Download as doc, pdf, or txt

You might also like

- Tutorial 10 - AnswersDocument2 pagesTutorial 10 - AnswersShankar A/L MuthukumaranNo ratings yet

- Dipak Kumar Bhattacharyya - Principles of Management - Text and Cases-Pearson Education (2012) PDFDocument489 pagesDipak Kumar Bhattacharyya - Principles of Management - Text and Cases-Pearson Education (2012) PDFShaji Zachariah80% (5)

- Business Finance Week 4Document3 pagesBusiness Finance Week 4JayMoralesNo ratings yet

- AccountantsDocument15 pagesAccountantsJenny EvangelistaNo ratings yet

- Fabm2 Q1 M4Document23 pagesFabm2 Q1 M4Beverly ComamoNo ratings yet

- Final ModuleDocument3 pagesFinal ModuleAnnabelle MancoNo ratings yet

- Fabm1 Quarter1 Module 6.2 Week 6Document22 pagesFabm1 Quarter1 Module 6.2 Week 6Danny BulacsoNo ratings yet

- M4 Prac Exer. 2Document10 pagesM4 Prac Exer. 2Jasmine ActaNo ratings yet

- As A Consumer, What Are The Different Factors That Will Make You Buy Their Products or Services? JollibeeDocument3 pagesAs A Consumer, What Are The Different Factors That Will Make You Buy Their Products or Services? JollibeeNur ShaNo ratings yet

- Answers 5Document101 pagesAnswers 5api-308823932100% (1)

- Accounting Concepts and Principles Are A Set of Broad Conventions That Have Been Devised To Provide A Basic Framework For Financial ReportingDocument8 pagesAccounting Concepts and Principles Are A Set of Broad Conventions That Have Been Devised To Provide A Basic Framework For Financial ReportingGesa StephenNo ratings yet

- LAS in Acounting 2 Week 1Document8 pagesLAS in Acounting 2 Week 1dorothytorino8No ratings yet

- (MKTG1 Lesson 1) PRINCIPLES OF MARKETINGDocument4 pages(MKTG1 Lesson 1) PRINCIPLES OF MARKETINGJeffrey Jazz BugashNo ratings yet

- Bus - Math11 Q1mod4of8 Markup-Markon - Markdown v2-SLMDocument27 pagesBus - Math11 Q1mod4of8 Markup-Markon - Markdown v2-SLMKathy BaynosaNo ratings yet

- Principles of MKTG Module Jan 11-29Document18 pagesPrinciples of MKTG Module Jan 11-29Roz AdaNo ratings yet

- Debits and CreditDocument3 pagesDebits and CreditAnne HathawayNo ratings yet

- Module in Fundamentals of Accountancy, Business and Management (Grade 12) Statement of Comprehensive Income (SCI)Document7 pagesModule in Fundamentals of Accountancy, Business and Management (Grade 12) Statement of Comprehensive Income (SCI)Jocelyn Estrella Prendol SorianoNo ratings yet

- w319 Lewis Structures Shapes and Polarity PDFDocument3 pagesw319 Lewis Structures Shapes and Polarity PDFJohn BartolomeNo ratings yet

- Fundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeDocument9 pagesFundamentals of Accountancy, Business and Management 2: Statement of Comprehensive IncomeBea allyssa CanapiNo ratings yet

- Business Finance Week 1 To 3 Without Answer KeyDocument29 pagesBusiness Finance Week 1 To 3 Without Answer KeyKristel Anne Roquero Balisi100% (1)

- HOPE 4 Module 8 Training PlanDocument10 pagesHOPE 4 Module 8 Training PlanAJ Bacarisas RochaNo ratings yet

- Business Mathematics: Specialized Subject - ABMDocument12 pagesBusiness Mathematics: Specialized Subject - ABMemmalou shane fernandezNo ratings yet

- Financial Statement Analysis: Mr. Christopher B. CauanDocument63 pagesFinancial Statement Analysis: Mr. Christopher B. CauanChristopher Beltran CauanNo ratings yet

- Pretest: Gine Bert Fariñas PalabricaDocument3 pagesPretest: Gine Bert Fariñas PalabricaGine Bert Fariñas PalabricaNo ratings yet

- Technology Forces in BusinessDocument3 pagesTechnology Forces in BusinessTurling100% (1)

- Cieverose College, Inc.: Fundamentals of Accountancy, Business and Management 2Document10 pagesCieverose College, Inc.: Fundamentals of Accountancy, Business and Management 2Venus Frias-Antonio100% (1)

- Accounting 2 Week 1-2Document6 pagesAccounting 2 Week 1-2Ace LincolnNo ratings yet

- Chapter 3 Financial PlanningDocument25 pagesChapter 3 Financial PlanningChristopher Beltran CauanNo ratings yet

- Edited Love by YouDocument49 pagesEdited Love by YouGElla BarRete ReQuilloNo ratings yet

- Entrep Reviewer 101444Document6 pagesEntrep Reviewer 101444hinacay.jonNo ratings yet

- Problems Accounting Equation 1 5 UnsolvedDocument5 pagesProblems Accounting Equation 1 5 UnsolvedRaja NarayananNo ratings yet

- Mark Up Versus MarginDocument18 pagesMark Up Versus MarginCaryl GalocgocNo ratings yet

- Principles of Marketing WEEK 3 and 4Document6 pagesPrinciples of Marketing WEEK 3 and 4JayMoralesNo ratings yet

- Eapp Module 3Document4 pagesEapp Module 3Alissa MayNo ratings yet

- G12 Principles of MKTG Q1WK2 ABCD FinalDocument8 pagesG12 Principles of MKTG Q1WK2 ABCD FinalRhesa Joy PalmesNo ratings yet

- Before You Start With Our Lesson, Answer First The Pre-Assessment On The ASSESSMENT SHEETS On Page 3Document4 pagesBefore You Start With Our Lesson, Answer First The Pre-Assessment On The ASSESSMENT SHEETS On Page 3Aldrin Aldrin100% (1)

- Applied Economics-2nd Quarter Week 1Document9 pagesApplied Economics-2nd Quarter Week 1Jean Irine TumamposNo ratings yet

- Activity 6.1Document5 pagesActivity 6.1Sonoko SuzukiNo ratings yet

- AppliedDocument33 pagesAppliedYnahNo ratings yet

- ABM PM 2nd QTR SLM Week12Document9 pagesABM PM 2nd QTR SLM Week12ganda dyosaNo ratings yet

- ENTREP ACTIVITY SHEET 1st Quarter Week 5 To 6 Edited 2Document8 pagesENTREP ACTIVITY SHEET 1st Quarter Week 5 To 6 Edited 2Pete CruzNo ratings yet

- Fabm 2Document170 pagesFabm 2Asti GumacaNo ratings yet

- LESSON 1.1. Introduction To AccountingDocument12 pagesLESSON 1.1. Introduction To AccountingTrisha PeñascozaNo ratings yet

- Sample Business PlanDocument29 pagesSample Business PlanAyse AyseNo ratings yet

- English For Academic and Professional Purpose Module 4 Lesson 2 & 2.Document13 pagesEnglish For Academic and Professional Purpose Module 4 Lesson 2 & 2.Frhea mae AlcaydeNo ratings yet

- Accounting ActivityDocument3 pagesAccounting ActivityKae Abegail GarciaNo ratings yet

- Accounting 2 - 2nd ModuleDocument8 pagesAccounting 2 - 2nd ModuleJessalyn Sarmiento Tancio100% (1)

- Lesson 2 - Users of Accounting InformationDocument46 pagesLesson 2 - Users of Accounting InformationJoanNo ratings yet

- Accounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloDocument41 pagesAccounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloRoxe XNo ratings yet

- Cash Flow Statement (CFS)Document8 pagesCash Flow Statement (CFS)KhayNo ratings yet

- Mixed Streams: Drew Fayth Mangrobang Angelie Momi Ariane Joyce ArqueroDocument22 pagesMixed Streams: Drew Fayth Mangrobang Angelie Momi Ariane Joyce ArqueroKatring O.No ratings yet

- FABM 1 Lesson 6 Accounting Concepts and PrinciplesDocument3 pagesFABM 1 Lesson 6 Accounting Concepts and PrinciplesTiffany CenizaNo ratings yet

- EntrepreneurshipDocument1 pageEntrepreneurshipJemel DelosReyes MuñozNo ratings yet

- Chapter 3: Elements of Demand and SupplyDocument19 pagesChapter 3: Elements of Demand and SupplySerrano EUNo ratings yet

- ABM FABM1 AIRs LM Q3 W5 M5Document20 pagesABM FABM1 AIRs LM Q3 W5 M5Trisha Mae DuatNo ratings yet

- Hope 4 Module 1Document25 pagesHope 4 Module 1Kchean Grace PensicaNo ratings yet

- 3 Users of Accounting InformationDocument29 pages3 Users of Accounting InformationAdrianChrisArciagaArevaloNo ratings yet

- Markup and Markdown: Mr. Christian Rae D. Bernales, LPTDocument7 pagesMarkup and Markdown: Mr. Christian Rae D. Bernales, LPTAlissa MayNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7Document6 pagesFundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7nicss bonaobraNo ratings yet

- LESSON 10 Business TransactionsDocument8 pagesLESSON 10 Business TransactionsUnamadable UnleomarableNo ratings yet

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Chapter Five Inventory Management - Chapter 4Document10 pagesChapter Five Inventory Management - Chapter 4eferemNo ratings yet

- TikemetreadingDocument2 pagesTikemetreadingAsteway MesfinNo ratings yet

- MGMT 221, Ch. IVDocument29 pagesMGMT 221, Ch. IVAsteway Mesfin100% (1)

- Allegato1 ENDocument9 pagesAllegato1 ENAsteway MesfinNo ratings yet

- The Dotcom BubbleDocument12 pagesThe Dotcom BubbleAsteway MesfinNo ratings yet

- Extended Terms of RFP For Travel ServicesDocument15 pagesExtended Terms of RFP For Travel ServicesAsteway MesfinNo ratings yet

- Capital Market and Financial Sector Development in Sub-Saharan AfricaDocument32 pagesCapital Market and Financial Sector Development in Sub-Saharan AfricaAsteway MesfinNo ratings yet

- Irida Huta Chairperson of The Payments Digitalization Alternative Channels Committee AABDocument8 pagesIrida Huta Chairperson of The Payments Digitalization Alternative Channels Committee AABAsteway MesfinNo ratings yet

- Profiteering From The Dot-Com Bubble, Sub-Prime Crisis and Asian Financial CrisisDocument44 pagesProfiteering From The Dot-Com Bubble, Sub-Prime Crisis and Asian Financial CrisisAsteway MesfinNo ratings yet

- G8 English Ch1-3Document37 pagesG8 English Ch1-3Asteway MesfinNo ratings yet

- MGMT 222 Ch. IIIDocument10 pagesMGMT 222 Ch. IIIAsteway MesfinNo ratings yet

- MGMT 222 Ch. V-1Document30 pagesMGMT 222 Ch. V-1Asteway Mesfin100% (1)

- Cash MGT MeklitDocument3 pagesCash MGT MeklitAsteway MesfinNo ratings yet

- Mathschapter FourDocument41 pagesMathschapter FourAsteway MesfinNo ratings yet

- AAU Group AssignmentDocument1 pageAAU Group AssignmentAsteway MesfinNo ratings yet

- Entrepreunership (Section 1) Group ListDocument1 pageEntrepreunership (Section 1) Group ListAsteway MesfinNo ratings yet

- Hypertensive Disorders of Pregnancy 33Document36 pagesHypertensive Disorders of Pregnancy 33Asteway MesfinNo ratings yet

- Shock Syndrome: DR Melkamu BDocument62 pagesShock Syndrome: DR Melkamu BAsteway MesfinNo ratings yet

- Addis Ababa University College of Business and Economics Department of Accounting and FinanceDocument9 pagesAddis Ababa University College of Business and Economics Department of Accounting and FinanceAsteway MesfinNo ratings yet

- Department of Accounting and Finance Risk Management Individual AssignmentDocument6 pagesDepartment of Accounting and Finance Risk Management Individual AssignmentAsteway MesfinNo ratings yet

- Postpartum Hemorrhage (PPH)Document12 pagesPostpartum Hemorrhage (PPH)Asteway MesfinNo ratings yet

- Addis Ababa Universty: NAME Dawit Admasu ID NUMBER BEE/8459/11 Departement Accounting Section 1Document9 pagesAddis Ababa Universty: NAME Dawit Admasu ID NUMBER BEE/8459/11 Departement Accounting Section 1Asteway MesfinNo ratings yet

- Addis Ababa University: College of Business and Economics Department of Accounting and FinanceDocument5 pagesAddis Ababa University: College of Business and Economics Department of Accounting and FinanceAsteway MesfinNo ratings yet

- Postpartum Hemorrhage (PPH)Document12 pagesPostpartum Hemorrhage (PPH)Asteway MesfinNo ratings yet

- Flexible Budgets&Standard Cost SystemDocument27 pagesFlexible Budgets&Standard Cost SystemAsteway Mesfin100% (1)

- Small Bowl SeriesDocument38 pagesSmall Bowl SeriesAsteway MesfinNo ratings yet

- Chapter Iii. Master Budget: An Overall PlanDocument16 pagesChapter Iii. Master Budget: An Overall PlanAsteway MesfinNo ratings yet

- Chapter One: Contrast MediaDocument61 pagesChapter One: Contrast MediaAsteway MesfinNo ratings yet

- Chapter II: Relevant Information & Decision MakingDocument15 pagesChapter II: Relevant Information & Decision MakingAsteway Mesfin100% (4)

- The Menstrual Cycle and Its AbnormalitiesDocument25 pagesThe Menstrual Cycle and Its AbnormalitiesAsteway MesfinNo ratings yet

- Caesarean Delivery: Basliel E M.DDocument13 pagesCaesarean Delivery: Basliel E M.DAsteway MesfinNo ratings yet

- Chapter 8 - Digital MarketingDocument58 pagesChapter 8 - Digital MarketingReno Soank100% (1)

- Designing A Smarter' Mystery Shopping Program: Seven Steps To SuccessDocument10 pagesDesigning A Smarter' Mystery Shopping Program: Seven Steps To SuccessWiena SariNo ratings yet

- Assessment of Inventory Management Practices at The Ethiopian Pharmaceuticals Supply AgencyDocument3 pagesAssessment of Inventory Management Practices at The Ethiopian Pharmaceuticals Supply AgencyshewameneBegashawNo ratings yet

- Consultancy BrochureDocument2 pagesConsultancy BrochureMelisaNo ratings yet

- 43TV-171 Barrier: 09-DCS-M-006-R MTL5546Y BA112Document1 page43TV-171 Barrier: 09-DCS-M-006-R MTL5546Y BA112Epull CoolNo ratings yet

- Karthika Suresh: National Institute of Fashion Technology, Chennai - MFMDocument3 pagesKarthika Suresh: National Institute of Fashion Technology, Chennai - MFMKarthika SureshNo ratings yet

- Anjali Kumari Minor Project FinalDocument48 pagesAnjali Kumari Minor Project Finalanjali kumari - 320No ratings yet

- Agricultural General ReviewerDocument126 pagesAgricultural General ReviewerShieldon BulawanNo ratings yet

- International BusinessDocument66 pagesInternational BusinessHarpal Singh MassanNo ratings yet

- Macroeconomic Assignment 1mba059 Ma Pann Myat PhyuDocument2 pagesMacroeconomic Assignment 1mba059 Ma Pann Myat PhyuCWHNo ratings yet

- Ma - Bep01 - LucioDocument4 pagesMa - Bep01 - LucioGrace SimonNo ratings yet

- E-Leadership Through Strategic AlignmentDocument22 pagesE-Leadership Through Strategic AlignmentAmin Jan FayezNo ratings yet

- MM Marketing Plan ReportDocument14 pagesMM Marketing Plan ReportBhavika GuptaNo ratings yet

- Structure of Tour Operator's BusinessDocument19 pagesStructure of Tour Operator's BusinessShepherd NyaruwataNo ratings yet

- Final Exam Preparation Busd 2027Document22 pagesFinal Exam Preparation Busd 2027Nyko Martin MartinNo ratings yet

- IKEADocument14 pagesIKEADindz SurioNo ratings yet

- Syllabus For RSMDocument2 pagesSyllabus For RSMRajula RamanaKrishnaNo ratings yet

- Full Download Operations Management 13th Edition Stevenson Solutions ManualDocument35 pagesFull Download Operations Management 13th Edition Stevenson Solutions Manualgayoyigachy100% (27)

- RESEARCH (Theoretical Framework)Document4 pagesRESEARCH (Theoretical Framework)Caryl Grace Dela CruzNo ratings yet

- Akhil Vayaliparambath - SAP FI CO - Masters Û Information Technology - 6 Yrs - North of BostonDocument4 pagesAkhil Vayaliparambath - SAP FI CO - Masters Û Information Technology - 6 Yrs - North of BostonPriya MadhuNo ratings yet

- 1 Pfep Introduction 2012Document19 pages1 Pfep Introduction 2012Roberto RocheNo ratings yet

- Cost Classification Theory and Practice QuestionsDocument9 pagesCost Classification Theory and Practice QuestionsBilal Rauf100% (1)

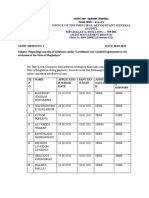

- Office of The Principal Accountant General (AUDIT), Meghalaya, Shillong - 793 001Document11 pagesOffice of The Principal Accountant General (AUDIT), Meghalaya, Shillong - 793 001ronald reaganNo ratings yet

- 20Mnv6 Hollow Bar: Iso Stocked Sizesiso ChartDocument3 pages20Mnv6 Hollow Bar: Iso Stocked Sizesiso ChartretrogradesNo ratings yet

- Chapter 1: Introduction To BPMDocument38 pagesChapter 1: Introduction To BPMjugraj randhawaNo ratings yet

- Marketing and Sales PlanDocument14 pagesMarketing and Sales PlanTharindu LankathilakaNo ratings yet

- CBN Turning InsertsDocument1 pageCBN Turning InsertsknujdloNo ratings yet

- Sourcing Costing of Apparel Products-JoggersDocument10 pagesSourcing Costing of Apparel Products-Joggersraish alamNo ratings yet