Download as pdf or txt

You might also like

- MECN430 Homework 3Document5 pagesMECN430 Homework 3Ramon GondimNo ratings yet

- The Philippine Garments and Textile IndustryDocument5 pagesThe Philippine Garments and Textile IndustryNisco NegrosNo ratings yet

- Amex STMTDocument1 pageAmex STMTMark GalantyNo ratings yet

- Cambodia: Date: GAIN Report NumberDocument15 pagesCambodia: Date: GAIN Report NumberFaran MoonisNo ratings yet

- DGC 20240130 BuyDocument17 pagesDGC 20240130 Buyntdh231198No ratings yet

- Statistics 0001Document12 pagesStatistics 0001Saurav kumarNo ratings yet

- BNI Sekuritas 08102021Document14 pagesBNI Sekuritas 08102021Quartantyo WijanarkoNo ratings yet

- Monthly Report: July Nylon 6 Chip Market ReportDocument6 pagesMonthly Report: July Nylon 6 Chip Market ReportNISHSHANKANo ratings yet

- Wood Pellet Production and Export of Vietnam T7-2023 - ENDocument7 pagesWood Pellet Production and Export of Vietnam T7-2023 - ENGiangNo ratings yet

- Ans To The 1st Part of MID PracticeDocument4 pagesAns To The 1st Part of MID PracticeMahmoud AlfarNo ratings yet

- Table 1: Summary of Australia'S Trade (A)Document4 pagesTable 1: Summary of Australia'S Trade (A)Mã Tố ThanhNo ratings yet

- Trade Statiscs Excel Tables Nov 2021Document157 pagesTrade Statiscs Excel Tables Nov 2021rogerNo ratings yet

- Export Data 2021 NewDocument71 pagesExport Data 2021 NewGautam SharmaNo ratings yet

- Morning Briefing: Afnan Iqbal 30 January 2020Document16 pagesMorning Briefing: Afnan Iqbal 30 January 2020afnaniqbalNo ratings yet

- Least Square Methyl ChlorideDocument11 pagesLeast Square Methyl ChlorideIqbal Muhamad IrfanNo ratings yet

- FMDQ Markets Monthly ReportDocument9 pagesFMDQ Markets Monthly ReportJohnNo ratings yet

- Corporate Performance AnalysisDocument217 pagesCorporate Performance Analysisroy_kohinoorNo ratings yet

- Part 2 Southeast Asia and The Pacific International LinkagesDocument129 pagesPart 2 Southeast Asia and The Pacific International LinkagesErizelle Anne BrunoNo ratings yet

- EC 052 Dt. 14.06.2022 Import of Veg. Oils Nov.21 May 22 - CompressedDocument7 pagesEC 052 Dt. 14.06.2022 Import of Veg. Oils Nov.21 May 22 - CompressedSAMYAK PANDEYNo ratings yet

- BD Cotton and Products Annual - Rome - Greece - GR2023-0001Document8 pagesBD Cotton and Products Annual - Rome - Greece - GR2023-0001Mike JarrodNo ratings yet

- Morning Breifing 30-01-2020Document16 pagesMorning Breifing 30-01-2020afnaniqbalNo ratings yet

- Quarter Reporty SampleDocument10 pagesQuarter Reporty Sampleshamsan dilangalenNo ratings yet

- Vietnam Market Trend Q3 - 2020Document22 pagesVietnam Market Trend Q3 - 2020cosmosmediavnNo ratings yet

- Bmd-Fcpo-Daily-Report - 2021-04-20T103624.301Document2 pagesBmd-Fcpo-Daily-Report - 2021-04-20T103624.301Bruce KingNo ratings yet

- Financial Analysis of Transport and Logistics IndustryDocument13 pagesFinancial Analysis of Transport and Logistics IndustryQamar PashaNo ratings yet

- Adro Mirae 02 Nov 2023 231102 150020Document9 pagesAdro Mirae 02 Nov 2023 231102 150020marcellusdarrenNo ratings yet

- Rain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImproveDocument8 pagesRain Industries: CMP: INR381 TP: INR480 (+26%) Carbon Prices and Margins Continue To ImprovedidwaniasNo ratings yet

- Bhutan Trade Statistics 2021Document534 pagesBhutan Trade Statistics 2021Tandin TshewangNo ratings yet

- Quarterly Bulletin of Statistics - Q1 2017Document6 pagesQuarterly Bulletin of Statistics - Q1 2017BernewsAdminNo ratings yet

- Grain and Feed Annual - Phnom Penh - Cambodia - CB2023-0003Document11 pagesGrain and Feed Annual - Phnom Penh - Cambodia - CB2023-0003dicky muharamNo ratings yet

- Canadian Provinces and Territories by GDPDocument9 pagesCanadian Provinces and Territories by GDPKwami YakobNo ratings yet

- Annual Trends in Area, Production, Consumption, Import, Export and Average Prices of Natural Rubber in IndiaDocument2 pagesAnnual Trends in Area, Production, Consumption, Import, Export and Average Prices of Natural Rubber in IndiaSayantan ChoudhuryNo ratings yet

- FINANCIALSDocument7 pagesFINANCIALSAmmon BelyonNo ratings yet

- Conveyor Belts of TextileDocument25 pagesConveyor Belts of TextileTed Habtu Mamo AsratNo ratings yet

- Statistical Bulletin OF Bangladesh Tea Board: For The Month of February, 2020Document13 pagesStatistical Bulletin OF Bangladesh Tea Board: For The Month of February, 2020Shafin AhmedNo ratings yet

- Https:/esalaryhry Nic in/EmpReport/RptSSRS AspxDocument2 pagesHttps:/esalaryhry Nic in/EmpReport/RptSSRS AspxDharmender MaanNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFAnwaruddin SalehNo ratings yet

- Content Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFDocument107 pagesContent Handbook of Energy and Economic Statistics of Indonesia 2018 Final Edition PDFIreg TraxNo ratings yet

- Imports and Exchange Rates of PakistanDocument6 pagesImports and Exchange Rates of PakistanZaukNo ratings yet

- Topics Impact of Payra Deep Sea Port On Bangladesh Economy: ID BatchDocument9 pagesTopics Impact of Payra Deep Sea Port On Bangladesh Economy: ID BatchRaju RiadNo ratings yet

- Morning Breifing 27-01-2020Document17 pagesMorning Breifing 27-01-2020afnaniqbalNo ratings yet

- Managerial Economics - Trend Analysis of Petroleum ProductsDocument5 pagesManagerial Economics - Trend Analysis of Petroleum ProductsTaha SuhailNo ratings yet

- Data BPS NitroselulosaDocument36 pagesData BPS Nitroselulosawilly dwinovNo ratings yet

- EC-083 Dt. 12.07.2022 - Import of Veg. Oils - Nov.'21 - June '22Document7 pagesEC-083 Dt. 12.07.2022 - Import of Veg. Oils - Nov.'21 - June '22SAMYAK PANDEYNo ratings yet

- GTA Edition - E-Paper (04 August 2021)Document6 pagesGTA Edition - E-Paper (04 August 2021)Rahul SoodNo ratings yet

- Monthly Report: July AA & Nylon 66 Chip Market ReportDocument5 pagesMonthly Report: July AA & Nylon 66 Chip Market ReportNISHSHANKANo ratings yet

- Business Name Patatasty Currency Symbol P Year End Month December Reporting Year 2020 Year End Reporting Date 29 February 2020Document35 pagesBusiness Name Patatasty Currency Symbol P Year End Month December Reporting Year 2020 Year End Reporting Date 29 February 2020Raschelle MayugbaNo ratings yet

- Issue No 227 February 2018Document34 pagesIssue No 227 February 2018Luna ChenNo ratings yet

- Quarterly Bulletin of Statistics - Q4 2017Document6 pagesQuarterly Bulletin of Statistics - Q4 2017BernewsAdminNo ratings yet

- Group 9 - Section A - MEP Assignment2Document3 pagesGroup 9 - Section A - MEP Assignment2Sudhir PawarNo ratings yet

- 05 - Fpa-Fertilizer-Prices-And-Inventory PPT May 18, 2022Document19 pages05 - Fpa-Fertilizer-Prices-And-Inventory PPT May 18, 2022Ruby CalesterioNo ratings yet

- Assignment 2 MEPDocument3 pagesAssignment 2 MEPSuraj ChaudharyNo ratings yet

- Budget RIZZA PIZZA - Luan GonzagaDocument15 pagesBudget RIZZA PIZZA - Luan GonzagaLuan Allama GonzagaNo ratings yet

- BizFin ICA2 ReportDocument11 pagesBizFin ICA2 Reporteval_2No ratings yet

- Equity Research: Company UpdateDocument6 pagesEquity Research: Company UpdateyolandaNo ratings yet

- CA TullyDocument11 pagesCA Tullychimiwangchuk1511No ratings yet

- 09ComInt 202210 ENDocument20 pages09ComInt 202210 ENRNo ratings yet

- Pak-Japan RelationDocument10 pagesPak-Japan RelationhaseebNo ratings yet

- JSW Steel LTD PDFDocument10 pagesJSW Steel LTD PDFTanzy SNo ratings yet

- Departement 1 Average & Departement 2 Average: NOTE!!Document28 pagesDepartement 1 Average & Departement 2 Average: NOTE!!17HARISA SETYA HANDININo ratings yet

- Oilseeds and Products Annual - Jakarta - Indonesia - ID2022-0007Document23 pagesOilseeds and Products Annual - Jakarta - Indonesia - ID2022-0007GabrielNo ratings yet

- The Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaFrom EverandThe Increasing Importance of Migrant Remittances from the Russian Federation to Central AsiaNo ratings yet

- Engineering Graphene Flakes For Wearable Textile Sensors Via Highly Scalable and Ultrafast Yarn Dyeing TechniqueDocument12 pagesEngineering Graphene Flakes For Wearable Textile Sensors Via Highly Scalable and Ultrafast Yarn Dyeing TechniqueNISHSHANKANo ratings yet

- Monthly Report: July Nylon 6 Chip Market ReportDocument6 pagesMonthly Report: July Nylon 6 Chip Market ReportNISHSHANKANo ratings yet

- China Spandex Industry Operation Report Jul 16-31, 2021: PriceDocument3 pagesChina Spandex Industry Operation Report Jul 16-31, 2021: PriceNISHSHANKANo ratings yet

- Monthly Report: June Nylon Filament Yarn Market ReportDocument5 pagesMonthly Report: June Nylon Filament Yarn Market ReportNISHSHANKANo ratings yet

- China Nylon Industry Operation Report: Crude Oil & Benzene 2-Aug 13-Aug ChangeDocument4 pagesChina Nylon Industry Operation Report: Crude Oil & Benzene 2-Aug 13-Aug ChangeNISHSHANKANo ratings yet

- Monthly Report: July AA & Nylon 66 Chip Market ReportDocument5 pagesMonthly Report: July AA & Nylon 66 Chip Market ReportNISHSHANKANo ratings yet

- Annual Report - 2018 2019 PDFDocument300 pagesAnnual Report - 2018 2019 PDFShekhar BanisettiNo ratings yet

- A Review of Dynamic Capabilities, Innovation Capabilities, Entrepreneurial Capabilities and Their ConsequencesDocument10 pagesA Review of Dynamic Capabilities, Innovation Capabilities, Entrepreneurial Capabilities and Their ConsequencessukorotoNo ratings yet

- Agency ProblemDocument11 pagesAgency Problemreigh paulusNo ratings yet

- Cost Benefit Analysis Is Done To Determine How WellDocument5 pagesCost Benefit Analysis Is Done To Determine How WellShaikh JahirNo ratings yet

- Lecture 4 - Project Management IDocument3 pagesLecture 4 - Project Management IcliffNo ratings yet

- Carta de La Junta de Supervisión FiscalDocument2 pagesCarta de La Junta de Supervisión FiscalEl Nuevo DíaNo ratings yet

- Polash Depo Mengecat USM Pack 1Document2 pagesPolash Depo Mengecat USM Pack 1Arifa HasnaNo ratings yet

- File Annual 5e1bec2ecdb1aDocument203 pagesFile Annual 5e1bec2ecdb1aTera Nova Puspa WijayantiNo ratings yet

- TTC Package 3D2N Istanbul Bursa Winter 2023Document1 pageTTC Package 3D2N Istanbul Bursa Winter 2023Meiryza AstutiNo ratings yet

- Tempalte e BankingDocument12 pagesTempalte e Bankingcorneles tuanakottaNo ratings yet

- Operations Management MCQs - Types of Production - MCQs ClubDocument7 pagesOperations Management MCQs - Types of Production - MCQs ClubPranoy SarkarNo ratings yet

- ESCAP Sustainable Business NetworkDocument15 pagesESCAP Sustainable Business Networkkhampa Pema DewaNo ratings yet

- Ts Grewal Solutions For Class 11 Accountancy Chapter 3Document10 pagesTs Grewal Solutions For Class 11 Accountancy Chapter 3Karan SharmaNo ratings yet

- Hong KongDocument12 pagesHong KongThảo Nguyễn PhươngNo ratings yet

- Data Tiket Dan Hotel Share H-1Document4 pagesData Tiket Dan Hotel Share H-1Ahmad NursalimNo ratings yet

- Legal Services Payment Plan AgreementDocument5 pagesLegal Services Payment Plan AgreementMaricar TelanNo ratings yet

- Batteries Company, Oil and Gas Company, Manufacturing Company DUBAIDocument28 pagesBatteries Company, Oil and Gas Company, Manufacturing Company DUBAIPacific HRNo ratings yet

- UNIT 1-IRDA's Guidelines - Both Pre-Sale and Post-SaleDocument26 pagesUNIT 1-IRDA's Guidelines - Both Pre-Sale and Post-SaleGame WinnerNo ratings yet

- CH 07Document100 pagesCH 07SamiNaserNo ratings yet

- Cash Flow Statement Example1Document3 pagesCash Flow Statement Example1ScribdJrNo ratings yet

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocument2 pagesBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total Amountamandeep kansalNo ratings yet

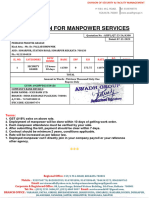

- Quotation For Manpower Services: Sl. No. Categories Duty Hours Basic EPF ESI Rate S.C. @10% TotalDocument1 pageQuotation For Manpower Services: Sl. No. Categories Duty Hours Basic EPF ESI Rate S.C. @10% TotalAwadh GroupNo ratings yet

- The Composable Commerce Cheat Sheet: How To Sell The Commerce Solution of Your Dreams To Your Business PeersDocument4 pagesThe Composable Commerce Cheat Sheet: How To Sell The Commerce Solution of Your Dreams To Your Business PeersSaurabh PantNo ratings yet

- A211 MC4 MFRS108 Mfrs110-StudentDocument6 pagesA211 MC4 MFRS108 Mfrs110-StudentGui Xue ChingNo ratings yet

- Analisis Negosiasi Bisnis Pada PT Allegrindo NusantaraDocument5 pagesAnalisis Negosiasi Bisnis Pada PT Allegrindo Nusantaramuhammad akmalulmazaya ChoiriNo ratings yet

- On Line Petty Cash Fund and Undeposited Collections LGlassDocument2 pagesOn Line Petty Cash Fund and Undeposited Collections LGlassM MNo ratings yet

- Business Tax ManagementDocument765 pagesBusiness Tax Managementmuralisk06No ratings yet

- 1995 Jan07 Subject-1995Document110 pages1995 Jan07 Subject-1995anonymous284.1.11No ratings yet