Formula Sheet Midterm2021

Formula Sheet Midterm2021

You might also like

- Equations From DamodaranDocument6 pagesEquations From DamodaranhimaggNo ratings yet

- Harmonic Trend Patterns Cheat SheetDocument3 pagesHarmonic Trend Patterns Cheat SheetSharma comp80% (5)

- CFA Formula Cheat SheetDocument9 pagesCFA Formula Cheat SheetChingWa ChanNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- FINA1221 Formula SheetDocument2 pagesFINA1221 Formula SheetTjia Hwei ChewNo ratings yet

- CorpFinance Cheat Sheet v2.2Document2 pagesCorpFinance Cheat Sheet v2.2subtle69100% (4)

- Kelly's Finance Cheat Sheet V6Document2 pagesKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Besserbrau AG-1Document3 pagesBesserbrau AG-1Linda Marceline100% (1)

- Corporate Finance Equations Notes 2Document9 pagesCorporate Finance Equations Notes 2Sotiris HarisNo ratings yet

- Equity ValuationDocument18 pagesEquity ValuationPhuntru PhiNo ratings yet

- List of Corporate Finance FormulasDocument9 pagesList of Corporate Finance FormulasYoungRedNo ratings yet

- E V: A A P: Perceived MispricingDocument19 pagesE V: A A P: Perceived MispricingHeidi HCNo ratings yet

- Finalexam - Financial Management FicheDocument6 pagesFinalexam - Financial Management FicheLouis BarbierNo ratings yet

- S&PM PPT CH 11Document10 pagesS&PM PPT CH 11newnoobgamer17No ratings yet

- Financial Market Problems and FormulasDocument3 pagesFinancial Market Problems and FormulasNufayl KatoNo ratings yet

- Executive Summary of Finance 430Document31 pagesExecutive Summary of Finance 430Ein LuckyNo ratings yet

- Models of Stock ValuationDocument12 pagesModels of Stock ValuationSam Sep A SixtyoneNo ratings yet

- 2FA3 Midterm 2 CribsheetDocument3 pages2FA3 Midterm 2 Cribsheetemri.yasso69No ratings yet

- C3 ValuationDocument26 pagesC3 ValuationMinh Lưu NhậtNo ratings yet

- S4 Valuation Online VersionDocument52 pagesS4 Valuation Online Versionconstruction omanNo ratings yet

- R) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVDocument9 pagesR) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVAgnes LoNo ratings yet

- ValuationDocument45 pagesValuationpptdineshNo ratings yet

- Formulas and ConceptsDocument7 pagesFormulas and Conceptscolen.anneNo ratings yet

- FM Formula Sheet - Not GivenDocument4 pagesFM Formula Sheet - Not GivenSophie ChopraNo ratings yet

- Equity Financing and Stock Valuation. Dividends. Real OptionsDocument5 pagesEquity Financing and Stock Valuation. Dividends. Real OptionsDaniel Chan Ka LokNo ratings yet

- Discounted Dividend ValuationDocument59 pagesDiscounted Dividend Valuationazzie3No ratings yet

- Totalvariable Cost of Annual Sales Turnover of Accounts ReceivableDocument3 pagesTotalvariable Cost of Annual Sales Turnover of Accounts ReceivableMaria Fe FerrarizNo ratings yet

- Công thức IM tự luận- cho finalDocument6 pagesCông thức IM tự luận- cho finalTuấn NguyễnNo ratings yet

- Valuation Model18Document27 pagesValuation Model18mustapha moncefNo ratings yet

- FM Formula Sheet 01Document2 pagesFM Formula Sheet 01Aninda DuttaNo ratings yet

- MGT201 Formulas From Chapter 1 To 22 (Document11 pagesMGT201 Formulas From Chapter 1 To 22 (Ali IbrahimNo ratings yet

- Equity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaDocument51 pagesEquity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaSheeza AshrafNo ratings yet

- An Introduction To Security Valuation: Dr. Amir RafiqueDocument34 pagesAn Introduction To Security Valuation: Dr. Amir RafiqueUsman MahmoodNo ratings yet

- Net Present Value (NPV) : Orporate InanceDocument27 pagesNet Present Value (NPV) : Orporate InanceCratos_PoseidonNo ratings yet

- Financial Management FormulasDocument9 pagesFinancial Management FormulasTannao100% (2)

- Exam Cheat Sheet VSJDocument3 pagesExam Cheat Sheet VSJMinh ANhNo ratings yet

- Corporate FinanceDocument96 pagesCorporate FinanceRohit Kumar83% (6)

- Finance NoteDocument19 pagesFinance NoteHui YiNo ratings yet

- Chapter 7 - Stocks and Stock ValuationDocument5 pagesChapter 7 - Stocks and Stock ValuationYasmine AbdelbaryNo ratings yet

- Chap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtDocument5 pagesChap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtTRANG NGUYỄN LÊ QUỲNHNo ratings yet

- FNCE Cheat Sheet Midterm 1Document1 pageFNCE Cheat Sheet Midterm 1carmenng1990No ratings yet

- Chap 4 BMADocument38 pagesChap 4 BMAGaurav SainiNo ratings yet

- Strategic FinanceDocument11 pagesStrategic FinanceMahrukh RasheedNo ratings yet

- Important FormulasDocument5 pagesImportant FormulasKhalil AkramNo ratings yet

- Stocks, Stock Valuation, and Stock Market EquilibriumDocument85 pagesStocks, Stock Valuation, and Stock Market EquilibriumshimulNo ratings yet

- Cost of CapitalDocument17 pagesCost of Capitalanindya_kundu100% (1)

- Session 4 - Valuation ConceptsDocument23 pagesSession 4 - Valuation Conceptssanjeet_kaur_10No ratings yet

- Dividend Discount ModelDocument19 pagesDividend Discount ModelAnkita PatelNo ratings yet

- Corporate Finance Sam en VattingDocument11 pagesCorporate Finance Sam en VattingVincent van MeeuwenNo ratings yet

- Slide 5Document10 pagesSlide 5Akash SinghNo ratings yet

- Financial Math 1tgtgtrDocument35 pagesFinancial Math 1tgtgtrOmer MehmedNo ratings yet

- The Value of Common StocksDocument32 pagesThe Value of Common StocksDavid BusinelliNo ratings yet

- FIN 401 - Cheat SheetDocument2 pagesFIN 401 - Cheat SheetStephanie NaamaniNo ratings yet

- 1/ Valuation:: Discounted Cash Flow Valuation Timing Value of MoneyDocument12 pages1/ Valuation:: Discounted Cash Flow Valuation Timing Value of MoneyBẢO NGUYỄN HUY100% (1)

- FormulasDocument20 pagesFormulasWilliam ZeNo ratings yet

- Financial Management Equations Korea UniversityDocument2 pagesFinancial Management Equations Korea UniversityTom DNo ratings yet

- Sample Level 1 Wiley Formula Sheets PDFDocument10 pagesSample Level 1 Wiley Formula Sheets PDFMuhammed RafiudeenNo ratings yet

- Slide 4Document27 pagesSlide 4Akash SinghNo ratings yet

- Free Cash Flow ValuationDocument46 pagesFree Cash Flow ValuationRakesh Khanna100% (2)

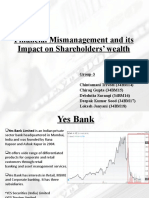

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet

- Federal Republic of Nigeria Foreign Exchange (Monitoring/ Miscellaneous Provision) Decree 1995Document1 pageFederal Republic of Nigeria Foreign Exchange (Monitoring/ Miscellaneous Provision) Decree 1995kasmarproNo ratings yet

- Chapter 7 ExerciseDocument4 pagesChapter 7 ExerciseJoe DicksonNo ratings yet

- Chap 4 - Digital Marketing StrategyDocument21 pagesChap 4 - Digital Marketing StrategyAmeer SaharudinNo ratings yet

- Telco ValuationsDocument24 pagesTelco Valuationschanchan86No ratings yet

- Foreign Currency TranslationDocument38 pagesForeign Currency TranslationAnmol GulatiNo ratings yet

- IOB Annual ReportDocument199 pagesIOB Annual ReportFebson Lee MathewNo ratings yet

- STD PPTch07 Pricing DecisionDocument39 pagesSTD PPTch07 Pricing DecisionNhi NhiNo ratings yet

- How To Value An Insurance CompanyDocument4 pagesHow To Value An Insurance CompanyTopArt Tân BìnhNo ratings yet

- PPT3-Consolidated Financial Statement - Date of AcquisitionDocument54 pagesPPT3-Consolidated Financial Statement - Date of AcquisitionRifdah Saphira100% (1)

- Lecture 7 Products and Product MixDocument33 pagesLecture 7 Products and Product Mixankitamoney1No ratings yet

- An Introduction: by Rajiv SrivastavaDocument17 pagesAn Introduction: by Rajiv SrivastavaM M PanditNo ratings yet

- Dow Waves 2Document5 pagesDow Waves 2brijeshagraNo ratings yet

- Dr. Carlos S. Lanting College: Basic Education DepartmentDocument2 pagesDr. Carlos S. Lanting College: Basic Education DepartmentdreyyNo ratings yet

- IRM Quiz 1 QuestionbankDocument7 pagesIRM Quiz 1 Questionbankgnishi2908No ratings yet

- The Simplest Momentum Indicator - Alvarez Quant TradingDocument8 pagesThe Simplest Momentum Indicator - Alvarez Quant Tradingcoachbiznesu0% (1)

- Calls and Puts: Group IDocument30 pagesCalls and Puts: Group IAayush GaurNo ratings yet

- Low Price-To-Book-Value Stocks: Finding The Winners AmongDocument4 pagesLow Price-To-Book-Value Stocks: Finding The Winners AmongNikunj PatelNo ratings yet

- (Thorpe Kay) Left in Trust (B-Ok - CC)Document68 pages(Thorpe Kay) Left in Trust (B-Ok - CC)krisbooNo ratings yet

- W15295 PDF EngDocument20 pagesW15295 PDF EngXie ZheyuanNo ratings yet

- HDFC ShareholdingDocument11 pagesHDFC ShareholdingCHINMOY PADHINo ratings yet

- GCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)Document14 pagesGCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)aman sainiNo ratings yet

- Currency Futures and Options - FinalDocument107 pagesCurrency Futures and Options - FinalRavindra BabuNo ratings yet

- Toby Crabel NR2Document5 pagesToby Crabel NR2Aditya SoniNo ratings yet

- Aco Ipo.Document166 pagesAco Ipo.Wee Tee FattNo ratings yet

- ECB - Monetary Policy Instruments (Summary) PDFDocument1 pageECB - Monetary Policy Instruments (Summary) PDFDomagoj DrešarNo ratings yet

- MVIS CryptoCompare Digital Assets IndicesDocument42 pagesMVIS CryptoCompare Digital Assets IndicesIsnan Hari MardikaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Equations From DamodaranDocument6 pagesEquations From DamodaranhimaggNo ratings yet

- Harmonic Trend Patterns Cheat SheetDocument3 pagesHarmonic Trend Patterns Cheat SheetSharma comp80% (5)

- CFA Formula Cheat SheetDocument9 pagesCFA Formula Cheat SheetChingWa ChanNo ratings yet

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- FINA1221 Formula SheetDocument2 pagesFINA1221 Formula SheetTjia Hwei ChewNo ratings yet

- CorpFinance Cheat Sheet v2.2Document2 pagesCorpFinance Cheat Sheet v2.2subtle69100% (4)

- Kelly's Finance Cheat Sheet V6Document2 pagesKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Besserbrau AG-1Document3 pagesBesserbrau AG-1Linda Marceline100% (1)

- Corporate Finance Equations Notes 2Document9 pagesCorporate Finance Equations Notes 2Sotiris HarisNo ratings yet

- Equity ValuationDocument18 pagesEquity ValuationPhuntru PhiNo ratings yet

- List of Corporate Finance FormulasDocument9 pagesList of Corporate Finance FormulasYoungRedNo ratings yet

- E V: A A P: Perceived MispricingDocument19 pagesE V: A A P: Perceived MispricingHeidi HCNo ratings yet

- Finalexam - Financial Management FicheDocument6 pagesFinalexam - Financial Management FicheLouis BarbierNo ratings yet

- S&PM PPT CH 11Document10 pagesS&PM PPT CH 11newnoobgamer17No ratings yet

- Financial Market Problems and FormulasDocument3 pagesFinancial Market Problems and FormulasNufayl KatoNo ratings yet

- Executive Summary of Finance 430Document31 pagesExecutive Summary of Finance 430Ein LuckyNo ratings yet

- Models of Stock ValuationDocument12 pagesModels of Stock ValuationSam Sep A SixtyoneNo ratings yet

- 2FA3 Midterm 2 CribsheetDocument3 pages2FA3 Midterm 2 Cribsheetemri.yasso69No ratings yet

- C3 ValuationDocument26 pagesC3 ValuationMinh Lưu NhậtNo ratings yet

- S4 Valuation Online VersionDocument52 pagesS4 Valuation Online Versionconstruction omanNo ratings yet

- R) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVDocument9 pagesR) (1 CF ...... R) (1 CF R) (1 CF CF NPV: Invesment Initial NPV 1 Invesments Initial Flows Cash Future of PVAgnes LoNo ratings yet

- ValuationDocument45 pagesValuationpptdineshNo ratings yet

- Formulas and ConceptsDocument7 pagesFormulas and Conceptscolen.anneNo ratings yet

- FM Formula Sheet - Not GivenDocument4 pagesFM Formula Sheet - Not GivenSophie ChopraNo ratings yet

- Equity Financing and Stock Valuation. Dividends. Real OptionsDocument5 pagesEquity Financing and Stock Valuation. Dividends. Real OptionsDaniel Chan Ka LokNo ratings yet

- Discounted Dividend ValuationDocument59 pagesDiscounted Dividend Valuationazzie3No ratings yet

- Totalvariable Cost of Annual Sales Turnover of Accounts ReceivableDocument3 pagesTotalvariable Cost of Annual Sales Turnover of Accounts ReceivableMaria Fe FerrarizNo ratings yet

- Công thức IM tự luận- cho finalDocument6 pagesCông thức IM tự luận- cho finalTuấn NguyễnNo ratings yet

- Valuation Model18Document27 pagesValuation Model18mustapha moncefNo ratings yet

- FM Formula Sheet 01Document2 pagesFM Formula Sheet 01Aninda DuttaNo ratings yet

- MGT201 Formulas From Chapter 1 To 22 (Document11 pagesMGT201 Formulas From Chapter 1 To 22 (Ali IbrahimNo ratings yet

- Equity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaDocument51 pagesEquity Valuation: BY: Sheeza Ashraf Neelam Afroz Aamir Khan Elna V. Rajan Suaid MullaSheeza AshrafNo ratings yet

- An Introduction To Security Valuation: Dr. Amir RafiqueDocument34 pagesAn Introduction To Security Valuation: Dr. Amir RafiqueUsman MahmoodNo ratings yet

- Net Present Value (NPV) : Orporate InanceDocument27 pagesNet Present Value (NPV) : Orporate InanceCratos_PoseidonNo ratings yet

- Financial Management FormulasDocument9 pagesFinancial Management FormulasTannao100% (2)

- Exam Cheat Sheet VSJDocument3 pagesExam Cheat Sheet VSJMinh ANhNo ratings yet

- Corporate FinanceDocument96 pagesCorporate FinanceRohit Kumar83% (6)

- Finance NoteDocument19 pagesFinance NoteHui YiNo ratings yet

- Chapter 7 - Stocks and Stock ValuationDocument5 pagesChapter 7 - Stocks and Stock ValuationYasmine AbdelbaryNo ratings yet

- Chap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtDocument5 pagesChap 2: 1. CF (A) OCF - Capital Spending - 2. CF (B) Debt Service - Long-Term DebtTRANG NGUYỄN LÊ QUỲNHNo ratings yet

- FNCE Cheat Sheet Midterm 1Document1 pageFNCE Cheat Sheet Midterm 1carmenng1990No ratings yet

- Chap 4 BMADocument38 pagesChap 4 BMAGaurav SainiNo ratings yet

- Strategic FinanceDocument11 pagesStrategic FinanceMahrukh RasheedNo ratings yet

- Important FormulasDocument5 pagesImportant FormulasKhalil AkramNo ratings yet

- Stocks, Stock Valuation, and Stock Market EquilibriumDocument85 pagesStocks, Stock Valuation, and Stock Market EquilibriumshimulNo ratings yet

- Cost of CapitalDocument17 pagesCost of Capitalanindya_kundu100% (1)

- Session 4 - Valuation ConceptsDocument23 pagesSession 4 - Valuation Conceptssanjeet_kaur_10No ratings yet

- Dividend Discount ModelDocument19 pagesDividend Discount ModelAnkita PatelNo ratings yet

- Corporate Finance Sam en VattingDocument11 pagesCorporate Finance Sam en VattingVincent van MeeuwenNo ratings yet

- Slide 5Document10 pagesSlide 5Akash SinghNo ratings yet

- Financial Math 1tgtgtrDocument35 pagesFinancial Math 1tgtgtrOmer MehmedNo ratings yet

- The Value of Common StocksDocument32 pagesThe Value of Common StocksDavid BusinelliNo ratings yet

- FIN 401 - Cheat SheetDocument2 pagesFIN 401 - Cheat SheetStephanie NaamaniNo ratings yet

- 1/ Valuation:: Discounted Cash Flow Valuation Timing Value of MoneyDocument12 pages1/ Valuation:: Discounted Cash Flow Valuation Timing Value of MoneyBẢO NGUYỄN HUY100% (1)

- FormulasDocument20 pagesFormulasWilliam ZeNo ratings yet

- Financial Management Equations Korea UniversityDocument2 pagesFinancial Management Equations Korea UniversityTom DNo ratings yet

- Sample Level 1 Wiley Formula Sheets PDFDocument10 pagesSample Level 1 Wiley Formula Sheets PDFMuhammed RafiudeenNo ratings yet

- Slide 4Document27 pagesSlide 4Akash SinghNo ratings yet

- Free Cash Flow ValuationDocument46 pagesFree Cash Flow ValuationRakesh Khanna100% (2)

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet

- Federal Republic of Nigeria Foreign Exchange (Monitoring/ Miscellaneous Provision) Decree 1995Document1 pageFederal Republic of Nigeria Foreign Exchange (Monitoring/ Miscellaneous Provision) Decree 1995kasmarproNo ratings yet

- Chapter 7 ExerciseDocument4 pagesChapter 7 ExerciseJoe DicksonNo ratings yet

- Chap 4 - Digital Marketing StrategyDocument21 pagesChap 4 - Digital Marketing StrategyAmeer SaharudinNo ratings yet

- Telco ValuationsDocument24 pagesTelco Valuationschanchan86No ratings yet

- Foreign Currency TranslationDocument38 pagesForeign Currency TranslationAnmol GulatiNo ratings yet

- IOB Annual ReportDocument199 pagesIOB Annual ReportFebson Lee MathewNo ratings yet

- STD PPTch07 Pricing DecisionDocument39 pagesSTD PPTch07 Pricing DecisionNhi NhiNo ratings yet

- How To Value An Insurance CompanyDocument4 pagesHow To Value An Insurance CompanyTopArt Tân BìnhNo ratings yet

- PPT3-Consolidated Financial Statement - Date of AcquisitionDocument54 pagesPPT3-Consolidated Financial Statement - Date of AcquisitionRifdah Saphira100% (1)

- Lecture 7 Products and Product MixDocument33 pagesLecture 7 Products and Product Mixankitamoney1No ratings yet

- An Introduction: by Rajiv SrivastavaDocument17 pagesAn Introduction: by Rajiv SrivastavaM M PanditNo ratings yet

- Dow Waves 2Document5 pagesDow Waves 2brijeshagraNo ratings yet

- Dr. Carlos S. Lanting College: Basic Education DepartmentDocument2 pagesDr. Carlos S. Lanting College: Basic Education DepartmentdreyyNo ratings yet

- IRM Quiz 1 QuestionbankDocument7 pagesIRM Quiz 1 Questionbankgnishi2908No ratings yet

- The Simplest Momentum Indicator - Alvarez Quant TradingDocument8 pagesThe Simplest Momentum Indicator - Alvarez Quant Tradingcoachbiznesu0% (1)

- Calls and Puts: Group IDocument30 pagesCalls and Puts: Group IAayush GaurNo ratings yet

- Low Price-To-Book-Value Stocks: Finding The Winners AmongDocument4 pagesLow Price-To-Book-Value Stocks: Finding The Winners AmongNikunj PatelNo ratings yet

- (Thorpe Kay) Left in Trust (B-Ok - CC)Document68 pages(Thorpe Kay) Left in Trust (B-Ok - CC)krisbooNo ratings yet

- W15295 PDF EngDocument20 pagesW15295 PDF EngXie ZheyuanNo ratings yet

- HDFC ShareholdingDocument11 pagesHDFC ShareholdingCHINMOY PADHINo ratings yet

- GCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)Document14 pagesGCC&BA SUPR Share-Capital-1 Sushita-Chakraborty UG (R1)aman sainiNo ratings yet

- Currency Futures and Options - FinalDocument107 pagesCurrency Futures and Options - FinalRavindra BabuNo ratings yet

- Toby Crabel NR2Document5 pagesToby Crabel NR2Aditya SoniNo ratings yet

- Aco Ipo.Document166 pagesAco Ipo.Wee Tee FattNo ratings yet

- ECB - Monetary Policy Instruments (Summary) PDFDocument1 pageECB - Monetary Policy Instruments (Summary) PDFDomagoj DrešarNo ratings yet

- MVIS CryptoCompare Digital Assets IndicesDocument42 pagesMVIS CryptoCompare Digital Assets IndicesIsnan Hari MardikaNo ratings yet