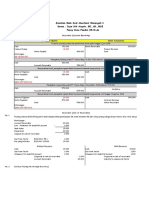

A) Year 0 Year 1 Year 2 Year 3

A) Year 0 Year 1 Year 2 Year 3

You might also like

- Solution Manual For Investment Science by David LuenbergerDocument94 pagesSolution Manual For Investment Science by David Luenbergerkoenajax96% (28)

- DS White-Papers Getting Started With Business Logic 3DEXPERIENCE R2017x V1Document52 pagesDS White-Papers Getting Started With Business Logic 3DEXPERIENCE R2017x V1AlexandreNo ratings yet

- Report Based On TransmissionDocument9 pagesReport Based On TransmissionBARUN SINGH100% (1)

- Bond Price 100,000Document22 pagesBond Price 100,000HAMMADHRNo ratings yet

- financial đề mẫuDocument6 pagesfinancial đề mẫuNgọc Minhh NgọcNo ratings yet

- Chapter 2Document14 pagesChapter 2Kumar ShivamNo ratings yet

- CFIN 3rd Edition by Besley Brigham ISBN Solution ManualDocument6 pagesCFIN 3rd Edition by Besley Brigham ISBN Solution Manualrussell100% (25)

- Answer Keys - Time Value of MoneyDocument22 pagesAnswer Keys - Time Value of MoneyrhlvajpayeeNo ratings yet

- MIDS CF Solutions MergedDocument43 pagesMIDS CF Solutions Mergedsohaib.uniqueNo ratings yet

- Cfin 2 2nd Edition Besley Test BankDocument5 pagesCfin 2 2nd Edition Besley Test BankBenjaminTaylorcbtgs100% (18)

- 13 - Chapter4 - Capital Budgeting - Part2Document9 pages13 - Chapter4 - Capital Budgeting - Part2com01156499073No ratings yet

- Chapter-3-Answers To Practice QuestionsDocument4 pagesChapter-3-Answers To Practice QuestionsqadirqadilNo ratings yet

- FM Assaignment Second SemisterDocument9 pagesFM Assaignment Second SemisterMotuma Abebe100% (1)

- Cfin 3 3rd Edition Besley Solutions ManualDocument5 pagesCfin 3 3rd Edition Besley Solutions Manualjenniferdrakenxkzgroiyt100% (10)

- Chapter 6 - Answer KeyDocument8 pagesChapter 6 - Answer KeyĐặng Thanh ThuỷNo ratings yet

- Budgeting, Capital Structure, and Working Capital ManagementDocument11 pagesBudgeting, Capital Structure, and Working Capital Managementritu paudelNo ratings yet

- IPF Assignment 4Document12 pagesIPF Assignment 4Nitesh MehlaNo ratings yet

- Chapter 02 - How To Calculate Present ValuesDocument15 pagesChapter 02 - How To Calculate Present ValuesShoaibTahirNo ratings yet

- Cfin 2 2nd Edition Besley Test BankDocument35 pagesCfin 2 2nd Edition Besley Test Bankghebre.comatula.75ew100% (23)

- Lecture Notes Topic 4 Part 2Document34 pagesLecture Notes Topic 4 Part 2sir bookkeeperNo ratings yet

- Corporate FinanceDocument11 pagesCorporate FinanceShamsul HaqimNo ratings yet

- Assignment 4 - Contemporary Engineering BookDocument9 pagesAssignment 4 - Contemporary Engineering BookDhiraj NayakNo ratings yet

- Chapter 2Document3 pagesChapter 2Ikramul HaqueNo ratings yet

- Managerial Economics (Chapter 14)Document28 pagesManagerial Economics (Chapter 14)api-3703724100% (1)

- Si7 - Tarquin (1) 1 9Document9 pagesSi7 - Tarquin (1) 1 9AlvarezMartinNo ratings yet

- Chapter 2 PQ FMDocument5 pagesChapter 2 PQ FMRohan SharmaNo ratings yet

- EE - Assignment Chapter 9-10 SolutionDocument11 pagesEE - Assignment Chapter 9-10 SolutionXuân ThànhNo ratings yet

- Busn 233 CH 08 EeeeDocument102 pagesBusn 233 CH 08 EeeeDavid IoanaNo ratings yet

- CFM Session 8Document7 pagesCFM Session 8khanhnguyenfgoNo ratings yet

- Dwnload Full Cfin 3 3rd Edition Besley Solutions Manual PDFDocument35 pagesDwnload Full Cfin 3 3rd Edition Besley Solutions Manual PDFbrandihansenjoqll2100% (17)

- Tla 9. Basic of Capital BudgetingDocument4 pagesTla 9. Basic of Capital BudgetingNINIO B. MANIALAGNo ratings yet

- Solutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDocument12 pagesSolutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment Decisionshung TranNo ratings yet

- Chapter 6 Answer Key (1 15)Document15 pagesChapter 6 Answer Key (1 15)Desrifta FaheraNo ratings yet

- Solution Assignment Chapter 9 10 1Document14 pagesSolution Assignment Chapter 9 10 1Huynh Ng Quynh NhuNo ratings yet

- Solutions Manual Corporate Fiance Ross W-75%Document10 pagesSolutions Manual Corporate Fiance Ross W-75%Desrifta FaheraNo ratings yet

- Solutions To Selected End-Of-Chapter 6 Problem Solving QuestionsDocument9 pagesSolutions To Selected End-Of-Chapter 6 Problem Solving QuestionsVân Anh Đỗ LêNo ratings yet

- Mock Test SolutionsDocument11 pagesMock Test SolutionsMyraNo ratings yet

- Dwnload Full Cfin 2 2nd Edition Besley Test Bank PDFDocument35 pagesDwnload Full Cfin 2 2nd Edition Besley Test Bank PDFbrandihansenjoqll2100% (17)

- FFM 9 Im 12Document31 pagesFFM 9 Im 12Mariel CorderoNo ratings yet

- Sesi 11 BDocument22 pagesSesi 11 BTata JanetaNo ratings yet

- MTP Soln 1Document14 pagesMTP Soln 1Anonymous 8wg4eowIdzNo ratings yet

- Tutorial 2 SolutionsDocument4 pagesTutorial 2 SolutionsSadia R ChowdhuryNo ratings yet

- Chapter #1 Solutions - Engineering Economy, 7 TH Editionleland Blank and Anthony TarquinDocument9 pagesChapter #1 Solutions - Engineering Economy, 7 TH Editionleland Blank and Anthony TarquinMusa'b100% (10)

- Solutions Review Problems Chap002Document4 pagesSolutions Review Problems Chap002andreaskarayian8972No ratings yet

- 4.01% Is The 1-Year Spot RateDocument6 pages4.01% Is The 1-Year Spot RatePaulo TorresNo ratings yet

- Chapter 02 - How To Calculate Present ValuesDocument14 pagesChapter 02 - How To Calculate Present Valuesdev4c-1No ratings yet

- Chiều t4 - Nhóm 4 - Chương 6Document15 pagesChiều t4 - Nhóm 4 - Chương 6Khánh QuỳnhNo ratings yet

- Lecture 8: Rate of Return Analysis: Instructional Material ForDocument20 pagesLecture 8: Rate of Return Analysis: Instructional Material ForAziezah PalintaNo ratings yet

- Engineering Economy Review III 2010Document4 pagesEngineering Economy Review III 2010Ma Ella Mae LogronioNo ratings yet

- Chapter 11 Exercises and Problems Exercise 11-2: 1. Straight-LineDocument23 pagesChapter 11 Exercises and Problems Exercise 11-2: 1. Straight-LineHazel Rose CabezasNo ratings yet

- Exercises: 1) Acme Borrowed $100,000 From A Local Bank, Which Charges Them An Interest Rate of 7% PerDocument4 pagesExercises: 1) Acme Borrowed $100,000 From A Local Bank, Which Charges Them An Interest Rate of 7% PerIslam MomtazNo ratings yet

- The Basics of Capital Budgeting: Solutions To End-Of-Chapter ProblemsDocument9 pagesThe Basics of Capital Budgeting: Solutions To End-Of-Chapter ProblemsTayeba AnwarNo ratings yet

- 3815capital Budgeting TechniqueDocument51 pages3815capital Budgeting TechniqueMUHMMAD ARSALAN 13728No ratings yet

- Group Assignment 2Document6 pagesGroup Assignment 2Tường ĐứcNo ratings yet

- Lecture-TIME VALUE OF MONEYDocument91 pagesLecture-TIME VALUE OF MONEYCalvin GadiweNo ratings yet

- A2 ADM Fall 2021 With SolutionDocument2 pagesA2 ADM Fall 2021 With SolutionJamal AnsariNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Manuel C. Espiritu, JR., Et Al. vs. Petron Corp., Et Al.Document6 pagesManuel C. Espiritu, JR., Et Al. vs. Petron Corp., Et Al.BERNADETTE SONo ratings yet

- IAS 1-Presenation of Financial StatementsDocument42 pagesIAS 1-Presenation of Financial StatementsTinoManhangaNo ratings yet

- Invitation For Pre Qualification at Michael Okpara University of Agriculture, Umudike SEPT2012Document4 pagesInvitation For Pre Qualification at Michael Okpara University of Agriculture, Umudike SEPT2012edmund44No ratings yet

- Level 2 - Core Competency FrameworkDocument14 pagesLevel 2 - Core Competency FrameworkbitatfatehNo ratings yet

- Effect of Website Quality On Customer Satisfaction and Purchase Intention in Online Travel Ticket Booking WebsitesDocument6 pagesEffect of Website Quality On Customer Satisfaction and Purchase Intention in Online Travel Ticket Booking Websiteslobna qassemNo ratings yet

- Chapter 3 Cost Accounting CycleDocument11 pagesChapter 3 Cost Accounting CycleSteffany RoqueNo ratings yet

- Translation Exposure Part 1Document31 pagesTranslation Exposure Part 1Magzoub MohaNo ratings yet

- Unit Converter: All in One: Ropani System Bigha System Square Feet Square MeterDocument3 pagesUnit Converter: All in One: Ropani System Bigha System Square Feet Square Meterपोखराको घरNo ratings yet

- The Direction of Fashion Change 1Document19 pagesThe Direction of Fashion Change 1Ratul HasanNo ratings yet

- Bolt™ Lithium Max Professional 2023F - 2 in 1 Stick Vacuum Cleaner BISSELL AustraliaDocument1 pageBolt™ Lithium Max Professional 2023F - 2 in 1 Stick Vacuum Cleaner BISSELL Australialin.odNo ratings yet

- The Seeding Company CEDE TRUST Owned by DTCDocument14 pagesThe Seeding Company CEDE TRUST Owned by DTCRoosevelt Kyle100% (2)

- Executive Summary: Changi AirportDocument18 pagesExecutive Summary: Changi AirportAnil AbduNo ratings yet

- Marketing Plan For Wildcraft Bags: Piyush Kariya 31 Prachi Jain 32 Prajakta Lakade 33 Pushpak Parab 34 Rahul Punjabi 35Document8 pagesMarketing Plan For Wildcraft Bags: Piyush Kariya 31 Prachi Jain 32 Prajakta Lakade 33 Pushpak Parab 34 Rahul Punjabi 35Rahul punjabiNo ratings yet

- Jawaban Soal, Akuntansi Menengah 1Document7 pagesJawaban Soal, Akuntansi Menengah 1Mira OktaviaNo ratings yet

- Marketing Test Bank Chap 10Document53 pagesMarketing Test Bank Chap 10Ta Thi Minh ChauNo ratings yet

- NestleDocument12 pagesNestleParadoxNo ratings yet

- Semua Online Assesment Mira Sem 4Document6 pagesSemua Online Assesment Mira Sem 4Hamierul MohamadNo ratings yet

- Holiday Homework - Worksheet Section 1Document2 pagesHoliday Homework - Worksheet Section 1Anavi KhoslaNo ratings yet

- Greek Gods of Aesthetics Phone Case - Etsy GuatemalaDocument1 pageGreek Gods of Aesthetics Phone Case - Etsy GuatemalaLucia DehesaNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- MTR Foods: Presentation TemplateDocument11 pagesMTR Foods: Presentation Template727821TPMB109 MANUKIRAN S.No ratings yet

- Creative ProcessDocument17 pagesCreative ProcessAlizan MaryNo ratings yet

- Public PolicyDocument11 pagesPublic PolicyssebandekejacksonNo ratings yet

- A ProjectDocument75 pagesA ProjectSameer KNo ratings yet

- Sekarningsih, Dkk. (2020)Document7 pagesSekarningsih, Dkk. (2020)iwang saudjiNo ratings yet

- Inflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyDocument34 pagesInflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyRazvan Catalin CostinNo ratings yet

- Voice of CustomerDocument2 pagesVoice of CustomerShivamNo ratings yet

- Organisational BehaviourDocument12 pagesOrganisational BehaviourMachineni ManaswiniNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Solution Manual For Investment Science by David LuenbergerDocument94 pagesSolution Manual For Investment Science by David Luenbergerkoenajax96% (28)

- DS White-Papers Getting Started With Business Logic 3DEXPERIENCE R2017x V1Document52 pagesDS White-Papers Getting Started With Business Logic 3DEXPERIENCE R2017x V1AlexandreNo ratings yet

- Report Based On TransmissionDocument9 pagesReport Based On TransmissionBARUN SINGH100% (1)

- Bond Price 100,000Document22 pagesBond Price 100,000HAMMADHRNo ratings yet

- financial đề mẫuDocument6 pagesfinancial đề mẫuNgọc Minhh NgọcNo ratings yet

- Chapter 2Document14 pagesChapter 2Kumar ShivamNo ratings yet

- CFIN 3rd Edition by Besley Brigham ISBN Solution ManualDocument6 pagesCFIN 3rd Edition by Besley Brigham ISBN Solution Manualrussell100% (25)

- Answer Keys - Time Value of MoneyDocument22 pagesAnswer Keys - Time Value of MoneyrhlvajpayeeNo ratings yet

- MIDS CF Solutions MergedDocument43 pagesMIDS CF Solutions Mergedsohaib.uniqueNo ratings yet

- Cfin 2 2nd Edition Besley Test BankDocument5 pagesCfin 2 2nd Edition Besley Test BankBenjaminTaylorcbtgs100% (18)

- 13 - Chapter4 - Capital Budgeting - Part2Document9 pages13 - Chapter4 - Capital Budgeting - Part2com01156499073No ratings yet

- Chapter-3-Answers To Practice QuestionsDocument4 pagesChapter-3-Answers To Practice QuestionsqadirqadilNo ratings yet

- FM Assaignment Second SemisterDocument9 pagesFM Assaignment Second SemisterMotuma Abebe100% (1)

- Cfin 3 3rd Edition Besley Solutions ManualDocument5 pagesCfin 3 3rd Edition Besley Solutions Manualjenniferdrakenxkzgroiyt100% (10)

- Chapter 6 - Answer KeyDocument8 pagesChapter 6 - Answer KeyĐặng Thanh ThuỷNo ratings yet

- Budgeting, Capital Structure, and Working Capital ManagementDocument11 pagesBudgeting, Capital Structure, and Working Capital Managementritu paudelNo ratings yet

- IPF Assignment 4Document12 pagesIPF Assignment 4Nitesh MehlaNo ratings yet

- Chapter 02 - How To Calculate Present ValuesDocument15 pagesChapter 02 - How To Calculate Present ValuesShoaibTahirNo ratings yet

- Cfin 2 2nd Edition Besley Test BankDocument35 pagesCfin 2 2nd Edition Besley Test Bankghebre.comatula.75ew100% (23)

- Lecture Notes Topic 4 Part 2Document34 pagesLecture Notes Topic 4 Part 2sir bookkeeperNo ratings yet

- Corporate FinanceDocument11 pagesCorporate FinanceShamsul HaqimNo ratings yet

- Assignment 4 - Contemporary Engineering BookDocument9 pagesAssignment 4 - Contemporary Engineering BookDhiraj NayakNo ratings yet

- Chapter 2Document3 pagesChapter 2Ikramul HaqueNo ratings yet

- Managerial Economics (Chapter 14)Document28 pagesManagerial Economics (Chapter 14)api-3703724100% (1)

- Si7 - Tarquin (1) 1 9Document9 pagesSi7 - Tarquin (1) 1 9AlvarezMartinNo ratings yet

- Chapter 2 PQ FMDocument5 pagesChapter 2 PQ FMRohan SharmaNo ratings yet

- EE - Assignment Chapter 9-10 SolutionDocument11 pagesEE - Assignment Chapter 9-10 SolutionXuân ThànhNo ratings yet

- Busn 233 CH 08 EeeeDocument102 pagesBusn 233 CH 08 EeeeDavid IoanaNo ratings yet

- CFM Session 8Document7 pagesCFM Session 8khanhnguyenfgoNo ratings yet

- Dwnload Full Cfin 3 3rd Edition Besley Solutions Manual PDFDocument35 pagesDwnload Full Cfin 3 3rd Edition Besley Solutions Manual PDFbrandihansenjoqll2100% (17)

- Tla 9. Basic of Capital BudgetingDocument4 pagesTla 9. Basic of Capital BudgetingNINIO B. MANIALAGNo ratings yet

- Solutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment DecisionsDocument12 pagesSolutions To Chapter 8 Using Discounted Cash-Flow Analysis To Make Investment Decisionshung TranNo ratings yet

- Chapter 6 Answer Key (1 15)Document15 pagesChapter 6 Answer Key (1 15)Desrifta FaheraNo ratings yet

- Solution Assignment Chapter 9 10 1Document14 pagesSolution Assignment Chapter 9 10 1Huynh Ng Quynh NhuNo ratings yet

- Solutions Manual Corporate Fiance Ross W-75%Document10 pagesSolutions Manual Corporate Fiance Ross W-75%Desrifta FaheraNo ratings yet

- Solutions To Selected End-Of-Chapter 6 Problem Solving QuestionsDocument9 pagesSolutions To Selected End-Of-Chapter 6 Problem Solving QuestionsVân Anh Đỗ LêNo ratings yet

- Mock Test SolutionsDocument11 pagesMock Test SolutionsMyraNo ratings yet

- Dwnload Full Cfin 2 2nd Edition Besley Test Bank PDFDocument35 pagesDwnload Full Cfin 2 2nd Edition Besley Test Bank PDFbrandihansenjoqll2100% (17)

- FFM 9 Im 12Document31 pagesFFM 9 Im 12Mariel CorderoNo ratings yet

- Sesi 11 BDocument22 pagesSesi 11 BTata JanetaNo ratings yet

- MTP Soln 1Document14 pagesMTP Soln 1Anonymous 8wg4eowIdzNo ratings yet

- Tutorial 2 SolutionsDocument4 pagesTutorial 2 SolutionsSadia R ChowdhuryNo ratings yet

- Chapter #1 Solutions - Engineering Economy, 7 TH Editionleland Blank and Anthony TarquinDocument9 pagesChapter #1 Solutions - Engineering Economy, 7 TH Editionleland Blank and Anthony TarquinMusa'b100% (10)

- Solutions Review Problems Chap002Document4 pagesSolutions Review Problems Chap002andreaskarayian8972No ratings yet

- 4.01% Is The 1-Year Spot RateDocument6 pages4.01% Is The 1-Year Spot RatePaulo TorresNo ratings yet

- Chapter 02 - How To Calculate Present ValuesDocument14 pagesChapter 02 - How To Calculate Present Valuesdev4c-1No ratings yet

- Chiều t4 - Nhóm 4 - Chương 6Document15 pagesChiều t4 - Nhóm 4 - Chương 6Khánh QuỳnhNo ratings yet

- Lecture 8: Rate of Return Analysis: Instructional Material ForDocument20 pagesLecture 8: Rate of Return Analysis: Instructional Material ForAziezah PalintaNo ratings yet

- Engineering Economy Review III 2010Document4 pagesEngineering Economy Review III 2010Ma Ella Mae LogronioNo ratings yet

- Chapter 11 Exercises and Problems Exercise 11-2: 1. Straight-LineDocument23 pagesChapter 11 Exercises and Problems Exercise 11-2: 1. Straight-LineHazel Rose CabezasNo ratings yet

- Exercises: 1) Acme Borrowed $100,000 From A Local Bank, Which Charges Them An Interest Rate of 7% PerDocument4 pagesExercises: 1) Acme Borrowed $100,000 From A Local Bank, Which Charges Them An Interest Rate of 7% PerIslam MomtazNo ratings yet

- The Basics of Capital Budgeting: Solutions To End-Of-Chapter ProblemsDocument9 pagesThe Basics of Capital Budgeting: Solutions To End-Of-Chapter ProblemsTayeba AnwarNo ratings yet

- 3815capital Budgeting TechniqueDocument51 pages3815capital Budgeting TechniqueMUHMMAD ARSALAN 13728No ratings yet

- Group Assignment 2Document6 pagesGroup Assignment 2Tường ĐứcNo ratings yet

- Lecture-TIME VALUE OF MONEYDocument91 pagesLecture-TIME VALUE OF MONEYCalvin GadiweNo ratings yet

- A2 ADM Fall 2021 With SolutionDocument2 pagesA2 ADM Fall 2021 With SolutionJamal AnsariNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- Manuel C. Espiritu, JR., Et Al. vs. Petron Corp., Et Al.Document6 pagesManuel C. Espiritu, JR., Et Al. vs. Petron Corp., Et Al.BERNADETTE SONo ratings yet

- IAS 1-Presenation of Financial StatementsDocument42 pagesIAS 1-Presenation of Financial StatementsTinoManhangaNo ratings yet

- Invitation For Pre Qualification at Michael Okpara University of Agriculture, Umudike SEPT2012Document4 pagesInvitation For Pre Qualification at Michael Okpara University of Agriculture, Umudike SEPT2012edmund44No ratings yet

- Level 2 - Core Competency FrameworkDocument14 pagesLevel 2 - Core Competency FrameworkbitatfatehNo ratings yet

- Effect of Website Quality On Customer Satisfaction and Purchase Intention in Online Travel Ticket Booking WebsitesDocument6 pagesEffect of Website Quality On Customer Satisfaction and Purchase Intention in Online Travel Ticket Booking Websiteslobna qassemNo ratings yet

- Chapter 3 Cost Accounting CycleDocument11 pagesChapter 3 Cost Accounting CycleSteffany RoqueNo ratings yet

- Translation Exposure Part 1Document31 pagesTranslation Exposure Part 1Magzoub MohaNo ratings yet

- Unit Converter: All in One: Ropani System Bigha System Square Feet Square MeterDocument3 pagesUnit Converter: All in One: Ropani System Bigha System Square Feet Square Meterपोखराको घरNo ratings yet

- The Direction of Fashion Change 1Document19 pagesThe Direction of Fashion Change 1Ratul HasanNo ratings yet

- Bolt™ Lithium Max Professional 2023F - 2 in 1 Stick Vacuum Cleaner BISSELL AustraliaDocument1 pageBolt™ Lithium Max Professional 2023F - 2 in 1 Stick Vacuum Cleaner BISSELL Australialin.odNo ratings yet

- The Seeding Company CEDE TRUST Owned by DTCDocument14 pagesThe Seeding Company CEDE TRUST Owned by DTCRoosevelt Kyle100% (2)

- Executive Summary: Changi AirportDocument18 pagesExecutive Summary: Changi AirportAnil AbduNo ratings yet

- Marketing Plan For Wildcraft Bags: Piyush Kariya 31 Prachi Jain 32 Prajakta Lakade 33 Pushpak Parab 34 Rahul Punjabi 35Document8 pagesMarketing Plan For Wildcraft Bags: Piyush Kariya 31 Prachi Jain 32 Prajakta Lakade 33 Pushpak Parab 34 Rahul Punjabi 35Rahul punjabiNo ratings yet

- Jawaban Soal, Akuntansi Menengah 1Document7 pagesJawaban Soal, Akuntansi Menengah 1Mira OktaviaNo ratings yet

- Marketing Test Bank Chap 10Document53 pagesMarketing Test Bank Chap 10Ta Thi Minh ChauNo ratings yet

- NestleDocument12 pagesNestleParadoxNo ratings yet

- Semua Online Assesment Mira Sem 4Document6 pagesSemua Online Assesment Mira Sem 4Hamierul MohamadNo ratings yet

- Holiday Homework - Worksheet Section 1Document2 pagesHoliday Homework - Worksheet Section 1Anavi KhoslaNo ratings yet

- Greek Gods of Aesthetics Phone Case - Etsy GuatemalaDocument1 pageGreek Gods of Aesthetics Phone Case - Etsy GuatemalaLucia DehesaNo ratings yet

- Lecture Notes - Code of EthicsDocument5 pagesLecture Notes - Code of EthicsHalim Matuan MaamorNo ratings yet

- MTR Foods: Presentation TemplateDocument11 pagesMTR Foods: Presentation Template727821TPMB109 MANUKIRAN S.No ratings yet

- Creative ProcessDocument17 pagesCreative ProcessAlizan MaryNo ratings yet

- Public PolicyDocument11 pagesPublic PolicyssebandekejacksonNo ratings yet

- A ProjectDocument75 pagesA ProjectSameer KNo ratings yet

- Sekarningsih, Dkk. (2020)Document7 pagesSekarningsih, Dkk. (2020)iwang saudjiNo ratings yet

- Inflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyDocument34 pagesInflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyRazvan Catalin CostinNo ratings yet

- Voice of CustomerDocument2 pagesVoice of CustomerShivamNo ratings yet

- Organisational BehaviourDocument12 pagesOrganisational BehaviourMachineni ManaswiniNo ratings yet