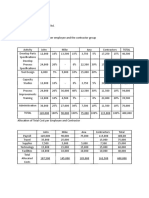

Practice Problem - Answer Recapture (Terminal Loss) UCC For CCA Ending UCC

Practice Problem - Answer Recapture (Terminal Loss) UCC For CCA Ending UCC

You might also like

- CASE STUDY (Danish Energy Agency)Document5 pagesCASE STUDY (Danish Energy Agency)Malik RayyanNo ratings yet

- Mystic SportsDocument6 pagesMystic SportsBatista Firangi100% (2)

- Case Hardhat - Rashik, PoorviDocument6 pagesCase Hardhat - Rashik, PoorviRashik Gupta100% (1)

- Optical Distortion Case StudyDocument4 pagesOptical Distortion Case StudyAmit Gokhale100% (2)

- PPE2-sample - Debi Comia PPE2-sample - Debi ComiaDocument16 pagesPPE2-sample - Debi Comia PPE2-sample - Debi ComiaAngelica Pagaduan50% (2)

- Gangham KemiDocument2 pagesGangham KemiDelmPia ValdezNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document6 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Cost Estimation & CVP Suggested SolutionDocument15 pagesCost Estimation & CVP Suggested SolutionNguyên Văn NhậtNo ratings yet

- Management and Financial Accounting Assessment-2Document6 pagesManagement and Financial Accounting Assessment-2saranyaNo ratings yet

- Same Questions - F303 - 1st MidDocument5 pagesSame Questions - F303 - 1st MidRafid Al Abid SpondonNo ratings yet

- Overheads Part 1 SolutionsDocument25 pagesOverheads Part 1 Solutionsdoshiviraj77No ratings yet

- Cash Flow EstimationDocument6 pagesCash Flow EstimationFazul RehmanNo ratings yet

- DownloadDocument18 pagesDownloadGaurav MandotNo ratings yet

- Cost Management AssignmentDocument29 pagesCost Management AssignmentInanda MeitasariNo ratings yet

- 1 Property, Plant and Equipment IAS 16 Slides 2022Document49 pages1 Property, Plant and Equipment IAS 16 Slides 2022Tuyakula ShipadiNo ratings yet

- ProblemSet Cash Flow EstimationQA 160611 021520 PDFDocument25 pagesProblemSet Cash Flow EstimationQA 160611 021520 PDFCucumber IsHealthy96No ratings yet

- ProblemSet Cash Flow EstimationQA-160611 - 021520Document25 pagesProblemSet Cash Flow EstimationQA-160611 - 021520Jonathan Punnalagan100% (2)

- CFAS - Depreciation Methods - Barcelona, JoyceAnnDocument9 pagesCFAS - Depreciation Methods - Barcelona, JoyceAnnJoyce Ann Agdippa BarcelonaNo ratings yet

- INTACC2 - Chapter 29Document4 pagesINTACC2 - Chapter 29Shane TabunggaoNo ratings yet

- Far Chapter 2 II Lkas 16 enDocument2 pagesFar Chapter 2 II Lkas 16 enTiran WijemanneNo ratings yet

- Alba, Camille Joy M. MGT211: Total Cost 240,000.00Document4 pagesAlba, Camille Joy M. MGT211: Total Cost 240,000.00Camille Joy AlbaNo ratings yet

- Chapter 5 ExercisesDocument12 pagesChapter 5 ExercisesIsaiah BatucanNo ratings yet

- Q-6 Spr-08 (Yahya Limited) Q ADocument2 pagesQ-6 Spr-08 (Yahya Limited) Q AiamneonkingNo ratings yet

- Practice Questions 1Document5 pagesPractice Questions 1Div_nNo ratings yet

- Bajaj Finserv Investor Presentation - Q2 FY2018-19Document19 pagesBajaj Finserv Investor Presentation - Q2 FY2018-19AmarNo ratings yet

- Class Exercise CH 10Document5 pagesClass Exercise CH 10Iftekhar AhmedNo ratings yet

- 7-28 7-29 The Direct MethodDocument5 pages7-28 7-29 The Direct MethodJohn Carlo AquinoNo ratings yet

- Module 5 CCA Exercise SolutionsDocument12 pagesModule 5 CCA Exercise SolutionshodaNo ratings yet

- 2nd Monthly AssessmentDocument58 pages2nd Monthly AssessmentMichale JacomillaNo ratings yet

- Key To Correction - Intermediate Accounting - Midterm - 2019-2020Document10 pagesKey To Correction - Intermediate Accounting - Midterm - 2019-2020Renalyn ParasNo ratings yet

- Management Accounting: Page 1 of 6Document70 pagesManagement Accounting: Page 1 of 6Ahmed Raza MirNo ratings yet

- Management and Financial Accounting: (Assignment-2)Document10 pagesManagement and Financial Accounting: (Assignment-2)kashish Agarwal100% (1)

- Management & Financial AccountingDocument6 pagesManagement & Financial AccountingAnamitra SenNo ratings yet

- Final Economy 2010 SolutionDocument6 pagesFinal Economy 2010 SolutionValadez28No ratings yet

- Answers For EXERCISES On TOPIC 6Document9 pagesAnswers For EXERCISES On TOPIC 6Alia HazwaniNo ratings yet

- In Class File Chapter 11Document17 pagesIn Class File Chapter 11kathleen fajardoNo ratings yet

- MA hw6Document5 pagesMA hw6Caleb BuddNo ratings yet

- Ch. 4Document9 pagesCh. 4Abel ZewdeNo ratings yet

- Solution 1 To 6 ProblemsDocument5 pagesSolution 1 To 6 Problemspratham kannanNo ratings yet

- Assignment 1556954208 SmsDocument59 pagesAssignment 1556954208 SmsentertainmentqurryNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 10Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 10Roshan RamkhalawonNo ratings yet

- Cañezal Assignment 2 CHECKEDDocument6 pagesCañezal Assignment 2 CHECKEDFeliz Victoria CañezalNo ratings yet

- Revaluation ModelDocument33 pagesRevaluation ModelLumongtadJoanMaeNo ratings yet

- Replacement Model 2Document12 pagesReplacement Model 2sathwikreddy123kasthuriNo ratings yet

- PM - Dec 2011.odsDocument2 pagesPM - Dec 2011.odsFarman ShaikhNo ratings yet

- Cup Pa Mania ProjectDocument4 pagesCup Pa Mania ProjectDurgaprasad VelamalaNo ratings yet

- Chapter 28Document6 pagesChapter 28Shane Ivory ClaudioNo ratings yet

- Pg-11-7 Book Valuve: Assignment Capital BudgetingDocument9 pagesPg-11-7 Book Valuve: Assignment Capital BudgetingIffi RaniNo ratings yet

- Question 4Document8 pagesQuestion 4Jeremiah NcubeNo ratings yet

- Intermediate Accounting 3Document18 pagesIntermediate Accounting 3Cristine MayNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Engineering Economy 15th Edition Sullivan Test BankDocument30 pagesEngineering Economy 15th Edition Sullivan Test Bankkieranthang03m100% (38)

- Engineering Economy 15th Edition Sullivan Test Bank Full Chapter PDFDocument51 pagesEngineering Economy 15th Edition Sullivan Test Bank Full Chapter PDFRobertFordicwr100% (15)

- Assignment - OHD ACC116Document3 pagesAssignment - OHD ACC116Nurul NajihaNo ratings yet

- Paper 2Document5 pagesPaper 2dua95960No ratings yet

- Module 2 - Laboratory Exercise 1Document10 pagesModule 2 - Laboratory Exercise 1Joana TrinidadNo ratings yet

- Comsats University Islamabad Abbottabad Campus Engineering Economics Assigment 04Document13 pagesComsats University Islamabad Abbottabad Campus Engineering Economics Assigment 04yaseen ayazNo ratings yet

- Category Cost of Asset Accumulated DepreciationDocument10 pagesCategory Cost of Asset Accumulated DepreciationAaliyah ManuelNo ratings yet

- Exercises On Joint Cost and By-ProductsDocument2 pagesExercises On Joint Cost and By-ProductsVixen Aaron EnriquezNo ratings yet

- Chapter 4 CB Problems - IDocument11 pagesChapter 4 CB Problems - IRoy YadavNo ratings yet

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1Document36 pagesFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1jillhernandezqortfpmndz100% (30)

- The AS9100C, AS9110, and AS9120 Handbook: Understanding Aviation, Space, and Defense Best PracticesFrom EverandThe AS9100C, AS9110, and AS9120 Handbook: Understanding Aviation, Space, and Defense Best PracticesNo ratings yet

- Optimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementFrom EverandOptimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementNo ratings yet

- Sri Harmandir SahibDocument1 pageSri Harmandir SahibSalman AliNo ratings yet

- Punjabi Kalam Mian SahibDocument178 pagesPunjabi Kalam Mian SahibSalman AliNo ratings yet

- The Quranic Concept of HistoryDocument18 pagesThe Quranic Concept of HistorySalman AliNo ratings yet

- Practice Problem - Answer A) Reconciliation ApproachDocument3 pagesPractice Problem - Answer A) Reconciliation ApproachSalman AliNo ratings yet

- Hadith and MosqueDocument451 pagesHadith and MosqueSalman AliNo ratings yet

- Durood SharifDocument3 pagesDurood SharifSalman AliNo ratings yet

- Western Scholarship and The AuthenticityDocument18 pagesWestern Scholarship and The AuthenticitySalman AliNo ratings yet

- Chapter 1.1 PDFDocument67 pagesChapter 1.1 PDFk61.2214535043No ratings yet

- Caiib Paper 1 PDFDocument262 pagesCaiib Paper 1 PDFDeepak Rathore100% (1)

- Quantity ManagementDocument16 pagesQuantity ManagementUsman MalikNo ratings yet

- 2011 MLS HandbookDocument167 pages2011 MLS HandbookAlisonAshby100% (1)

- Effective Price Vs PO Price in SAPDocument2 pagesEffective Price Vs PO Price in SAP83pankajNo ratings yet

- Price Determination Under Monopolistic Competition: DefinitionsDocument8 pagesPrice Determination Under Monopolistic Competition: DefinitionsAman MittalNo ratings yet

- ECON 205 Chapters 3 & 4 Practice QuestionsDocument4 pagesECON 205 Chapters 3 & 4 Practice Questionskely wilsonNo ratings yet

- ARKA - Arkha Jayanti Persada TBK.: RTI AnalyticsDocument1 pageARKA - Arkha Jayanti Persada TBK.: RTI AnalyticsfarialNo ratings yet

- WebSim - Price Volume PDFDocument10 pagesWebSim - Price Volume PDFNeelesh KumarNo ratings yet

- Tax Invoice: ARJUNA INDANE AGENCY (0000117657)Document1 pageTax Invoice: ARJUNA INDANE AGENCY (0000117657)VrathakrishnanNo ratings yet

- Colgate Palmolive FinalDocument18 pagesColgate Palmolive FinalSruti PujariNo ratings yet

- Hal, R. Varian (Academic and Bio Information)Document23 pagesHal, R. Varian (Academic and Bio Information)Juan Camilo Osorio GallegoNo ratings yet

- Mepco Per Unit Price 2021Document2 pagesMepco Per Unit Price 2021Thai jasiiNo ratings yet

- CBSE Class 12 Economics Paper 2019 Set 1Document76 pagesCBSE Class 12 Economics Paper 2019 Set 1NikhilNo ratings yet

- Paul Schneiderman, PH.D., Professor of Finance & Economics, Southern New Hampshire University ©2008 South-WesternDocument33 pagesPaul Schneiderman, PH.D., Professor of Finance & Economics, Southern New Hampshire University ©2008 South-WesternEmily TanNo ratings yet

- MarketingDocument486 pagesMarketingRs rsNo ratings yet

- The Flights of Malaysia Airlines Marketing EssayDocument17 pagesThe Flights of Malaysia Airlines Marketing EssayMia KulalNo ratings yet

- Law of Demand: Course Code: KMB 102 Faculty: Ms Avneet KaurDocument92 pagesLaw of Demand: Course Code: KMB 102 Faculty: Ms Avneet KaurShivani MishraNo ratings yet

- Sales of Goods Act, 1930Document20 pagesSales of Goods Act, 1930ohmygodhritikNo ratings yet

- IJAZ AHMED M R - Business-Plan-Of-Leather-ProductsDocument21 pagesIJAZ AHMED M R - Business-Plan-Of-Leather-ProductsDon’t KnowNo ratings yet

- McDonalds Case StudyDocument20 pagesMcDonalds Case StudyNeelmani SharmaNo ratings yet

- The Hindu Editorial With Vocabulary PDFDocument43 pagesThe Hindu Editorial With Vocabulary PDFGulshan D'souzaNo ratings yet

- CONSIGNMENTDocument1 pageCONSIGNMENTLayla SimNo ratings yet

- Hydrogen and Fuel Cell Scooters - Electric Bicycles - WheelchairsDocument6 pagesHydrogen and Fuel Cell Scooters - Electric Bicycles - WheelchairsHasanUSLUMNo ratings yet

- Penny Candy?: Whatever HappenedDocument82 pagesPenny Candy?: Whatever HappenedcocoNo ratings yet

- Narayan Acharya QuotationDocument1 pageNarayan Acharya QuotationsanjayaNo ratings yet

- Mind Teasers: The Pizza Menu Maths Puzzle: Answer & ExplanationDocument4 pagesMind Teasers: The Pizza Menu Maths Puzzle: Answer & Explanationarockia rajNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- CASE STUDY (Danish Energy Agency)Document5 pagesCASE STUDY (Danish Energy Agency)Malik RayyanNo ratings yet

- Mystic SportsDocument6 pagesMystic SportsBatista Firangi100% (2)

- Case Hardhat - Rashik, PoorviDocument6 pagesCase Hardhat - Rashik, PoorviRashik Gupta100% (1)

- Optical Distortion Case StudyDocument4 pagesOptical Distortion Case StudyAmit Gokhale100% (2)

- PPE2-sample - Debi Comia PPE2-sample - Debi ComiaDocument16 pagesPPE2-sample - Debi Comia PPE2-sample - Debi ComiaAngelica Pagaduan50% (2)

- Gangham KemiDocument2 pagesGangham KemiDelmPia ValdezNo ratings yet

- RUNNING HEAD: Accounting Questions 1Document6 pagesRUNNING HEAD: Accounting Questions 1Chirayu ThapaNo ratings yet

- Cost Estimation & CVP Suggested SolutionDocument15 pagesCost Estimation & CVP Suggested SolutionNguyên Văn NhậtNo ratings yet

- Management and Financial Accounting Assessment-2Document6 pagesManagement and Financial Accounting Assessment-2saranyaNo ratings yet

- Same Questions - F303 - 1st MidDocument5 pagesSame Questions - F303 - 1st MidRafid Al Abid SpondonNo ratings yet

- Overheads Part 1 SolutionsDocument25 pagesOverheads Part 1 Solutionsdoshiviraj77No ratings yet

- Cash Flow EstimationDocument6 pagesCash Flow EstimationFazul RehmanNo ratings yet

- DownloadDocument18 pagesDownloadGaurav MandotNo ratings yet

- Cost Management AssignmentDocument29 pagesCost Management AssignmentInanda MeitasariNo ratings yet

- 1 Property, Plant and Equipment IAS 16 Slides 2022Document49 pages1 Property, Plant and Equipment IAS 16 Slides 2022Tuyakula ShipadiNo ratings yet

- ProblemSet Cash Flow EstimationQA 160611 021520 PDFDocument25 pagesProblemSet Cash Flow EstimationQA 160611 021520 PDFCucumber IsHealthy96No ratings yet

- ProblemSet Cash Flow EstimationQA-160611 - 021520Document25 pagesProblemSet Cash Flow EstimationQA-160611 - 021520Jonathan Punnalagan100% (2)

- CFAS - Depreciation Methods - Barcelona, JoyceAnnDocument9 pagesCFAS - Depreciation Methods - Barcelona, JoyceAnnJoyce Ann Agdippa BarcelonaNo ratings yet

- INTACC2 - Chapter 29Document4 pagesINTACC2 - Chapter 29Shane TabunggaoNo ratings yet

- Far Chapter 2 II Lkas 16 enDocument2 pagesFar Chapter 2 II Lkas 16 enTiran WijemanneNo ratings yet

- Alba, Camille Joy M. MGT211: Total Cost 240,000.00Document4 pagesAlba, Camille Joy M. MGT211: Total Cost 240,000.00Camille Joy AlbaNo ratings yet

- Chapter 5 ExercisesDocument12 pagesChapter 5 ExercisesIsaiah BatucanNo ratings yet

- Q-6 Spr-08 (Yahya Limited) Q ADocument2 pagesQ-6 Spr-08 (Yahya Limited) Q AiamneonkingNo ratings yet

- Practice Questions 1Document5 pagesPractice Questions 1Div_nNo ratings yet

- Bajaj Finserv Investor Presentation - Q2 FY2018-19Document19 pagesBajaj Finserv Investor Presentation - Q2 FY2018-19AmarNo ratings yet

- Class Exercise CH 10Document5 pagesClass Exercise CH 10Iftekhar AhmedNo ratings yet

- 7-28 7-29 The Direct MethodDocument5 pages7-28 7-29 The Direct MethodJohn Carlo AquinoNo ratings yet

- Module 5 CCA Exercise SolutionsDocument12 pagesModule 5 CCA Exercise SolutionshodaNo ratings yet

- 2nd Monthly AssessmentDocument58 pages2nd Monthly AssessmentMichale JacomillaNo ratings yet

- Key To Correction - Intermediate Accounting - Midterm - 2019-2020Document10 pagesKey To Correction - Intermediate Accounting - Midterm - 2019-2020Renalyn ParasNo ratings yet

- Management Accounting: Page 1 of 6Document70 pagesManagement Accounting: Page 1 of 6Ahmed Raza MirNo ratings yet

- Management and Financial Accounting: (Assignment-2)Document10 pagesManagement and Financial Accounting: (Assignment-2)kashish Agarwal100% (1)

- Management & Financial AccountingDocument6 pagesManagement & Financial AccountingAnamitra SenNo ratings yet

- Final Economy 2010 SolutionDocument6 pagesFinal Economy 2010 SolutionValadez28No ratings yet

- Answers For EXERCISES On TOPIC 6Document9 pagesAnswers For EXERCISES On TOPIC 6Alia HazwaniNo ratings yet

- In Class File Chapter 11Document17 pagesIn Class File Chapter 11kathleen fajardoNo ratings yet

- MA hw6Document5 pagesMA hw6Caleb BuddNo ratings yet

- Ch. 4Document9 pagesCh. 4Abel ZewdeNo ratings yet

- Solution 1 To 6 ProblemsDocument5 pagesSolution 1 To 6 Problemspratham kannanNo ratings yet

- Assignment 1556954208 SmsDocument59 pagesAssignment 1556954208 SmsentertainmentqurryNo ratings yet

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 10Document2 pagesAllocation and Apportionment and Job and Batch Costing Worked Example Question 10Roshan RamkhalawonNo ratings yet

- Cañezal Assignment 2 CHECKEDDocument6 pagesCañezal Assignment 2 CHECKEDFeliz Victoria CañezalNo ratings yet

- Revaluation ModelDocument33 pagesRevaluation ModelLumongtadJoanMaeNo ratings yet

- Replacement Model 2Document12 pagesReplacement Model 2sathwikreddy123kasthuriNo ratings yet

- PM - Dec 2011.odsDocument2 pagesPM - Dec 2011.odsFarman ShaikhNo ratings yet

- Cup Pa Mania ProjectDocument4 pagesCup Pa Mania ProjectDurgaprasad VelamalaNo ratings yet

- Chapter 28Document6 pagesChapter 28Shane Ivory ClaudioNo ratings yet

- Pg-11-7 Book Valuve: Assignment Capital BudgetingDocument9 pagesPg-11-7 Book Valuve: Assignment Capital BudgetingIffi RaniNo ratings yet

- Question 4Document8 pagesQuestion 4Jeremiah NcubeNo ratings yet

- Intermediate Accounting 3Document18 pagesIntermediate Accounting 3Cristine MayNo ratings yet

- Answer Key Discussion of Sir Paul of PreweekDocument2 pagesAnswer Key Discussion of Sir Paul of PreweekElaine Joyce GarciaNo ratings yet

- Engineering Economy 15th Edition Sullivan Test BankDocument30 pagesEngineering Economy 15th Edition Sullivan Test Bankkieranthang03m100% (38)

- Engineering Economy 15th Edition Sullivan Test Bank Full Chapter PDFDocument51 pagesEngineering Economy 15th Edition Sullivan Test Bank Full Chapter PDFRobertFordicwr100% (15)

- Assignment - OHD ACC116Document3 pagesAssignment - OHD ACC116Nurul NajihaNo ratings yet

- Paper 2Document5 pagesPaper 2dua95960No ratings yet

- Module 2 - Laboratory Exercise 1Document10 pagesModule 2 - Laboratory Exercise 1Joana TrinidadNo ratings yet

- Comsats University Islamabad Abbottabad Campus Engineering Economics Assigment 04Document13 pagesComsats University Islamabad Abbottabad Campus Engineering Economics Assigment 04yaseen ayazNo ratings yet

- Category Cost of Asset Accumulated DepreciationDocument10 pagesCategory Cost of Asset Accumulated DepreciationAaliyah ManuelNo ratings yet

- Exercises On Joint Cost and By-ProductsDocument2 pagesExercises On Joint Cost and By-ProductsVixen Aaron EnriquezNo ratings yet

- Chapter 4 CB Problems - IDocument11 pagesChapter 4 CB Problems - IRoy YadavNo ratings yet

- Fundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1Document36 pagesFundamentals of Corporate Finance Canadian 6th Edition Brealey Solutions Manual 1jillhernandezqortfpmndz100% (30)

- The AS9100C, AS9110, and AS9120 Handbook: Understanding Aviation, Space, and Defense Best PracticesFrom EverandThe AS9100C, AS9110, and AS9120 Handbook: Understanding Aviation, Space, and Defense Best PracticesNo ratings yet

- Optimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementFrom EverandOptimizing Factory Performance: Cost-Effective Ways to Achieve Significant and Sustainable ImprovementNo ratings yet

- Sri Harmandir SahibDocument1 pageSri Harmandir SahibSalman AliNo ratings yet

- Punjabi Kalam Mian SahibDocument178 pagesPunjabi Kalam Mian SahibSalman AliNo ratings yet

- The Quranic Concept of HistoryDocument18 pagesThe Quranic Concept of HistorySalman AliNo ratings yet

- Practice Problem - Answer A) Reconciliation ApproachDocument3 pagesPractice Problem - Answer A) Reconciliation ApproachSalman AliNo ratings yet

- Hadith and MosqueDocument451 pagesHadith and MosqueSalman AliNo ratings yet

- Durood SharifDocument3 pagesDurood SharifSalman AliNo ratings yet

- Western Scholarship and The AuthenticityDocument18 pagesWestern Scholarship and The AuthenticitySalman AliNo ratings yet

- Chapter 1.1 PDFDocument67 pagesChapter 1.1 PDFk61.2214535043No ratings yet

- Caiib Paper 1 PDFDocument262 pagesCaiib Paper 1 PDFDeepak Rathore100% (1)

- Quantity ManagementDocument16 pagesQuantity ManagementUsman MalikNo ratings yet

- 2011 MLS HandbookDocument167 pages2011 MLS HandbookAlisonAshby100% (1)

- Effective Price Vs PO Price in SAPDocument2 pagesEffective Price Vs PO Price in SAP83pankajNo ratings yet

- Price Determination Under Monopolistic Competition: DefinitionsDocument8 pagesPrice Determination Under Monopolistic Competition: DefinitionsAman MittalNo ratings yet

- ECON 205 Chapters 3 & 4 Practice QuestionsDocument4 pagesECON 205 Chapters 3 & 4 Practice Questionskely wilsonNo ratings yet

- ARKA - Arkha Jayanti Persada TBK.: RTI AnalyticsDocument1 pageARKA - Arkha Jayanti Persada TBK.: RTI AnalyticsfarialNo ratings yet

- WebSim - Price Volume PDFDocument10 pagesWebSim - Price Volume PDFNeelesh KumarNo ratings yet

- Tax Invoice: ARJUNA INDANE AGENCY (0000117657)Document1 pageTax Invoice: ARJUNA INDANE AGENCY (0000117657)VrathakrishnanNo ratings yet

- Colgate Palmolive FinalDocument18 pagesColgate Palmolive FinalSruti PujariNo ratings yet

- Hal, R. Varian (Academic and Bio Information)Document23 pagesHal, R. Varian (Academic and Bio Information)Juan Camilo Osorio GallegoNo ratings yet

- Mepco Per Unit Price 2021Document2 pagesMepco Per Unit Price 2021Thai jasiiNo ratings yet

- CBSE Class 12 Economics Paper 2019 Set 1Document76 pagesCBSE Class 12 Economics Paper 2019 Set 1NikhilNo ratings yet

- Paul Schneiderman, PH.D., Professor of Finance & Economics, Southern New Hampshire University ©2008 South-WesternDocument33 pagesPaul Schneiderman, PH.D., Professor of Finance & Economics, Southern New Hampshire University ©2008 South-WesternEmily TanNo ratings yet

- MarketingDocument486 pagesMarketingRs rsNo ratings yet

- The Flights of Malaysia Airlines Marketing EssayDocument17 pagesThe Flights of Malaysia Airlines Marketing EssayMia KulalNo ratings yet

- Law of Demand: Course Code: KMB 102 Faculty: Ms Avneet KaurDocument92 pagesLaw of Demand: Course Code: KMB 102 Faculty: Ms Avneet KaurShivani MishraNo ratings yet

- Sales of Goods Act, 1930Document20 pagesSales of Goods Act, 1930ohmygodhritikNo ratings yet

- IJAZ AHMED M R - Business-Plan-Of-Leather-ProductsDocument21 pagesIJAZ AHMED M R - Business-Plan-Of-Leather-ProductsDon’t KnowNo ratings yet

- McDonalds Case StudyDocument20 pagesMcDonalds Case StudyNeelmani SharmaNo ratings yet

- The Hindu Editorial With Vocabulary PDFDocument43 pagesThe Hindu Editorial With Vocabulary PDFGulshan D'souzaNo ratings yet

- CONSIGNMENTDocument1 pageCONSIGNMENTLayla SimNo ratings yet

- Hydrogen and Fuel Cell Scooters - Electric Bicycles - WheelchairsDocument6 pagesHydrogen and Fuel Cell Scooters - Electric Bicycles - WheelchairsHasanUSLUMNo ratings yet

- Penny Candy?: Whatever HappenedDocument82 pagesPenny Candy?: Whatever HappenedcocoNo ratings yet

- Narayan Acharya QuotationDocument1 pageNarayan Acharya QuotationsanjayaNo ratings yet

- Mind Teasers: The Pizza Menu Maths Puzzle: Answer & ExplanationDocument4 pagesMind Teasers: The Pizza Menu Maths Puzzle: Answer & Explanationarockia rajNo ratings yet