Download as pdf or txt

You might also like

- Van Hoisington Letter, Q3 2011Document5 pagesVan Hoisington Letter, Q3 2011Elliott WaveNo ratings yet

- HIM2018Q4NPDocument6 pagesHIM2018Q4NPPuru SaxenaNo ratings yet

- Lacy Hunt - Hoisington - Quartely Review Q1 2015Document5 pagesLacy Hunt - Hoisington - Quartely Review Q1 2015TREND_7425No ratings yet

- Hoisington Q4Document6 pagesHoisington Q4ZerohedgeNo ratings yet

- Global Forecast: UpdateDocument6 pagesGlobal Forecast: Updatebkginting6300No ratings yet

- IMF World Economic and Financial Surveys Consolidated Multilateral Surveillance Report Sept 2011Document12 pagesIMF World Economic and Financial Surveys Consolidated Multilateral Surveillance Report Sept 2011babstar999No ratings yet

- RCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013Document7 pagesRCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013RCS_CFANo ratings yet

- Mizuho EconomicOutlook 17.5.29Document3 pagesMizuho EconomicOutlook 17.5.29abraNo ratings yet

- CIO CMO - The Pressure's On Emerging Market Central BanksDocument9 pagesCIO CMO - The Pressure's On Emerging Market Central BanksRCS_CFANo ratings yet

- CIO CMO - Approving Fiscal BoostersDocument10 pagesCIO CMO - Approving Fiscal BoostersRCS_CFANo ratings yet

- CIO Weekly Letter - Mexico The Global PiñataDocument4 pagesCIO Weekly Letter - Mexico The Global PiñataRCS_CFANo ratings yet

- Economic Insights 25 02 13Document16 pagesEconomic Insights 25 02 13vikashpunglia@rediffmail.comNo ratings yet

- Quarterly Market Review: Second Quarter 2016Document15 pagesQuarterly Market Review: Second Quarter 2016Anonymous Ht0MIJNo ratings yet

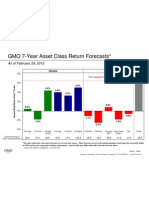

- GMO 7-Year Forecast - Feb '12Document1 pageGMO 7-Year Forecast - Feb '12Douglas RattrayNo ratings yet

- GMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamDocument11 pagesGMO Quarterly Letter-My Sister's Pension Assets 0412 GMO-GranthamMarko AleksicNo ratings yet

- Capital Flow AnalysisDocument8 pagesCapital Flow AnalysisNak-Gyun KimNo ratings yet

- 7YrForecasts 111Document1 page7YrForecasts 111maxiannozziNo ratings yet

- 7-Year Asset Class Real Return Forecasts : As of May 31, 2019Document1 page7-Year Asset Class Real Return Forecasts : As of May 31, 2019Tim TruaxNo ratings yet

- Understanding Vietnam - A Look Beyond The Facts and PDFDocument24 pagesUnderstanding Vietnam - A Look Beyond The Facts and PDFDawood GacayanNo ratings yet

- Euro Themes - SpainDocument22 pagesEuro Themes - SpainGuy DviriNo ratings yet

- 7YrForecasts 813Document1 page7YrForecasts 813CanadianValueNo ratings yet

- Gic WeeklyDocument12 pagesGic WeeklycampiyyyyoNo ratings yet

- Global Markets Chart Book: High-Grade Bond Yields Plunge To Record LowsDocument12 pagesGlobal Markets Chart Book: High-Grade Bond Yields Plunge To Record LowslosdiabloNo ratings yet

- Yearly Outlook 2011Document36 pagesYearly Outlook 2011Trading FloorNo ratings yet

- GMO 7 Year Asset Class Forecast Apr 14Document1 pageGMO 7 Year Asset Class Forecast Apr 14CanadianValueNo ratings yet

- The End of An Era: Uarterly EtterDocument10 pagesThe End of An Era: Uarterly EtterthickskinNo ratings yet

- Grantham Quarterly Dec 2011Document4 pagesGrantham Quarterly Dec 2011careyescapitalNo ratings yet

- JPM Global Data Watch Se 2012-09-21 946463Document88 pagesJPM Global Data Watch Se 2012-09-21 946463Siddhartha SinghNo ratings yet

- How Urban Planners Caused The Housing Bubble, Cato Policy Analysis No. 646Document28 pagesHow Urban Planners Caused The Housing Bubble, Cato Policy Analysis No. 646Cato InstituteNo ratings yet

- Hayman July 07Document5 pagesHayman July 07grumpyfeckerNo ratings yet

- Charlie McElligott Transcript Nov 14th - 2019Document16 pagesCharlie McElligott Transcript Nov 14th - 2019ZerohedgeNo ratings yet

- Sustainability of Govt DebtDocument8 pagesSustainability of Govt DebtSpencer RascoffNo ratings yet

- Second Quarter 2010 GTAA Fixed IncomeDocument32 pagesSecond Quarter 2010 GTAA Fixed IncomeZerohedge100% (1)

- Synopsis On Subprime Crisis and Its Impact On Indian EconomyDocument2 pagesSynopsis On Subprime Crisis and Its Impact On Indian EconomySadasivuni007No ratings yet

- Second Quarter 2010 GTAA EquitiesDocument68 pagesSecond Quarter 2010 GTAA EquitiesZerohedge100% (1)

- Across - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFDocument60 pagesAcross - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFQuantDev-MNo ratings yet

- 16.02 RWC GIAA PresentationDocument35 pages16.02 RWC GIAA PresentationGIAANo ratings yet

- Grantham 4-25-11 Letter Part 1Document19 pagesGrantham 4-25-11 Letter Part 1wompyfratNo ratings yet

- GMO Grantham July 09Document6 pagesGMO Grantham July 09rodmorleyNo ratings yet

- Treasury Outlook MarDocument6 pagesTreasury Outlook Marelise_stefanikNo ratings yet

- Global Macro Trends and Strategies - BloombergDocument70 pagesGlobal Macro Trends and Strategies - Bloombergdrewmx100% (1)

- Aig Best of Bernstein SlidesDocument50 pagesAig Best of Bernstein SlidesYA2301100% (1)

- Economics Docs 2022 184258.ashxDocument65 pagesEconomics Docs 2022 184258.ashxTshepo ThaisiNo ratings yet

- Gundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedDocument73 pagesGundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedZerohedge100% (1)

- Bar Cap 3Document11 pagesBar Cap 3Aquila99999No ratings yet

- The GIC Weekly Update November 2015Document12 pagesThe GIC Weekly Update November 2015John MathiasNo ratings yet

- Return On EquityDocument6 pagesReturn On EquitySharathNo ratings yet

- What Are 'Narrow' and 'Broad' Money?Document2 pagesWhat Are 'Narrow' and 'Broad' Money?saurabhshineNo ratings yet

- RCSI Presentation - China's Threats: Deflation & Slowing GrowthDocument10 pagesRCSI Presentation - China's Threats: Deflation & Slowing GrowthRCS_CFANo ratings yet

- Answers To 10 Common Questions On EMU BreakupDocument11 pagesAnswers To 10 Common Questions On EMU BreakupzeleneyeNo ratings yet

- The GIC WeeklyDocument12 pagesThe GIC WeeklyedgarmerchanNo ratings yet

- ASEAN Corporate Governance Scorecard Country Reports and Assessments 2019From EverandASEAN Corporate Governance Scorecard Country Reports and Assessments 2019No ratings yet

- India Economic Update: September, 2011Document17 pagesIndia Economic Update: September, 2011Rahul KaushikNo ratings yet

- OverviewDocument9 pagesOverviewsaeed abbasiNo ratings yet

- Quick Start Report - 2011-12 - Final 11.5.10Document50 pagesQuick Start Report - 2011-12 - Final 11.5.10New York SenateNo ratings yet

- Monetary Policy Report To The Congress: Board of Governors of The Federal Reserve SystemDocument56 pagesMonetary Policy Report To The Congress: Board of Governors of The Federal Reserve SystemLuis Riestra Delgado100% (1)

- The Broyhill Letter - Part Duex (Q2-11)Document5 pagesThe Broyhill Letter - Part Duex (Q2-11)Broyhill Asset ManagementNo ratings yet

- BNP Paribas The Financial Crisis and Household Savings Behaviour in France 11102010Document12 pagesBNP Paribas The Financial Crisis and Household Savings Behaviour in France 11102010YUGANDHAR016577No ratings yet

- Monetary Policy of Pakistan: Submitted To: Mirza Aqeel BaigDocument9 pagesMonetary Policy of Pakistan: Submitted To: Mirza Aqeel BaigAli AmjadNo ratings yet

- US Economy 2010 Q4 - MRDocument11 pagesUS Economy 2010 Q4 - MRMartin RosenburghNo ratings yet

- A Summary of Opinion Surveys On Wind PowerDocument11 pagesA Summary of Opinion Surveys On Wind PowerHonza MynarNo ratings yet

- Relative ValuationDocument100 pagesRelative ValuationHonza MynarNo ratings yet

- Discounted Cash Flow Valuation SlidesDocument260 pagesDiscounted Cash Flow Valuation Slidesgambino03100% (2)

- European Austerity SocGenDocument29 pagesEuropean Austerity SocGenHonza MynarNo ratings yet