Download as docx, pdf, or txt

You might also like

- 191 - 197 - Detection of Transaction Fraud Using Deep LearningDocument28 pages191 - 197 - Detection of Transaction Fraud Using Deep LearningADRINEEL SAHANo ratings yet

- Assignment On Banking Service & Operation (EBankingDocument15 pagesAssignment On Banking Service & Operation (EBankingpridegiri86% (7)

- Roots Causes of TerrorismDocument41 pagesRoots Causes of TerrorismMikel Rodríguez33% (3)

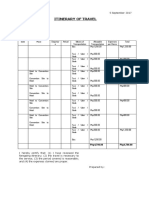

- Travel ItineraryDocument1 pageTravel ItineraryNorthCarolinaNo ratings yet

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Ummasking Digital FraudDocument15 pagesUmmasking Digital Fraudaymen marzoukiNo ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- Paypal: Presentation Done By: Danilo Joncic & Pavle StevanovicDocument10 pagesPaypal: Presentation Done By: Danilo Joncic & Pavle StevanoviclilpvciNo ratings yet

- "The Automated Teller Machine": Engineering College BikanerDocument12 pages"The Automated Teller Machine": Engineering College BikanerRajesh BishnoiNo ratings yet

- City Bank ScamDocument15 pagesCity Bank ScamshrillNo ratings yet

- D B: W U W "C " R: ATA Reaches Hat The Nderground Orld of Arding EvealsDocument33 pagesD B: W U W "C " R: ATA Reaches Hat The Nderground Orld of Arding EvealsMalik Tanveer HussainNo ratings yet

- <!DOCTYPE HTML PUBLIC "-//W3C//DTD HTML 4.01 Transitional//EN" "http://www.w3.org/TR/html4/loose.dtd"> <HTML><HEAD><META HTTP-EQUIV="Content-Type" CONTENT="text/html; charset=iso-8859-1"> <TITLE>ERROR: The requested URL could not be retrieved</TITLE> <STYLE type="text/css"><!--BODY{background-color:#ffffff;font-family:verdana,sans-serif}PRE{font-family:sans-serif}--></STYLE> </HEAD><BODY> <H1>ERROR</H1> <H2>The requested URL could not be retrieved</H2> <HR noshade size="1px"> <P> While trying to process the request: <PRE> TEXT http://www.scribd.com/titlecleaner?title=CyberCrime+Report.docx HTTP/1.1 Host: www.scribd.com Proxy-Connection: keep-alive Accept: */* Origin: http://www.scribd.com X-CSRF-Token: ea5b3d74fc35283c15ef440947b36a61b715cffd User-Agent: Mozilla/5.0 (Windows NT 6.1; WOW64) AppleWebKit/537.31 (KHTML, like Gecko) Chrome/26.0.1410.64 Safari/537.31 X-Requested-With: XMLHttpRequest Referer: http://www.scribd.com/upload-document Accept-Encoding: gzip,deflDocument32 pages<!DOCTYPE HTML PUBLIC "-//W3C//DTD HTML 4.01 Transitional//EN" "http://www.w3.org/TR/html4/loose.dtd"> <HTML><HEAD><META HTTP-EQUIV="Content-Type" CONTENT="text/html; charset=iso-8859-1"> <TITLE>ERROR: The requested URL could not be retrieved</TITLE> <STYLE type="text/css"><!--BODY{background-color:#ffffff;font-family:verdana,sans-serif}PRE{font-family:sans-serif}--></STYLE> </HEAD><BODY> <H1>ERROR</H1> <H2>The requested URL could not be retrieved</H2> <HR noshade size="1px"> <P> While trying to process the request: <PRE> TEXT http://www.scribd.com/titlecleaner?title=CyberCrime+Report.docx HTTP/1.1 Host: www.scribd.com Proxy-Connection: keep-alive Accept: */* Origin: http://www.scribd.com X-CSRF-Token: ea5b3d74fc35283c15ef440947b36a61b715cffd User-Agent: Mozilla/5.0 (Windows NT 6.1; WOW64) AppleWebKit/537.31 (KHTML, like Gecko) Chrome/26.0.1410.64 Safari/537.31 X-Requested-With: XMLHttpRequest Referer: http://www.scribd.com/upload-document Accept-Encoding: gzip,deflUttam KumarNo ratings yet

- Bank of America On Mobile BankingDocument72 pagesBank of America On Mobile BankingDr. Rajeev AgarwalNo ratings yet

- Unit 3 E-CommerceDocument49 pagesUnit 3 E-Commerceanon_733630181No ratings yet

- Credit CardsDocument50 pagesCredit Cardsprince100% (3)

- SRS For ATM SystemDocument21 pagesSRS For ATM SystemUrja DhabardeNo ratings yet

- Fraud in Internet BankingDocument31 pagesFraud in Internet BankingnewasyrafNo ratings yet

- Mobile BankingDocument17 pagesMobile BankingSuchet SinghNo ratings yet

- HDFC Online BankingDocument24 pagesHDFC Online BankingAmardeep SinghNo ratings yet

- Axis Bank Debit and Credit Card SonamDocument81 pagesAxis Bank Debit and Credit Card SonamsonamNo ratings yet

- ATM ProjectDocument88 pagesATM ProjectRajat BansalNo ratings yet

- Credit Card Information LeakedDocument2 pagesCredit Card Information LeakedHentaiNo ratings yet

- Surecash Mobile BankingDocument36 pagesSurecash Mobile Bankingমেহেদি তসলিমNo ratings yet

- Credit Card Pricing Strategy: Davide Capodici, Brooke Chang, Brian Feldman, Erica GluckDocument75 pagesCredit Card Pricing Strategy: Davide Capodici, Brooke Chang, Brian Feldman, Erica GluckBinay Kumar SinghNo ratings yet

- Cred FraudDocument22 pagesCred FraudAshish KumarNo ratings yet

- Jumpstart Credit Card Processing (Version 1)Document15 pagesJumpstart Credit Card Processing (Version 1)Oleksiy KovyrinNo ratings yet

- 8 Credit Card System OOADDocument29 pages8 Credit Card System OOADMahesh WaraNo ratings yet

- MasterCard JJDocument7 pagesMasterCard JJjohnjamgochianNo ratings yet

- Types of Software Used in BanksDocument3 pagesTypes of Software Used in BanksMussadaq JavedNo ratings yet

- Bhavik BlackbookDocument29 pagesBhavik BlackbookBhavik khairNo ratings yet

- Money Mule Recruitment Among University Students in Malaysia Awareness PerspectiveDocument19 pagesMoney Mule Recruitment Among University Students in Malaysia Awareness PerspectiveGlobal Research and Development ServicesNo ratings yet

- Payments For Electronic CommerceDocument48 pagesPayments For Electronic CommerceMariaSangsterNo ratings yet

- Credit Card Fraud Detection and Classification byDocument6 pagesCredit Card Fraud Detection and Classification byDikshantNo ratings yet

- ScammerDocument2 pagesScammerAqilah HanisNo ratings yet

- The Insider CodeDocument15 pagesThe Insider CodeJohn PatlolNo ratings yet

- Cybercrime - Britannica Online EncyclopediaDocument16 pagesCybercrime - Britannica Online EncyclopediaH M Masum HasanNo ratings yet

- Atms: Automated Teller MachinesDocument31 pagesAtms: Automated Teller MachinesOnkar KanadeNo ratings yet

- TT Aug 2011Document28 pagesTT Aug 2011Daniel MurffNo ratings yet

- E PaymentDocument22 pagesE PaymentxanshahNo ratings yet

- Cases of Computer FraudDocument3 pagesCases of Computer FraudAnthony FloresNo ratings yet

- Citibank Scam at Gurgaon Retail BranchDocument8 pagesCitibank Scam at Gurgaon Retail BranchMandeep DalalNo ratings yet

- Security of Electronic Payment Systems: A Comprehensive SurveyDocument29 pagesSecurity of Electronic Payment Systems: A Comprehensive Surveyshriram1082883No ratings yet

- Online Bank Management SystemDocument64 pagesOnline Bank Management SystemMahesh.S. SatbhaiNo ratings yet

- Chapter-1 Introduciton: 1.1 What Is Debit C Ard?Document60 pagesChapter-1 Introduciton: 1.1 What Is Debit C Ard?glorydharmarajNo ratings yet

- Building An E Commerce Site A Systematic ApproachDocument31 pagesBuilding An E Commerce Site A Systematic ApproachAlliah Fe Kyreh SegoviaNo ratings yet

- EMV Card and Terminal Basic Requirements FINAL 04 15 v2.2Document29 pagesEMV Card and Terminal Basic Requirements FINAL 04 15 v2.2hellojanakaNo ratings yet

- 8x Protocol WhitepaperDocument11 pages8x Protocol WhitepaperKerman KohliNo ratings yet

- Money PadDocument15 pagesMoney PadAnvita_Jain_2921No ratings yet

- IN Banks: Cyber CrimesDocument34 pagesIN Banks: Cyber CrimesPreethi RaviNo ratings yet

- B For BlockchainDocument59 pagesB For BlockchainTeam CoinDCXNo ratings yet

- Mobilink-Network Partial List of PartnersDocument5 pagesMobilink-Network Partial List of PartnersEksdiNo ratings yet

- OWASPLondon 20180125leigh Anne Galloway TYunusov Buy Hack ATMDocument57 pagesOWASPLondon 20180125leigh Anne Galloway TYunusov Buy Hack ATMBoby JosephNo ratings yet

- Scams in Banking IndustryDocument9 pagesScams in Banking IndustryMini sureshNo ratings yet

- Chapter One 1.0Document16 pagesChapter One 1.0Eet's Marve RichyNo ratings yet

- Plastic MoneyDocument15 pagesPlastic MoneyRazzat AroraNo ratings yet

- Listening Log 1 (Banking Transaction)Document4 pagesListening Log 1 (Banking Transaction)Gitaaf AFNo ratings yet

- Atm With An EyeDocument25 pagesAtm With An EyeKiran StridesNo ratings yet

- Ki Gerl 2017Document19 pagesKi Gerl 2017Bern Jonathan SembiringNo ratings yet

- How To Make An Online Donation To CMCCKL Online AccountDocument4 pagesHow To Make An Online Donation To CMCCKL Online AccountEdwin NgNo ratings yet

- What Is The Dark WebDocument11 pagesWhat Is The Dark Websinaglaya hallNo ratings yet

- Cariaga Vs LagunaDocument2 pagesCariaga Vs LagunaMaCai YambaoNo ratings yet

- 07 LTE Handovers P PDFDocument60 pages07 LTE Handovers P PDFAjbouni AnisNo ratings yet

- A Voice For The VoicelessDocument3 pagesA Voice For The VoicelessKatherine AquinoNo ratings yet

- FortiOS 7.2.0 CLI ReferenceDocument1,831 pagesFortiOS 7.2.0 CLI ReferenceAyan Naskar100% (1)

- Song Kiat v. Central Bank DigestDocument1 pageSong Kiat v. Central Bank DigestNamiel Maverick D. BalinaNo ratings yet

- Rotary Policies On Sexual HarassmentDocument23 pagesRotary Policies On Sexual HarassmentJames JimenezNo ratings yet

- Circumstances Affecting Criminal LiabilityDocument1 pageCircumstances Affecting Criminal LiabilityMikail Lee BelloNo ratings yet

- New Board MemberDocument2 pagesNew Board MemberJBS RINo ratings yet

- NegoDocument16 pagesNegodollyccruzNo ratings yet

- LSS - A Software Presentation For Indian NVOCCsDocument33 pagesLSS - A Software Presentation For Indian NVOCCsSyscon InfotechNo ratings yet

- Nitric Acid 70%Document10 pagesNitric Acid 70%Oscar ValdezNo ratings yet

- Easa Emergency Airworthiness Directive: AD No.: 2009-0245-EDocument3 pagesEasa Emergency Airworthiness Directive: AD No.: 2009-0245-EYuri SilvaNo ratings yet

- CSC vs. Magnaye, G.R. 183337, April 23, 2010Document1 pageCSC vs. Magnaye, G.R. 183337, April 23, 2010Charmila SiplonNo ratings yet

- Risk Assessment ChecklistDocument1 pageRisk Assessment ChecklistSyed Irtiza HassanNo ratings yet

- Mins 081030 CCDocument1 pageMins 081030 CCJames LindonNo ratings yet

- National Institute of Technology Durgapur India: Shubham SarafDocument2 pagesNational Institute of Technology Durgapur India: Shubham SarafShubham SarafNo ratings yet

- Company Profile 2023Document28 pagesCompany Profile 2023Elsa B. AntonioNo ratings yet

- Sultan Mehmed Al-FatehDocument2 pagesSultan Mehmed Al-FatehAni AniyoNo ratings yet

- Ayodhya Ram Temple EventDocument1 pageAyodhya Ram Temple EventExpress WebNo ratings yet

- Jenny Louise Cudd - Motion To Sever CaseDocument6 pagesJenny Louise Cudd - Motion To Sever CaseLaw&CrimeNo ratings yet

- Application To Extend/Change Nonimmigrant Status USCIS Form I-539 Department of Homeland SecurityDocument6 pagesApplication To Extend/Change Nonimmigrant Status USCIS Form I-539 Department of Homeland SecurityGabriel VaelanteNo ratings yet

- Citizenship Requirement CIT0007E-2Document1 pageCitizenship Requirement CIT0007E-2Abu HudaNo ratings yet

- Lesson 2 Pre-Spanish and Spanish Era Literature PresentationDocument92 pagesLesson 2 Pre-Spanish and Spanish Era Literature PresentationShunuan HuangNo ratings yet

- Chrome Hearts v. Fashion NovaDocument15 pagesChrome Hearts v. Fashion NovaThe Fashion LawNo ratings yet

- Ruthless - Week 1Document28 pagesRuthless - Week 1Luke Harris100% (1)

- Faq Aluminum MW Us Transaction Premium SwapDocument4 pagesFaq Aluminum MW Us Transaction Premium Swapnerolf73No ratings yet

- Jon Del Arroz v. Worldcon: 21) LAW AND MOTION TENTATIVE RULINGS DATE: 2-21-19 TIME: 9 A.MDocument37 pagesJon Del Arroz v. Worldcon: 21) LAW AND MOTION TENTATIVE RULINGS DATE: 2-21-19 TIME: 9 A.MDonut Glaze100% (1)

- Billie Eilish - Bad Guy Piano Sheet Music PDFDocument7 pagesBillie Eilish - Bad Guy Piano Sheet Music PDFtiger lily0% (6)