Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Bill Already Paid in Full LetterDocument8 pagesBill Already Paid in Full LetterRoberto Monterrosa98% (80)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Bakery Manufacturing ProcessesDocument26 pagesBakery Manufacturing ProcessesKhundrakpam Satyabarta50% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Uhone Broker GuideDocument28 pagesUhone Broker Guidestech137No ratings yet

- Microsoft Word Shortcut KeysDocument9 pagesMicrosoft Word Shortcut KeysKhundrakpam Satyabarta100% (2)

- Manipur Bank Branches ListDocument17 pagesManipur Bank Branches ListKhundrakpam SatyabartaNo ratings yet

- Information System and Control Audit For Ca FinalDocument157 pagesInformation System and Control Audit For Ca FinalKhundrakpam SatyabartaNo ratings yet

- Mco-7 emDocument8 pagesMco-7 emKhundrakpam Satyabarta100% (3)

- Mnemonics of AuditsDocument17 pagesMnemonics of AuditsKhundrakpam SatyabartaNo ratings yet

- 25 Company Law NotesDocument23 pages25 Company Law NotesKhundrakpam SatyabartaNo ratings yet

- Organisational ChartDocument1 pageOrganisational ChartKhundrakpam SatyabartaNo ratings yet

- G.R. No. 195072. August 1, 2016. Bonifacio Danan, Petitioner, Spouses Gregorio Serrano and Adelaida Reyes, RespondentsDocument19 pagesG.R. No. 195072. August 1, 2016. Bonifacio Danan, Petitioner, Spouses Gregorio Serrano and Adelaida Reyes, RespondentsJENNY BUTACANNo ratings yet

- NSD 2020 Circular PDFDocument11 pagesNSD 2020 Circular PDFRamesh ChavanNo ratings yet

- Ing Bank v. CIR / G.R. No. 167679 / July 22, 2015Document1 pageIng Bank v. CIR / G.R. No. 167679 / July 22, 2015Mini U. Soriano100% (1)

- Elshayeboracler12purchasing 141118065305 Conversion Gate02 PDFDocument250 pagesElshayeboracler12purchasing 141118065305 Conversion Gate02 PDFadnanahmarNo ratings yet

- Annex VDocument4 pagesAnnex VMuhammad Talha ShoaibNo ratings yet

- Invoice 2022 06Document2 pagesInvoice 2022 06violetaNo ratings yet

- Code ListDocument26 pagesCode ListaNo ratings yet

- Sod Risk SummarysapDocument57 pagesSod Risk SummarysapLinh HuynhNo ratings yet

- Ip Ip-Gas Extra Inc Ltd-Agreement-Template-Final-Field-SecuredDocument14 pagesIp Ip-Gas Extra Inc Ltd-Agreement-Template-Final-Field-SecuredQuang Thắng TrầnNo ratings yet

- Applyonline OcmrDocument9 pagesApplyonline Ocmrjafarjsk95No ratings yet

- GI Tecnnology ICASH CARDDocument12 pagesGI Tecnnology ICASH CARDGINo ratings yet

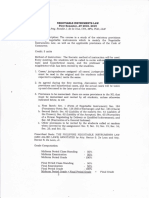

- Liability For Dishonor of Cheques - ProjectDocument53 pagesLiability For Dishonor of Cheques - Projectparullawyer89% (18)

- Cardiopulmonary Physiotherapy in Trauma An Evidence-Based ApproachDocument3 pagesCardiopulmonary Physiotherapy in Trauma An Evidence-Based ApproachGme RpNo ratings yet

- Mahindra Satyam - Oracle EBS R12 EnhancementsDocument73 pagesMahindra Satyam - Oracle EBS R12 EnhancementsRBalajiNo ratings yet

- Detailed Supplier Ledger: Memon Motors (PVT) LimitedDocument4 pagesDetailed Supplier Ledger: Memon Motors (PVT) LimitedSaood ElahiNo ratings yet

- Consultant Agreement HDocument6 pagesConsultant Agreement HVidya Rajawasam Mba Acma100% (1)

- Lecture Notes Cash & Cash Equivalent: Page 1 of 7Document7 pagesLecture Notes Cash & Cash Equivalent: Page 1 of 7Dalia DelrosarioNo ratings yet

- Is The: A Which MainlyDocument7 pagesIs The: A Which MainlyJoovs JoovhoNo ratings yet

- ExerciseDocument18 pagesExerciseRavi Kanth KNo ratings yet

- Gov Acc Module 2Document6 pagesGov Acc Module 2Dadang100% (2)

- Cash and Cash EquivalentsDocument50 pagesCash and Cash EquivalentsAnne EstrellaNo ratings yet

- Serv Central 2307 November 2023Document1 pageServ Central 2307 November 2023andrea.begulbuilderscorpNo ratings yet

- Current & Saving Account StatementDocument164 pagesCurrent & Saving Account StatementNarayan RNo ratings yet

- 1988 Mail Order Hobby Shop CatalogDocument124 pages1988 Mail Order Hobby Shop CatalogJeremy Smith100% (2)

- Al Basit Grands-1Document15 pagesAl Basit Grands-1BAZIL KHANNo ratings yet

- Ryde Hospital Consignment Order Form-14Jan14 PDFDocument1 pageRyde Hospital Consignment Order Form-14Jan14 PDFAndrew WongNo ratings yet

- Action 2Document458 pagesAction 2Stanciu Diana AndreeaNo ratings yet