Download as pdf or txt

You might also like

- Question bank-BBA 208-Income Tax by Dr. Preeti JindalDocument2 pagesQuestion bank-BBA 208-Income Tax by Dr. Preeti JindalDrPreeti JindalNo ratings yet

- Cpar Tax Problems ReviewerDocument8 pagesCpar Tax Problems ReviewerAnonymous swtSOYwLrMNo ratings yet

- Work Estimate Template Calculates TotalDocument2 pagesWork Estimate Template Calculates TotalKizzy Anne Boatswain CarbonNo ratings yet

- How Landed Cost Management and Accounts Payable Accounting FlowDocument5 pagesHow Landed Cost Management and Accounts Payable Accounting Flowjazharscribd100% (2)

- Cloud KitchensDocument24 pagesCloud KitchensAnonymous tg2wr3Yn100% (3)

- Group 6 Tax AssignmentDocument14 pagesGroup 6 Tax Assignmentdianaowani2No ratings yet

- Changes in Income-Tax - 2020-21 PDFDocument32 pagesChanges in Income-Tax - 2020-21 PDFmir makarim ahsanNo ratings yet

- Taxation Handbook - Tanoy - 2022-2023Document125 pagesTaxation Handbook - Tanoy - 2022-2023twsif777No ratings yet

- Income TaxDocument244 pagesIncome TaxAnil AsNo ratings yet

- Notes in Train Law PDFDocument11 pagesNotes in Train Law PDFJanica Lobas100% (1)

- 6 Activities For Business Structure & TaxationDocument16 pages6 Activities For Business Structure & TaxationDawit TilahunNo ratings yet

- 6 Activities For Business Structure & TaxationDocument16 pages6 Activities For Business Structure & Taxationyabmitiku123No ratings yet

- Income Tax AuthoritiesDocument12 pagesIncome Tax Authoritiesroni286No ratings yet

- Individual Income Tax May 2020Document6 pagesIndividual Income Tax May 2020ziikerr99No ratings yet

- TRAIN LawDocument38 pagesTRAIN LawJorrel BautistaNo ratings yet

- Tax RateDocument10 pagesTax Rateusha chimariyaNo ratings yet

- ACE Advisory - Finance Bill 2020 Highlights PDFDocument6 pagesACE Advisory - Finance Bill 2020 Highlights PDFEmran HossenNo ratings yet

- Train I.ppt - Vers. 10.21.2018Document103 pagesTrain I.ppt - Vers. 10.21.2018Ellard28 saturnoNo ratings yet

- Tax Intro - AmendmentsDocument8 pagesTax Intro - AmendmentsNombs NomNo ratings yet

- Taxation in Uganda: Tax AdministrationDocument9 pagesTaxation in Uganda: Tax AdministrationJeff QueiroNo ratings yet

- TRAIN Law Explained Autosaved From Atty Lea 201215Document140 pagesTRAIN Law Explained Autosaved From Atty Lea 201215'Naif Sampaco PimpingNo ratings yet

- New Tax ReformDocument4 pagesNew Tax ReformEDISON SAGUIRERNo ratings yet

- Prizes - 20% Prizes - 20% Winnings - 20% Winnings - 20%Document4 pagesPrizes - 20% Prizes - 20% Winnings - 20% Winnings - 20%Aly ConcepcionNo ratings yet

- Income TAX CalculationDocument33 pagesIncome TAX CalculationTaharat Ahmed ChowdhuryNo ratings yet

- Tax Reform For Acceleration and Inclusion LawDocument28 pagesTax Reform For Acceleration and Inclusion LawGloriosa SzeNo ratings yet

- Reviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%Document7 pagesReviewer (Tax) : National Internal Revenue Taxes Computation For Mixed Income Earner Who Availed 8%LeeshNo ratings yet

- Amendment Finance Act 2009Document66 pagesAmendment Finance Act 2009Sanjay GuptaNo ratings yet

- TaxDocument19 pagesTaxjhevesNo ratings yet

- 1035 Withholding TaxDocument8 pages1035 Withholding TaxViren GandhiNo ratings yet

- TRAIN I Atty - CasasolaDocument97 pagesTRAIN I Atty - Casasolaleynonlineshop.birNo ratings yet

- Finance Bill 2014Document18 pagesFinance Bill 2014Tanvir Ahmed SyedNo ratings yet

- CA Final Revision MaterialDocument477 pagesCA Final Revision Materialsathish_61288@yahooNo ratings yet

- 4/25/2016 21st MCMC 1Document19 pages4/25/2016 21st MCMC 1ShaniNo ratings yet

- Adobe Scan Oct 11, 2023Document9 pagesAdobe Scan Oct 11, 2023Amir HamzaNo ratings yet

- Answer 1Document5 pagesAnswer 1mayetteNo ratings yet

- CH2 0Document1 pageCH2 0number oneNo ratings yet

- Income Tax Act As Amended by The Finance Act, 2008: SupplementDocument13 pagesIncome Tax Act As Amended by The Finance Act, 2008: SupplementbhavaniNo ratings yet

- Ammendments Made by Finance Bill 2068 in All ActsDocument14 pagesAmmendments Made by Finance Bill 2068 in All ActsNiraj ShresthaNo ratings yet

- Ca Inter Full Book 2Document32 pagesCa Inter Full Book 2Amar SharmaNo ratings yet

- Lec 6 Income Tax RatesDocument4 pagesLec 6 Income Tax Ratesrehan87100% (2)

- Tax Liab. of Ind.Document13 pagesTax Liab. of Ind.Arun SwamiNo ratings yet

- Taxation System of BangladeshDocument21 pagesTaxation System of BangladeshSDNo ratings yet

- LIM2019PROBLEMEXERCISESININCOMETAXATIONandTRAINLAW BDocument11 pagesLIM2019PROBLEMEXERCISESININCOMETAXATIONandTRAINLAW BMark MagnoNo ratings yet

- TRAIN LAW - 3.9.18 - Laguna ChapterDocument408 pagesTRAIN LAW - 3.9.18 - Laguna ChapterDeoshel AlagonNo ratings yet

- Republic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Document24 pagesRepublic Act No. 10963: Tax Reform For Acceleration and Inclusion (Train)Johayra AbbasNo ratings yet

- Excercise 1:: Year Person A (Million) Person B (Million) 1 2 3 4 5 60 60 60 60 60 80 80 60 30 50 Total 300 300Document4 pagesExcercise 1:: Year Person A (Million) Person B (Million) 1 2 3 4 5 60 60 60 60 60 80 80 60 30 50 Total 300 300Quynh NguyenNo ratings yet

- RC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeDocument7 pagesRC Nirc, Ra, Nra-Etb Nra-Netb: Taxpayer Tax Base Source of Taxable IncomeGwyneth GloriaNo ratings yet

- 1997 Tax Code vs. TRAINDocument4 pages1997 Tax Code vs. TRAINCyrine CalagosNo ratings yet

- PH Tax RMC No 19 2015 NoexpDocument1 pagePH Tax RMC No 19 2015 NoexpRodel Ryan YanaNo ratings yet

- Train LawDocument25 pagesTrain LawMariel Mangalino BautistaNo ratings yet

- Income Tax Slab RatesDocument5 pagesIncome Tax Slab RatesBaibhav JauhariNo ratings yet

- Tax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963Document41 pagesTax Reform For Acceleration and Inclusion (Train Law) : Republic Act No. 10963maricrisandem100% (2)

- Amendments - For A.Y. 2011-12Document49 pagesAmendments - For A.Y. 2011-12Arun BansalNo ratings yet

- Income Tax Slabs & Rates For Assessment Year 2014-15Document4 pagesIncome Tax Slabs & Rates For Assessment Year 2014-15ptk_guly3871No ratings yet

- JBDimaampao - Train Law and Tax UpdatesDocument19 pagesJBDimaampao - Train Law and Tax UpdateshlcameroNo ratings yet

- Basic Concepts of TaxationDocument5 pagesBasic Concepts of TaxationMaya SharmaNo ratings yet

- Direct Rax CodeDocument14 pagesDirect Rax CodedivajainNo ratings yet

- Income Tax Ready Reckoner PDFDocument15 pagesIncome Tax Ready Reckoner PDFtushar sharmaNo ratings yet

- Module 07 Introduction To Regular Income TaxDocument21 pagesModule 07 Introduction To Regular Income TaxJeon KookieNo ratings yet

- Tax 605Document5 pagesTax 605NhajNo ratings yet

- Amendments Introduced by TRAINDocument4 pagesAmendments Introduced by TRAINMarc Lester Hernandez-Sta AnaNo ratings yet

- 1040 Exam Prep: Module I: The Form 1040 FormulaFrom Everand1040 Exam Prep: Module I: The Form 1040 FormulaRating: 1 out of 5 stars1/5 (3)

- US Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesFrom EverandUS Taxation of International Startups and Inbound Individuals: For Founders and Executives, Updated for 2023 rulesNo ratings yet

- CH - 3 Ohmae's 5 CsDocument3 pagesCH - 3 Ohmae's 5 CsMd.HasanNo ratings yet

- 02 Strategic ChoiceDocument1 page02 Strategic ChoiceMd.HasanNo ratings yet

- Knowledge Level Icab Class Lecture Sv-1-170508024655Document32 pagesKnowledge Level Icab Class Lecture Sv-1-170508024655Md.HasanNo ratings yet

- Business Law, NotesDocument53 pagesBusiness Law, NotesMd.HasanNo ratings yet

- Income From Interest On SecuritiesDocument2 pagesIncome From Interest On SecuritiesMd.HasanNo ratings yet

- Business and Commercial Law-AsimDocument42 pagesBusiness and Commercial Law-AsimMd.HasanNo ratings yet

- B. Law - by HM ShahriarDocument49 pagesB. Law - by HM ShahriarMd.HasanNo ratings yet

- Income From House PropertiesDocument5 pagesIncome From House PropertiesMd.HasanNo ratings yet

- Advance Payment of TaxDocument2 pagesAdvance Payment of TaxMd.HasanNo ratings yet

- Income From SalaryDocument6 pagesIncome From SalaryMd.HasanNo ratings yet

- Income - Tax - and - VAT - Changes - by - Finance Act - 2021Document73 pagesIncome - Tax - and - VAT - Changes - by - Finance Act - 2021Md.HasanNo ratings yet

- Karnataka Engineering Company Limited (KECL)Document13 pagesKarnataka Engineering Company Limited (KECL)miku hrshNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument30 pagesFinancial Statements, Cash Flow, and TaxesSumitMadnaniNo ratings yet

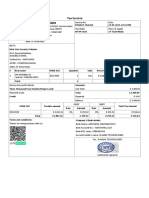

- NH73034207108458 Finance InvoiceDocument1 pageNH73034207108458 Finance InvoiceNaresh kumarNo ratings yet

- Effects of Contraband Trade On Ethiopian Infant IndustriesDocument16 pagesEffects of Contraband Trade On Ethiopian Infant IndustriesUrji Terefe67% (3)

- Mc-Sse 8 Macroeconomics Group V : Fiscal PolicyDocument35 pagesMc-Sse 8 Macroeconomics Group V : Fiscal PolicyMaria Cristina ImportanteNo ratings yet

- SOA009005567079Document2 pagesSOA009005567079Jeevan NJNo ratings yet

- Answers - Business Taxation - Exempt Sales (Chapter 4)Document3 pagesAnswers - Business Taxation - Exempt Sales (Chapter 4)Gino CajoloNo ratings yet

- Conditional Deed of SaleDocument4 pagesConditional Deed of SaleMhel LaurelNo ratings yet

- Ec320 May 2020Document4 pagesEc320 May 2020Potatoes JimNo ratings yet

- RA 10708 - Tax Incentives Management and Transparency Act (TIMTA) - 1Document2 pagesRA 10708 - Tax Incentives Management and Transparency Act (TIMTA) - 1Vince De GuzmanNo ratings yet

- K.Venkat Reddy-Offerletter PDFDocument21 pagesK.Venkat Reddy-Offerletter PDFFrontdoorNo ratings yet

- Manual Instructions Surcharge 80EEBDocument11 pagesManual Instructions Surcharge 80EEBSuprasannaPradhanNo ratings yet

- Political Economy of Trade Ch. 6Document17 pagesPolitical Economy of Trade Ch. 6Athar's PageNo ratings yet

- Siwes Report FinalDocument19 pagesSiwes Report Finalali purityNo ratings yet

- NFJPIA MockboardDocument36 pagesNFJPIA MockboardExequielCamisaCruspero0% (1)

- Peter F. McConaughy Jacqueline W. McConaughy v. United States, 34 F.3d 1066, 4th Cir. (1994)Document6 pagesPeter F. McConaughy Jacqueline W. McConaughy v. United States, 34 F.3d 1066, 4th Cir. (1994)Scribd Government DocsNo ratings yet

- Eacffpc Ethics and Integrity Training ManualDocument48 pagesEacffpc Ethics and Integrity Training ManualKerretts Kimoikong73% (11)

- Test Bank For Corporate Finance A Focused Approach 7th Edition Michael C Ehrhardt Eugene F BrighamDocument24 pagesTest Bank For Corporate Finance A Focused Approach 7th Edition Michael C Ehrhardt Eugene F BrighamDebraWrighterbis100% (43)

- Techniques On Seeking, Screening and Seizing OpportunitiesDocument13 pagesTechniques On Seeking, Screening and Seizing Opportunitiesjenny SalongaNo ratings yet

- 1 Sta. Lucia Realty & Development, Inc. vs. City of Pasig PDFDocument9 pages1 Sta. Lucia Realty & Development, Inc. vs. City of Pasig PDFPS PngnbnNo ratings yet

- KPMG Taxation Handbook - Finance Act 2019Document85 pagesKPMG Taxation Handbook - Finance Act 2019Fatema JidnaNo ratings yet

- Letter of Fiscal: By: Zaqiah Jihan SijayaDocument10 pagesLetter of Fiscal: By: Zaqiah Jihan SijayaZaqiah Jihan SijayaNo ratings yet

- Tax Invoice - BT 2022-23 6262 - 24 - 03 - 23Document1 pageTax Invoice - BT 2022-23 6262 - 24 - 03 - 23karthick manoharanNo ratings yet

- Pi Kit - Iim RaipurDocument48 pagesPi Kit - Iim RaipurpromitiamNo ratings yet

- Pre-Feasibility Study Departmental StoreDocument25 pagesPre-Feasibility Study Departmental StoreMuhammad Mubasher Rafique50% (4)

- Macroeconomics A Contemporary Approach 10th Edition McEachern Test Bank DownloadDocument90 pagesMacroeconomics A Contemporary Approach 10th Edition McEachern Test Bank DownloadDolores Tobias100% (16)