinezNo ratings yet

- Wa0013.Document7 pagesWa0013.viphainhumNo ratings yet

- b2c Authorization Form TemplateDocument2 pagesb2c Authorization Form TemplateshahinaNo ratings yet

- Mailer Jun2014Document3 pagesMailer Jun2014sjplepNo ratings yet

- Nevada Reports 1906-1907 (29 Nev.) PDFDocument420 pagesNevada Reports 1906-1907 (29 Nev.) PDFthadzigsNo ratings yet

- Wells Fargo Advisors Premium Rewards Visa Signature CardDocument13 pagesWells Fargo Advisors Premium Rewards Visa Signature CardRalph YoungNo ratings yet

- Colorado House Bill 13-1114Document20 pagesColorado House Bill 13-1114Medicinal ColoradoNo ratings yet

- Apartemt Lease Agreement ExampleDocument3 pagesApartemt Lease Agreement ExampleLINH PHAMNo ratings yet

- Amerita Vision PlanDocument41 pagesAmerita Vision Planbutt7474No ratings yet

- Direct Deposit Authorization Form Raina MadridDocument1 pageDirect Deposit Authorization Form Raina MadridMatt ManuelNo ratings yet

- Application Certificate DeathDocument2 pagesApplication Certificate DeathAkshayNo ratings yet

- Client Application and AgreementDocument1 pageClient Application and Agreementcrdt4rl100% (1)

- Social Security Numbers For Noncitizens: Does A Noncitizen Need A Social Security Number?Document2 pagesSocial Security Numbers For Noncitizens: Does A Noncitizen Need A Social Security Number?antonioNo ratings yet

- TNC 280Document20 pagesTNC 280naveen.bitsgoa8303No ratings yet

- TRENT COLBY GEERDES ReportDocument36 pagesTRENT COLBY GEERDES ReportYyNo ratings yet

- 00.3.3 - D's 2-619a9 - 79Document121 pages00.3.3 - D's 2-619a9 - 79Christopher LangoneNo ratings yet

- Credit Card Authorization Form: Thomas A. KeelerDocument1 pageCredit Card Authorization Form: Thomas A. KeelerThomas KeelerNo ratings yet

- Merchant Cash Factoring Business Cash LoansDocument2 pagesMerchant Cash Factoring Business Cash LoansMerchantCashinAdvanceNo ratings yet

- Methods of Payment - AIU PDFDocument2 pagesMethods of Payment - AIU PDFMasiko MosesNo ratings yet

- Annexure A Application For MSME Loan Upto Rs.100 LakhDocument6 pagesAnnexure A Application For MSME Loan Upto Rs.100 LakhChayan MajumdarNo ratings yet

- Amex Case Group5Document22 pagesAmex Case Group5skaifNo ratings yet

- Driver License/identification Card and REAL ID ChecklistDocument3 pagesDriver License/identification Card and REAL ID ChecklistMuneeb QayyumNo ratings yet

- Business Loan - Application Form & Document ListDocument5 pagesBusiness Loan - Application Form & Document ListsamaadhuNo ratings yet

- (Company Name) : Direct Deposit Agreement FormDocument1 page(Company Name) : Direct Deposit Agreement FormMalikBeyNo ratings yet

- EMV Issuer Security Guidelines: Emvco, LLCDocument33 pagesEMV Issuer Security Guidelines: Emvco, LLCchinmay451No ratings yet

- Request Form (Request For Modification and Affidavit)Document3 pagesRequest Form (Request For Modification and Affidavit)eagles39100% (1)

- Keywordio Longtail KeywordsDocument8 pagesKeywordio Longtail KeywordsAkshat GroverNo ratings yet

- PenFed Signature PageDocument3 pagesPenFed Signature PageL KNo ratings yet

- Heritage Bank Bank Account Opening FormDocument18 pagesHeritage Bank Bank Account Opening FormJose M AlayetoNo ratings yet

- Schmieding Setup Packet For CarriersDocument28 pagesSchmieding Setup Packet For CarriersFabianNo ratings yet

- Queens 11092021 PDFDocument267 pagesQueens 11092021 PDFOp MassNo ratings yet

- Including The Long Form Fee Disclosure ("List of All Fees.")Document9 pagesIncluding The Long Form Fee Disclosure ("List of All Fees.")Shamara LoganNo ratings yet

- Priority Pass FormDocument2 pagesPriority Pass Formatrish07No ratings yet

- Conventional Bridge Loan FinancingDocument1 pageConventional Bridge Loan FinancingcambridgecapNo ratings yet

- Firstdirect Credit Card Consumer Credit Agreement Signed 180120081401 PDFDocument14 pagesFirstdirect Credit Card Consumer Credit Agreement Signed 180120081401 PDFryanNo ratings yet

- Service Payout Request: Policy FormDocument4 pagesService Payout Request: Policy FormAkshayNo ratings yet

- DR-SM Lipa (Renewal)Document2 pagesDR-SM Lipa (Renewal)Cha DelicaNo ratings yet

- Federal Reserve Consumer Credit-G.19Document3 pagesFederal Reserve Consumer Credit-G.19Jackson SinnenbergNo ratings yet

- W8Document6 pagesW8Muhammad Husnain Ijaz0% (1)

- ID RFID Reader Writer InstructionsDocument2 pagesID RFID Reader Writer InstructionsHamizan Mohd NoorNo ratings yet

- Ebay ReportDocument159 pagesEbay ReportDhananjay Parshuram SawantNo ratings yet

- Social Security Form OnlineDocument5 pagesSocial Security Form OnlineDiego PinedoNo ratings yet

- Security Bank Credit Card Application Form419889820191115Document2 pagesSecurity Bank Credit Card Application Form419889820191115Frances Julianna DangananNo ratings yet

- MCSBG@co - Monterey.ca - Us: County of Monterey Workforce Development Board EmailDocument2 pagesMCSBG@co - Monterey.ca - Us: County of Monterey Workforce Development Board EmailIliana RamosNo ratings yet

- Bottles by Sickles BankruptcyDocument47 pagesBottles by Sickles BankruptcyDennis CarmodyNo ratings yet

- Nacha FormatDocument14 pagesNacha FormatPradeep Kumar ShuklaNo ratings yet

- EFT Request FormDocument2 pagesEFT Request Formekuhni2012No ratings yet

- Master Document For FamilyDocument58 pagesMaster Document For FamilydigiowlmedialabNo ratings yet

- A Presentation On Family Decision MakingDocument23 pagesA Presentation On Family Decision MakingDhruva Jyoti SharmaNo ratings yet

- UIB Care - User ManualDocument10 pagesUIB Care - User ManualParag DekhaneNo ratings yet

- User Manual Doc 1711711657Document11 pagesUser Manual Doc 1711711657kaushik21185No ratings yet

- Diego Gallo Macin Janet Santagada Eac 150 NBQ 09. Mar. 2018 Research Skills AssignmentDocument5 pagesDiego Gallo Macin Janet Santagada Eac 150 NBQ 09. Mar. 2018 Research Skills AssignmentDiego Gallo MacínNo ratings yet

- De002 Fami002 1 Family Insurance Form AnpassungDocument2 pagesDe002 Fami002 1 Family Insurance Form Anpassungnaumkina2000No ratings yet

- Investing With Negen Capital PMS: Let's Build TogetherDocument12 pagesInvesting With Negen Capital PMS: Let's Build TogetherSumit SagarNo ratings yet

- NCERT - Principle Basic of Geography XI (Old Edition)Document231 pagesNCERT - Principle Basic of Geography XI (Old Edition)Sumit SagarNo ratings yet

- Course Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallDocument3 pagesCourse Title: Value Investing: An Introduction Course Code: BUS 123 W Instructor Name: Kenneth Jeffrey MarshallSumit SagarNo ratings yet

- Negen Capital: (Portfolio Management Service)Document5 pagesNegen Capital: (Portfolio Management Service)Sumit SagarNo ratings yet

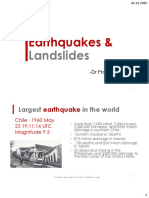

- Earthquakes and LandslidesDocument19 pagesEarthquakes and LandslidesSumit SagarNo ratings yet

- Rock Mass Rating System (After Bieniawski 1989)Document6 pagesRock Mass Rating System (After Bieniawski 1989)Sumit SagarNo ratings yet

- Folding Faulting - NegiDocument31 pagesFolding Faulting - NegiSumit SagarNo ratings yet

- Greystone Capital Pitchbook 7.14.2020Document47 pagesGreystone Capital Pitchbook 7.14.2020Sumit SagarNo ratings yet

- Underground: WaterDocument12 pagesUnderground: WaterSumit Sagar0% (1)

- Critically EndengeredDocument9 pagesCritically EndengeredSumit SagarNo ratings yet

- East Coast 2015 Letter Twin LightsDocument15 pagesEast Coast 2015 Letter Twin LightsSumit SagarNo ratings yet

- Cheetah: SR N O Name Picture Distributi ONDocument5 pagesCheetah: SR N O Name Picture Distributi ONSumit SagarNo ratings yet

- Architecture MCQ (Rohit Kumar Verma 170544)Document8 pagesArchitecture MCQ (Rohit Kumar Verma 170544)Sumit SagarNo ratings yet

- Parag Parikh Pole Star of Value InvestinDocument3 pagesParag Parikh Pole Star of Value InvestinSumit SagarNo ratings yet

- Architecture MCQsDocument8 pagesArchitecture MCQsSumit SagarNo ratings yet

- Architecture MCQS: Dynapoloiscentric MonopolyDocument9 pagesArchitecture MCQS: Dynapoloiscentric MonopolySumit SagarNo ratings yet

- Greystone Capital Introductory LetterDocument3 pagesGreystone Capital Introductory LetterSumit SagarNo ratings yet

- Greystone Capital Founders LetterDocument14 pagesGreystone Capital Founders LetterSumit SagarNo ratings yet

- Ethno ArchaeologyDocument3 pagesEthno ArchaeologySumit SagarNo ratings yet

- Schedule For Vacating The Neel Kanth HostelDocument5 pagesSchedule For Vacating The Neel Kanth HostelSumit SagarNo ratings yet

- Day 6 AssignmentDocument2 pagesDay 6 AssignmentSumit SagarNo ratings yet

- Meaning in Grammatology and SemiologyDocument6 pagesMeaning in Grammatology and SemiologyRandolph DibleNo ratings yet

- White PaperDocument17 pagesWhite Papernanadmyro Photo6No ratings yet

- For Any Reference Visit: Https://sarathi - Parivahan.gov - In/sarathiserviceDocument1 pageFor Any Reference Visit: Https://sarathi - Parivahan.gov - In/sarathiserviceKavan AminNo ratings yet

- NOA Sociology 01Document39 pagesNOA Sociology 01Nazrat AnemNo ratings yet

- Geography Chapter - (Agriculture) Class 8Document5 pagesGeography Chapter - (Agriculture) Class 8Khushi Kumari class 9 adm 664No ratings yet

- College Schedule: Thursday Friday Saturday Sunday MondayDocument5 pagesCollege Schedule: Thursday Friday Saturday Sunday MondayGomv ConsNo ratings yet

- Turn in For LTC MANDAL NCDocument2 pagesTurn in For LTC MANDAL NCMary Anne GamboaNo ratings yet

- Chapter 1Document25 pagesChapter 1Naman PalindromeNo ratings yet

- Distributed PowerDocument3 pagesDistributed PowertibvalNo ratings yet

- The Principle of Human Dignity Rel Ed 6Document22 pagesThe Principle of Human Dignity Rel Ed 6MJ LazaroNo ratings yet

- BSF Lesson 27Document2 pagesBSF Lesson 27nathaniel07No ratings yet

- EL112 SURVEY OF AFRO ReviewerDocument5 pagesEL112 SURVEY OF AFRO ReviewerUkulele PrincessNo ratings yet

- Lzu 1431171 M 7Document24 pagesLzu 1431171 M 7ravitheleoNo ratings yet

- Textile Technology SylaDocument104 pagesTextile Technology SylaMaruti ArkachariNo ratings yet

- Aqyila - Bloom LyricsDocument2 pagesAqyila - Bloom Lyrics9gdbkfmv9yNo ratings yet

- Teacher Toolbox Assignment Example From ShaneDocument2 pagesTeacher Toolbox Assignment Example From Shaned0% (1)

- Internship Report On Performance Appraisal System of Janata Bank LimitedDocument47 pagesInternship Report On Performance Appraisal System of Janata Bank LimitedFahimNo ratings yet

- Exam NotesDocument104 pagesExam NotesJezMillerNo ratings yet

- Dwi Herinanto-Semnas DJ 2021 Old 2Document9 pagesDwi Herinanto-Semnas DJ 2021 Old 2Bernadhita HerindriNo ratings yet

- Set B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDDocument12 pagesSet B: Part 1 A) Using Suitable Software, Prepare The Following Documentations For of SESB SDN BHDdini sofiaNo ratings yet

- Saurer Insight 01 2019 ENDocument60 pagesSaurer Insight 01 2019 ENSIVAKUMAR KNo ratings yet

- Intercultural Communication Globalization and Social Justice 2nd Edition Sorrells Test Bank 1Document25 pagesIntercultural Communication Globalization and Social Justice 2nd Edition Sorrells Test Bank 1erinbartlettcbrsgawejx100% (34)

- Transfer Pricing Country Profile BulgariaDocument16 pagesTransfer Pricing Country Profile BulgariaIoanna ZlatevaNo ratings yet

- Latest RFQ (Hospet Bellary Karntaka Dated - 29102010Document69 pagesLatest RFQ (Hospet Bellary Karntaka Dated - 29102010xanblakeNo ratings yet

- FINA 410 - Exercises (NOV)Document7 pagesFINA 410 - Exercises (NOV)said100% (1)