Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

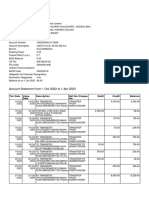

- Account Statement From 1 Oct 2022 To 1 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 Oct 2022 To 1 Apr 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceAman JaiswalNo ratings yet

- Midterm TestDocument2 pagesMidterm TestHailee HayesNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Calling DataDocument1,961 pagesCalling DataShubham TyagiNo ratings yet

- Adoption of Big Data For Last Mile Optimization: The Case of DHLDocument2 pagesAdoption of Big Data For Last Mile Optimization: The Case of DHLHailee HayesNo ratings yet

- Brand EquityDocument6 pagesBrand EquityHailee HayesNo ratings yet

- Accounting System in SpainDocument5 pagesAccounting System in SpainHailee HayesNo ratings yet

- Questions 13. What Is The Most Important Use of The Statement of The International Investment Position of A Nation?Document2 pagesQuestions 13. What Is The Most Important Use of The Statement of The International Investment Position of A Nation?Hailee HayesNo ratings yet

- Table 2. U.S. International Trade in Goods-: ContinuesDocument5 pagesTable 2. U.S. International Trade in Goods-: ContinuesHailee HayesNo ratings yet

- Analysis of Corporate Strategy of ZaraDocument14 pagesAnalysis of Corporate Strategy of ZaraHailee HayesNo ratings yet

- Of Which: Seasonal Adjustment DiscrepancyDocument6 pagesOf Which: Seasonal Adjustment DiscrepancyHailee HayesNo ratings yet

- Homework: I. Questions For ReviewDocument16 pagesHomework: I. Questions For ReviewHailee HayesNo ratings yet

- Homework: I. Questions For ReviewDocument12 pagesHomework: I. Questions For ReviewHailee HayesNo ratings yet

- Statement of AccountDocument5 pagesStatement of AccountJustin DyerNo ratings yet

- Screenshot 2024-04-10 at 1.18.02 PMDocument8 pagesScreenshot 2024-04-10 at 1.18.02 PMfaezahmed014No ratings yet

- Notice BoardDocument33 pagesNotice BoardEnduva SrinivasNo ratings yet

- Joshi 2021Document10 pagesJoshi 2021askdjnasdkNo ratings yet

- Costco Wholesale Corporation Module 3Document6 pagesCostco Wholesale Corporation Module 3api-564978867No ratings yet

- Narrative On Financial AnalysisDocument28 pagesNarrative On Financial AnalysisJeremiah GarciaNo ratings yet

- Module 3 Buying and Selling For Students Copy 1Document35 pagesModule 3 Buying and Selling For Students Copy 1Alexander GuevarraNo ratings yet

- The Characteristics of The Labor Market Are As FollowsDocument20 pagesThe Characteristics of The Labor Market Are As FollowsPriti KshirsagarNo ratings yet

- CBBE ModelDocument2 pagesCBBE Modelkshitiz32450% (2)

- ECO 2115 Agricultural Production and Management 2021Document3 pagesECO 2115 Agricultural Production and Management 2021Waidembe YusufuNo ratings yet

- Reporting of Loan Agreement Details Under Foreign Exchange Management Act, 1999Document7 pagesReporting of Loan Agreement Details Under Foreign Exchange Management Act, 1999Pankaj Kumar SaoNo ratings yet

- CHAPTER 18 - THE NEGOTIABLE INSTRUMENTS - ACT, 1881 Summary NotesDocument32 pagesCHAPTER 18 - THE NEGOTIABLE INSTRUMENTS - ACT, 1881 Summary Notesshivam kumarNo ratings yet

- Tutorial 1 by HenryDocument21 pagesTutorial 1 by HenryChris WongNo ratings yet

- TPF OrderDocument2 pagesTPF OrderbeobhavanischoolsNo ratings yet

- Joint VentureDocument6 pagesJoint VentureAditya RajNo ratings yet

- SMK Convent Teluk Intan 7 Jan 2023 - Proforma Invoice - BuffetDocument2 pagesSMK Convent Teluk Intan 7 Jan 2023 - Proforma Invoice - BuffetnaimahNo ratings yet

- Part 3 - American MVNO 2015 - ETC - Eligible Telecommunication Carrier (Life Line Program) - Christian Gomez - LinkedInDocument6 pagesPart 3 - American MVNO 2015 - ETC - Eligible Telecommunication Carrier (Life Line Program) - Christian Gomez - LinkedIndwiaryantaNo ratings yet

- Identify The Controllable and Uncontrollable Elements That Starbucks Has Encountered in Entering Global MarketsDocument3 pagesIdentify The Controllable and Uncontrollable Elements That Starbucks Has Encountered in Entering Global MarketsSobia Zafar Sobia ZafarNo ratings yet

- Production Costs Calculation Model in Crushing & ScreeningDocument223 pagesProduction Costs Calculation Model in Crushing & ScreeningOktay GülenNo ratings yet

- Transfer PricingDocument15 pagesTransfer PricingJulie Marie Anne LUBINo ratings yet

- Goldman Sachs Hyrdrogen GasDocument14 pagesGoldman Sachs Hyrdrogen GasVivek AgNo ratings yet

- Funds Transfer Form - For Wholesale Banking Customers Only: Debit Account DetailsDocument1 pageFunds Transfer Form - For Wholesale Banking Customers Only: Debit Account Detailsdon EzeNo ratings yet

- 5 Questions and Case Studies For Seminars EngDocument6 pages5 Questions and Case Studies For Seminars EngHuỳnh Quốc TuấnNo ratings yet

- Business Model Final ProjectDocument12 pagesBusiness Model Final ProjectAyesha KhalidNo ratings yet

- Commercials: Sr. No. TXN Mode Services Type Vle ShareDocument2 pagesCommercials: Sr. No. TXN Mode Services Type Vle ShareSHASHI KANTNo ratings yet

- Current & Saving Account Statement: Vijaya B S/O Belli Karadigodu Siddapur SiddapurDocument13 pagesCurrent & Saving Account Statement: Vijaya B S/O Belli Karadigodu Siddapur SiddapurWipro Foundation KARNo ratings yet

- Support Services Calculation - Feb.23.xDocument91 pagesSupport Services Calculation - Feb.23.xThanh TuyenNo ratings yet

- 8904 - Contract of PartnershipDocument39 pages8904 - Contract of PartnershipElaine Joyce GarciaNo ratings yet