Download as docx, pdf, or txt

You might also like

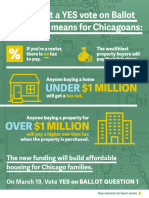

- BCHI24023 Explainer Infographic FINAL FPODocument2 pagesBCHI24023 Explainer Infographic FINAL FPORobert GarciaNo ratings yet

- Joint Status ReportDocument4 pagesJoint Status ReportKenan FarrellNo ratings yet

- FRCR Part 1 - Radiological Anatomy - New For 2013 - Set 02 PDFDocument109 pagesFRCR Part 1 - Radiological Anatomy - New For 2013 - Set 02 PDFmohamed100% (3)

- The Economic Theory of Rent Seeking TollisonDocument11 pagesThe Economic Theory of Rent Seeking TollisonMinToo KaaLitaNo ratings yet

- HLTH 101 Final Research Paper - Due 11 30Document7 pagesHLTH 101 Final Research Paper - Due 11 30api-625713699No ratings yet

- Leslie AbbottDocument6 pagesLeslie AbbottZewa MiteuNo ratings yet

- UGA RMIN 4000 Exam 2 Study GuideDocument13 pagesUGA RMIN 4000 Exam 2 Study GuideBrittany Danielle ThompsonNo ratings yet

- SEARS HOLDINGS Bankruptcy Doc 1436 Junior DipDocument258 pagesSEARS HOLDINGS Bankruptcy Doc 1436 Junior DipEric MooreNo ratings yet

- t180 6902502 SM 7-09Document961 pagest180 6902502 SM 7-09vadim vadim100% (3)

- Ainslie, George - Breakdown of Will PDFDocument272 pagesAinslie, George - Breakdown of Will PDFIsisGV50% (2)

- Underwriting in Insurance: Maharaja Agrasen Institute of Management StudiesDocument18 pagesUnderwriting in Insurance: Maharaja Agrasen Institute of Management Studiesfrnds4everzNo ratings yet

- 200 IC 33 Test QuestionsDocument36 pages200 IC 33 Test QuestionsDinesh KatochNo ratings yet

- Insurance of Assets and Personnel - Legal and Statutory FrameworkDocument32 pagesInsurance of Assets and Personnel - Legal and Statutory FrameworkChinedu Cordelia OkpalekeNo ratings yet

- Rent Regulation Hstpa PresentationDocument19 pagesRent Regulation Hstpa PresentationLuke ParsnowNo ratings yet

- American ExpreesDocument11 pagesAmerican ExpreesShikha Varshney0% (1)

- Principles of Insurance: IndemnityDocument27 pagesPrinciples of Insurance: IndemnitytaijulshadinNo ratings yet

- Guide To Interruption InsuranceDocument46 pagesGuide To Interruption InsuranceBrian HughesNo ratings yet

- PIImageDisplay AspxDocument6 pagesPIImageDisplay AspxBea ParrillaaNo ratings yet

- Real Estate - Understanding U.S. Real Estate DebtDocument16 pagesReal Estate - Understanding U.S. Real Estate DebtgarchevNo ratings yet

- Fiancial Market InfrastructureDocument16 pagesFiancial Market InfrastructureBoubacar Zakari WARGONo ratings yet

- ContractsDocument6 pagesContractsChristopher DizonNo ratings yet

- Property Tax CADocument42 pagesProperty Tax CAElnur5No ratings yet

- Memo To Riverside County Supervisors On Improvements To Child and Adult Protective ServicesDocument5 pagesMemo To Riverside County Supervisors On Improvements To Child and Adult Protective ServicesThe Press-Enterprise / pressenterprise.comNo ratings yet

- Session 4 - Types of InsuranceDocument50 pagesSession 4 - Types of InsuranceJames Patrick PedrosoNo ratings yet

- FTPrep Exam 1Document27 pagesFTPrep Exam 1Motion ParallaxNo ratings yet

- RHB Product TC Personal FinancingDocument17 pagesRHB Product TC Personal FinancingDon LotNo ratings yet

- Elements of Insurance E-ContentDocument29 pagesElements of Insurance E-ContentPrem Kumar.DNo ratings yet

- A Study On Risk Management Tools and Techniques in Life Insurance Industry in IndiaDocument30 pagesA Study On Risk Management Tools and Techniques in Life Insurance Industry in IndiadevilNo ratings yet

- Go To The United States Code Service Archive DirectoryDocument10 pagesGo To The United States Code Service Archive DirectoryAndy Williams Jr.No ratings yet

- TFAS Ebook Speeches Vol 1 v8Document22 pagesTFAS Ebook Speeches Vol 1 v8Chris Huss Sr.No ratings yet

- Asset Forfeiture Policy Manual 2023Document190 pagesAsset Forfeiture Policy Manual 2023AndreaNo ratings yet

- People's Choice Mag PDFDocument32 pagesPeople's Choice Mag PDFAMH_DocsNo ratings yet

- India:: Title Insurance: New Product For Old IssuesDocument37 pagesIndia:: Title Insurance: New Product For Old IssuesRaman AgarwalNo ratings yet

- What Is Bad Faith InsuranceDocument11 pagesWhat Is Bad Faith InsurancechaimaNo ratings yet

- Digital SignatureDocument39 pagesDigital Signaturevijay anandNo ratings yet

- 22D OptionalClausesDocument2 pages22D OptionalClausesJanet NNo ratings yet

- PFN MLO Onboarding Package&Agreement-Contreras, Adriell - EncryptedDocument73 pagesPFN MLO Onboarding Package&Agreement-Contreras, Adriell - EncryptedVanessa GuardadoNo ratings yet

- COST - Re Nevis TrustDocument5 pagesCOST - Re Nevis TrustAJ SinghNo ratings yet

- Types of Insurance/Life Insurance/General InsuranceDocument3 pagesTypes of Insurance/Life Insurance/General Insuranceamarx29200050% (2)

- Frauds in InsuranceDocument35 pagesFrauds in Insuranceprjivi100% (1)

- American Airline 2019Document227 pagesAmerican Airline 2019gbenga oyedele100% (1)

- Deal or No Deal - Buying A CarDocument3 pagesDeal or No Deal - Buying A CarJalen ChaneyNo ratings yet

- Calabrese's RulingDocument31 pagesCalabrese's RulingDoug100% (1)

- INTERNATIONAL CONSUMER'S LAW Chapter 3Document24 pagesINTERNATIONAL CONSUMER'S LAW Chapter 3Maereenyll OnifaNo ratings yet

- Free Guide Section8Document1 pageFree Guide Section8BảooTrânnNo ratings yet

- 2nature and StatusDocument8 pages2nature and StatusTheplaymaker508No ratings yet

- Life and General Insurance - Bcom 5 Sem Ebook and NotesDocument28 pagesLife and General Insurance - Bcom 5 Sem Ebook and NotesEnoch Gilchrist100% (1)

- Benefits of InsuranceDocument42 pagesBenefits of InsurancerocksonNo ratings yet

- The 3DayCar Programme - The Customer and The 3DayCar - Focus Groups FindingsDocument105 pagesThe 3DayCar Programme - The Customer and The 3DayCar - Focus Groups FindingsYan1203No ratings yet

- 2021 2022 Xtreme WA Mock Trial CaseDocument73 pages2021 2022 Xtreme WA Mock Trial CaseGrace RosenNo ratings yet

- From Primitive Barter To Inflationary Dollar: A Warless Economic Weapon of Mass DestructionDocument50 pagesFrom Primitive Barter To Inflationary Dollar: A Warless Economic Weapon of Mass DestructionJohn TaskinsoyNo ratings yet

- Hud PdfbackuplinkDocument2 pagesHud PdfbackuplinkCorla Reeves JacksonNo ratings yet

- ARES 2004-8A - ProspectusDocument242 pagesARES 2004-8A - ProspectusnagobadsNo ratings yet

- BerkshirehathawayDocument11 pagesBerkshirehathawayTraderCat SolarisNo ratings yet

- Vaxart Class Action Proposed SettlementDocument46 pagesVaxart Class Action Proposed SettlementEric SandersNo ratings yet

- Atlantic Permanent Federal Savings and Loan Association v. American Casualty Company of Reading, Pennsylvania, 839 F.2d 212, 4th Cir. (1988)Document12 pagesAtlantic Permanent Federal Savings and Loan Association v. American Casualty Company of Reading, Pennsylvania, 839 F.2d 212, 4th Cir. (1988)Scribd Government Docs100% (1)

- SCLiquor LLC V Empire Investment Inc.Document27 pagesSCLiquor LLC V Empire Investment Inc.BillboardNo ratings yet

- Bill 87Document62 pagesBill 87Webbie HeraldNo ratings yet

- Break Down ContractsDocument41 pagesBreak Down ContractsGreta CarterNo ratings yet

- Group Captives: Are They Right For You?: by - Jim HoittDocument6 pagesGroup Captives: Are They Right For You?: by - Jim HoittVicente TorresNo ratings yet

- On Wave Nature of MatterDocument16 pagesOn Wave Nature of MatterAparna GorakhiaNo ratings yet

- City of Scottsdale - Rio Verde Foothills - Petition - City ResponseDocument101 pagesCity of Scottsdale - Rio Verde Foothills - Petition - City ResponseamyjoiNo ratings yet

- Judicial Branch Study GuideDocument2 pagesJudicial Branch Study GuideEUGENE DEXTER NONESNo ratings yet

- 11.0 Project Risk ManagementDocument14 pages11.0 Project Risk ManagementEUGENE DEXTER NONES100% (1)

- Human Resources Management (DECA)Document4 pagesHuman Resources Management (DECA)EUGENE DEXTER NONESNo ratings yet

- Chapter 6 Project Activity PlanningDocument5 pagesChapter 6 Project Activity PlanningEUGENE DEXTER NONESNo ratings yet

- Political Sociology Chapter 11Document2 pagesPolitical Sociology Chapter 11EUGENE DEXTER NONESNo ratings yet

- Unit 4 PopulationsDocument2 pagesUnit 4 PopulationsEUGENE DEXTER NONESNo ratings yet

- Leisure and RecreationDocument5 pagesLeisure and RecreationEUGENE DEXTER NONESNo ratings yet

- Intro To Computer CH 9Document5 pagesIntro To Computer CH 9EUGENE DEXTER NONESNo ratings yet

- Ethical Hacking Test 1Document15 pagesEthical Hacking Test 1EUGENE DEXTER NONESNo ratings yet

- Chapter 15 - Authority and The StateDocument9 pagesChapter 15 - Authority and The StateEUGENE DEXTER NONESNo ratings yet

- 304 Stainless Steel Chemical Compatibility Chart From IsmDocument11 pages304 Stainless Steel Chemical Compatibility Chart From IsmchenNo ratings yet

- FL3100H and FL3101H UV IR and UV Unitized Flame DetectorsDocument2 pagesFL3100H and FL3101H UV IR and UV Unitized Flame DetectorsRomdhoni Widyo BaskoroNo ratings yet

- Parent Letter To MCPS Re Student Injury Data - 01-14-2015Document11 pagesParent Letter To MCPS Re Student Injury Data - 01-14-2015Concussion_MCPS_MdNo ratings yet

- Free Calisthenics EbookDocument20 pagesFree Calisthenics Ebookaltclips0No ratings yet

- Complexometric Titrations by Gunja ChaturvediDocument16 pagesComplexometric Titrations by Gunja ChaturvediGunja Chaturvedi100% (3)

- Causes and Prevention of Paint Failure PDFDocument14 pagesCauses and Prevention of Paint Failure PDFsenthilkumarNo ratings yet

- En - Techinfo - TRILITE SM210Document9 pagesEn - Techinfo - TRILITE SM210Emrh YsltsNo ratings yet

- Admission FormDocument1 pageAdmission FormYasin AhmedNo ratings yet

- Audio Frequency Amplifier Applications: Absolute Maximum RatingsDocument5 pagesAudio Frequency Amplifier Applications: Absolute Maximum RatingsDinh NguyenNo ratings yet

- Hira WalravenDocument219 pagesHira WalravennunnaraoNo ratings yet

- Geotechnical Factual ReportDocument89 pagesGeotechnical Factual ReportMohamed RusfanNo ratings yet

- BAND 675 North RD - Mechanical IFC - 2023-11-15Document162 pagesBAND 675 North RD - Mechanical IFC - 2023-11-15Hakar Qadir GardiNo ratings yet

- Final Health 1-10 01.09.2014Document66 pagesFinal Health 1-10 01.09.2014Jinsen Paul Martin100% (1)

- Compressed Air System Design, Operating and MaintenanceDocument29 pagesCompressed Air System Design, Operating and Maintenanceibrahim1961No ratings yet

- Driving Exam NotesDocument7 pagesDriving Exam Notesreach2ashish5065No ratings yet

- Icl 8069Document6 pagesIcl 8069Ion Mikel Onandia MartinezNo ratings yet

- IPCO IP Release-Agent-spraying-system ProSpray 03 2020 v1.0 LO-RESDocument2 pagesIPCO IP Release-Agent-spraying-system ProSpray 03 2020 v1.0 LO-RESborodichNo ratings yet

- Uhv Unit 4Document25 pagesUhv Unit 4Radha KrishnaNo ratings yet

- XC975 EV 英语译文Document2 pagesXC975 EV 英语译文abangNo ratings yet

- Physics: AssignmentDocument27 pagesPhysics: AssignmentElakkiya Elakkiya0% (1)

- Divya Kit Online All ProductsDocument6 pagesDivya Kit Online All ProductsDivya KitNo ratings yet

- ExamsDocument110 pagesExamsMody XpressNo ratings yet

- Hitachi Mild Hybrid Press ReleaseDocument4 pagesHitachi Mild Hybrid Press ReleaseRafa SilesNo ratings yet

- Test Glo-Qc-Tm-0744Document6 pagesTest Glo-Qc-Tm-0744rx bafnaNo ratings yet

- Fuel Cell Powered Model - Project ReportDocument10 pagesFuel Cell Powered Model - Project ReportShivranjan SangitalayaNo ratings yet

- 2-2 Letter To Sarah BallouDocument4 pages2-2 Letter To Sarah BallouLuis AsteteNo ratings yet

- Aadhaar Enabled Public Distribution System - Aepds: Food and Consumer Protection Department Government of BiharDocument1 pageAadhaar Enabled Public Distribution System - Aepds: Food and Consumer Protection Department Government of BiharAnil SharmaNo ratings yet