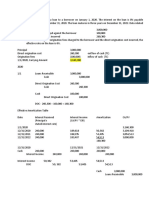

Receivable Financing Sample Problem

Receivable Financing Sample Problem

You might also like

- Application - Regular Income Tax On Individuals and CorporationsDocument8 pagesApplication - Regular Income Tax On Individuals and CorporationsElla Marie Lopez0% (1)

- COSO Model and COCO Model As Control FrameworksDocument18 pagesCOSO Model and COCO Model As Control FrameworksKathleen FrondozoNo ratings yet

- Proof of Cash ProblemDocument3 pagesProof of Cash ProblemKathleen Frondozo71% (7)

- Drill ReceivablesDocument3 pagesDrill ReceivablesGlecel BustrilloNo ratings yet

- Loans Receivable ReviewerDocument3 pagesLoans Receivable ReviewerWilliam TabuenaNo ratings yet

- Practice Set For ACC 111Document6 pagesPractice Set For ACC 111Irahq Yarte TorrejosNo ratings yet

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDocument23 pagesPittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNo ratings yet

- FInancial Accounting and Reporting1C6Document19 pagesFInancial Accounting and Reporting1C6Yen YenNo ratings yet

- Intermediate Accounting I - Cash and Cash EquivalentsDocument2 pagesIntermediate Accounting I - Cash and Cash EquivalentsJoovs Joovho0% (1)

- Chapter 28 - Gross Profit and Retail Method: ANSWER 28-1Document12 pagesChapter 28 - Gross Profit and Retail Method: ANSWER 28-1Cyrus IsanaNo ratings yet

- Proof of CashDocument22 pagesProof of CashYen RabotasoNo ratings yet

- An Entity Reported Current Receivables On December 31Document1 pageAn Entity Reported Current Receivables On December 31pompomNo ratings yet

- Problem 8Document3 pagesProblem 8Coleen Lara SedillesNo ratings yet

- ValixDocument12 pagesValixJESTONI RAMOSNo ratings yet

- IntAcc 1 Reviewer - Module 2 (Theories)Document8 pagesIntAcc 1 Reviewer - Module 2 (Theories)Lizette Janiya SumantingNo ratings yet

- PDFDocument7 pagesPDFAbegail AdoraNo ratings yet

- 33Document2 pages33yes yesnoNo ratings yet

- IA Activity 1Document13 pagesIA Activity 1Sunghoon SsiNo ratings yet

- Chapter 2 5Document36 pagesChapter 2 5Jaztine Danikka GimpayaNo ratings yet

- Chapter 5 Estimation of Doubtful AccountsDocument13 pagesChapter 5 Estimation of Doubtful AccountsAngelie LaxaNo ratings yet

- IA1 - Quiz#1 (Chapter 1 & 2 - CCE & Bank Recon) Theories and ProblemsDocument27 pagesIA1 - Quiz#1 (Chapter 1 & 2 - CCE & Bank Recon) Theories and ProblemsChristabel Lecita PuigNo ratings yet

- Proof of Cash Problem 3-1Document5 pagesProof of Cash Problem 3-1Coleen Lara SedillesNo ratings yet

- Week - 5 Proof of Cash FinalDocument26 pagesWeek - 5 Proof of Cash FinalChengg JainarNo ratings yet

- Pract 1Document159 pagesPract 1bonnyme.00No ratings yet

- ACT1104 Assignment 4Document5 pagesACT1104 Assignment 4cjorillosa2004No ratings yet

- Manaytay, Desiree (Unbalanced) CheckedDocument3 pagesManaytay, Desiree (Unbalanced) CheckedDesiree ManaytayNo ratings yet

- Quiz 1.02 Cash and Cash Equivalents To Loan ImpairmentDocument13 pagesQuiz 1.02 Cash and Cash Equivalents To Loan ImpairmentJohn Lexter MacalberNo ratings yet

- Module 3 - Accounts Receivable Part II - 111702467Document11 pagesModule 3 - Accounts Receivable Part II - 111702467shimizuyumi53No ratings yet

- HW AjeDocument5 pagesHW AjeBenicel Lane M. D. V.No ratings yet

- Problem 1 ReqDocument5 pagesProblem 1 ReqAgent348No ratings yet

- Machete Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument29 pagesChapter 1 Cash and Cash EquivalentsENCARNACION Princess MarieNo ratings yet

- Term Exam 2edited Answer KeyDocument10 pagesTerm Exam 2edited Answer KeyPRINCESS HONEYLET SIGESMUNDONo ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Cash and Cash EquivalentsDocument7 pagesCash and Cash EquivalentsDianna DayawonNo ratings yet

- Martinez, Althea E. Abm 12-1 (Accounting 2)Document13 pagesMartinez, Althea E. Abm 12-1 (Accounting 2)Althea Escarpe MartinezNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- Cash and Cash Equivalents (Theory and Problem)Document9 pagesCash and Cash Equivalents (Theory and Problem)Kim Cristian MaañoNo ratings yet

- IntAcc Reviewer - Module 2 (Problems)Document26 pagesIntAcc Reviewer - Module 2 (Problems)Lizette Janiya SumantingNo ratings yet

- Loans ReceivableDocument22 pagesLoans ReceivableJendall SisonNo ratings yet

- Far Quiz 2Document13 pagesFar Quiz 2Shiela Jane CrismundoNo ratings yet

- ACC 101 - NR Assignment SolutionDocument6 pagesACC 101 - NR Assignment SolutionAdyangNo ratings yet

- (03A) AR NR Quiz ANSWER KEYDocument8 pages(03A) AR NR Quiz ANSWER KEYKhai Ed PabelicoNo ratings yet

- National Bank Grants A 10Document2 pagesNational Bank Grants A 10George PascualNo ratings yet

- 6-4 Gullible Company Req 1Document2 pages6-4 Gullible Company Req 1mercyvienhoNo ratings yet

- Mythical Company Provided The Following Transactions:: University - Year 2 AccountingDocument2 pagesMythical Company Provided The Following Transactions:: University - Year 2 Accountingcollegestudent2000No ratings yet

- BANK RECON and PROOF OF CASHDocument2 pagesBANK RECON and PROOF OF CASHJay-an AntipoloNo ratings yet

- Bleak Company Requirement A Debit Credit Requirement BDocument2 pagesBleak Company Requirement A Debit Credit Requirement BAnonn100% (1)

- Chapter 5 (Estimation of Doubtful Accounts)Document8 pagesChapter 5 (Estimation of Doubtful Accounts)Joan LeonorNo ratings yet

- Test Bank Notes ReceivableDocument5 pagesTest Bank Notes ReceivableErrold john DulatreNo ratings yet

- Cash EquivalentDocument9 pagesCash EquivalentMaria G. BernardinoNo ratings yet

- Cash Priority ProgramDocument1 pageCash Priority Programyela garcia0% (1)

- Cash and Cash EquivalentsDocument408 pagesCash and Cash EquivalentsJanea ArinyaNo ratings yet

- Affectionate CompanyDocument1 pageAffectionate CompanyAnonnNo ratings yet

- Module 2d Loan ReceivableDocument24 pagesModule 2d Loan ReceivableChen HaoNo ratings yet

- Chapter08 Inventory Cost Other Basis Student Copy LectureDocument9 pagesChapter08 Inventory Cost Other Basis Student Copy LectureAngelo Christian B. OreñadaNo ratings yet

- Quiz Notes and Loans Receivable SY 2022 2023 SolutionDocument4 pagesQuiz Notes and Loans Receivable SY 2022 2023 Solutionreagan blaireNo ratings yet

- Walleye Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageWalleye Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- AE 121 Prelim Quiz 1 THEORIES (10 Items X 2 Points 20 POINTS)Document10 pagesAE 121 Prelim Quiz 1 THEORIES (10 Items X 2 Points 20 POINTS)Eryn GabrielleNo ratings yet

- MidtermsDocument8 pagesMidtermsRhea BadanaNo ratings yet

- Answer Key Far Assessment Questionairre 1Document22 pagesAnswer Key Far Assessment Questionairre 1Johnfree VallinasNo ratings yet

- INTERMEDIATE ACCOUNTING 1 EditedDocument18 pagesINTERMEDIATE ACCOUNTING 1 EditedApril Mae LomboyNo ratings yet

- Audit Planning Approaches, Planning Process, and Preliminary Survey ComponentsDocument34 pagesAudit Planning Approaches, Planning Process, and Preliminary Survey ComponentsKathleen FrondozoNo ratings yet

- PPE Sample ProblemsDocument5 pagesPPE Sample ProblemsKathleen FrondozoNo ratings yet

- Testing As A Strategy, Types of Testing, Testing Techniques, and The Processes Conducted in The Testing ProcessDocument12 pagesTesting As A Strategy, Types of Testing, Testing Techniques, and The Processes Conducted in The Testing ProcessKathleen FrondozoNo ratings yet

- Loan Receivable ProblemsDocument6 pagesLoan Receivable ProblemsKathleen Frondozo100% (1)

- QUIZ No. 1Document6 pagesQUIZ No. 1Kathleen FrondozoNo ratings yet

- Activity 4 Multiple ChoiceDocument5 pagesActivity 4 Multiple ChoiceKathleen FrondozoNo ratings yet

- Investment Property Sample ProblemsDocument3 pagesInvestment Property Sample ProblemsKathleen Frondozo100% (1)

- TD29T2223-41786 DSCDocument4 pagesTD29T2223-41786 DSCBalaram SatapathyNo ratings yet

- EntrepreneurshipDocument66 pagesEntrepreneurshipMary Joy Estrologo DescalsotaNo ratings yet

- How To Make FriendsDocument1 pageHow To Make FriendsJust Chill100% (1)

- Central Place TheoryDocument16 pagesCentral Place TheoryajNo ratings yet

- Palo Alto Networks Cortex XDR Prevention and Deployment (Z-Library)Document595 pagesPalo Alto Networks Cortex XDR Prevention and Deployment (Z-Library)alfredo.carracedoNo ratings yet

- 04 Impact of CRM On Customer Satisfaction and Customer Loyalty - PHD ThesisDocument190 pages04 Impact of CRM On Customer Satisfaction and Customer Loyalty - PHD ThesisWelly MahardhikaNo ratings yet

- IWC203 Introduction To MacroeconomicsDocument3 pagesIWC203 Introduction To MacroeconomicsToby ChungNo ratings yet

- A Report On Strategic Management of National Bank LimitedDocument36 pagesA Report On Strategic Management of National Bank LimitedNabila AhmadNo ratings yet

- WFH Internet Upgrade Memo EmblemHealth ACPNYDocument2 pagesWFH Internet Upgrade Memo EmblemHealth ACPNYJoyce AnnNo ratings yet

- In A Bind Peak Sealing Technologies' Product Line Extension DilemmaDocument2 pagesIn A Bind Peak Sealing Technologies' Product Line Extension DilemmaAryan GargNo ratings yet

- Tax Estate CreditableDocument2 pagesTax Estate Creditablepatburner1108No ratings yet

- Atithi Devo Bhavah: Success or Failure in IndiaDocument19 pagesAtithi Devo Bhavah: Success or Failure in IndiaAmita AgrawalNo ratings yet

- Kassel Resume May 2021Document1 pageKassel Resume May 2021api-548693113No ratings yet

- Assignment On Permanent Settlement ActDocument3 pagesAssignment On Permanent Settlement ActAhnaf AliNo ratings yet

- Operations and Supply Chain Management The Core 4th Edition Jacobs Chase Solution ManualDocument26 pagesOperations and Supply Chain Management The Core 4th Edition Jacobs Chase Solution Manualkaren100% (29)

- Unilever Annual Report and Accounts 2017Document187 pagesUnilever Annual Report and Accounts 2017Anonymous BoGI0PwvqvNo ratings yet

- Transforming Public Sector BanksDocument21 pagesTransforming Public Sector BanksMansi VyasNo ratings yet

- Chapter 2 ActivityDocument10 pagesChapter 2 ActivityBELARMINO LOUIE A.No ratings yet

- Compu 1Document4 pagesCompu 1SK SchreaveNo ratings yet

- CHAPTER 25 - Borrowing CostsDocument6 pagesCHAPTER 25 - Borrowing CostsRosee D.No ratings yet

- Solved Jennifer Is Single and Has The Following Income and ExpensesDocument1 pageSolved Jennifer Is Single and Has The Following Income and ExpensesAnbu jaromiaNo ratings yet

- Wa0000Document4 pagesWa0000donimrlyNo ratings yet

- Alfa Laval Repair For Aalborg BoilersDocument2 pagesAlfa Laval Repair For Aalborg Boilersmichall123No ratings yet

- 10 Best Trading Chart Patterns PDF GuideDocument43 pages10 Best Trading Chart Patterns PDF Guidemcjn.commercialNo ratings yet

- 3i Research Paper Noriels GroupDocument76 pages3i Research Paper Noriels GroupMICHELLE LENDESNo ratings yet

- Assignment - Ankit Singh BBA (P) 2Document19 pagesAssignment - Ankit Singh BBA (P) 2Rahul SinghNo ratings yet

- Joint Product by Product QuestionsDocument7 pagesJoint Product by Product QuestionsShibin XavierNo ratings yet

- CH 21Document144 pagesCH 21Indah PNo ratings yet

- Question: Discuss The Causes of Market Failure and How The Government Can Intervene To Correct Market Failure?Document4 pagesQuestion: Discuss The Causes of Market Failure and How The Government Can Intervene To Correct Market Failure?Dafrosa HonorNo ratings yet

Download as docx, pdf, or txt

You might also like

- Application - Regular Income Tax On Individuals and CorporationsDocument8 pagesApplication - Regular Income Tax On Individuals and CorporationsElla Marie Lopez0% (1)

- COSO Model and COCO Model As Control FrameworksDocument18 pagesCOSO Model and COCO Model As Control FrameworksKathleen FrondozoNo ratings yet

- Proof of Cash ProblemDocument3 pagesProof of Cash ProblemKathleen Frondozo71% (7)

- Drill ReceivablesDocument3 pagesDrill ReceivablesGlecel BustrilloNo ratings yet

- Loans Receivable ReviewerDocument3 pagesLoans Receivable ReviewerWilliam TabuenaNo ratings yet

- Practice Set For ACC 111Document6 pagesPractice Set For ACC 111Irahq Yarte TorrejosNo ratings yet

- Pittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditDocument23 pagesPittance Company Requirement: Prepare Journal Entries To Record The Transactions Debit CreditAnonnNo ratings yet

- FInancial Accounting and Reporting1C6Document19 pagesFInancial Accounting and Reporting1C6Yen YenNo ratings yet

- Intermediate Accounting I - Cash and Cash EquivalentsDocument2 pagesIntermediate Accounting I - Cash and Cash EquivalentsJoovs Joovho0% (1)

- Chapter 28 - Gross Profit and Retail Method: ANSWER 28-1Document12 pagesChapter 28 - Gross Profit and Retail Method: ANSWER 28-1Cyrus IsanaNo ratings yet

- Proof of CashDocument22 pagesProof of CashYen RabotasoNo ratings yet

- An Entity Reported Current Receivables On December 31Document1 pageAn Entity Reported Current Receivables On December 31pompomNo ratings yet

- Problem 8Document3 pagesProblem 8Coleen Lara SedillesNo ratings yet

- ValixDocument12 pagesValixJESTONI RAMOSNo ratings yet

- IntAcc 1 Reviewer - Module 2 (Theories)Document8 pagesIntAcc 1 Reviewer - Module 2 (Theories)Lizette Janiya SumantingNo ratings yet

- PDFDocument7 pagesPDFAbegail AdoraNo ratings yet

- 33Document2 pages33yes yesnoNo ratings yet

- IA Activity 1Document13 pagesIA Activity 1Sunghoon SsiNo ratings yet

- Chapter 2 5Document36 pagesChapter 2 5Jaztine Danikka GimpayaNo ratings yet

- Chapter 5 Estimation of Doubtful AccountsDocument13 pagesChapter 5 Estimation of Doubtful AccountsAngelie LaxaNo ratings yet

- IA1 - Quiz#1 (Chapter 1 & 2 - CCE & Bank Recon) Theories and ProblemsDocument27 pagesIA1 - Quiz#1 (Chapter 1 & 2 - CCE & Bank Recon) Theories and ProblemsChristabel Lecita PuigNo ratings yet

- Proof of Cash Problem 3-1Document5 pagesProof of Cash Problem 3-1Coleen Lara SedillesNo ratings yet

- Week - 5 Proof of Cash FinalDocument26 pagesWeek - 5 Proof of Cash FinalChengg JainarNo ratings yet

- Pract 1Document159 pagesPract 1bonnyme.00No ratings yet

- ACT1104 Assignment 4Document5 pagesACT1104 Assignment 4cjorillosa2004No ratings yet

- Manaytay, Desiree (Unbalanced) CheckedDocument3 pagesManaytay, Desiree (Unbalanced) CheckedDesiree ManaytayNo ratings yet

- Quiz 1.02 Cash and Cash Equivalents To Loan ImpairmentDocument13 pagesQuiz 1.02 Cash and Cash Equivalents To Loan ImpairmentJohn Lexter MacalberNo ratings yet

- Module 3 - Accounts Receivable Part II - 111702467Document11 pagesModule 3 - Accounts Receivable Part II - 111702467shimizuyumi53No ratings yet

- HW AjeDocument5 pagesHW AjeBenicel Lane M. D. V.No ratings yet

- Problem 1 ReqDocument5 pagesProblem 1 ReqAgent348No ratings yet

- Machete Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageMachete Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Chapter 1 Cash and Cash EquivalentsDocument29 pagesChapter 1 Cash and Cash EquivalentsENCARNACION Princess MarieNo ratings yet

- Term Exam 2edited Answer KeyDocument10 pagesTerm Exam 2edited Answer KeyPRINCESS HONEYLET SIGESMUNDONo ratings yet

- Inventories&Inventoryestimation GAPASINAODocument25 pagesInventories&Inventoryestimation GAPASINAOGerly GapasinaoNo ratings yet

- Cash and Cash EquivalentsDocument7 pagesCash and Cash EquivalentsDianna DayawonNo ratings yet

- Martinez, Althea E. Abm 12-1 (Accounting 2)Document13 pagesMartinez, Althea E. Abm 12-1 (Accounting 2)Althea Escarpe MartinezNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Proof of Cash Syria CompanyDocument4 pagesProof of Cash Syria CompanyCJ alandy100% (1)

- Cash and Cash Equivalents (Theory and Problem)Document9 pagesCash and Cash Equivalents (Theory and Problem)Kim Cristian MaañoNo ratings yet

- IntAcc Reviewer - Module 2 (Problems)Document26 pagesIntAcc Reviewer - Module 2 (Problems)Lizette Janiya SumantingNo ratings yet

- Loans ReceivableDocument22 pagesLoans ReceivableJendall SisonNo ratings yet

- Far Quiz 2Document13 pagesFar Quiz 2Shiela Jane CrismundoNo ratings yet

- ACC 101 - NR Assignment SolutionDocument6 pagesACC 101 - NR Assignment SolutionAdyangNo ratings yet

- (03A) AR NR Quiz ANSWER KEYDocument8 pages(03A) AR NR Quiz ANSWER KEYKhai Ed PabelicoNo ratings yet

- National Bank Grants A 10Document2 pagesNational Bank Grants A 10George PascualNo ratings yet

- 6-4 Gullible Company Req 1Document2 pages6-4 Gullible Company Req 1mercyvienhoNo ratings yet

- Mythical Company Provided The Following Transactions:: University - Year 2 AccountingDocument2 pagesMythical Company Provided The Following Transactions:: University - Year 2 Accountingcollegestudent2000No ratings yet

- BANK RECON and PROOF OF CASHDocument2 pagesBANK RECON and PROOF OF CASHJay-an AntipoloNo ratings yet

- Bleak Company Requirement A Debit Credit Requirement BDocument2 pagesBleak Company Requirement A Debit Credit Requirement BAnonn100% (1)

- Chapter 5 (Estimation of Doubtful Accounts)Document8 pagesChapter 5 (Estimation of Doubtful Accounts)Joan LeonorNo ratings yet

- Test Bank Notes ReceivableDocument5 pagesTest Bank Notes ReceivableErrold john DulatreNo ratings yet

- Cash EquivalentDocument9 pagesCash EquivalentMaria G. BernardinoNo ratings yet

- Cash Priority ProgramDocument1 pageCash Priority Programyela garcia0% (1)

- Cash and Cash EquivalentsDocument408 pagesCash and Cash EquivalentsJanea ArinyaNo ratings yet

- Affectionate CompanyDocument1 pageAffectionate CompanyAnonnNo ratings yet

- Module 2d Loan ReceivableDocument24 pagesModule 2d Loan ReceivableChen HaoNo ratings yet

- Chapter08 Inventory Cost Other Basis Student Copy LectureDocument9 pagesChapter08 Inventory Cost Other Basis Student Copy LectureAngelo Christian B. OreñadaNo ratings yet

- Quiz Notes and Loans Receivable SY 2022 2023 SolutionDocument4 pagesQuiz Notes and Loans Receivable SY 2022 2023 Solutionreagan blaireNo ratings yet

- Walleye Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageWalleye Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- AE 121 Prelim Quiz 1 THEORIES (10 Items X 2 Points 20 POINTS)Document10 pagesAE 121 Prelim Quiz 1 THEORIES (10 Items X 2 Points 20 POINTS)Eryn GabrielleNo ratings yet

- MidtermsDocument8 pagesMidtermsRhea BadanaNo ratings yet

- Answer Key Far Assessment Questionairre 1Document22 pagesAnswer Key Far Assessment Questionairre 1Johnfree VallinasNo ratings yet

- INTERMEDIATE ACCOUNTING 1 EditedDocument18 pagesINTERMEDIATE ACCOUNTING 1 EditedApril Mae LomboyNo ratings yet

- Audit Planning Approaches, Planning Process, and Preliminary Survey ComponentsDocument34 pagesAudit Planning Approaches, Planning Process, and Preliminary Survey ComponentsKathleen FrondozoNo ratings yet

- PPE Sample ProblemsDocument5 pagesPPE Sample ProblemsKathleen FrondozoNo ratings yet

- Testing As A Strategy, Types of Testing, Testing Techniques, and The Processes Conducted in The Testing ProcessDocument12 pagesTesting As A Strategy, Types of Testing, Testing Techniques, and The Processes Conducted in The Testing ProcessKathleen FrondozoNo ratings yet

- Loan Receivable ProblemsDocument6 pagesLoan Receivable ProblemsKathleen Frondozo100% (1)

- QUIZ No. 1Document6 pagesQUIZ No. 1Kathleen FrondozoNo ratings yet

- Activity 4 Multiple ChoiceDocument5 pagesActivity 4 Multiple ChoiceKathleen FrondozoNo ratings yet

- Investment Property Sample ProblemsDocument3 pagesInvestment Property Sample ProblemsKathleen Frondozo100% (1)

- TD29T2223-41786 DSCDocument4 pagesTD29T2223-41786 DSCBalaram SatapathyNo ratings yet

- EntrepreneurshipDocument66 pagesEntrepreneurshipMary Joy Estrologo DescalsotaNo ratings yet

- How To Make FriendsDocument1 pageHow To Make FriendsJust Chill100% (1)

- Central Place TheoryDocument16 pagesCentral Place TheoryajNo ratings yet

- Palo Alto Networks Cortex XDR Prevention and Deployment (Z-Library)Document595 pagesPalo Alto Networks Cortex XDR Prevention and Deployment (Z-Library)alfredo.carracedoNo ratings yet

- 04 Impact of CRM On Customer Satisfaction and Customer Loyalty - PHD ThesisDocument190 pages04 Impact of CRM On Customer Satisfaction and Customer Loyalty - PHD ThesisWelly MahardhikaNo ratings yet

- IWC203 Introduction To MacroeconomicsDocument3 pagesIWC203 Introduction To MacroeconomicsToby ChungNo ratings yet

- A Report On Strategic Management of National Bank LimitedDocument36 pagesA Report On Strategic Management of National Bank LimitedNabila AhmadNo ratings yet

- WFH Internet Upgrade Memo EmblemHealth ACPNYDocument2 pagesWFH Internet Upgrade Memo EmblemHealth ACPNYJoyce AnnNo ratings yet

- In A Bind Peak Sealing Technologies' Product Line Extension DilemmaDocument2 pagesIn A Bind Peak Sealing Technologies' Product Line Extension DilemmaAryan GargNo ratings yet

- Tax Estate CreditableDocument2 pagesTax Estate Creditablepatburner1108No ratings yet

- Atithi Devo Bhavah: Success or Failure in IndiaDocument19 pagesAtithi Devo Bhavah: Success or Failure in IndiaAmita AgrawalNo ratings yet

- Kassel Resume May 2021Document1 pageKassel Resume May 2021api-548693113No ratings yet

- Assignment On Permanent Settlement ActDocument3 pagesAssignment On Permanent Settlement ActAhnaf AliNo ratings yet

- Operations and Supply Chain Management The Core 4th Edition Jacobs Chase Solution ManualDocument26 pagesOperations and Supply Chain Management The Core 4th Edition Jacobs Chase Solution Manualkaren100% (29)

- Unilever Annual Report and Accounts 2017Document187 pagesUnilever Annual Report and Accounts 2017Anonymous BoGI0PwvqvNo ratings yet

- Transforming Public Sector BanksDocument21 pagesTransforming Public Sector BanksMansi VyasNo ratings yet

- Chapter 2 ActivityDocument10 pagesChapter 2 ActivityBELARMINO LOUIE A.No ratings yet

- Compu 1Document4 pagesCompu 1SK SchreaveNo ratings yet

- CHAPTER 25 - Borrowing CostsDocument6 pagesCHAPTER 25 - Borrowing CostsRosee D.No ratings yet

- Solved Jennifer Is Single and Has The Following Income and ExpensesDocument1 pageSolved Jennifer Is Single and Has The Following Income and ExpensesAnbu jaromiaNo ratings yet

- Wa0000Document4 pagesWa0000donimrlyNo ratings yet

- Alfa Laval Repair For Aalborg BoilersDocument2 pagesAlfa Laval Repair For Aalborg Boilersmichall123No ratings yet

- 10 Best Trading Chart Patterns PDF GuideDocument43 pages10 Best Trading Chart Patterns PDF Guidemcjn.commercialNo ratings yet

- 3i Research Paper Noriels GroupDocument76 pages3i Research Paper Noriels GroupMICHELLE LENDESNo ratings yet

- Assignment - Ankit Singh BBA (P) 2Document19 pagesAssignment - Ankit Singh BBA (P) 2Rahul SinghNo ratings yet

- Joint Product by Product QuestionsDocument7 pagesJoint Product by Product QuestionsShibin XavierNo ratings yet

- CH 21Document144 pagesCH 21Indah PNo ratings yet

- Question: Discuss The Causes of Market Failure and How The Government Can Intervene To Correct Market Failure?Document4 pagesQuestion: Discuss The Causes of Market Failure and How The Government Can Intervene To Correct Market Failure?Dafrosa HonorNo ratings yet